Global Sternal Closure Systems Market

Market Size in USD Billion

USD

2.48 Billion

USD

3.94 Billion

2024

2032

USD

2.48 Billion

USD

3.94 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.48 Billion | |

| USD 3.94 Billion | |

| % | |

|

Sternal Closure Systems Market Size

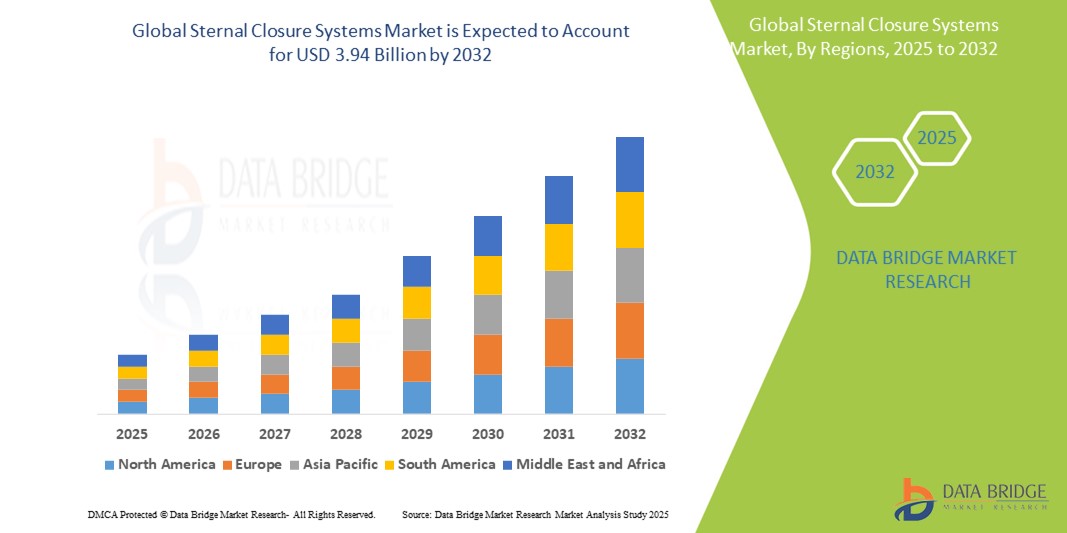

- The global sternal closure systems market size was valued at USD 2.48 billion in 2024 and is expected to reach USD 3.94 billion by 2032, at a CAGR of 5.93% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress within cardiac surgery procedures and the increasing prevalence of cardiovascular diseases requiring sternotomies, leading to greater utilization of sternal closure devices in both established and emerging healthcare systems

- Furthermore, rising demand for advanced closure systems that improve patient outcomes, reduce complications, and enhance healing is establishing modern sternal closure techniques as the standard of care. These converging factors are accelerating the uptake of sternal closure systems solutions, thereby significantly boosting the industry's growth

Sternal Closure Systems Market Analysis

- Sternal closure systems, offering devices for stabilizing the sternum after open-heart surgery, are increasingly vital components of modern cardiac surgical procedures in both hospital and specialized clinics due to their enhanced stability, reduced risk of complications, and promotion of faster healing

- The escalating demand for sternal closure systems is primarily fueled by the rising number of cardiac surgeries performed globally, growing awareness of the benefits of rigid fixation, and a rising preference for systems that improve patient outcomes and reduce sternal wound infections

- North America dominates the sternal closure systems market with the largest revenue share of 44.5% in 2025, characterized by a high volume of cardiac surgeries, well-established healthcare infrastructure, and a strong presence of key industry players, with the U.S. experiencing substantial growth in the adoption of advanced closure technologies, particularly in major cardiac centers and hospitals, driven by innovations from both established medical device companies and startups focusing on improved materials and designs

- Asia-Pacific is expected to be the fastest-growing region in the sternal closure systems market during the forecast period with a CAGR of 6.9%, due to increasing prevalence of cardiovascular diseases, rising geriatric population requiring cardiac interventions, and improving healthcare infrastructure and access in developing economies

