Global Structural Core Materials Market

Market Size in USD Billion

CAGR :

%

USD

2.77 Billion

USD

4.55 Billion

2024

2032

USD

2.77 Billion

USD

4.55 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.77 Billion | |

| USD 4.55 Billion | |

| % | |

|

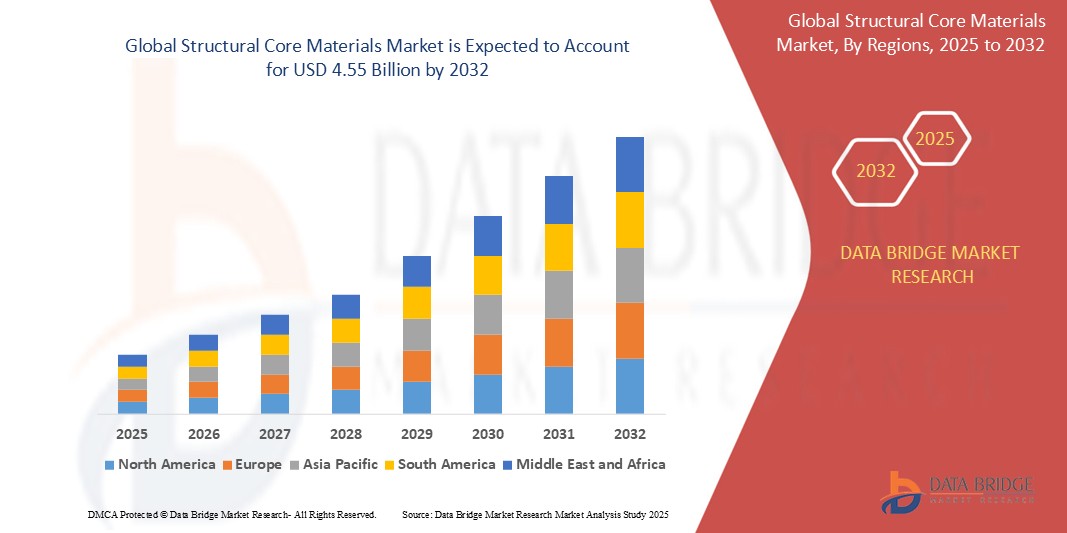

Structural Core Materials Market Size

- The global structural core materials market size was valued at USD 2.77 billion in 2024 and is expected to reach USD 4.55 billion by 2032, at a CAGR of 6.42% during the forecast period

- The market growth is largely fueled by increasing demand for lightweight and high-performance materials in key industries such as aerospace, automotive, and wind energy.

- Growing demand for fuel-efficient and lightweight vehicles and aircraft is driving the use of structural core materials that offer high strength-to-weight ratios. Industries are increasingly adopting these materials to meet strict environmental regulations and improve overall performance

- Rapid expansion of the wind energy sector, especially in Asia-Pacific and Europe, is boosting the need for core materials used in turbine blades. These materials enhance durability and efficiency, supporting the shift toward sustainable energy solutions

Structural Core Materials Market Analysis

- The structural core materials market is currently experiencing substantial growth, driven by increasing demand from key sectors such as aerospace and wind energy, which require lightweight and high-strength materials for enhanced efficiency and performance

- This market is characterized by ongoing technological advancements and a focus on developing more sustainable and recyclable core materials, indicating a dynamic landscape with continuous innovation in material properties and applications

- North America dominates the smart lock market with the share of 36.11% in 2024, due to strong presence of advanced manufacturing industries and high investments in aerospace, wind energy, and marine sectors

- Asia-Pacific is expected to be the fastest growing region in the smart lock market during the forecast period, propelled by rapid industrialization, infrastructure development, and renewable energy initiatives across emerging economies

- The honeycomb segment holds the largest market revenue share of 36.13% in 2024, due to its versatility, low density, and suitability across a range of industries such as transportation, wind energy, and marine

Report Scope and Structural Core Materials Market Segmentation

|

Attributes |

Structural Core Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Structural Core Materials Market Trends

“Growing Demand for Sustainable Structural Core Materials”

- A significant market trend is the increasing focus on sustainability, driving the demand for recyclable and bio-based structural core materials

- The development and adoption of PET foam cores made from recycled plastic bottles showcase this trend towards environmentally friendly material options

- This emphasis on sustainability is influencing material innovation and manufacturing processes across the structural core materials market

- Consequently, manufacturers are investing in research and development to create greener alternatives without compromising performance

- In conclusion, the current market increasingly favors sustainable structural core materials, reflecting a broader industry commitment to environmental responsibility

Structural Core Materials Market Dynamics

Driver

“Growing Demand from Wind Energy Sector Fuels Market Expansion”

