Global Serverless Architecture Market

Market Size in USD Billion

CAGR :

%

USD

19.10 Billion

USD

70.50 Billion

2024

2032

USD

19.10 Billion

USD

70.50 Billion

2024

2032

| 2025 - 2032 | |

| USD 19.10 Billion | |

| USD 70.50 Billion | |

| % | |

|

Serverless Architecture Market Size

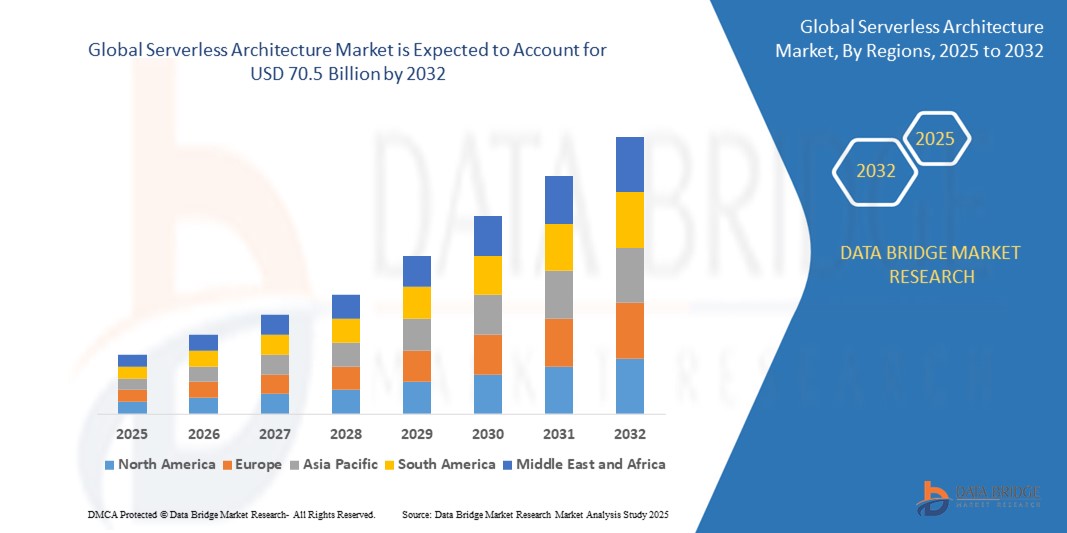

- The Global Serverless Architecture Market size was valued at USD 19.1 billion in 2024 and is expected to reach USD 70.5 billion by 2032, at a CAGR of 21% during the forecast period.

- Serverless architectures are revolutionizing the software development lifecycle by removing infrastructure management responsibilities, enabling developers to focus solely on writing and deploying code. This growth is driven by the demand for agile development, cost reduction, and enhanced scalability across sectors.

Serverless Architecture Market Analysis

- Serverless computing represents a transformative shift in application development and infrastructure management. It allows organizations to execute code on-demand without provisioning or managing underlying servers, enabling faster deployments, reduced operational complexity, and optimized cost structures. Positioned at the intersection of DevOps, microservices, and event-driven architecture, serverless platforms are becoming critical for modern cloud-native development.

- Services form the largest component of the market, encompassing managed cloud functions, backend integration, monitoring, and developer support. These services provide the backbone for abstracted infrastructure that enables seamless scalability and high availability. Software solutions, including serverless orchestration frameworks, logging tools, and function runtimes, support deployment automation and observability. Though hardware is a less prominent segment, edge devices and data center infrastructure supporting serverless workloads play a vital role in reducing latency and enhancing responsiveness, especially in edge computing use cases.

- On the technology front, Function-as-a-Service (FaaS) dominates due to its flexibility and efficiency in handling asynchronous workloads. It enables event-driven architectures where compute resources are automatically triggered by pre-defined events. Backend-as-a-Service (BaaS) complements FaaS by providing serverless backend capabilities such as databases, authentication, and storage—essential for rapid mobile and web application development. Automation & Control, including serverless CI/CD pipelines and infrastructure-as-code capabilities, is gaining traction among DevOps teams. Other technologies such as API management and monitoring/logging tools are crucial for enabling secure, efficient, and observable serverless operations.

- In terms of application, web application development remains the leading use case due to the ease of deploying scalable APIs, backend logic, and front-end integrations using serverless stacks. Data processing and real-time analytics are gaining momentum, especially in industries handling high-volume streaming data. IoT backends and mobile application development are also seeing increased adoption due to the reduced infrastructure overhead and ease of integrating serverless functions with device-side operations.

