Global Skeletal Dysplasia Market

Market Size in USD Billion

CAGR :

%

USD

3.57 Billion

USD

5.49 Billion

2025

2033

USD

3.57 Billion

USD

5.49 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.57 Billion | |

| USD 5.49 Billion | |

| % | |

|

Skeletal Dysplasia Market Size

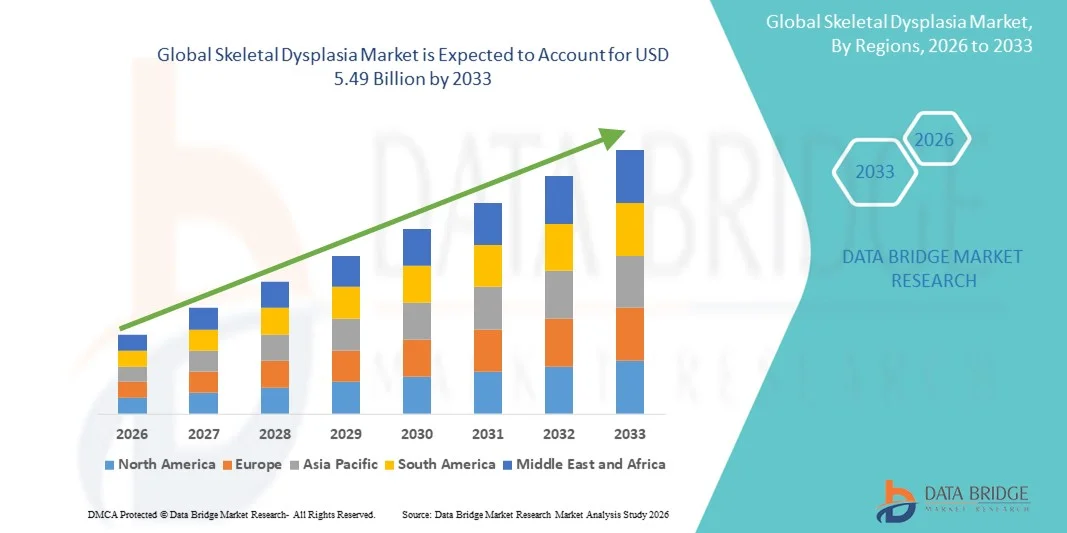

- The global skeletal dysplasia market size was valued at USD 3.57 billion in 2025 and is expected to reach USD 5.49 billion by 2033, at a CAGR of 5.51% during the forecast period

- The market growth is primarily driven by the increasing prevalence of rare genetic bone disorders, advancements in diagnostic technologies, and rising awareness of early detection and management of skeletal abnormalities

- Furthermore, the growing adoption of targeted therapies, personalized treatment approaches, and supportive care solutions for patients with skeletal dysplasia is enhancing patient outcomes and quality of life. These factors are collectively driving the demand for comprehensive skeletal dysplasia management solutions, thereby propelling the market’s growth

Skeletal Dysplasia Market Analysis

- Skeletal dysplasia, encompassing a group of rare genetic disorders affecting bone and cartilage growth, is increasingly recognized as a critical area in pediatric and genetic healthcare due to its impact on patient mobility, growth, and quality of life. Early diagnosis and specialized management are essential to mitigate complications and improve outcomes

- The rising demand for advanced diagnostic solutions, including genetic testing, imaging technologies, and personalized treatment approaches, is primarily driving market growth, alongside increasing awareness among healthcare providers and caregivers about early intervention

- North America dominated the skeletal dysplasia market with the largest revenue share of 38.4% in 2025, fueled by well-established healthcare infrastructure, high adoption of genetic testing and advanced imaging, and significant research and development activities by key players in rare disease therapeutics

- Asia-Pacific is expected to be the fastest growing region in the skeletal dysplasia market during the forecast period due to improving healthcare access, increasing government initiatives for rare diseases, and growing investment in pediatric and genetic healthcare infrastructure

- Achondroplasia segment dominated the skeletal dysplasia market with a market share of 42.8% in 2025, driven by its high prevalence among skeletal dysplasia types and the availability of specialized treatment and management options for affected patients

Report Scope and Skeletal Dysplasia Market Segmentation

|

Attributes |

Skeletal Dysplasia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Skeletal Dysplasia Market Trends

Advancements in Genetic Testing and Early Diagnosis

- A major and accelerating trend in the global skeletal dysplasia market is the increasing adoption of advanced genetic testing technologies, enabling early and accurate diagnosis of rare bone disorders and personalized treatment planning

- For instance, next-generation sequencing panels are now widely used to identify mutations in genes such as FGFR3, COL1A1, and COL1A2, helping clinicians classify skeletal dysplasia types and guide management decisions

