Global Subsea Thermal Insulation Materials Market

Market Size in USD Million

USD

254.32 Million

USD

372.89 Million

2024

2032

USD

254.32 Million

USD

372.89 Million

2024

2032

| 2025 - 2032 | |

| USD 254.32 Million | |

| USD 372.89 Million | |

| % | |

|

Subsea Thermal Insulation Materials Market Size

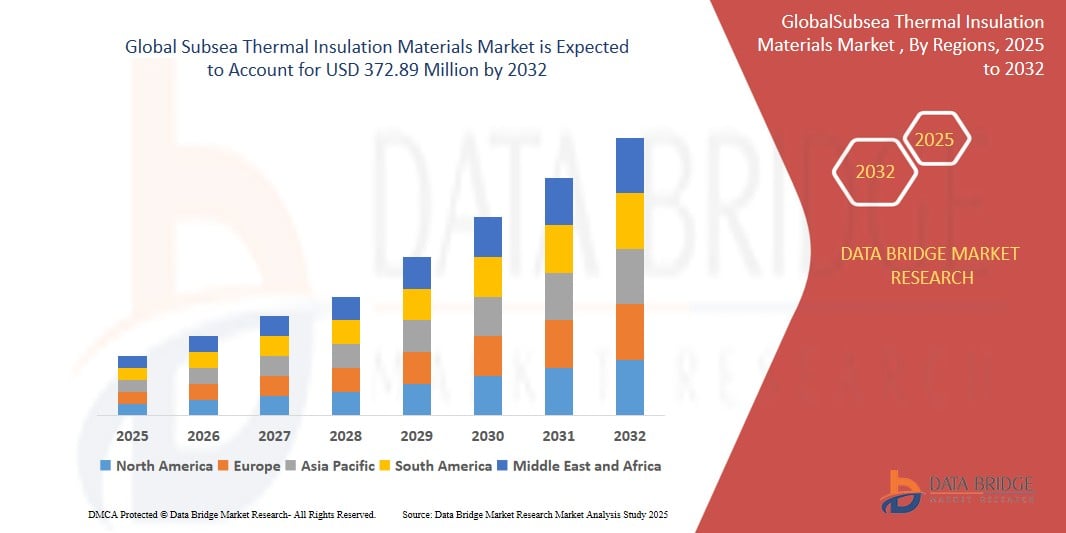

- The global Subsea Thermal Insulation Materials market size was valued at USD 254.32 Million in 2024 and is expected to reach USD 372.89 Million by 2032, at a CAGR of 4.90% during the forecast period

- The market growth is largely fueled by the expanding offshore oil and gas exploration activities, along with increasing investments in deepwater and ultra-deepwater projects, necessitating high-performance insulation solutions for subsea infrastructure.

- Furthermore, rising demand for durable, corrosion-resistant, and thermally efficient materials in harsh subsea environments is positioning Subsea Thermal Insulation Materials as a critical component in offshore operations. These converging factors are accelerating the adoption of advanced insulation technologies, thereby significantly boosting the industry's growth.

Subsea Thermal Insulation Materials Market Analysis

- Subsea Thermal Insulation Materials, designed to provide thermal stability and protect subsea equipment from extreme temperatures and harsh marine environments, are becoming increasingly essential in offshore oil and gas projects, especially in deepwater and ultra-deepwater applications, due to their durability, corrosion resistance, and performance efficiency

- The escalating demand for Subsea Thermal Insulation Materials is primarily fueled by rising offshore exploration and production activities, stringent safety and environmental regulations, and the growing need for flow assurance in subsea pipelines and equipment

- North America dominates the Subsea Thermal Insulation Materials market with the largest revenue share of 40.01% in 2025, driven by significant offshore developments in the Mexico, strong technological capabilities, and robust investment by key players in enhancing subsea infrastructure and production efficiency

- Asia-Pacific is expected to be the fastest-growing region in the Subsea Thermal Insulation Materials market during the forecast period, owing to increasing offshore oil and gas activities, rapid industrialization, and rising energy demand from emerging economies like China, India, and Southeast Asian nations

- The polyurethane segment is expected to dominate the Subsea Thermal Insulation Materials market, with a market share of 43.2% in 2025, due to its excellent thermal insulation properties, low water absorption, and cost-effectiveness, making it the material of choice for coating subsea pipelines, field joints, and equipment.

