Global Surgical Robots Market

Market Size in USD Billion

CAGR :

%

USD

6.12 Billion

USD

23.02 Billion

2024

2032

USD

6.12 Billion

USD

23.02 Billion

2024

2032

| 2025 –2032 | |

| USD 6.12 Billion | |

| USD 23.02 Billion | |

| % | |

|

Surgical Robots Market Size

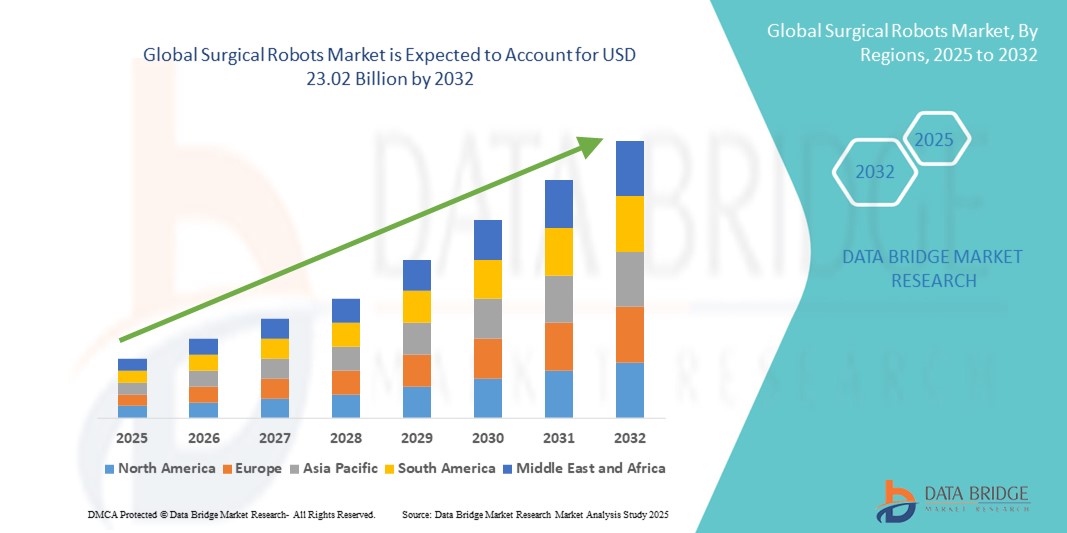

- The global surgical robots market size was valued at USD 6.12 billion in 2024 and is expected to reach USD 23.02 billion by 2032, at a CAGR of 18.00% during the forecast period

- The market growth is largely driven by the increasing adoption of minimally invasive surgical procedures, supported by advancements in robotic technology that offer greater precision, control, and improved patient outcomes

- Furthermore, rising demand for automation in the operating room, along with growing investments in healthcare infrastructure and surgeon training, is positioning surgical robots as a critical component of next-generation surgical care. These converging factors are accelerating the adoption of surgical robotic systems, thereby significantly boosting the industry’s growth

Surgical Robots Market Analysis

- Surgical robots, which enable high-precision and minimally invasive procedures through robotic-assisted platforms, are becoming increasingly essential in modern operating rooms across both hospitals and ambulatory surgical centers due to their ability to enhance surgical accuracy, reduce recovery times, and improve patient outcomes

- The rising demand for surgical robots is primarily fueled by growing volumes of complex surgical procedures, a global shift toward minimally invasive surgeries, and continuous technological advancements in robotic instrumentation, AI integration, and real-time imaging

- North America dominated the surgical robots market with the largest revenue share of 51.8% in 2024, driven by advanced healthcare infrastructure, rapid adoption of innovative surgical technologies, and strong reimbursement frameworks, with the U.S. leading due to high utilization rates of robotic systems in specialties such as urology, gynecology, and general surgery

- Asia-Pacific is expected to be the fastest growing region in the surgical robots market during the forecast period due to expanding healthcare investments, increasing surgeon training programs, and rising demand for high-tech surgical solutions across countries such as China, India, and Japan

- The general surgery segment dominated the surgical robots market with a market share of 39% in 2024, owing to its wide range of applications and increased adoption of robotic-assisted techniques in procedures such as hernia repair, colorectal surgeries, and bariatric operations

Report Scope and Surgical Robots Market Segmentation

|

Attributes |

Surgical Robots Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Surgical Robots Market Trends

AI-Driven Precision and Integration with Imaging & Navigation Systems

- A significant and rapidly advancing trend in the global surgical robots market is the integration of artificial intelligence (AI) and advanced imaging technologies such as real-time 3D visualization, intraoperative navigation, and augmented reality. This fusion is revolutionizing surgical precision, improving outcomes, and enabling more complex minimally invasive procedures across specialties

