Global Secondary Refrigerants Market

Market Size in USD Million

USD

874.10 Million

USD

1,429.33 Million

2025

2033

USD

874.10 Million

USD

1,429.33 Million

2025

2033

| 2026 - 2033 | |

| USD 874.10 Million | |

| USD 1,429.33 Million | |

| % | |

|

Secondary Refrigerants Market Size

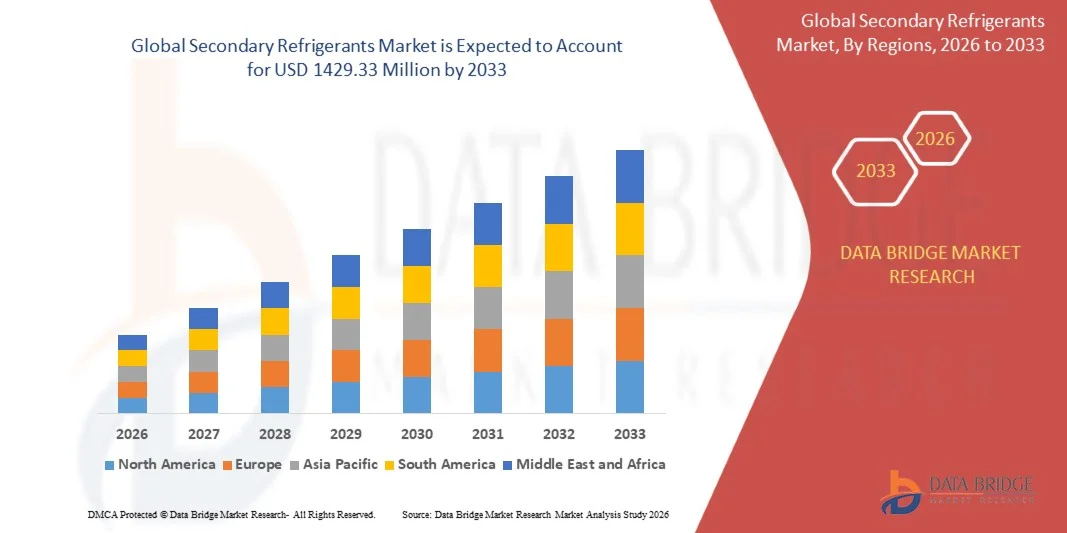

- The global secondary refrigerants market size was valued at USD 874.1 million in 2025 and is expected to reach USD 1429.33 million by 2033, at a CAGR of 6.34% during the forecast period

- The market growth is largely fueled by the increasing adoption of energy-efficient and environmentally friendly refrigeration solutions, leading to higher demand for secondary refrigerants such as glycols, salt brines, and CO₂-based fluids across industrial, commercial, and residential applications

- Furthermore, rising regulatory pressure to reduce global warming potential (GWP) and minimize direct refrigerant emissions is driving manufacturers and end-users to adopt secondary refrigerants as safer, sustainable alternatives. These converging factors are accelerating the uptake of secondary refrigerant solutions, thereby significantly boosting the market’s expansion

Secondary Refrigerants Market Analysis

- Secondary refrigerants are heat transfer fluids, including glycols, brines, and CO₂-based solutions, used in indirect cooling systems to absorb and transfer thermal energy from primary refrigerants. They enhance energy efficiency, safety, and environmental compliance across industrial refrigeration, commercial cooling, and HVAC systems

- The escalating demand for secondary refrigerants is primarily fueled by the global push for low-GWP cooling solutions, increasing industrial and commercial refrigeration needs, and a growing emphasis on energy efficiency, sustainability, and regulatory compliance in temperature-critical applications

- Asia-Pacific dominated the secondary refrigerants market with a share of 51.2% in 2025, due to expanding food and beverage processing, rapid industrialization, and a strong presence of commercial and industrial refrigeration infrastructure

