Global Sleep Apnea Monitoring Instruments Market

Market Size in USD Billion

CAGR :

%

USD

1.14 Billion

USD

1.76 Billion

2025

2033

USD

1.14 Billion

USD

1.76 Billion

2025

2033

| 2026 –2033 | |

| USD 1.14 Billion | |

| USD 1.76 Billion | |

| % | |

|

Sleep Apnea Monitoring Instruments Market Size

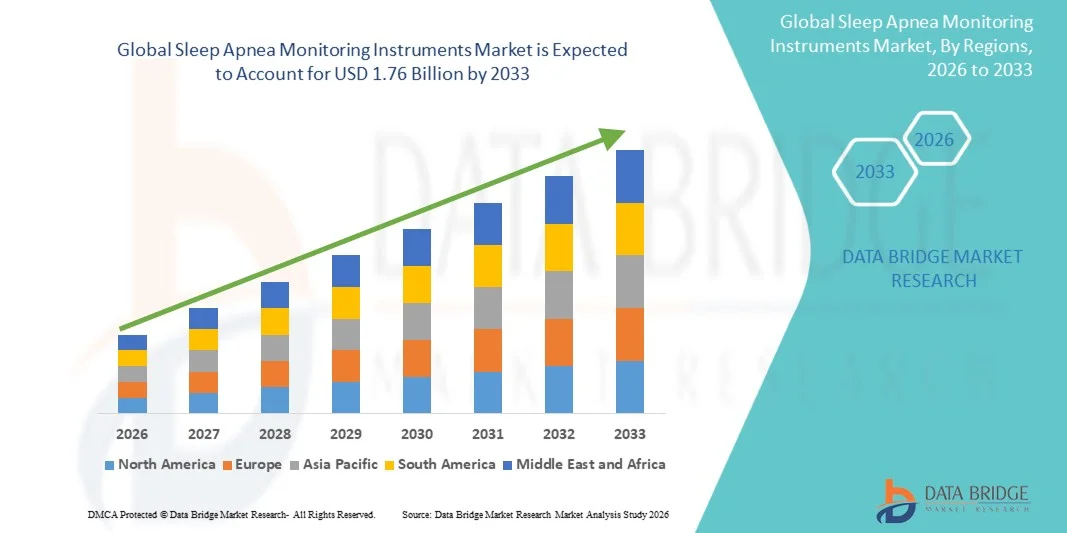

- The global sleep apnea monitoring instruments market size was valued at USD 1.14 billion in 2025 and is expected to reach USD 1.76 billion by 2033, at a CAGR of 5.65% during the forecast period

- The market growth is largely fueled by the rising prevalence of sleep disorders, particularly obstructive sleep apnea, along with increasing awareness regarding the importance of early diagnosis and continuous monitoring, leading to greater adoption of advanced sleep apnea monitoring instruments across hospitals, sleep laboratories, and home-care settings

- Furthermore, growing patient preference for portable, easy-to-use, and technologically advanced monitoring devices, combined with expanding telehealth integration and remote patient monitoring capabilities, is establishing sleep apnea monitoring instruments as essential tools in modern respiratory care. These converging factors are accelerating the uptake of sleep apnea monitoring solutions, thereby significantly boosting the industry’s growth

Sleep Apnea Monitoring Instruments Market Analysis

- Sleep apnea monitoring instruments, including polysomnography systems, portable sleep monitors, and wearable diagnostic devices, are becoming increasingly vital in modern healthcare due to their ability to enable early diagnosis, continuous monitoring, and effective management of sleep-related breathing disorders across both clinical and home-care settings.