- Integration of genetic testing with advanced imaging modalities, such as 3D CT scans and MRI, allows for comprehensive evaluation of skeletal abnormalities and better prediction of growth patterns and potential complications

- This trend is also fostering the development of digital health platforms that combine genetic data, imaging results, and patient history to provide clinicians with actionable insights for individualized care

- Consequently, companies such as Invitae and Blueprint Genetics are focusing on expanding their genetic testing panels and bioinformatics tools to offer more precise, early-stage diagnostic solutions for patients with skeletal dysplasia

- The growing emphasis on early and accurate diagnosis is driving investments in R&D and fostering collaborations between genetic testing providers, hospitals, and research institutes, enhancing market penetration globally

- In addition, telemedicine and remote consultation services are being increasingly leveraged to provide specialized care and genetic counseling to patients in remote or underserved areas, improving access to skeletal dysplasia expertise

- Furthermore, artificial intelligence and machine learning tools are being integrated into diagnostic workflows to analyze imaging and genetic data more efficiently, reducing diagnostic delays and enabling more accurate classification of skeletal dysplasia types

Skeletal Dysplasia Market Dynamics

Driver

Increasing Prevalence of Rare Bone Disorders and Personalized Therapies

- The rising prevalence of skeletal dysplasia and other rare genetic bone disorders, coupled with advancements in personalized therapies, is a significant driver for the growth of the skeletal dysplasia market

- For instance, in March 2025, BioMarin Pharmaceutical expanded its clinical trials for vosoritide, a targeted therapy for achondroplasia, aiming to improve bone growth outcomes in pediatric patients

- Growing awareness among healthcare providers and caregivers regarding early diagnosis and timely intervention is also driving the adoption of advanced management solutions for skeletal dysplasia patients

- Furthermore, the increasing availability of targeted pharmacological therapies, surgical interventions, and multidisciplinary care approaches is enhancing patient outcomes and driving market demand

- The focus on individualized treatment strategies, including gene-based and biologic therapies, is encouraging investments by pharmaceutical companies and research institutes to develop novel solutions addressing the unique needs of skeletal dysplasia patients

- Rising patient advocacy initiatives and support programs are also contributing to increased diagnosis rates and better access to specialized care, further propelling market growth

- In addition, partnerships between hospitals, research institutions, and biotechnology companies are accelerating the development and commercialization of novel therapies for rare skeletal disorders

- Advances in pediatric orthopedic surgery techniques and minimally invasive interventions are improving clinical outcomes and reducing recovery times, making surgical management a more attractive and feasible option for patients

Restraint/Challenge

High Treatment Costs and Limited Access in Emerging Regions

- The high cost of specialized therapies, surgical procedures, and genetic testing for skeletal dysplasia poses a significant challenge to broader market adoption, particularly in low- and middle-income countries

- For instance, limited access to targeted therapies such as vosoritide or enzyme replacement treatments in emerging markets can delay intervention and restrict treatment availability for patients in need

- In addition, the complexity of managing skeletal dysplasia, which often requires multidisciplinary care involving geneticists, orthopedic surgeons, and pediatricians, can increase overall healthcare costs and logistical challenges

- Insurance coverage limitations and reimbursement issues for rare disease treatments further exacerbate the financial burden for patients and families, slowing market penetration

- While awareness and diagnostic capabilities are improving, affordability and accessibility challenges continue to restrict widespread adoption, particularly in regions with underdeveloped healthcare infrastructure

- Overcoming these challenges through cost-effective therapies, government support programs, and expanded access to genetic testing and treatment facilities will be critical for sustained market growth

- Inadequate trained medical professionals and specialists in rare bone disorders can hinder timely diagnosis and proper management, limiting market expansion in certain regions

- Regulatory hurdles related to clinical trials, approval of novel therapies, and cross-border genetic testing can delay product launches and restrict the availability of new treatment options for skeletal dysplasia patients

Skeletal Dysplasia Market Scope

The market is segmented on the basis of type, treatment, and end users.

- By Type

On the basis of type, the skeletal dysplasia market is segmented into achondroplasia, hypochondroplasia, thanatophoric dysplasia, osteogenesis imperfecta, and others. The Achondroplasia segment dominated the market with the largest revenue share of 42.8% in 2025, driven by its high prevalence among skeletal dysplasia types and increasing availability of specialized treatment options. Patients with Achondroplasia often require continuous medical monitoring, orthopedic interventions, and growth-targeted therapies, which contributes significantly to market revenue. The segment also benefits from ongoing research and clinical trials, particularly for novel pharmacological agents such as vosoritide. In addition, the awareness campaigns and patient advocacy programs targeting Achondroplasia are helping in early diagnosis and intervention, further consolidating its market dominance. Hospitals and specialty clinics prioritize resources for managing Achondroplasia due to its clinical significance and demand for comprehensive care.