- North America is expected to be the fastest growing region in the secondary refrigerants market during the forecast period due to increasing demand for energy-efficient and environmentally friendly refrigeration solutions in food processing, pharmaceuticals, and chemical industries

- Glycols segment dominated the market with a market share of 42.5% in 2025, due to its widespread use in industrial and commercial refrigeration systems due to excellent thermal stability and freeze protection. Glycols offer flexibility in formulation, allowing tailored solutions for various temperature requirements, which makes them highly preferred in food processing, pharmaceutical, and chemical industries

Report Scope and Secondary Refrigerants Market Segmentation

|

Attributes |

Secondary Refrigerants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Secondary Refrigerants Market Trends

“Increasing Adoption of Low-GWP Secondary Refrigerants”

- A significant trend in the secondary refrigerants market is the growing adoption of low-global warming potential (GWP) secondary refrigerants, driven by stricter environmental regulations and rising awareness of climate impact in refrigeration and HVAC systems. This adoption is pushing manufacturers and end-users to transition from conventional refrigerants to more sustainable alternatives that offer energy efficiency and lower environmental footprint

- For instance, Honeywell and Chemours are developing and supplying low-GWP secondary refrigerants such as Solstice® N41 and Opteon™ XP40, which are increasingly used in commercial and industrial cooling systems to reduce greenhouse gas emissions. These solutions enable facilities to meet regulatory standards while maintaining optimal cooling performance

- The use of secondary refrigerants is expanding in large-scale refrigeration systems where ammonia or CO₂-based loops circulate the fluid to cool secondary fluids, improving system safety and reducing direct emissions. This trend is positioning secondary refrigerants as critical enablers of environmentally responsible and energy-efficient cooling infrastructure

- Industrial sectors, including food processing and cold storage, are integrating low-GWP secondary refrigerants to enhance operational efficiency while minimizing environmental risks. The growing preference for safer refrigerants is accelerating the retrofitting of existing facilities and adoption in new installations

- Emerging applications in district cooling and commercial HVAC systems are driving further adoption of secondary refrigerants that support indirect cooling loops, optimizing energy use and system stability. This trend is shaping market growth as stakeholders prioritize compliance, safety, and energy efficiency

- The market is witnessing strong momentum as global sustainability initiatives and regulatory frameworks, such as the Kigali Amendment and EU F-Gas regulations, incentivize the transition toward low-GWP refrigerants. This is reinforcing the role of secondary refrigerants in reducing carbon footprint and enabling greener refrigeration and HVAC solutions

Secondary Refrigerants Market Dynamics

Driver

“Rising Demand for Energy-Efficient Cooling Systems”

- The rising demand for energy-efficient cooling systems is driving growth in the secondary refrigerants market as organizations seek to lower operational costs and reduce environmental impact. Secondary refrigerants help optimize system efficiency by enabling indirect cooling loops that consume less energy than traditional direct expansion systems

- For instance, Johnson Controls incorporates secondary refrigerants such as glycol-based solutions in their large-scale HVAC systems, improving energy efficiency and reducing refrigerant charge while maintaining cooling performance. These systems support sustainability goals in commercial buildings and industrial facilities

- Increasing focus on energy management and green building certifications, such as LEED, is encouraging the adoption of energy-efficient refrigeration solutions that use secondary refrigerants to minimize electricity consumption. Facilities are able to achieve higher efficiency ratings and reduced operating expenses

- The integration of advanced monitoring and control systems in refrigeration and HVAC infrastructure enhances the performance of secondary refrigerants, enabling precise temperature regulation and energy savings. This trend is accelerating deployment in supermarkets, cold storage warehouses, and data centers

- Industries are upgrading conventional systems to hybrid configurations that leverage secondary refrigerants to meet both energy efficiency and environmental compliance objectives. This shift is positioning secondary refrigerants as essential components in modern, sustainable cooling infrastructure

Restraint/Challenge

“Regulatory Compliance and Fluctuating Raw Material Availability”