- For instance, Intuitive Surgical’s da Vinci systems increasingly incorporate AI-driven analytics and image-guided tools to assist surgeons with enhanced decision-making and instrument control. Similarly, Medtronic’s Hugo™ RAS platform leverages AI algorithms for improved workflow automation and robotic arm coordination

- AI integration enables predictive analytics, real-time feedback, and machine learning-based motion scaling that helps reduce hand tremors and optimize surgical performance. For instance, CMR Surgical’s Versius system is designed with modularity and data-capturing capabilities to continuously refine surgeon techniques using AI insights

- The combination of robotics with intraoperative imaging allows for dynamic adjustments during surgery, leading to improved anatomical targeting and reduced risks. Companies such as Zimmer Biomet and Stryker are enhancing their systems with AI-enabled navigation platforms for orthopedic procedures such as knee and hip replacements

- This trend toward smart, AI-assisted surgical systems is redefining the expectations of safety, accuracy, and personalization in the operating room. As a result, startups and major players are investing heavily in R&D to create interoperable robotic platforms that integrate seamlessly with hospital IT infrastructure and data analytics systems

- The demand for surgical robots equipped with intelligent guidance systems is growing steadily across both developed and emerging markets, as healthcare providers increasingly prioritize surgical efficiency, precision, and patient recovery outcomes

Surgical Robots Market Dynamics

Driver

Rising Demand for Minimally Invasive Procedures and Technological Advancements

- The growing global preference for minimally invasive surgeries (MIS), which offer reduced trauma, shorter hospital stays, and quicker recovery, is a primary driver accelerating the demand for surgical robots

- For instance, in February 2024, Johnson & Johnson’s Ottava robotic platform entered advanced trials, offering a six-arm configuration and integrated imaging, aimed at expanding the scope of robotic procedures in general and thoracic surgeries. Such innovation-driven strategies by key players are expected to bolster market expansion over the forecast period

- Surgical robots offer enhanced dexterity, 3D visualization, and tremor filtration, making them ideal for complex procedures across urology, gynecology, orthopedics, and cardiology

- The increasing adoption of robotic systems in ambulatory surgical centers and community hospitals, driven by technological miniaturization and modular platforms, is expanding accessibility beyond top-tier institutions

- In addition, the rising number of surgeon training programs, favorable reimbursement policies in developed regions, and growing clinical evidence supporting improved outcomes with robotic-assisted surgeries are further driving market growth

Restraint/Challenge

High System Costs and Regulatory Barriers

- The substantial upfront investment required for surgical robotic systems remains a key barrier to adoption, especially for small or mid-sized hospitals and facilities in price-sensitive markets

- For instance, in March 2024, the U.S. FDA issued a hold on the review process for a next-generation robotic system by a U.S.-based startup due to insufficient long-term clinical data, delaying the company’s entry into the market and highlighting the rigorous standards required for approval

- Alongside acquisition costs, recurring expenses for maintenance, instruments, and software licensing contribute to a high total cost of ownership, deterring some healthcare providers from early adoption

- In addition, navigating complex regulatory pathways for robotic surgical systems poses challenges for market entrants. Regulatory approvals often require extensive clinical trials to demonstrate safety and efficacy, which can prolong time-to-market and inflate development costs

- Newer robotic platforms from companies such as Asensus Surgical or Medicaroid face competitive pressures and compliance hurdles as they expand globally, particularly in regions with stringent regulatory frameworks such as the U.S., EU, and Japan

- To overcome these challenges, key players are focusing on developing cost-effective, compact, and modular robotic systems, alongside expanding value-based healthcare models and flexible financing options

- Strengthening regulatory collaboration, increasing physician training, and demonstrating long-term clinical and economic benefits will be critical to achieving sustained market growth in the coming years

Surgical Robots Market Scope

The market is segmented on the basis of product type, brand, application, and end-user.

- By Product Type

On the basis of product type, the surgical robots market is segmented into instruments, robotic systems, accessories, and services. The instruments segment dominated the market with the largest market revenue share in 2024, owing to their recurrent use in procedures and the need for frequent replacement after specific usage cycles. Instruments such as robotic arms, surgical tools, and end-effectors are essential for precision and are replaced more regularly than the robotic systems themselves, contributing significantly to recurring revenues.

The robotic systems segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by increasing installations of advanced robotic platforms across hospitals and surgical centers. Technological advancements such as modular systems, AI integration, and improved ergonomics are attracting new investments, particularly in emerging healthcare markets aiming to modernize their surgical infrastructure.