Report Scope and Subsea Thermal Insulation Materials Market Segmentation

|

Attributes |

Subsea Thermal Insulation Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Subsea Thermal Insulation Materials Market Trends

“Advanced Material Innovations and Integration with Digital Monitoring”

- A significant and accelerating trend in the global Subsea Thermal Insulation Materials market is the development of advanced composite insulation materials that offer enhanced thermal performance, durability, and resistance to extreme subsea pressures and chemical exposure. These innovations are driven by the need for reliable insulation in increasingly deeper and more hostile offshore environments.

- For example, manufacturers are focusing on aerogel-based and syntactic foam materials, which provide superior insulation and lightweight characteristics—critical for deepwater operations. Aerogel insulation is especially gaining traction for its low thermal conductivity and hydrophobic properties.

- Furthermore, digitalization is playing a growing role in the subsea industry. Subsea Thermal Insulation Materials are now being integrated with smart sensors and digital monitoring systems, allowing operators to track pipeline temperature, pressure, and insulation integrity in real time.

- This trend is reshaping operational standards by enabling predictive maintenance, reducing downtime, and enhancing safety and performance. It aligns with the broader move toward digital twins and intelligent subsea infrastructure in offshore oil and gas.

- As oil and gas operators seek more cost-efficient and risk-reducing technologies, the convergence of innovative materials and digital monitoring capabilities is establishing new performance benchmarks and transforming insulation solutions into critical strategic assets.

Subsea Thermal Insulation Materials Market Dynamics

Driver

“Expanding Deepwater Exploration and Demand for Flow Assurance”

- The growing demand for oil and gas from deepwater and ultra-deepwater fields is a major driver of the Subsea Thermal Insulation Materials market. As exploration moves into deeper and colder waters, the need for effective thermal insulation to ensure flow assurance becomes critical.

- Flow assurance challenges such as hydrate formation and wax deposition in subsea pipelines are pushing operators to invest in high-performance insulation solutions that maintain fluid temperatures and prevent blockages.

- For instance, key companies are developing multi-layer insulation systems that combine thermal, mechanical, and anti-corrosion protection, enabling safe and cost-effective transportation of hydrocarbons from subsea wells to processing facilities.

- Additionally, regulatory standards for environmental protection and safety in offshore operations are also encouraging the adoption of advanced insulation materials that minimize the risk of leaks and ensure long-term reliability.

Restraint/Challenge

“High Cost of Advanced Insulation Systems and Harsh Deployment Conditions”

- One of the primary challenges facing the Subsea Thermal Insulation Materials market is the high capital cost associated with the development and installation of advanced insulation systems, particularly in ultra-deepwater projects.

- Materials such as aerogels and high-performance syntactic foams, while offering excellent thermal properties, come with a premium price tag due to complex manufacturing and installation requirements.

- Furthermore, the challenging deployment conditions in deep-sea environments—such as extreme pressures, low temperatures, and strong ocean currents—require rigorous testing and quality assurance, which adds to overall project costs.

- Smaller operators may be hesitant to adopt newer technologies due to budget constraints, opting instead for traditional, less effective insulation solutions.

- Overcoming this barrier will require cost optimization, scalable manufacturing processes, and strong collaboration between insulation material providers and offshore engineering firms to develop modular, easy-to-install solutions that lower lifecycle costs while maintaining performance.

Subsea Thermal Insulation Materials Market Scope

The market is segmented on the basis application, type.