- The secondary refrigerants market faces challenges due to strict environmental regulations and variable availability of raw materials needed for formulation. Compliance with standards such as the Montreal Protocol and regional refrigerant phase-down policies requires careful selection and documentation of refrigerant blends

- For instance, companies such as Arkema must navigate complex regulatory environments when producing low-GWP secondary refrigerants such as Forane HFO blends, ensuring that products meet global and local legislation. Failure to comply can result in fines or restricted market access

- Fluctuating availability of base chemicals, including glycols and HFOs, impacts production planning and cost stability for manufacturers. Supply chain disruptions and price volatility can delay projects and increase operational expenses

- The market also faces challenges in balancing environmental compliance with technical performance, as some low-GWP formulations may require careful handling or specialized infrastructure. Maintaining performance standards while adhering to evolving regulations demands significant investment in research and quality assurance

- Overall, regulatory complexity and material supply constraints continue to be key barriers to market expansion, requiring manufacturers and end-users to invest in compliant, reliable, and sustainable secondary refrigerant solutions

Secondary Refrigerants Market Scope

The market is segmented on the basis of type, application, and end-user.

• By Type

On the basis of type, the secondary refrigerants market is segmented into salt brines, glycols, carbon dioxide, and others. The glycols segment dominated the largest market revenue share of 42.5% in 2025, driven by its widespread use in industrial and commercial refrigeration systems due to excellent thermal stability and freeze protection. Glycols offer flexibility in formulation, allowing tailored solutions for various temperature requirements, which makes them highly preferred in food processing, pharmaceutical, and chemical industries. The market demand for glycol-based secondary refrigerants is also supported by their compatibility with multiple primary refrigerants and ease of handling in closed-loop systems. Furthermore, regulatory acceptance and extensive safety data contribute to their established adoption across diverse sectors.

The carbon dioxide segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing focus on low-GWP (Global Warming Potential) and environmentally friendly refrigerant solutions. CO₂-based secondary refrigerants provide high energy efficiency and reduced environmental impact, making them appealing for sustainable refrigeration practices. For instance, companies such as A-Gas leverage CO₂ secondary refrigerants in commercial refrigeration projects to meet green building standards. The rising adoption in supermarkets, cold storage, and process cooling applications is driving market expansion.

• By Application

On the basis of application, the secondary refrigerants market is segmented into industrial refrigeration, heat pumps, commercial refrigeration, and air conditioning. The industrial refrigeration segment dominated the largest market revenue share in 2025 due to the increasing need for large-scale cooling in food processing, chemical manufacturing, and cold storage facilities. Industrial applications demand highly efficient and stable secondary refrigerants capable of maintaining precise temperature control over large volumes. Glycol- and CO₂-based solutions are widely used in these systems for their safety, thermal efficiency, and adaptability to varying load conditions. The market growth is further supported by modernization and expansion of industrial plants across key regions.

The commercial refrigeration segment is projected to witness the fastest CAGR from 2026 to 2033, driven by rapid growth in retail, hospitality, and supermarket chains seeking energy-efficient and environmentally safe cooling systems. For instance, companies such as Emerson implement secondary refrigerants in commercial display and storage units to reduce energy consumption and comply with environmental regulations. Rising consumer preference for fresh food preservation and cold chain management is also increasing adoption in this segment.

• By End-User

On the basis of end-user, the secondary refrigerants market is segmented into oil and gas, food and beverages, pharmaceuticals, chemical, plastics, and others. The food and beverages segment dominated the largest market revenue share in 2025 due to high demand for temperature-sensitive storage and processing applications. Secondary refrigerants help maintain product quality, extend shelf life, and ensure compliance with stringent hygiene and safety standards. Glycol-based solutions are particularly preferred in cold storage and processing plants due to their reliability and ease of integration with existing refrigeration systems. The rising need for energy-efficient and environmentally sustainable operations further reinforces the adoption of secondary refrigerants in this sector.