- End-user industries such as IT & Telecom, BFSI, and Retail & E-commerce are spearheading adoption. In BFSI, serverless is being used for transaction processing, fraud detection, and compliance reporting. Retailers benefit from serverless scalability during traffic spikes and sales events, while telecoms utilize serverless for managing large-scale event logs and subscriber services. The Healthcare sector is leveraging serverless to support telemedicine platforms, patient portals, and HIPAA-compliant data processing. Government and Manufacturing sectors are also embracing serverless models for smart infrastructure, predictive maintenance, and public service delivery.

Report Scope and Serverless Architecture Market Segmentation

|

Attributes |

Smart Lock Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

• Rising Microservices and DevOps Adoption: Serverless architecture is ideally suited for microservices and CI/CD workflows, supporting rapid innovation, modular development, and dynamic scaling. It simplifies deployment processes and enhances agility across the software lifecycle, making it a core component of modern DevOps strategies. • Edge Computing and Microservices Enablement: Serverless computing is increasingly integrated with edge services, enabling real-time processing and reduced latency at the point of data generation. This synergy is crucial for IoT, autonomous systems, and content delivery, where speed and localized responsiveness are essential. • Low-Code and No-Code Integration: The rise of low-code and no-code platforms is driving demand for serverless backends that offer pre-built functions and APIs. This integration enables business users to develop applications quickly and efficiently, lowering technical barriers and accelerating digital transformation. |

|

Value Added Data Infosets |

|

Serverless Architecture Market Trends

"Cold Start Optimization and Multi-Language Runtime Support"

- Cloud providers are actively addressing one of the most persistent challenges in serverless computing—cold start latency. When a serverless function is triggered after a period of inactivity, the platform must initialize the runtime environment, leading to delays known as cold starts. To mitigate this, vendors are implementing advanced solutions such as provisioned concurrency, which keeps functions warm and ready to respond instantly. Additional techniques like lazy loading and pre-warmed containers are being deployed to minimize initialization time. These innovations are significantly improving the responsiveness of serverless platforms, making them more suitable for real-time, latency-sensitive applications such as financial transactions, IoT data processing, and user-facing web services.

- Major cloud platforms such as AWS Lambda, Azure Functions, and Google Cloud Functions are continually expanding their support for diverse programming languages to cater to a wider developer base. These platforms now offer compatibility with popular runtimes including Python, JavaScript (Node.js), Java, Go, .NET, and Rust. This multi-language support allows developers to leverage familiar tools and frameworks, increasing flexibility and accelerating development cycles. By enabling broader runtime options, serverless platforms are fostering greater adoption across industries and use cases, from backend services and APIs to AI-powered workflows and real-time data analytics.

- The expansion of supported runtimes across serverless platforms is significantly enhancing developer flexibility. With the ability to use preferred programming languages and frameworks, developers can build and deploy serverless applications without having to learn new tools or shift away from established workflows. This alignment with existing tech stacks not only streamlines development processes but also improves productivity and collaboration within teams. As a result, organizations can accelerate project timelines and reduce overhead by leveraging the skill sets they already possess, making serverless computing more accessible and practical for a broader range of applications.

- Improvements in startup performance and the availability of diverse runtime environments are expanding the applicability of serverless architecture across a wider array of use cases. Workloads that were once constrained by latency—such as machine learning inference, event-driven microservices, and real-time IoT data processing—can now be effectively managed within serverless environments. Reduced cold start times ensure faster response rates, while multi-language support allows developers to tailor solutions for specific technical requirements. This enhanced compatibility is driving broader adoption of serverless platforms across industries seeking scalable, low-maintenance, and event-responsive architectures.

- The serverless ecosystem is rapidly evolving with the development of advanced toolsets and software development kits (SDKs) that enhance the developer experience. Tools for local testing, debugging, and multi-runtime packaging are becoming more robust, allowing developers to simulate cloud environments and streamline deployment workflows. Intelligent orchestration platforms now support features such as automated scaling, function chaining, and monitoring across multiple runtimes. These advancements not only help mitigate cold start challenges but also improve overall deployment performance, making it easier for development teams to build, test, and manage complex serverless applications efficiently.

Serverless Architecture Market Dynamics

Driver

“SME Cloud Adoption & Cost-Effective Infrastructure”

- Serverless computing removes the need to provision and manage physical or virtual servers. This significantly reduces IT complexity and operational overhead. Development teams can focus purely on coding, while cloud providers handle scaling and maintenance automatically. This shift boosts agility and innovation across enterprises.]

- With serverless, organizations only pay for actual compute time consumed, not for idle infrastructure. This model minimizes waste and aligns IT costs with real usage patterns. It is particularly beneficial for SMEs and startups seeking cost control and financial flexibility. This pricing efficiency supports lean operations and scalability.

- Serverless platforms automatically scale functions based on demand, from a few requests per day to thousands per second. This eliminates the risk of under- or over-provisioning infrastructure. It ensures high performance during traffic spikes without manual intervention. Such elasticity improves service reliability and customer experience.