- By Brand

On the basis of brand, the surgical robots market is segmented into da Vinci Surgical System, CyberKnife, Renaissance, ARTAS, ROSA, and others. The da Vinci Surgical System held the largest market share in 2024 due to its pioneering role and extensive global adoption across specialties including urology, gynecology, and general surgery. Its proven clinical outcomes, broad regulatory approvals, and continuous upgrades have solidified its leadership position in the robotic surgery space.

The ROSA system is projected to experience the highest growth rate over the forecast period, driven by its specialized applications in neurosurgery and orthopedic procedures. Its ability to integrate with imaging and navigation tools enhances precision and is gaining traction among orthopedic and brain surgeons seeking less invasive, robot-assisted techniques.

- By Application

On the basis of application, the surgical robots market is segmented into general surgery, urological, gynecological, gastrointestinal, radical prostatectomy, cardiothoracic surgery, colorectal surgery, radiotherapy, and others. The general surgery segment dominated the market with the highest share of 39% in 2024, supported by the broad adoption of robotic assistance in laparoscopic procedures such as hernia repair and bariatric surgeries. The flexibility of surgical robots across multiple general procedures has made them an essential part of modern operating rooms.

The urological segment is expected to grow at the fastest pace from 2025 to 2032, driven by the high volume of prostatectomies and kidney surgeries performed with robotic systems. Robotic surgery offers enhanced visualization and dexterity in confined anatomical spaces, making it highly suited for delicate urological interventions.

- By End-User

On the basis of end-user, the surgical robots market is segmented into clinics, hospitals, ambulatory care centers, and others. The hospitals segment accounted for the largest revenue share in 2024, driven by higher adoption capacity, availability of skilled professionals, and access to capital for robotic infrastructure. Hospitals also serve as training centers and conduct most high-complexity procedures, solidifying their dominance in the market.

The ambulatory care centers segment is projected to register the fastest growth from 2025 to 2032. This is due to the rise of outpatient minimally invasive surgeries and the increasing deployment of compact, cost-effective robotic systems suitable for same-day surgical settings. Enhanced recovery protocols and lower procedural costs are accelerating the shift of robotic procedures to these facilities.

Surgical Robots Market Regional Analysis

- North America dominated the surgical robots market with the largest revenue share of 51.8% in 2024, driven by advanced healthcare infrastructure, rapid adoption of innovative surgical technologies, and strong reimbursement frameworks, with the U.S. leading due to high utilization rates of robotic systems in specialties such as urology, gynecology, and general surgery

- Hospitals and surgical centers in the region increasingly rely on robotic systems to perform complex procedures with enhanced precision and reduced recovery times, particularly in specialties such as urology, gynecology, and general surgery

- The strong presence of key market players, robust clinical research activity, and growing investments in AI-integrated surgical solutions continue to accelerate adoption, positioning North America as a global leader in the robotic-assisted surgery landscape

U.S. Surgical Robots Market Insight

The U.S. surgical robots market captured the largest revenue share of 87% in 2024 within North America, driven by the widespread adoption of robotic-assisted procedures in hospitals and advanced surgical centers. The country's strong focus on minimally invasive surgeries, backed by favorable reimbursement structures and rapid technological innovation, continues to accelerate demand. Leading manufacturers such as Intuitive Surgical, Stryker, and Medtronic maintain significant influence, offering cutting-edge robotic systems across multiple specialties. Moreover, growing investment in AI-integrated surgical platforms and the expansion of training programs further reinforce the U.S. as a global leader in the surgical robotics domain.

Europe Surgical Robots Market Insight

The Europe surgical robots market is projected to grow at a substantial CAGR throughout the forecast period, fueled by the rising prevalence of chronic conditions, the increasing number of complex surgeries, and robust healthcare infrastructure. Countries across the region are embracing robotic systems to enhance surgical precision and improve patient outcomes. EU-wide initiatives to modernize hospitals and rising demand for minimally invasive surgeries are boosting adoption. In addition, collaborations between medtech firms and academic institutions are fostering innovation and encouraging the broader implementation of robotic systems across general and specialized surgeries.

U.K. Surgical Robots Market Insight

The U.K. surgical robots market is expected to grow at a noteworthy CAGR during the forecast period, propelled by the increasing shift toward minimally invasive techniques and the modernization of National Health Service (NHS) surgical facilities. The government’s investment in digital healthcare infrastructure and the presence of skilled surgical professionals support the integration of robotic systems in urology, gynecology, and colorectal procedures. In addition, growing awareness among patients and favorable clinical outcomes are driving demand across both public and private hospitals.