The pharmaceuticals segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing demand for controlled temperature storage in drug manufacturing, vaccines, and biopharmaceuticals. For instance, companies such as Thermo Fisher Scientific utilize secondary refrigerants in cold chain logistics to ensure precise thermal management and regulatory compliance. Rising investments in pharmaceutical infrastructure and expanding production capacities are driving market growth in this end-user segment.

Secondary Refrigerants Market Regional Analysis

- Asia-Pacific dominated the secondary refrigerants market with the largest revenue share of 51.2% in 2025, driven by expanding food and beverage processing, rapid industrialization, and a strong presence of commercial and industrial refrigeration infrastructure

- The region’s cost-effective manufacturing landscape, growing adoption of energy-efficient cooling solutions, and rising investments in cold chain logistics are accelerating market expansion

- The availability of skilled labor, supportive government policies, and increasing demand for sustainable and low-GWP refrigerants are contributing to higher consumption of secondary refrigerants across industrial and commercial sectors

China Secondary Refrigerants Market Insight

China held the largest share in the Asia-Pacific secondary refrigerants market in 2025, owing to its leadership in industrial and commercial refrigeration, extensive food processing operations, and strong manufacturing base. The country’s investments in energy-efficient cooling systems and expanding cold storage facilities are major growth drivers. Demand is further supported by rising focus on sustainable refrigeration solutions and adoption of glycol- and CO₂-based secondary refrigerants for industrial and commercial applications.

India Secondary Refrigerants Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by increasing industrialization, expanding food and pharmaceutical production, and rising demand for cold storage and commercial refrigeration. Initiatives to modernize supply chains, enhance energy efficiency, and implement low-GWP refrigerants are strengthening demand. In addition, rising exports of processed foods and pharmaceuticals, along with growing investments in industrial refrigeration infrastructure, are driving robust market growth.

Europe Secondary Refrigerants Market Insight

The Europe secondary refrigerants market is expanding steadily, supported by stringent environmental regulations, high demand for energy-efficient and low-GWP refrigerants, and growing investments in sustainable industrial and commercial cooling systems. The region emphasizes quality, safety, and environmental compliance, particularly in food processing, pharmaceuticals, and chemical industries. Increasing adoption of CO₂- and glycol-based secondary refrigerants in modern refrigeration solutions is further enhancing market growth.

Germany Secondary Refrigerants Market Insight

Germany’s secondary refrigerants market is driven by its advanced industrial refrigeration sector, strong chemical and pharmaceutical industry heritage, and focus on energy-efficient cooling technologies. Well-established R&D networks and collaborations between manufacturers and academic institutions are fostering innovation in low-GWP and high-performance secondary refrigerants. Demand is particularly strong in food and beverage processing, cold storage, and high-value industrial applications.

U.K. Secondary Refrigerants Market Insight

The U.K. market is supported by a mature food and beverage sector, growing focus on sustainable and energy-efficient refrigeration, and increasing adoption of low-GWP secondary refrigerants. Investments in R&D, industrial automation, and cold chain infrastructure are supporting market growth. Rising awareness of environmental compliance and efficiency in commercial and industrial refrigeration is further accelerating adoption of glycol- and CO₂-based secondary refrigerants.

North America Secondary Refrigerants Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for energy-efficient and environmentally friendly refrigeration solutions in food processing, pharmaceuticals, and chemical industries. A strong focus on sustainability, cold chain modernization, and adoption of low-GWP secondary refrigerants is boosting growth. In addition, reshoring of industrial refrigeration projects and collaborations between commercial refrigeration providers and industrial end-users are supporting market expansion.

U.S. Secondary Refrigerants Market Insight

The U.S. accounted for the largest share in the North America market in 2025, underpinned by its expansive food processing, pharmaceutical, and chemical industries, strong R&D infrastructure, and focus on energy-efficient cooling solutions. The country’s emphasis on sustainability, regulatory compliance, and adoption of low-GWP glycol- and CO₂-based secondary refrigerants is driving growth. Presence of key industry players and well-developed cold chain and industrial refrigeration networks further solidify the U.S.’s leading position in the region.