- The increasing global emphasis on renewable energy prominently features wind power, significantly driving the need for sophisticated structural core materials

- The trend towards larger offshore wind turbines with longer rotor blades necessitates lightweight yet robust core materials such as PET foam and honeycomb to endure substantial operational stresses

- These advanced materials ensure turbine durability and efficiency by offering high stiffness-to-weight ratios, crucial for minimizing stress and maximizing energy capture, for instance, longer blades made possible by these cores enhance power generation

- Supportive governmental policies and incentives for renewable energy projects worldwide are further fueling the expansion of the wind energy sector, thereby creating a sustained demand for these high-performance core materials

- In conclusion, the symbiotic growth of wind power and advancements in structural core materials highlights a key market driver, with ongoing material innovation crucial for future turbine development and efficiency

Restraint/Challenge

“High Initial Material and Processing Costs Impede Wider Adoption”

- The considerable initial expenses related to both raw materials and specialized processing methods present a notable impediment to the wider and quicker acceptance of sophisticated structural core materials across diverse sectors

- The production of aerospace-quality foams and intricate honeycomb structures necessitates complex manufacturing, leading to elevated costs compared to conventional materials such as metals

- Integrating these core materials often requires specialized knowledge and equipment for tasks such as precision bonding in aircraft panels, further contributing to the overall expense

- While the long-term advantages, such as enhanced fuel efficiency in vehicles, can offset the initial investment, the higher upfront costs can particularly challenge smaller businesses or industries sensitive to price

- In conclusion, reducing these costs through manufacturing innovations and the development of more economical material options is crucial for broader market penetration of advanced structural core solutions

Structural Core Materials Market Scope

The market is segmented on the basis of type, communication protocol, unlocking mechanism, and application.

- By Skin Type

On the basis of skin type, the structural core materials market is segmented into GFRP, CFRP, NFRP, and other. The GFRP segment dominates the largest market revenue share of 43.2% in 2024, driven by its cost-effectiveness, excellent mechanical properties, and corrosion resistance. GFRP is widely used across marine, wind energy, and construction sectors, where durability and affordability are key considerations. Its compatibility with various core materials and ease of fabrication further boost its preference in industrial applications.

The CFRP segment is anticipated to witness the fastest growth rate of 21.7% from 2025 to 2032, fueled by rising demand in aerospace and automotive industries. Its superior strength-to-weight ratio makes it ideal for lightweight, high-performance components. CFRP'S role in reducing fuel consumption and emissions aligns with sustainability goals, enhancing its adoption across advanced engineering applications.

- By Type

On the basis of type, the structural core materials market is segmented into foam, honeycomb, and balsa. The honeycomb segment holds the largest market revenue share of 36.13% in 2024, due to its versatility, low density, and suitability across a range of industries such as transportation, wind energy, and marine. Its ease of machining and adaptability to different shapes make it a preferred choice for lightweight structural applications.

The honeycomb segment is projected to register the fastest growth rate of from 2025 to 2032, driven by increasing demand in aerospace and defense sectors. Its exceptional stiffness and minimal weight make it ideal for high-performance, weight-sensitive structures. Additionally, its energy absorption capacity and thermal insulation properties further drive its uptake in advanced engineering systems.

- By End User Industry

On the basis of end user industry, the structural core materials market is segmented into oil and gas, aerospace, wind energy, marine, transportation, construction, and others. The wind energy segment commands the largest market revenue share in 2024, propelled by the global shift towards renewable energy. Structural core materials play a crucial role in manufacturing long and durable wind turbine blades, enhancing efficiency and operational life. Investments in offshore wind farms and supportive government policies are further reinforcing market demand.

The aerospace segment is expected to witness the fastest growth from 2025 to 2032, backed by increased aircraft production and focus on lightweight materials to reduce fuel consumption. Structural core materials are increasingly used in interior panels, flooring, and control surfaces to improve performance and meet stringent safety and weight standards. Their high strength and rigidity also contribute to greater fuel efficiency and load-bearing capacity.

Structural Core Materials Market Regional Analysis

- North America dominates the structural core materials market with the share of 36.11% in 2024, due to strong presence of advanced manufacturing industries and high investments in aerospace, wind energy, and marine sectors

- The region benefits from well-established aerospace and defense industries, particularly in the U.S., where lightweight and high-performance materials are in high demand for aircraft and military applications

- Increasing investments in renewable energy, especially offshore and onshore wind projects, are fueling the adoption of structural core materials to enhance turbine efficiency and durability

U.S. Structural Core Materials Market Insight

The U.S. structural core materials market captured the largest revenue share within North America in 2024, driven by the strong presence of aerospace, wind energy, and marine industries. High investments in renewable energy infrastructure and defense contribute to robust demand for lightweight and high-performance core materials. The U.S. also benefits from advanced manufacturing capabilities and a mature composites industry, which supports innovation and broad application of structural core materials across various sectors.

