Global Sperm Separation Devices Market

Market Size in USD Million

CAGR :

%

USD

690.47 Million

USD

2,310.91 Million

2024

2032

USD

690.47 Million

USD

2,310.91 Million

2024

2032

| 2025 - 2032 | |

| USD 690.47 Million | |

| USD 2,310.91 Million | |

| % | |

|

Sperm Separation Devices Market Size

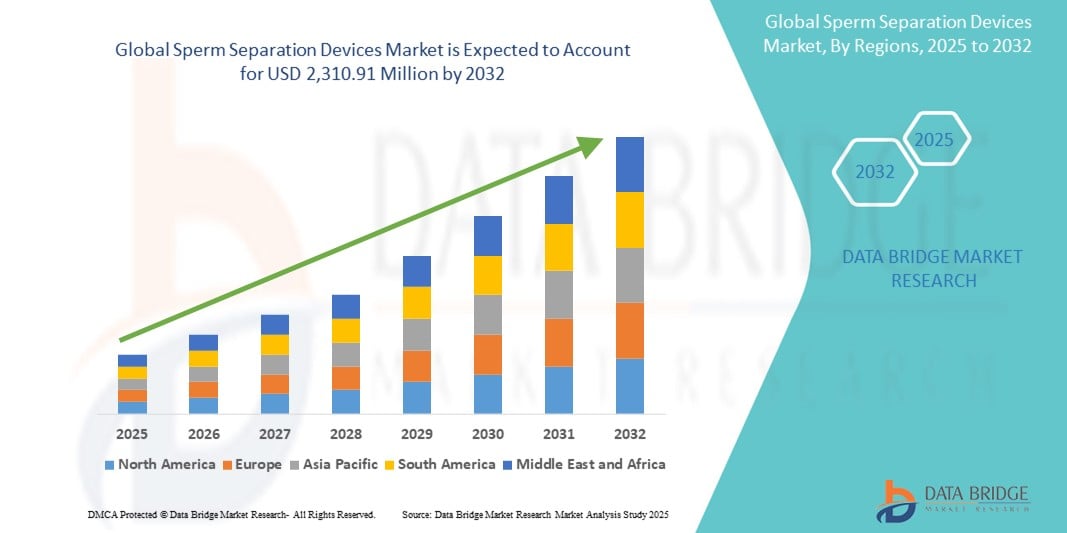

- The global sperm separation devices market size was valued at USD 690.47 million in 2024 and is expected to reach USD 2,310.91 million by 2032, at a CAGR of 16.30% during the forecast period

- The market growth is largely fueled by the rising prevalence of infertility and the increasing adoption of assisted reproductive technologies (ART) such as in vitro fertilization (IVF) and intrauterine insemination (IUI). These medical advancements are driving demand for efficient and reliable sperm separation devices that improve fertilization outcomes

- Furthermore, ongoing technological progress in microfluidics and non-invasive sperm sorting techniques is transforming traditional sperm preparation methods. This is enabling greater accuracy, reduced DNA fragmentation, and improved clinical efficiency. These converging factors are accelerating the uptake of sperm separation device solutions, thereby significantly boosting the industry's growth

Sperm Separation Devices Market Analysis

- Sperm separation devices, designed to isolate high-quality, motile sperm for use in assisted reproductive technologies, are increasingly vital tools in fertility treatments due to their ability to improve fertilization success rates, reduce the risk of genetic abnormalities, and enhance patient outcomes in both clinical and home-based reproductive settings

- The escalating demand for sperm separation devices is primarily fueled by the rising global incidence of male infertility, the growing popularity of in vitro fertilization (IVF) and intrauterine insemination (IUI), and an increasing focus on non-invasive and precise sperm selection technologies such as microfluidic-based systems

- North America dominated the sperm separation devices market, capturing the largest revenue share of 38.7% in 2024, driven by high awareness of infertility treatments, strong healthcare infrastructure, and the presence of leading ART clinics and device manufacturers. The U.S. in particular is seeing significant growth in fertility procedures, supported by ongoing R&D investments and favorable reimbursement policies

- Asia-Pacific is expected to be the fastest growing region in the sperm separation devices market during the forecast period, projected to grow at a CAGR of 8.5%, owing to increasing urbanization, rising disposable incomes, improving access to fertility care, and a growing awareness of reproductive health in countries such as India, China, and Japan

- The centrifugation devices segment dominated the sperm separation devices market, with a market share of 57.4% in 2024, owing to its widespread clinical use, cost-effectiveness, and established efficacy in separating motile sperm for use in assisted reproductive procedures such as IUI and IVF

Report Scope and Sperm Separation Devices Market Segmentation

|

Attributes |

Sperm Separation Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Sperm Separation Devices Market Trends