- The escalating demand for sleep apnea monitoring instruments is primarily fueled by the rising prevalence of obstructive sleep apnea, increasing awareness of sleep health, growing adoption of home-based diagnostic solutions, and advancements in sensor technology, AI-driven analytics, and remote patient monitoring capabilities

- North America dominated the sleep apnea monitoring instruments market with the largest revenue share of 41.3% in 2025, supported by high diagnosis rates, well-established sleep clinics, favorable reimbursement policies, and strong adoption of technologically advanced monitoring devices, with the U.S. accounting for a major share due to widespread awareness and continuous product innovations by key market players

- Asia-Pacific is expected to be the fastest-growing region in the sleep apnea monitoring instruments market, registering a CAGR of 10.9% during the forecast period, driven by increasing urbanization, rising disposable incomes, a growing aging population, improving access to sleep diagnostic services, and expanding healthcare infrastructure across countries such as China, India, and Japan

- The therapeutic devices segment dominated the market, accounting for approximately 62.7% of the revenue share in 2025, primarily driven by the widespread use of Continuous Positive Airway Pressure (CPAP), BiPAP, and Automatic Positive Airway Pressure (APAP) systems for long-term sleep apnea management

Report Scope and Sleep Apnea Monitoring Instruments Market Segmentation

|

Attributes |

Sleep Apnea Monitoring Instruments Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Sleep Apnea Monitoring Instruments Market Trends

“Adoption of Advanced Wearable and Home-Based Sleep Monitoring Technologies”

- A significant and accelerating trend in the global sleep apnea monitoring instruments market is the increasing adoption of wearable and home-based sleep monitoring devices that enable convenient long-term respiratory tracking outside traditional sleep laboratories

- Manufacturers are developing compact, wireless, and patient-friendly monitoring systems capable of continuously tracking oxygen saturation, airflow, respiratory effort, and sleep patterns, improving early diagnosis and treatment compliance

- For instance, modern home sleep testing (HST) devices allow patients to conduct overnight sleep assessments in their homes, reducing hospital visits and lowering diagnostic costs while maintaining clinically reliable data collection

- Integration of cloud-based data platforms is also enabling physicians to remotely access patient sleep data, facilitating real-time monitoring and personalized treatment adjustments

- Furthermore, increasing patient preference for minimally intrusive monitoring solutions is encouraging the development of lightweight wearable sensors and patch-based monitoring technologies designed to enhance comfort and long-term usability

- This shift toward portable, home-centered sleep diagnostics is transforming sleep apnea detection and management, supporting wider screening coverage and earlier intervention

Sleep Apnea Monitoring Instruments Market Dynamics

Driver

“Rising Prevalence of Sleep Disorders and Growing Awareness of Early Diagnosis”

- The rising global prevalence of obstructive sleep apnea (OSA), driven by increasing obesity rates, aging populations, and sedentary lifestyles, is a major factor accelerating demand for sleep apnea monitoring instruments

- For instance, the growing number of patients undergoing routine sleep disorder screening programs in hospitals and sleep clinics is significantly increasing the utilization of diagnostic monitoring systems

- Increasing awareness among healthcare providers and patients regarding the health risks associated with untreated sleep apnea—such as cardiovascular diseases, hypertension, and metabolic disorders—is encouraging early diagnostic testing

- Expansion of sleep disorder treatment centers and improved insurance coverage for sleep testing in several developed countries are further strengthening market demand

- In addition, the rapid growth of telehealth services and remote patient monitoring programs is supporting wider adoption of portable sleep monitoring devices across both clinical and home-care environments

Restraint/Challenge

“High Diagnostic Costs and Limited Access to Specialized Sleep Laboratories”

- High costs associated with advanced diagnostic monitoring systems and sleep laboratory testing procedures remain a key challenge, particularly in low- and middle-income regions where access to specialized sleep centers is limited

- For instance, full polysomnography testing conducted in hospital sleep laboratories can be expensive, leading many patients to delay diagnosis and treatment

- Variability in reimbursement policies for sleep testing across different healthcare systems can also influence adoption rates of advanced monitoring instruments

- In addition, limited awareness about sleep apnea symptoms in certain populations results in underdiagnosis, reducing timely utilization of monitoring technologies

- Addressing these challenges through expansion of affordable home-based monitoring solutions, awareness campaigns, and improved reimbursement frameworks will be essential for sustaining long-term growth in the Sleep Apnea Monitoring Instruments market

Sleep Apnea Monitoring Instruments Market Scope

The market is segmented on the basis of product and end users.