- By Type

On the basis of type, the Subsea Thermal Insulation Materials market is segmented into Polypropylene, Polyurethane, Silicone Rubber, Aerogel, Epoxy. The Polyurethane segment dominates the largest market revenue share of 43.2% in 2025, driven by its excellent thermal insulation properties, mechanical strength, and adaptability in coating subsea pipelines and field joints. Its widespread usage is attributed to cost-effectiveness, ease of application, and proven performance in deepwater conditions. The Aerogel segment is anticipated to witness the fastest growth rate of 21.7% from 2025 to 2032, due to its ultra-low thermal conductivity, lightweight characteristics, and increasing demand in high-performance insulation applications. The material’s hydrophobic and corrosion-resistant nature makes it ideal for extreme subsea environments, fueling its rapid adoption in advanced offshore developments.

- By Application

On the basis of application, the Subsea Thermal Insulation Materials market is segmented into Pipe Cover, Field Joints, Pipe-in-Pipe, Equipment. The Pipe Cover segment accounted for the largest market revenue share in 2024, driven by the extensive use of thermal insulation materials to maintain optimal fluid temperatures and ensure flow assurance across long pipeline systems. The segment benefits from continuous offshore pipeline installations and growing deepwater projects.

The Field Joints segment is expected to witness the fastest CAGR from 2025 to 2032, propelled by increasing offshore pipeline welding and connection activities. Field joints require specialized insulation solutions to ensure thermal continuity, and the rising demand for efficient installation techniques in subsea environments is accelerating growth in this application area.

Subsea Thermal Insulation Materials Market Regional Analysis

- North America dominates the Subsea Thermal Insulation Materials market with the largest revenue share of 40.01% in 2024, driven by increased offshore oil & gas activities, particularly in the Gulf of Mexico, and ongoing deepwater and ultra-deepwater exploration projects

- The region benefits from well-established subsea infrastructure, strong government support for energy security, and investments in extending the lifecycle of mature offshore assets through advanced insulation technologies

- Technological innovations and collaborations between major energy firms and material manufacturers further enhance the deployment of efficient, corrosion-resistant insulation solutions tailored to harsh subsea environments

U.S. Subsea Thermal Insulation Materials Market Insight

The U.S. market captured the largest revenue share of 81% within North America in 2025, owing to robust investments in offshore oil & gas projects and the country’s leadership in deepwater drilling operations. The use of advanced insulation materials for flow assurance, energy efficiency, and pipeline protection is growing significantly in the U.S., especially in the Gulf of Mexico. Ongoing exploration in deep and ultra-deep waters is driving continuous demand for high-performance insulation systems, particularly polyurethane and polypropylene coatings

Europe Subsea Thermal Insulation Materials Market Insight

The European market is projected to expand at a substantial CAGR during the forecast period, led by the North Sea and Norwegian Continental Shelf activities. Europe’s focus on sustainable energy extraction, aging pipeline infrastructure, and stringent environmental regulations is encouraging the use of durable and eco-friendly thermal insulation materials. Growing investments in carbon capture and storage (CCS) and subsea processing also contribute to the region's insulation material demand.

U.K. Subsea Thermal Insulation Materials Market Insight

The U.K. market is anticipated to grow at a noteworthy CAGR, supported by revitalized North Sea exploration and production efforts. Government initiatives to extend the operational life of brownfield sites, combined with rising demand for energy efficiency, are boosting market adoption. Innovative solutions such as wet insulation systems and aerogel-based materials are increasingly utilized in harsh offshore conditions.

Germany Subsea Thermal Insulation Materials Market Insight

Germany’s market is expected to expand at a considerable CAGR, mainly driven by engineering innovation and the country's leadership in subsea equipment manufacturing. R&D efforts in green materials and insulation coatings align with Germany’s focus on sustainability and energy efficiency. The demand for advanced syntactic foams and hydrophobic materials is growing, particularly in high-pressure environments.