“Advancements in Microfluidics and Automated Sperm Selection”

- A significant and accelerating trend in the global sperm separation devices market is the integration of advanced microfluidic technologies and automated sperm sorting systems, enhancing precision, efficiency, and non-invasiveness in assisted reproductive techniques. These innovations are significantly improving user convenience, clinical outcomes, and accessibility of fertility care

- For instance, Zymot sperm separation devices utilize microfluidic channels to mimic the natural environment of the female reproductive tract, enabling selection of highly motile sperm without the use of damaging centrifugation. This technology ensures higher DNA integrity and improved fertilization potential

- Automated sperm selection systems now include intelligent sorting algorithms capable of distinguishing viable sperm cells based on motility and morphology. These systems minimize human error, reduce procedural time, and improve reproducibility across fertility clinics

- The seamless integration of sperm separation devices with assisted reproductive platforms such as IVF and ICSI systems allows clinicians to streamline workflows, reduce contamination risks, and maintain higher sperm quality through closed-system designs. This creates a more effective and hygienic procedure for patients and practitioners alike

- This trend towards more intelligent, efficient, and clinically optimized sperm selection systems is fundamentally reshaping the landscape of male infertility treatment. Consequently, companies such as Memphasys and DxNow are actively developing next-generation microfluidic and magnetic separation platforms that prioritize sperm DNA integrity, automation, and ease of use

- The demand for sperm separation devices that offer non-invasive, reproducible, and clinically superior performance is growing rapidly across both advanced fertility centers and emerging markets, as patients and providers increasingly prioritize effective and patient-friendly reproductive technologies

Sperm Separation Devices Market Dynamics

Driver

“Growing Demand Due to Rising Infertility Rates and Advancements in Assisted Reproductive Technology (ART)”

- The increasing prevalence of infertility among men and couples worldwide, coupled with advancements in assisted reproductive technologies, is a significant driver for the growing adoption of sperm separation devices

- For instance, in March 2024, Memphasys Ltd. announced new clinical trial results for its Felix device, which uses electrophoresis and membrane separation to isolate high-quality sperm, improving ART success rates. Such innovations are expected to accelerate the growth of the sperm separation devices market during the forecast period

- As awareness around male infertility rises and more couples seek fertility assistance, sperm separation devices are gaining importance for their role in selecting motile, morphologically normal, and DNA-intact sperm, critical for successful fertilization and pregnancy

- Furthermore, the growing number of IVF and ICSI procedures globally is increasing the demand for sperm selection tools that can improve outcomes by reducing DNA fragmentation and selecting viable sperm with greater accuracy

- The convenience of newer, non-invasive, microfluidic-based separation techniques, along with the desire for improved pregnancy outcomes and patient-friendly procedures, is propelling the adoption of sperm separation devices in both high- and middle-income healthcare markets. The trend toward personalized and precision reproductive treatments further contributes to this demand

Restraint/Challenge

“High Device Costs and Limited Access in Developing Regions”

- Despite technological advancements, the high cost associated with advanced sperm separation devices and limited access in resource-constrained settings pose significant challenges to broader market penetration. Many of these devices incorporate proprietary microfluidic technology or automation, which increases the overall cost

- For instance, devices such as the Zymot multi or ICSI-specific separation chips, while highly effective, are priced higher than conventional methods such as density gradient centrifugation, creating barriers for smaller clinics or public hospitals in low-income regions

- In addition, there is a lack of trained professionals and limited awareness about advanced sperm selection techniques in developing countries, which hinders adoption even when devices are available

- Addressing these challenges will require increased investment in cost-effective device development, partnerships with public health systems, and training programs to broaden accessibility. Moreover, educating healthcare providers and patients on the clinical benefits of improved sperm separation—such as higher fertilization success rates and lower miscarriage risks—will be crucial to driving adoption

- Without efforts to reduce device pricing and improve healthcare infrastructure, the benefits of sperm separation technologies risk being limited to high-resource settings, slowing down global market expansion

Sperm Separation Devices Market Scope

The market is segmented on the basis of devices, media, assisted devices, technology, application, end user and distribution channel

- By Devices

On the basis of devices, the market is segmented into centrifugation devices, centrifugation-free devices, and others. The centrifugation devices segment dominated the market with the largest revenue share of 57.4% in 2024, owing to their established use in fertility clinics and IVF laboratories for sperm purification and quality assessment.

The Centrifugation-Free Devices segment is projected to witness the fastest CAGR of 15.8% from 2025 to 2032, driven by increasing demand for less invasive, faster, and more sperm-friendly methods such as microfluidic technologies.