• By Product

On the basis of product, the Global Sleep Apnea Monitoring Instruments market is segmented into Therapeutic Devices and Diagnostic Devices. The therapeutic devices segment dominated the market, accounting for approximately 62.7% of the revenue share in 2025, primarily driven by the widespread use of Continuous Positive Airway Pressure (CPAP), BiPAP, and Automatic Positive Airway Pressure (APAP) systems for long-term sleep apnea management. These devices are essential for maintaining airway patency during sleep, making them the primary treatment solution for moderate to severe obstructive sleep apnea patients. The growing global prevalence of obesity and lifestyle-related respiratory disorders has significantly increased demand for therapeutic sleep apnea devices. Rising awareness regarding untreated sleep apnea complications, including cardiovascular risks and daytime fatigue, further encourages treatment adoption. Technological advancements such as quieter motors, portable designs, and integrated wireless connectivity improve patient comfort and compliance. Increasing reimbursement coverage for CPAP therapy in developed countries also supports segment dominance. Healthcare providers strongly recommend therapeutic devices as the first-line treatment, ensuring continuous product demand. Expansion of sleep disorder clinics and respiratory therapy programs further contributes to usage growth. In addition, the growing aging population worldwide increases the incidence of sleep-related breathing disorders. Continuous innovation in mask design and humidification technologies enhances therapy adherence. As treatment compliance remains a key clinical priority, therapeutic devices are expected to maintain their leading position throughout the forecast period.

The diagnostic devices segment is projected to witness the fastest growth, registering a CAGR of approximately 8.9% from 2026 to 2033, driven by increasing emphasis on early diagnosis and screening of sleep disorders. Diagnostic devices, including polysomnography (PSG) systems and home sleep apnea testing (HSAT) monitors, are gaining significant traction due to their ability to identify sleep apnea conditions accurately. Growing awareness campaigns encouraging early diagnosis of sleep apnea significantly boost testing rates. The rising adoption of portable and wearable sleep monitoring technologies further accelerates segment growth. Home-based diagnostic testing solutions offer convenience and cost-effectiveness, encouraging patient adoption and expanding market penetration. Increasing investments in sleep research and diagnostic infrastructure also support growth. Technological advancements enabling wireless connectivity, cloud-based reporting, and AI-assisted sleep data analysis improve diagnostic efficiency. Healthcare systems focusing on preventive healthcare and early intervention strategies further drive demand. Expansion of telemedicine and remote patient monitoring services enhances accessibility to diagnostic testing. Growing physician referrals for sleep studies due to increased recognition of sleep apnea complications further contribute to demand. Favorable reimbursement policies for diagnostic testing in several developed markets strengthen adoption. These factors collectively position diagnostic devices as the fastest-growing product segment.

• By End Users

On the basis of end users, the Sleep Apnea Monitoring Instruments market is segmented into Hospitals, Home Healthcare, Sleep Laboratories, and Others. Hospitals accounted for the largest market revenue share of approximately 38.9% in 2025, driven by the high volume of sleep disorder diagnosis and treatment procedures conducted in hospital settings. Hospitals are equipped with advanced diagnostic infrastructure, including polysomnography systems, enabling accurate detection of complex sleep apnea cases. The presence of specialized respiratory and neurology departments ensures continuous patient inflow for diagnosis and treatment. Hospitals also manage severe sleep apnea cases requiring multidisciplinary care, strengthening their market share. Increasing hospital admissions related to respiratory and cardiovascular conditions further contribute to demand. Government healthcare investments aimed at improving hospital-based diagnostic services support segment dominance. Availability of trained sleep specialists and respiratory therapists enhances procedural reliability and patient outcomes. Hospitals frequently establish integrated sleep centers, increasing service capacity and device utilization. Favorable reimbursement policies for hospital-based sleep studies further boost patient testing volumes. Bulk procurement agreements for therapeutic and diagnostic devices also strengthen hospital usage. Rising awareness among physicians regarding the health risks associated with untreated sleep apnea increases hospital referrals. These combined factors ensure hospitals remain the dominant end-user segment throughout the forecast period.