- Closure devices segment is expected to dominate the sternal closure systems market with market revenue share with 84.2% in 2025, driven by the increasing preference for rigid fixation and the availability of various advanced designs such as plates and screws offering enhanced stability

Report Scope and Sternal Closure Systems Market Segmentation

|

Attributes |

Sternal Closure Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Sternal Closure Systems Market Trends

“Enhanced Convenience Through AI and Digital Integration in Surgical Planning”

- A significant and accelerating trend in the global sternal closure systems market is the deepening integration with artificial intelligence (AI) and advanced digital platforms for surgical planning and postoperative monitoring. This fusion of technologies is significantly enhancing surgeon convenience and control over the entire sternal closure process

- For instance, AI-powered surgical planning software can analyze patient-specific CT scans to suggest optimal closure techniques and device placement. Similarly, digital platforms allow for remote monitoring of sternal stability and healing progress post-surgery

- AI integration in surgical planning enables features such as predicting potential complications based on patient data and suggesting personalized closure strategies. For instance, AI algorithms can analyze risk factors to recommend specific plate configurations. Furthermore, digital monitoring capabilities offer surgeons the ease of remotely tracking patient recovery and identifying potential issues early

- The seamless integration of sternal closure devices with digital surgical planning tools and patient monitoring platforms facilitates centralized management of the entire surgical episode. Through a single interface, surgeons can plan the procedure, select appropriate devices, and monitor postoperative outcomes, creating a unified and optimized surgical experience

- This trend towards more intelligent, intuitive, and interconnected surgical solutions is fundamentally reshaping surgeon expectations for sternal closure procedures. Consequently, companies are developing AI-enabled surgical planning software with features such as automated device selection based on anatomical data and digital platforms compatible with remote patient monitoring systems

Sternal Closure Systems Market Dynamics

Driver

“Growing Need Due to Rising Cardiac Surgeries and Focus on Patient Outcomes”

- The increasing prevalence of cardiovascular diseases requiring surgical intervention and the growing emphasis on improved patient outcomes following sternotomies are significant drivers for the heightened demand for advanced sternal closure systems

- For instance, in April 2024, major medical device companies announced the launch of new sternal closure technologies designed to enhance stability and reduce the risk of post-operative complications. Such strategic initiatives by key companies are expected to drive the sternal closure systems industry growth in the forecast period

- As surgeons become more aware of the benefits of rigid sternal fixation in reducing pain, accelerating healing, and minimizing the incidence of sternal dehiscence and infection, advanced closure systems offer a compelling upgrade over traditional wire closure techniques

- Furthermore, the growing adoption of enhanced recovery after surgery (ERAS) protocols and the desire for shorter hospital stays are making advanced sternal closure systems an integral component of modern cardiac surgery, offering improved stability and potentially faster rehabilitation

- The convenience of using rigid fixation devices that provide superior stability, reduce the need for prolonged immobilization, and potentially lower the risk of re-intervention are key factors propelling the adoption of advanced sternal closure systems in both routine and complex cardiac procedures. The trend towards minimally invasive cardiac surgery, which still often requires a partial sternotomy, further contributes to market growth

Restraint/Challenge

“Concerns Regarding Cost and Surgeon Preference for Traditional Methods”

- Concerns surrounding the higher cost of advanced sternal closure systems compared to traditional sternal wires pose a significant challenge to broader market penetration. As hospitals and healthcare systems face increasing budgetary pressures, the upfront cost of newer technologies can raise concerns about cost-effectiveness, particularly for routine procedures

- For instance, the higher price point of plate and screw systems has made some institutions hesitant to adopt them universally over the more familiar and less expensive wire closure techniques