- By Media

On the basis of media, the market is segmented into sperm washing media, sperm freezing media, and others. The sperm washing media segment held the largest revenue share of 33.6% in 2024, due to its widespread use in preparing sperm for intrauterine insemination (IUI) and IVF procedures.

The Sperm Freezing Media segment is anticipated to witness the fastest CAGR of 14.5% during 2025–2032, as demand grows for long-term sperm storage solutions for fertility preservation, especially among cancer patients and sperm donors.

- By Assisted Devices

On the basis of assisted devices, the market is segmented into incubators, imaging systems, and others. The incubators segment dominated the assisted devices market with a revenue share of 37.9% in 2024, owing to their critical role in maintaining optimal sperm viability during the processing phase.

The imaging systems segment is projected to expand at the highest CAGR of 13.4% from 2025 to 2032, driven by innovations in motility and morphology tracking to enhance sperm selection accuracy.

- By Technology

On the basis of technology, the market is segmented into electrophoresis, on-chip technology, and others. The electrophoresis segment captured the largest share of 45.2% in 2024, favored for its high efficiency in separating healthy and motile sperm with minimal DNA fragmentation.

The on-chip technology segment is expected to grow at the fastest CAGR of 17.3% from 2025 to 2032, due to its promise in non-invasive, real-time sperm sorting integrated within microfluidic lab-on-a-chip platforms.

- By Application

On the basis of application, the market is segmented into fertility, diagnostics, and others. The Fertility segment dominated with the highest share of 66.1% in 2024, as the primary driver for sperm separation technologies lies in assisted reproductive treatments such as IVF and ICSI.

The diagnostics segment is forecast to grow at the fastest CAGR of 14.9% from 2025 to 2032, due to increasing male infertility testing and growing awareness around sperm DNA fragmentation analysis.

- By End User

On the basis of end user, the market is divided into Fertility centers and IVF laboratories, Cryobanks, and Others. The fertility centers and IVF laboratories segment accounted for the largest market share of 41.8% in 2024, driven by their routine and advanced use of sperm separation technologies for ART procedures.

The cryobanks segment is expected to register the highest CAGR of 15.1% during 2025–2032, as demand for sperm preservation and donor banking continues to rise globally.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct tender, third-party distributors, and others. The direct tender segment held the largest market share of 54.3% in 2024, largely due to direct procurement by hospitals, clinics, and research institutions.

The third-party distributors segment is expected to grow at the fastest CAGR of 13.7% from 2025 to 2032, driven by the expansion of regional distributor networks and digital B2B platforms.

The market is segmented intoSperm Separation Devices Market Regional Analysis

- North America dominated the sperm separation devices market with the largest revenue share of 38.7% in 2024, driven by increasing infertility rates, advancements in assisted reproductive technologies (ART), and growing awareness about male fertility treatments

- Consumers and fertility clinics in the region highly value the precision, efficiency, and improved success rates offered by sperm separation devices, which aid in enhancing outcomes in procedures such as in vitro fertilization (IVF) and intrauterine insemination (IUI)

- This widespread adoption is further supported by well-established healthcare infrastructure, rising investments in fertility research, and a growing number of fertility clinics, establishing sperm separation devices as a critical component in male infertility management across North America

U.S. Sperm Separation Devices Market Insight

The U.S. sperm separation devices market captured the largest revenue share in 2024. This dominant position is driven by heightened awareness of male infertility issues and the increasing adoption of advanced assisted reproductive technologies (ART) such as IVF and IUI. Fertility clinics and hospitals across the country are rapidly integrating sophisticated sperm separation devices to improve treatment success rates. The well-established healthcare infrastructure, coupled with significant investments in reproductive health research, continues to fuel demand. Moreover, supportive insurance coverage and government initiatives aimed at improving fertility treatments further bolster market growth in the U.S.

Europe Sperm Separation Devices Market Insight

The Europe sperm separation devices market is projected to expand at a substantial CAGR throughout the forecast period. The region’s growth is supported by rising infertility rates and increased government and private investments in reproductive healthcare technologies. Countries such as Germany, the U.K., and France are leading markets within Europe due to high patient awareness and access to advanced fertility clinics. The region’s stringent healthcare regulations and growing preference for precision-driven fertility treatments are major growth drivers. Additionally, delayed parenthood trends and lifestyle changes are contributing to increasing demand for sperm separation devices in both residential fertility services and clinical settings.

U.K. Sperm Separation Devices Market Insight

The U.K. sperm separation devices market is anticipated to grow at a noteworthy CAGR during the forecast period. The country’s market growth is supported by rising rates of male infertility and a robust network of fertility clinics. Government initiatives promoting reproductive health awareness, coupled with a growing patient preference for technologically advanced sperm separation devices, further strengthen the market. The U.K.’s well-developed healthcare infrastructure and thriving private fertility sector ensure continuous adoption of cutting-edge ART solutions.