Home healthcare is expected to witness the fastest growth, expanding at a CAGR of approximately 9.6% from 2026 to 2033, driven by the increasing shift toward home-based diagnosis and long-term therapy management. The growing availability of portable CPAP devices and home sleep apnea testing systems significantly supports adoption in residential settings. Patients increasingly prefer home-based monitoring due to comfort, convenience, and reduced hospital visits. Expansion of telehealth platforms enabling remote monitoring and physician consultations further accelerates growth. Aging populations and rising prevalence of chronic respiratory conditions increase the need for long-term home therapy solutions. Healthcare systems focusing on cost reduction are encouraging home-based care models, supporting segment expansion. Technological advancements enabling smartphone-connected monitoring devices improve therapy adherence and patient engagement. Increasing reimbursement coverage for home sleep apnea testing in several developed markets also drives adoption. Manufacturers are introducing compact, user-friendly devices specifically designed for home use, further strengthening demand. Growth in remote patient monitoring programs enhances the adoption of connected therapeutic devices. Rising patient awareness regarding sleep health management contributes to market penetration. These factors collectively position home healthcare as the fastest-growing end-user segment in the sleep apnea monitoring instruments market.

Sleep Apnea Monitoring Instruments Market Regional Analysis

- North America dominated the sleep apnea monitoring instruments market with the largest revenue share of 41.3% in 2025, supported by high diagnosis rates, well-established sleep clinics, favorable reimbursement policies, and strong adoption of technologically advanced monitoring devices

- The region also benefits from the presence of leading medical device manufacturers, continuous technological innovation in home sleep testing systems, and growing awareness of sleep disorders among patients and healthcare professionals

- Increasing adoption of portable and wearable sleep monitoring technologies for home-based diagnostics is further strengthening regional market growth

U.S. Sleep Apnea Monitoring Instruments Market Insight

The U.S. sleep apnea monitoring instruments market captured the largest revenue share within North America in 2025, driven by widespread awareness of sleep apnea, strong healthcare spending, and continuous product innovations by major industry players. The country’s advanced healthcare infrastructure, growing use of home sleep apnea testing (HSAT) devices, and increasing adoption of remote patient monitoring technologies are further accelerating market expansion. In addition, favorable insurance coverage for sleep disorder diagnostics and treatment significantly supports the adoption of monitoring instruments across hospitals, sleep laboratories, and home-care settings.

Europe Sleep Apnea Monitoring Instruments Market Insight

The Europe sleep apnea monitoring instruments market is projected to expand at a substantial CAGR during the forecast period, primarily driven by the increasing prevalence of sleep disorders, growing geriatric population, and improved awareness regarding early diagnosis. Government-supported healthcare programs and expanding access to sleep diagnostic services across countries such as Germany, France, and the U.K. are further encouraging adoption of advanced monitoring devices. In addition, the rising use of portable and home-based diagnostic systems is contributing to regional growth.

U.K. Sleep Apnea Monitoring Instruments Market Insight

The U.K. sleep apnea monitoring instruments market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by increasing screening initiatives for sleep disorders, improved referral systems through national healthcare programs, and growing awareness among patients regarding the long-term health risks associated with untreated sleep apnea. The increasing availability of home-based sleep testing devices and telemonitoring solutions is also boosting market adoption across the country.

Germany Sleep Apnea Monitoring Instruments Market Insight

The Germany sleep apnea monitoring instruments market is expected to expand at a considerable CAGR, driven by strong healthcare infrastructure, a high prevalence of sleep-related breathing disorders, and increasing adoption of technologically advanced diagnostic equipment in sleep laboratories and hospitals. Rising demand for accurate and efficient monitoring systems, along with growing utilization of portable sleep diagnostic devices, is further supporting market growth in the country.

Asia Pacific Sleep Apnea Monitoring Instruments Market Insight

Asia-Pacific sleep apnea monitoring instruments market is expected to be the fastest-growing region, registering a CAGR of 10.9% during the forecast period, driven by increasing urbanization, rising disposable incomes, a growing aging population, improving access to sleep diagnostic services, and expanding healthcare infrastructure across countries such as China, India, and Japan. Increasing awareness of sleep disorders and the gradual expansion of private sleep clinics are also contributing to regional demand for monitoring instruments.