- By abstracting backend infrastructure, serverless reduces time spent on configuration and deployment. Developers can push code faster, enabling shorter release cycles and faster time-to-market. This speed supports agile methodologies and empowers teams to respond quickly to user feedback and market changes.

- Serverless architecture supports rapid experimentation and iterative development. It allows businesses to launch new features or products without long lead times or infrastructure investments. This makes it ideal for digital-first companies and industries undergoing rapid digital transformation, such as fintech, e-commerce, and SaaS.

Restraint/Challenge

“Restricted Support and Ongoing Maintenance Limit Broader Enterprise Adoption”

- Serverless abstracts the underlying infrastructure, which makes it difficult for developers to gain full visibility into system behavior. Traditional monitoring tools often fall short in capturing metrics across function executions, third-party services, and API calls. This lack of end-to-end observability creates blind spots in identifying root causes of issues.

- Real-time debugging is complex in serverless environments due to the stateless nature of functions and distributed execution across microservices. Developers must rely on logs and traces that may not capture sufficient context. This slows down issue resolution and increases the time required for performance tuning and troubleshooting.

- Tracing performance bottlenecks is difficult when workloads span multiple functions, APIs, and external services. The absence of unified tracing mechanisms across providers leads to fragmented diagnostics. For large-scale enterprise deployments, this can hinder service optimization and SLA compliance.

- Organizations often rely on third-party observability platforms to bridge monitoring gaps in serverless applications. While helpful, these tools add complexity, cost, and integration overhead. Inconsistent data formats and vendor-specific metrics also make it hard to maintain a unified performance view.

- For large enterprises with mission-critical workloads, the inability to monitor and debug effectively poses operational risks. Concerns over accountability, compliance, and latency resolution may deter adoption in heavily regulated sectors. Without better built-in tools, serverless adoption at scale remains constrained.

Serverless Architecture Market Scope

The market is segmented on the basis of Type, Material, Application, Form, End Users, Component, Cooling type and Distribution Channels.

- By Component

The market is divided into Software, Services, and Infrastructure Support (Hardware). Services dominate the segment, encompassing managed function execution, monitoring, API management, and DevOps automation. Software includes developer tools, orchestration frameworks, and runtime environments. While hardware is abstracted in serverless environments, infrastructure support such as edge nodes and data center capabilities form the backbone for function execution.

- By Technology

The market includes Function as a Service (FaaS) and Backend as a Service (BaaS). FaaS holds a dominant position due to its use in real-time, event-driven applications and microservices deployment. BaaS is growing steadily, offering pre-built backend functionalities like user authentication, database management, and file storage—making it ideal for mobile and web app development.

- By Enterprise Size

The market is segmented into Small & Medium Enterprises (SMEs) and Large Enterprises. SMEs are emerging as key adopters due to the minimal upfront infrastructure cost and ease of deployment. Serverless platforms help these businesses achieve enterprise-level scalability and speed. Large enterprises utilize serverless for modular development, hybrid cloud deployment, and AI/ML workloads, especially where agility and automation are critical.

- By Application

The market is segmented into Web Applications, Mobile Applications, Data Processing, IoT Backends, and Analytics Workloads. Web and mobile apps lead adoption due to rapid prototyping and scaling needs. Data processing and analytics are growing with the rise of serverless-powered ETL pipelines and real-time dashboards. Serverless is also increasingly used for managing IoT data and executing machine learning inference.

- By End User

The serverless market serves a wide range of industries, including IT & Telecom, BFSI, Retail & E-Commerce, Healthcare, Government, Education, and Manufacturing. IT & Telecom leverage serverless for scalable API services and DevOps automation. BFSI and Healthcare adopt it for secure data workflows and compliance automation. Retail and E-Commerce benefit from elastic scaling during high traffic. Government and education sectors use it to modernize digital service delivery.

Serverless Architecture Market Regional Analysis

- North America: Leads the global market, driven by advanced cloud maturity and enterprise adoption. The U.S. is the dominant contributor, with heavy use in fintech, e-commerce, and AI applications.

- Europe: GDPR compliance is shaping demand for secure, localized serverless platforms. Growth is strong in Germany, France, and the U.K.

- Asia-Pacific: Fastest-growing region. Markets like India, China, and Southeast Asia are leveraging serverless for mobile-first and digital-native applications.

- Middle East & Africa: Driven by cloud investments and digital governance initiatives, especially in the UAE and Saudi Arabia.

- South America: Brazil leads, with demand from mobile fintech apps and regional SaaS platforms seeking scalable, pay-as-you-go infrastructure.