Germany Sperm Separation Devices Market Insight

The Germany sperm separation devices market is expected to expand at a considerable CAGR during the forecast period. The market is propelled by the country’s focus on innovation in medical technologies, rising infertility awareness, and strong healthcare infrastructure. German fertility clinics emphasize precision and safety in sperm separation processes, driving demand for advanced devices. Moreover, Germany’s emphasis on sustainability and eco-friendly medical solutions contributes to the adoption of new-generation sperm separation technologies.

Asia-Pacific Sperm Separation Devices Market Insight

The Asia-Pacific sperm separation devices market emerged as the fastest-growing market segment in 2024 and is expected to have a CAGR of 8.5% in 2025 to 2032. This rapid growth is fueled by increasing infertility rates, expanding healthcare infrastructure, and rising disposable incomes in emerging economies such as India, China, Japan, and South Korea. Government initiatives to improve fertility healthcare access and growing public awareness are accelerating the adoption of sperm separation technologies. Additionally, the region’s expanding network of fertility clinics and technological advancements in ART further drive market penetration. The manufacturing boom in Asia-Pacific, particularly in China and India, is making devices more affordable and accessible to a broader population.

China Sperm Separation Devices Market Insight

The China sperm separation devices market accounted for the largest market revenue share in Asia Pacific in 2024, making it the largest contributor within the Asia-Pacific region. Factors contributing to China’s market share include rapid urbanization, a growing middle-class population with increased healthcare spending, and government initiatives aimed at advancing reproductive health services. China’s strong domestic manufacturing sector also helps reduce costs, making sperm separation devices more affordable. The country’s push toward smart fertility clinics and smart city development enhances the adoption of connected, technology-driven fertility solutions.

India Sperm Separation Devices Market Insight

The India sperm separation devices market captured about 10% of the global sperm separation devices market revenue share in 2024, reflecting its rising prominence within the Asia-Pacific region. Increasing infertility prevalence, growing public awareness about male reproductive health, and a surge in fertility clinics are key drivers. Government efforts to improve access to fertility treatments and a rising middle class with greater healthcare affordability further stimulate market growth. As the country continues to develop its healthcare infrastructure and increase investment in ART technologies, India is poised to become a major market for sperm separation devices in the coming years.

Sperm Separation Devices Market Share

The sperm separation devices industry is primarily led by well-established companies, including:

- CooperSurgical, Inc. (U.S.)

- Hamilton Thorne (U.S.)

- Menicon (Japan)

- Promega Corporation (U.S.)

- NidaCon International AB (Sweden)

- Bonraybio (Taiwan)

- SAR Healthline Pvt Ltd. (India)

- Memphasys (Australia)

- Sperm Processor (India)

- Hydrix Limited (Australia)

- Gennet (Czech Republic)

Latest Developments in Global Sperm Separation Devices Market

- In April 2024, Hamilton Thorne Ltd. (U.S.), a leader in precision laser and imaging systems for the fertility sector, announced the launch of its next-generation automated sperm analysis and separation system, ZyMōt X2. The advanced device enhances the separation of motile sperm with higher DNA integrity, supporting improved outcomes in assisted reproductive technologies (ART). This launch reinforces Hamilton Thorne’s commitment to innovation in reproductive health

- In March 2024, Memphasys Ltd. (Australia) received regulatory approval in India for its flagship sperm separation device, Felix. The device uses electrophoresis and size-exclusion membranes to select high-quality sperm non-invasively. The approval opens a large potential market, enhancing fertility treatment options in one of the world’s fastest-growing ART markets

- In February 2024, CooperSurgical Inc. (U.S.) expanded its ART portfolio by acquiring several new patents related to microfluidic sperm sorting technologies. These developments aim to improve the efficiency and safety of sperm preparation, particularly for use in intrauterine insemination (IUI) and in vitro fertilization (IVF)

- In January 2024, SAR Healthline Pvt Ltd. (India) introduced a cost-effective, single-use sperm separation kit for emerging markets. Designed for small to mid-sized fertility clinics, this launch aligns with the company's goal to improve access to fertility treatments across underserved regions in Asia and Africa

- In December 2023, Nidacon International AB (Sweden) partnered with leading fertility clinics in Europe to pilot its AI-integrated sperm selection platform. The system utilizes machine learning to analyze motility patterns and morphology in real-time, significantly boosting the accuracy of sperm separation processes and clinical outcomes

- In November 2023, Bonraybio (India) announced the development of a novel sperm preparation medium specifically tailored for high-viscosity semen samples. This innovation addresses a major challenge in male infertility treatments and has been well-received by embryologists in both domestic and Southeast Asian markets

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.