Europe Structural Core Materials Market Insight

The European structural core materials market is projected to expand at a substantial CAGR throughout the forecast period with share of 17.1%, fueled by the region’s focus on sustainability and carbon reduction. Stringent EU regulations promoting energy efficiency and lightweight construction in transportation and building sectors are spurring demand. Key countries such as Germany, France, and the U.K. are heavily investing in wind power and aerospace industries, where structural core materials are integral for improving performance and durability while reducing weight.

U.K. Structural Core Materials Market Insight

The U.K. structural core materials market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by the country’s expanding aerospace, marine, and wind energy sectors. The shift towards sustainable construction and lightweight materials in public infrastructure and commercial buildings is enhancing the adoption of core materials. Additionally, the government’s push for renewable energy and decarbonization targets further supports the increased use of structural core solutions in wind turbine and transport applications.

Germany Structural Core Materials Market Insight

The German structural core materials market is expected to expand at a considerable CAGR during the forecast period, due to its leadership in automotive and engineering industries. Demand for lightweight, high-strength materials to meet stringent EU emissions standards is pushing structural core material adoption. Germany's strong focus on R&D, combined with increasing offshore wind energy projects and aerospace production, plays a critical role in driving the market forward.

Asia-Pacific Structural Core Materials Market Insight

The Asia-Pacific structural core materials market is poised to grow at the share of 34.3%in 2024, propelled by rapid industrialization, infrastructure development, and renewable energy initiatives across emerging economies. Countries such as China, India, and Southeast Asian nations are significantly increasing investments in wind energy, marine transport, and construction sectors, thereby boosting demand. APAC's competitive manufacturing landscape and increasing adoption of composite materials make it a high-growth region for structural core materials.

Japan Structural Core Materials Market Insight

The Japan structural core materials market is gaining traction due to rising demand in aerospace and public infrastructure development. The country’s advanced technological landscape and focus on earthquake-resilient, lightweight construction solutions are encouraging the adoption of structural core materials. Japan's active participation in offshore wind projects and innovation in transport technologies also support market growth, alongside a national drive for greater energy efficiency and sustainability.

China Structural Core Materials Market Insight

The China structural core materials market accounted for the largest market revenue share in Asia-Pacific in 2024, driven by the country’s dominant position in wind energy and transportation manufacturing. China’s large-scale infrastructure projects and growing aerospace industry are significant contributors to demand. With strong government support for renewable energy and energy-efficient technologies, as well as a well-established composites production base, China continues to be a central hub for structural core materials manufacturing and consumption.

Structural Core Materials Market Share

The structural core materials industry is primarily led by well-established companies, including:

- Evonik Industries AG (Germany)

- BASF SE (Germany)

- SABIC (Saudi Arabia)

- Plascore, Inc. (U.S.)

- CoreLite (U.S.)

- Collins Aerospace (U.S.)

- Diab (Sweden)

- Gurit (Switzerland)

- SCHWEITER TECHNOLOGIES (Switzerland)

- Hexcel Corporation (U.S.)

- The Gill Corporation (U.S.)

- EURO-COMPOSITES (Luxembourg)

- Advanced Honeycomb Technologies (U.S.)

- 3A Composites GmbH (Germany)

- Armacell (Germany)

- I-Core Composites, LLC (U.S.)

- COMPOSITE ESSENTIAL MATERIALS (U.S.)

- Arkema (France)

- DSM (Netherlands)

- 3M (U.S.)

Latest Developments in Global Structural Core Materials Market

- In March 2023, 3A Composites Core Materials introduced the Engicore core materials product line for the North and South American markets. This new portfolio expands the company’s range of offerings, providing customers with customized core solutions that are designed to adapt to and function optimally within their manufacturing processes and standard requirements

- In August 2023, Owens Corning partners with a leading boat manufacturer to develop new lightweight and fuel-efficient boat designs using its core materials

- In September 2023, The Gill Corporation launches a new online configurator tool for customers to design and order custom core material solutions

- In October 2023, Plascore announces the expansion of its manufacturing facility in Europe to meet the growing demand for core materials in the construction industry

- In November 2023, A consortium of leading research institutions and industry players launches a project to develop new recyclable and high-performance core materials

- In, December 2023, The E.U. announces stricter regulations on the use of certain flame retardants in core materials, impacting the market for some traditional materials

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Structural Core Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Structural Core Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Structural Core Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.