The Thanatophoric Dysplasia segment is expected to witness the fastest growth rate of 18.5% from 2026 to 2033, driven by advancements in prenatal diagnostics and early genetic testing. Improved ultrasound and genetic screening techniques are enabling earlier detection, which is critical for clinical decision-making and parental counseling. The growth is also supported by increasing investments in rare disease research and rising government initiatives for neonatal and pediatric healthcare. Enhanced awareness among clinicians and parents about Thanatophoric Dysplasia management contributes to the faster adoption of diagnostic and supportive care solutions. Emerging markets with improving healthcare infrastructure are gradually increasing accessibility to advanced diagnostics for this rare condition.

- By Treatment

On the basis of treatment, the skeletal dysplasia market is segmented into medication, surgery, and others. The Medication segment dominated the market with a market share of 41.7% in 2025, driven by the increasing use of targeted therapies such as growth-promoting agents and enzyme replacement treatments for certain genetic bone disorders. Medications are preferred due to their non-invasive nature and ability to address underlying pathophysiological mechanisms, providing improved outcomes in both pediatric and adult patients. Clinical trials and approvals of new drugs continue to expand the available treatment options, further boosting market revenue. The demand is further fueled by personalized medicine approaches, where therapy is tailored to specific genetic mutations and patient profiles.

The Surgery segment is expected to witness the fastest CAGR from 2026 to 2033, driven by advancements in minimally invasive orthopedic procedures and corrective surgeries that improve mobility and quality of life. Surgical interventions are often necessary for severe skeletal deformities or growth-related complications, and innovations in surgical techniques are making procedures safer and more effective. Increasing adoption of multidisciplinary care combining surgery with physiotherapy and rehabilitation is also supporting market growth. Rising investments in pediatric orthopedic facilities in emerging regions are contributing to the faster expansion of this segment.

- By End Users

On the basis of end users, the skeletal dysplasia market is segmented into hospitals, ambulatory surgical centres, and others. The Hospitals segment dominated the market with the largest revenue share of 45.6% in 2025, driven by the presence of advanced diagnostic facilities, specialized orthopedic and genetic departments, and access to multidisciplinary care teams. Hospitals are the preferred choice for patients due to their ability to provide comprehensive treatment, long-term monitoring, and post-surgical rehabilitation services. High patient trust, established clinical expertise, and availability of advanced equipment further contribute to the dominance of this segment. The growing number of pediatric and rare disease centers in tertiary hospitals is also fueling revenue growth.

The Ambulatory Surgical Centres segment is expected to witness the fastest growth rate of 19.2% from 2026 to 2033, driven by the increasing preference for outpatient procedures and minimally invasive surgeries. These centers offer cost-effective solutions, shorter recovery times, and convenience for patients requiring corrective orthopedic interventions or minor surgical procedures. Expanding healthcare infrastructure and rising awareness about ambulatory care benefits are boosting the adoption of such centers for skeletal dysplasia management, particularly in urban and semi-urban regions. Emerging regions are witnessing gradual growth in outpatient surgical facilities with specialized pediatric orthopedic services, supporting segment expansion.

Skeletal Dysplasia Market Regional Analysis

- North America dominated the skeletal dysplasia market with the largest revenue share of 38.4% in 2025, fueled by well-established healthcare infrastructure, high adoption of genetic testing and advanced imaging, and significant research and development activities by key players in rare disease therapeutics

- Patients and caregivers in the region highly value early diagnosis, targeted therapies, and multidisciplinary care approaches, which are widely available through specialized hospitals and rare disease centers

- This widespread adoption is further supported by significant R&D investments, strong government initiatives for rare diseases, and high awareness among healthcare providers and patient communities, establishing North America as a leading market for skeletal dysplasia management solutions

U.S. Skeletal Dysplasia Market Insight

The U.S. skeletal dysplasia market captured the largest revenue share of 42% in 2025 within North America, driven by high adoption of advanced genetic testing and targeted therapies for rare bone disorders. Patients and caregivers are increasingly prioritizing early diagnosis and personalized treatment plans, supported by well-established healthcare infrastructure. The growing prevalence of pediatric skeletal conditions, combined with government initiatives for rare diseases and strong patient advocacy programs, further propels market growth. Moreover, the availability of specialized orthopedic and genetic centers, along with multidisciplinary care teams, significantly contributes to improved patient outcomes and market expansion.

Europe Skeletal Dysplasia Market Insight

The Europe skeletal dysplasia market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising awareness of rare bone disorders and advanced healthcare infrastructure. Increasing urbanization, along with growing investments in pediatric and genetic care, is fostering the adoption of early diagnostic and therapeutic solutions. European patients and caregivers are drawn to specialized treatment programs, integrated care approaches, and access to clinical trials for innovative therapies. The market is witnessing growth across hospitals, specialty clinics, and research institutions, with skeletal dysplasia management being incorporated into both new and existing healthcare frameworks.