Japan Sleep Apnea Monitoring Instruments Market Insight

The Japan sleep apnea monitoring instruments market is gaining momentum due to the country’s rapidly aging population, increasing prevalence of sleep apnea among elderly individuals, and strong adoption of technologically advanced medical monitoring devices. The growing use of wearable sleep monitoring systems and expansion of home-care diagnostic solutions are further driving market growth.

China Sleep Apnea Monitoring Instruments Market Insight

The China sleep apnea monitoring instruments market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s large patient population, expanding healthcare infrastructure, and increasing awareness regarding sleep-related disorders. Government initiatives aimed at improving healthcare access, rising investments in hospital infrastructure, and the increasing availability of cost-effective diagnostic devices are key factors supporting market expansion in China.

Sleep Apnea Monitoring Instruments Market Share

The Sleep Apnea Monitoring Instruments industry is primarily led by well-established companies, including:

- ResMed Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Fisher & Paykel Healthcare (New Zealand)

- Medtronic plc (Ireland)

- Nihon Kohden Corporation (Japan)

- Natus Medical Incorporated (U.S.)

- Masimo Corporation (U.S.)

- BMC Medical Co., Ltd. (China)

- Compumedics Limited (Australia)

- SOMNOmedics GmbH (Germany)

- Löwenstein Medical Technology (Germany)

- Drive DeVilbiss Healthcare (U.S.)

- Itamar Medical Ltd. (Israel)

- Cadwell Industries, Inc. (U.S.)

- Neurovirtual (Italy)

- CleveMed, Inc. (U.S.)

- Advanced Brain Monitoring, Inc. (U.S.)

- Medical Depot, Inc. (U.S.)

- React Health (U.S.)

- Vyaire Medical, Inc. (U.S.)

Latest Developments in Global Sleep Apnea Monitoring Instruments Market

- In August 2021, ResMed, a leading sleep-technology company, announced the launch of its AirSense 11 continuous positive airway pressure (CPAP) device in the United States, featuring enhanced digital connectivity, patient-engagement tools, and integrated coaching functions designed to improve adherence to sleep apnea therapy. The introduction of AirSense 11 strengthened ResMed’s digital health ecosystem by integrating cloud-based monitoring and personalized therapy guidance, supporting improved patient outcomes and remote clinical monitoring

- In September 2021, Philips introduced the DreamStation 2 CPAP device globally, designed with a smaller form factor, simplified user interface, and advanced comfort features aimed at improving patient compliance and enabling remote monitoring through digital connectivity tools. This product introduction reflected Philips’ focus on connected sleep-therapy platforms that allow clinicians to monitor therapy performance remotely and enhance treatment effectiveness

- . In May 2023, Inspire Medical Systems received U.S. FDA approval to expand the indications of its Inspire Upper Airway Stimulation (UAS) system for a broader patient population with obstructive sleep apnea, allowing use among patients with higher body-mass-index (BMI) ranges. This regulatory expansion significantly increased the addressable patient pool for implantable sleep apnea monitoring and therapeutic devices, supporting wider clinical adoption

- In January 2024, Samsung announced the FDA authorization of its Galaxy Watch sleep apnea detection feature, which uses smartwatch sensors to monitor breathing interruptions and help identify potential obstructive sleep apnea risk. The feature marked a significant step toward wearable-based sleep apnea monitoring solutions, enabling early screening through consumer health devices integrated with mobile health ecosystem

- In December 2024, the U.S. FDA approved Eli Lilly’s Zepbound (tirzepatide) as the first medication indicated for treating moderate-to-severe obstructive sleep apnea in adults with obesity, based on clinical trials demonstrating significant reductions in apnea-hypopnea events. Although primarily a pharmaceutical development, the approval is expected to complement device-based monitoring and therapy solutions, reshaping the broader sleep apnea treatment ecosystem

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.