- Addressing these cost concerns through demonstrating clear long-term benefits such as reduced complications and readmission rates, and offering value-based purchasing options, is crucial for wider adoption. Companies are increasingly focusing on highlighting the overall cost savings associated with advanced closure systems due to improved patient outcomes. In addition, the established comfort level and extensive clinical experience surgeons have with traditional wire closure methods can create resistance to adopting new techniques and devices. Overcoming this requires comprehensive training, compelling clinical data demonstrating the superiority of advanced systems in specific patient populations, and addressing any perceived learning curves associated with new technologies

- While the clinical benefits of advanced sternal closure systems are becoming increasingly evident, the perceived higher cost and the inertia associated with established surgical practices can still hinder widespread adoption, especially in cost-sensitive healthcare environments or among surgeons with a strong preference for traditional methods

- Overcoming these challenges through robust economic evaluations, comprehensive surgeon education and training programs, and the development of more cost-effective advanced closure options will be vital for sustained market growth

Sternal Closure Systems Market Scope

The market is segmented on the basis of product type, procedure, material and end user.

By Product Type

On the basis of product type, the sternal closure systems market is segmented into closure devices and bone cement. The closure devices segment dominates the largest market revenue share with 84.2% in 2025, driven by the increasing preference for rigid fixation and the availability of various advanced designs such as plates and screws offering enhanced stability. The market also sees strong demand for closure devices due to their proven efficacy in reducing complications compared to traditional methods

The bone cement segment is anticipated to witness a steady growth rate from 2025 to 2032, fueled by its use in specific patient populations and complex sternal reconstructions, offering gap filling and additional stability

By Procedure

On the basis of procedure, the sternal closure systems market is segmented into median sternotomy, hemisternotomy, bilateral thoracosternotomy, and others. The median sternotomy segment held the largest market revenue share in 2025, driven by the high volume of open-heart surgeries performed using this standard approach. Median sternotomy remains the most common access for various cardiac procedures

The hemisternotomy and bilateral thoracosternotomy segments are expected to witness increasing adoption from 2025 to 2032, fueled by the rise in minimally invasive cardiac surgery techniques and specific surgical requirements in complex cases

By Material

On the basis of material, the sternal closure systems market is segmented into stainless steel, titanium, polyether ether ketone (PEEK), and others. The titanium segment held the largest market revenue share in 2025, driven by its biocompatibility, corrosion resistance, and non-ferromagnetic properties, making it suitable for a wide range of patients, including those needing MRI scans post-surgery

The PEEK segment is expected to witness the fastest CAGR from 2025 to 2032, favored for its excellent biocompatibility, radiolucency, and mechanical properties that closely match bone, leading to increased adoption in advanced fixation techniques

By End User

On the basis of end user, the sternal closure Systems market is segmented into hospitals, specialty clinics, and ambulatory surgical centers. The hospitals segment accounted for the largest market revenue share in 2024, driven by the high volume of cardiac surgeries performed in hospital settings and the availability of comprehensive surgical facilities. The increasing number of cardiac centers and the rising geriatric population requiring cardiac interventions further support this segment's dominance

The specialty clinics and ambulatory surgical centers segments are expected to witness a significant growth rate from 2025 to 2032, driven by the increasing focus on cost-effective outpatient procedures and the expansion of specialized cardiac care facilities

Sternal Closure Systems Market Regional Analysis

- North America dominates the sternal closure systems market with the largest revenue share of approximately 44.5% in 2025, driven by a high volume of cardiac surgeries, a well-established and technologically advanced healthcare infrastructure, and the strong presence of leading medical device manufacturers

- Healthcare providers and patients in the region place a high value on the benefits of advanced sternal closure technologies, including reduced risk of complications, improved patient outcomes, and enhanced healing

- This widespread adoption is further supported by favorable reimbursement structures, significant healthcare expenditure, and a growing emphasis on procedural efficiency and patient comfort, establishing modern sternal closure systems as the preferred method for sternal closure following cardiac surgery

U.S. Sternal Closure Systems Market Insight

The U.S. sternal closure systems market is a significant segment within North America. With a market share of 36.7%, driven by a high prevalence of cardiovascular diseases and a large number of open-heart surgeries performed annually. In addition, the presence of key market players and their focus on technological advancements contribute to the market's expansion. Factors such as favorable reimbursement regulations and substantial investments in research and development further fuel market growth.