Secondary Refrigerants Market Share

The secondary refrigerants industry is primarily led by well-established companies, including:

- SRS Frigadon (U.S.)

- Hydratech Industries (U.S.)

- Dow (U.S.)

- Tazzetti S.p.A (Italy)

- National Refrigerants Ltd. (U.K.)

- Clariant (Switzerland)

- Environmental Process Systems Ltd. (U.K.)

- Arteco (Italy)

- Linde plc (Germany)

- Eastman Chemical Company (U.S.)

- Temper Technology AB (Sweden)

- Hitachi Ltd. (Japan)

- Gas Servei (Spain)

- Hillphoenix, A Dover Company (U.S.)

- Climalife Dehon (France)

- Trane (U.S.)

- Nisso Shoji Co. Ltd. (Japan)

- A-Gas (Australia)

- Mitsubishi Electric Corporation (Japan)

- Dynalene Inc. (U.S.)

- NEI Corporation (U.S.)

- Chemtex Speciality Limited (India)

Latest Developments in Global Secondary Refrigerants Market

- In March 2026, Hudson Technologies signed a licensing agreement with Solstice Advanced Materials to reclaim and resell R‑448A and R‑449A refrigerants in the United States and Canada. This initiative expands Hudson Technologies’ commercial refrigeration portfolio while supporting sustainability goals by promoting the reuse of low-GWP refrigerants. The development strengthens infrastructure for reclaimed secondary refrigerants, meeting growing regulatory and industry demand for environmentally friendly cooling solutions. It also enhances supply chain resilience and encourages wider adoption of sustainable refrigerants in supermarkets, cold storage, and commercial refrigeration systems

- In December 2025, Honeywell introduced an enhanced line of salt brine secondary refrigerants with higher thermal conductivity specifically for commercial refrigeration systems. These advanced formulations improve heat transfer efficiency, reduce energy consumption, and ensure better system performance. The launch addresses the rising demand for energy-efficient and low-GWP refrigerants, helping commercial facilities meet environmental compliance standards. By offering improved thermal management, Honeywell’s products enable operators to optimize refrigeration performance, reduce operational costs, and expand adoption of advanced secondary refrigerants across commercial sectors

- In December 2024, Clariant commenced construction of a second production line at its Cangzhou facility in Hebei Province, China, to manufacture the multifunctional additive Nylostab S-EED in partnership with Beijing Tiangang Auxiliary Co., Ltd. This expansion responds to increasing demand from China’s nylon industry and indirectly supports the secondary refrigerants market by enhancing thermal stability and process efficiency in industrial cooling systems. The new line allows manufacturers to produce higher-quality nylon components that require precise temperature control, driving greater utilization of glycol- and CO₂-based secondary refrigerants in industrial refrigeration applications

- In February 2022, Linde announced a long-term agreement with BASF to supply hydrogen and steam to BASF's new hexamethylenediamine (HMD) facility in Chalampé, France, including construction of a second hydrogen production plant. This development indirectly impacts the secondary refrigerants market by supporting industrial processes that require consistent, reliable cooling. Increased hydrogen and steam production facilitates efficient operation of large-scale chemical and polymer plants, which in turn drives demand for high-performance secondary refrigerants to maintain stable temperature conditions and optimize energy use

- In November 2021, Chemours expanded production of its Opteon™ line of low-GWP refrigerants in the U.S., increasing availability of CO₂- and glycol-compatible secondary refrigerants. The expansion strengthens supply chain stability and encourages the adoption of environmentally friendly refrigerants across industrial and commercial sectors. By providing low-GWP alternatives, Chemours’ development supports regulatory compliance, reduces environmental impact, and promotes modernization of refrigeration systems in food processing, pharmaceuticals, and commercial cooling applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Secondary Refrigerants Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Secondary Refrigerants Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Secondary Refrigerants Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.