U.K. Skeletal Dysplasia Market Insight

The U.K. skeletal dysplasia market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the rising trend of early genetic testing and personalized therapy adoption. In addition, increasing awareness of rare bone disorders and government support programs for rare diseases are encouraging timely diagnosis and treatment. The U.K.’s robust healthcare system and focus on multidisciplinary care further stimulate market growth. Patients benefit from access to specialized centers, pediatric orthopedic care, and advanced diagnostic technologies, which together enhance disease management and improve quality of life.

Germany Skeletal Dysplasia Market Insight

The Germany skeletal dysplasia market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of rare skeletal disorders and demand for technologically advanced diagnostic and treatment solutions. Germany’s strong healthcare infrastructure, emphasis on innovation, and availability of genetic and orthopedic expertise promote the adoption of skeletal dysplasia management solutions. Hospitals and specialty clinics are increasingly integrating multidisciplinary care programs, while government initiatives for rare disease research and support enhance accessibility to therapies. Patients are also benefiting from improved diagnostic accuracy and access to novel treatments.

Asia-Pacific Skeletal Dysplasia Market Insight

The Asia-Pacific skeletal dysplasia market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by improving healthcare infrastructure, rising awareness of rare diseases, and increasing investment in pediatric care in countries such as China, Japan, and India. The region’s growing inclination toward early diagnosis, supported by government initiatives and private healthcare expansion, is driving the adoption of genetic testing and targeted therapies. Furthermore, emerging markets in APAC are witnessing better access to specialty care centers and affordable treatment options, broadening the patient base and supporting market growth.

Japan Skeletal Dysplasia Market Insight

The Japan skeletal dysplasia market is gaining momentum due to the country’s advanced healthcare system, high awareness of genetic disorders, and increasing focus on early intervention. Japanese patients benefit from access to specialized pediatric orthopedic care, multidisciplinary clinics, and innovative treatment options. The integration of genetic testing, imaging technologies, and personalized therapies is fueling market growth. In addition, rising government support for rare disease research and the availability of clinical trials contribute to enhanced disease management and market expansion.

India Skeletal Dysplasia Market Insight

The India skeletal dysplasia market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to improving healthcare access, increasing awareness of rare genetic disorders, and rapid urbanization. India is witnessing growing adoption of genetic testing, pediatric orthopedic services, and targeted therapies for skeletal dysplasia patients. The push towards advanced pediatric care facilities, government initiatives supporting rare diseases, and the availability of cost-effective treatment options are key factors propelling the market. Increasing patient education and awareness campaigns are also driving early diagnosis and improved disease management.

Skeletal Dysplasia Market Share

The Skeletal Dysplasia industry is primarily led by well-established companies, including:

- BioMarin (U.S.)

- Amgen Inc. (U.S.)

- Merck & Co., Inc. (Germany)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Alexion Pharmaceuticals, Inc. (U.S.)

- Ipsen S.A. (France)

- AstraZeneca (U.K.)

- Cipla (India)

- Eli Lilly and Company (U.S.)

- F. Hoffmann-La Roche AG (Switzerland)

- Pfizer, Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Ultragenyx Pharmaceutical Inc. (U.S.)

- Ascendis Pharma A/S (Denmark)

- BridgeBio Pharma, Inc. (U.S.)

- Kyowa Kirin Co., Ltd. (Japan)

- AbbVie Inc. (U.S.)

- Sanofi (France)

- Johnson & Johnson Services, Inc. (U.S.)

- Novartis AG (Switzerland)

What are the Recent Developments in Global Skeletal Dysplasia Market?

- In May 2025, VOXZOGO (vosoritide) was shown to significantly improve tibial bowing a common orthopedic complication in children with Achondroplasia, marking a shift from height‑only outcomes to functional bone improvements

- In March 2025, real‑world data for VOXZOGO in children under 3 demonstrated favorable safety and strong adherence, with no reported treatment‑related adverse events over nearly 2 years of follow-up supporting its use even in very young patients

- In November 2024, Infigratinib an oral FGFR3 inhibitor posted positive 18‑month results in the PROPEL 2 trial in children with achondroplasia, showing sustained increases in annualized height velocity (≈ +2.50 cm/year) and no serious adverse effects. These results were published in The New England Journal of Medicine

- In September 2024, the U.S. Food and Drug Administration (FDA) granted Breakthrough Therapy Designation to Infigratinib for achondroplasia the first-ever investigational therapeutic option for this condition to receive that designation highlighting its potential as a first-in-class oral treatment

- In June 2024, VOXZOGO data presented from an investigator-led study showed that treated children with achondroplasia experienced increased bone length while maintaining bone strength after long‑term therapy addressing concerns about whether growth comes at the cost of bone fragility

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.