Europe Sternal Closure Systems Market Insight

The Europe sternal closure systems market is experiencing substantial growth due to an increasing geriatric population and a rising number of cardiac surgeries. The focus on healthcare infrastructure and increasing healthcare expenditure also contribute significantly. The adoption of advanced sternal closure devices and techniques is becoming more prevalent, leading to better patient outcomes and reduced complications.

U.K. Sternal Closure Systems Market Insight

The U.K. market for sternal closure systems is growing due to the increasing number of cardiac procedures and the adoption of sophisticated sternal closure systems, such as rigid fixation devices. These advanced systems facilitate better patient outcomes and earlier hospital discharge, driving their adoption in the UK. The market is also influenced by the presence of a well-established healthcare system and increasing awareness of advanced surgical techniques.

Germany Sternal Closure Systems Market Insight

The German sternal closure systems market is expanding, driven by increasing awareness of advanced medical technologies and a strong healthcare infrastructure. The emphasis on innovation in medical devices and a growing geriatric population requiring cardiac surgeries contribute to the market's growth. The market also benefits from the presence of well-established hospitals and cardiac centers.

Asia-Pacific Sternal Closure Systems Market Insight

Asia-Pacific sternal closure systems market is poised for the fastest growth, with a CAGR of 6.9%, driven by increasing urbanization, rising healthcare expenditure, and a growing prevalence of cardiovascular diseases in countries such as China, Japan, and India. The region's expanding geriatric population and improvements in healthcare infrastructure are also significant growth drivers. Furthermore, increasing medical tourism and the adoption of advanced surgical procedures contribute to the market's rapid expansion.

Japan Sternal Closure Systems Market Insight

The Japan sternal closure systems market is gaining momentum due to the country's advanced healthcare system, high adoption of medical technologies, and a significant elderly population requiring cardiac interventions. The market is driven by a focus on surgical outcomes and the integration of sternal closure techniques in cardiac surgeries.

China Sternal Closure Systems Market Insight

The China sternal closure systems market accounted for the fastest-growing country in Asia Pacific with a CAGR of 7.1%. This is attributed to the country's large population, increasing prevalence of cardiovascular diseases, and expanding healthcare infrastructure. The rising number of cardiac surgeries and increasing healthcare spending are key factors propelling the market in China. In addition, government initiatives to improve healthcare access and the increasing adoption of advanced medical technologies contribute to the market's growth.

Sternal Closure Systems Market Share

The Sternal Closure Systems industry is primarily led by well-established companies, including:

- Zimmer Biomet (U.S.)

- KLS Martin Group (Germany)

- Acute Innovations LLC (U.S.)

- IDEAR S.R.L (Argentina)

- Kinamed Incorporated (U.S.)

- Neuromedex GmbH (Germany)

- ABYRX, INC. (U.S.)

- JEIL MEDICAL CORPORATION (South Korea)

- Waston Medical corporation (China)

- Johnson & Johnson Services, Inc. (U.S.)

- Teleflex Incorporated (U.S.)

- B. Braun SE (Germany)

- Sklar Instruments (U.S.)

- Cardiolink (Spain)

- Stryker (U.S.)

- Acumed LLC (U.S.)

Latest Developments in Global Sternal Closure Systems Market

- In August 2024, DePuy Synthes (Johnson & Johnson) launched the MatrixSTERNUM Fixation System. This is a plate and screw fixation system designed to stabilize the chest wall after procedures such as open-heart and chest surgery. The system boasts stronger locking strength, faster chest fixation, and thinner, low-profile plates compared to some existing products

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.