Asia-Pacific Subsea Thermal Insulation Materials Market Insight

The Asia-Pacific market is poised to grow at the fastest CAGR of over 24% in 2025, led by deepwater projects in China, India, Malaysia, and Australia. Rapid industrialization, expanding offshore fields, and favorable government initiatives are major growth drivers. The region also benefits from cost-effective manufacturing hubs and increasing domestic energy demand, particularly in China and India.

Japan Subsea Thermal Insulation Materials Market Insight

Japan’s market is gaining momentum due to its technological expertise and focus on energy efficiency in offshore projects. The country’s stringent regulatory standards and investments in advanced subsea robotics and pipeline technologies are supporting market expansion. Adoption of insulation materials is expected to rise in floating LNG projects and deep-sea extraction efforts.

China Subsea Thermal Insulation Materials Market Insight

China accounted for the largest revenue share in Asia-Pacific in 2025, fueled by the expansion of deepwater oil & gas fields in the South China Sea. Strong government backing for energy independence, massive infrastructure development, and domestic production of insulation materials are key growth enablers. China is also investing in localized solutions and partnerships with global oilfield service providers to enhance technological capabilities and cost-efficiency.

Subsea Thermal Insulation Materials Market Share

The Subsea Thermal Insulation Materials industry is primarily led by well-established companies, including:

- Cabot Corporation (U.S.)

- Aspen Aerogels Inc. (U.S.)

- TechnipFMC plc (U.K.)

- Advanced Insulation Limited (U.K.)

- BASF SE (Germany)

- The Dow Chemical Company (U.S.)

- Ameriforge Group Inc. (U.S.)

- Trelleborg AB (publ) (Sweden)

- SHAWCOR (Canada)

- Tenaris (Luxembourg)

- Aegion Corporation (U.S.)

- Balmoral Group Holdings Ltd (U.K.)

- Engineered Syntactic Systems (U.S.)

- Materia Inc. (U.S.)

Latest Developments in Global Subsea Thermal Insulation Materials Market

- In April 2023, Trelleborg Group, a key player in engineered polymer solutions, announced the launch of its next-generation subsea thermal insulation coating system — Vikotherm R2. This advanced solution enhances flow assurance and durability in extreme subsea environments. The innovation aims to improve resistance against hydrostatic pressure and aggressive fluids, further cementing Trelleborg’s leadership in offshore oil & gas insulation applications.

- In March 2023, Shawcor Ltd. (now Mattr Infratech) completed the qualification and deployment of its new Thermotite ULTRA system, designed for ultra-deepwater thermal insulation. This development supports subsea tieback and pipeline projects requiring high thermal performance under extreme pressure and temperature. The launch demonstrates Shawcor’s commitment to meeting the growing demands of subsea field operators globally.

- In February 2023, Advanced Insulation Ltd. expanded its manufacturing capacity in the Middle East region, aimed at supplying subsea insulation materials for major offshore projects in the Persian Gulf. The company’s ContraTherm C55 and C25 products have gained traction due to their excellent performance in subsea structures and flowlines. This strategic move strengthens its global footprint and improves delivery timelines.

- In January 2023, TechnipFMC, in collaboration with TotalEnergies, initiated a pilot project in West Africa utilizing innovative aerogel-based thermal insulation for flowline applications. The use of aerogel materials aims to significantly reduce heat loss while lowering weight and space constraints on subsea structures. This marks a step toward sustainable and efficient offshore production systems.

- In December 2022, BASF SE introduced a modified polyurethane-based insulation system under its Elastopor series tailored for subsea equipment. The formulation is engineered for improved bonding, impact resistance, and long-term thermal efficiency in harsh marine environments. BASF’s investment in R&D for subsea thermal materials reflects the rising demand for customized, high-performance insulation systems in deepwater applications.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Subsea Thermal Insulation Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Subsea Thermal Insulation Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Subsea Thermal Insulation Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.