Germany Surgical Robots Market Insight

The Germany surgical robots market is poised to expand at a considerable CAGR over the forecast period, driven by high healthcare expenditure, strong regulatory support for medical technology innovation, and a growing emphasis on surgical efficiency. Germany’s technologically advanced hospitals are increasingly adopting robotic systems for orthopedic, cardiac, and general surgery. Strategic partnerships between healthcare providers and medtech companies are fostering the development of localized robotic solutions, while patient demand for faster recovery and lower post-operative complications fuels continued growth.

Asia-Pacific Surgical Robots Market Insight

The Asia-Pacific surgical robots market is projected to grow at the fastest CAGR of 25.3% during the forecast period of 2025 to 2032, supported by the rising healthcare expenditure, urbanization, and increasing adoption of smart healthcare technologies in countries such as China, Japan, and India. Government initiatives promoting the digitalization of healthcare and rapid expansion of hospital infrastructure are accelerating market growth. In addition, domestic production and rising competition are making robotic systems more accessible, enabling broader adoption across both public and private healthcare sectors.

Japan Surgical Robots Market Insight

The Japan surgical robots market is gaining traction due to the country’s strong focus on advanced medical technology and demographic shifts such as an aging population. With a robust hospital network and a cultural inclination toward precision and automation, Japan is rapidly integrating robotic systems into general, urologic, and orthopedic surgeries. The government’s support for AI in healthcare and increasing investments by domestic firms are bolstering the market. In addition, rising demand for less invasive, robot-assisted procedures is being driven by patient preferences for faster recovery and fewer complications.

India Surgical Robots Market Insight

The India surgical robots market accounted for the largest market revenue share in Asia-Pacific in 2024, driven by growing awareness of robotic surgery, a rapidly expanding private healthcare sector, and an increasing burden of chronic diseases. The adoption of surgical robots is accelerating in metropolitan hospitals, especially for gynecology, oncology, and urology procedures. Initiatives promoting medical technology startups and the availability of cost-effective robotic solutions by domestic manufacturers are expanding access across urban and semi-urban regions. The market is also benefiting from increased surgeon training programs and tele-mentoring collaborations

Surgical Robots Market Share

The Surgical Robots industry is primarily led by well-established companies, including:

- Intuitive Surgical Inc (U.S.)

- Stryker (U.S.)

- Medrobotics Corporation (U.S)

- Johnson & Johnson and its affiliates (U.S.)

- Globus Medical (U.S.)

- NuVasive Inc. (U.S.)

- Smith + Nephew (U.K.)

- Titan Medical Inc (Canada)

- TransEnterix Inc (U.S.)

- University of Pittsburgh Medical Center (U.S.)

- Mazor Robotics (Israel)

- Auris Health Inc. (U.S.)

- Corindus Inc. (U.S.)

- Renishaw plc (U.K.)

- Medineering GmbH (Germany)

- Medtronic (Ireland)

- Renishaw plc. (U.K.)

- Preceyes BV (Netherlands)

- MicroSure (Netherlands)

- avateramedical GmbH (Germany)

- Siemens AG (Germany)

What are the Recent Developments in Global Surgical Robots Market?

- In March 2024, Intuitive Surgical, Inc. received FDA clearance for the next-generation da Vinci 5 Surgical System, introducing enhanced haptic feedback, improved 3D vision, and an AI-powered analytics suite. This upgrade aims to increase surgical precision and optimize surgeon performance through real-time insights. The da Vinci 5 system reflects Intuitive’s continued leadership in surgical robotics and its investment in evolving capabilities to support complex, minimally invasive proceduresIn March 2024, Intuitive Surgical, Inc. received FDA 510(k) clearance for its fifth-generation da Vinci 5 surgical system, featuring over 150 improvements including force-sensing (haptic feedback), enhanced 3D visualization, expanded computing power, and an optimized console design

- In February 2024, CMR Surgical unveiled a major update to its Versius system, integrating new ICG (Indocyanine Green) imaging capabilities for enhanced visualization of blood flow and tissue perfusion during minimally invasive surgery

- In March 2024, CMR Surgical announced a significant milestone: over 20,000 surgeries performed using the Versius robotic system, including the first pediatric robotic case in the UK—a seven-year-old treated for a kidney condition

- In April 2024, Medical MicroInstruments’ (MMI) Symani surgical system, featuring wristed robotic arms with seven degrees of freedom and tremor suppression, became the first FDA-approved robot for microsurgery, marking a breakthrough in ultra-precise surgical applications

- In July 2025, Zimmer Biomet announced it would acquire Monogram Technologies for approximately USD 177 million, gaining access to semi- and fully autonomous surgical technologies—including a knee replacement system cleared by the FDA in March 2025—in a strategic move to bolster its surgical robotics portfolio

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.