United States Serverless Architecture Market Insight

The United States leads the global serverless architecture market due to its advanced cloud ecosystem, early adoption of DevOps and microservices, and strong presence of hyperscale providers like AWS, Microsoft Azure, and Google Cloud. Enterprises across sectors such as finance, healthcare, and media are leveraging serverless for cost-efficient, scalable application development. Government-backed digital initiatives and robust tech startup ecosystems further boost market penetration. Additionally, strong demand for AI, data analytics, and real-time services accelerates serverless integration across enterprise workloads.

Germany Serverless Architecture Market Insight

Germany is one of the most mature serverless markets in Europe, driven by strong enterprise IT adoption, GDPR compliance requirements, and cloud-first policies in manufacturing, automotive, and finance sectors. The emphasis on data sovereignty has encouraged the use of localized serverless deployments within European data centers. German businesses are increasingly using serverless architecture for microservices, event-driven automation, and industrial IoT applications. Local cloud providers and EU-compliant hyperscale platforms support demand from mid-sized enterprises and regulated industries.

India Serverless Architecture Market Insight

India represents one of the fastest-growing markets for serverless architecture, fueled by rapid digital transformation, cloud-native startup ecosystems, and strong mobile and e-commerce penetration. Initiatives such as “Digital India” and cloud adoption in sectors like fintech, edtech, and government services are creating widespread demand for agile, scalable backend solutions. SMEs and developers are opting for serverless to accelerate product development without heavy infrastructure investments. Major cloud providers are expanding their data center footprint in India to meet regional latency and compliance needs.

Japan Serverless Architecture Market Insight

Japan’s serverless market is expanding steadily, backed by its well-established tech industry, widespread use of automation, and increasing reliance on hybrid cloud strategies. Enterprises in sectors such as telecommunications, gaming, and manufacturing are utilizing serverless platforms to support high-performance, real-time applications. The emphasis on reliability, security, and performance stability aligns well with serverless offerings from AWS Japan, Azure, and domestic providers. Energy efficiency and high-density data center designs are also supporting the growth of scalable serverless infrastructure.

China Serverless Architecture Market Insight

China is emerging as a key growth market for serverless architecture, supported by aggressive cloud adoption, smart city projects, and the rapid digitalization of SMEs. Domestic giants such as Alibaba Cloud, Huawei Cloud, and Tencent Cloud are heavily investing in serverless services and developer ecosystems. Due to internet regulation and data localization policies, Chinese businesses prefer localized serverless platforms that comply with national standards. Use cases in e-commerce, mobile apps, and video streaming are especially prominent, driving demand for scalable, event-driven backends.

Brazil Serverless Architecture Market Insight

Brazil leads the serverless architecture market in Latin America, driven by cloud investments, rising internet penetration, and demand for modern application infrastructure in fintech, e-learning, and retail. Businesses are increasingly adopting serverless models to minimize operational costs and support agile deployments. With the expansion of AWS, Google Cloud, and Microsoft Azure data centers in the region, Brazilian companies now have access to low-latency, localized infrastructure. Serverless adoption is growing among startups and SMBs seeking flexible and developer-friendly cloud solutions.

Global Serverless Architecture Market Share

The Global Serverless Architecture Market is led by a combination of hyperscale cloud providers and specialized platform vendors offering robust, scalable, and developer-centric solutions. These providers dominate market share through extensive infrastructure networks, advanced developer tools, integrated security features, and comprehensive global reach.

The Serverless Architecture industry is primarily led by well-established companies, including:

- Microsoft Azure

- Amazon Web Services, Inc.

- Google Cloud

- IBM Corp.

- Oracle

- Alibaba Cloud

- Tencent Cloud

- Cloudflare, Inc

- Fastly

- Stackery, Inc.

Latest Developments in Global Serverless Architecture Market

- In March 2025, Google Cloud announced the integration of Firestore triggers with its Cloud Functions, enabling developers to build real-time, event-driven applications with greater efficiency. This enhancement supports more responsive backend logic, especially in chat apps, collaborative tools, and live dashboards.

- In January 2025, AWS introduced SnapStart for Java-based Lambda functions, reducing cold start latency by up to 80%. This innovation significantly improves performance for financial services, gaming, and other latency-sensitive applications, enhancing user experience and scalability.

- In November 2024, Microsoft Azure Functions rolled out support for .NET 8 alongside AI-powered monitoring tools via Azure Monitor. These features provide improved runtime efficiency and intelligent diagnostics, enabling faster troubleshooting and better observability across serverless environments.

- In August 2024, Oracle Cloud launched a serverless Kubernetes integration designed for hybrid and enterprise-grade deployments. This solution supports containerized workflows within a serverless framework, offering greater control, resource optimization, and multi-cloud compatibility.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.