Global Proliferative Diabetic Retinopathy Market

Market Size in USD Billion

CAGR :

%

USD

3.20 Billion

USD

5.58 Billion

2025

2033

USD

3.20 Billion

USD

5.58 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.20 Billion | |

| USD 5.58 Billion | |

| % | |

|

Proliferative Diabetic Retinopathy Market Overview

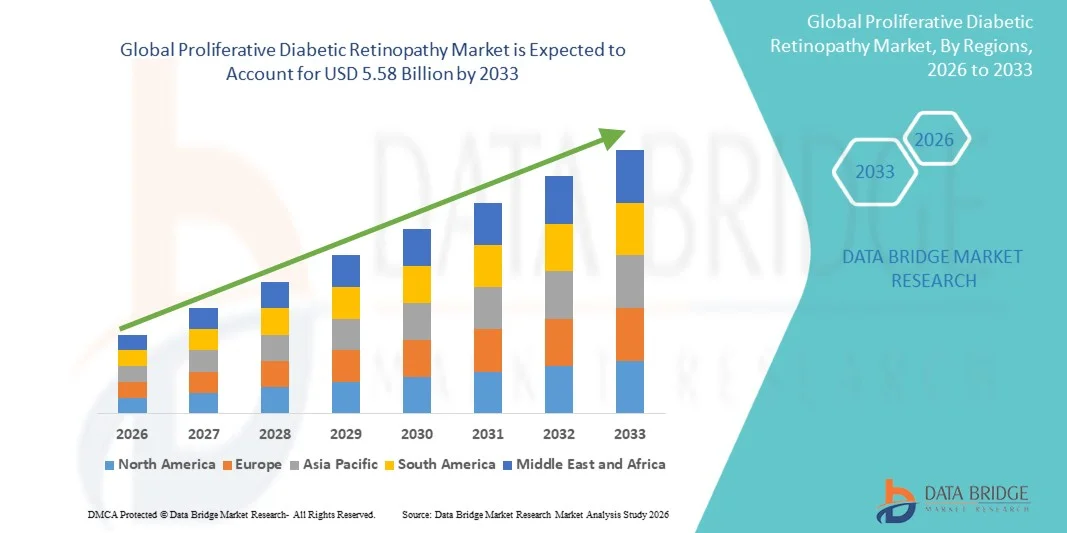

The Proliferative Diabetic Retinopathy Market was valued at USD 3.20 billion in 2025 and is projected to reach USD 5.58 billion by 2033, growing at a CAGR of 7.2% from 2026 to 2033. The market is witnessing steady growth driven by the rising global prevalence of diabetes, increasing incidence of vision-threatening retinal complications, and growing awareness regarding early diagnosis and advanced ophthalmic treatment options such as anti-VEGF therapy, laser photocoagulation, and vitrectomy procedures. Expanding screening programs and improved access to retinal imaging technologies are further supporting early detection and treatment adoption.

The increasing burden of diabetes-related eye disorders, particularly among aging populations and patients with uncontrolled blood sugar levels, is pushing demand for effective and minimally invasive treatment approaches. Advancements in ophthalmic drug delivery systems, surgical techniques, and retinal imaging diagnostics are improving treatment outcomes and expanding clinical applications across hospitals, specialty eye centers, and ambulatory surgical centers. In addition, growing healthcare investments and favorable reimbursement policies in developed regions are accelerating market penetration and improving patient access to advanced proliferative diabetic retinopathy management solutions.

Key Market Trends & Insights

- North America dominated the Proliferative Diabetic Retinopathy Market with the largest revenue share of 36.12% in 2025, supported by advanced ophthalmic care infrastructure, high diabetes prevalence, and strong adoption of anti-VEGF therapies and retinal imaging technologies.

- The Anti-VEGF Therapy segment led the market with a 44.87% share in 2025, driven by its strong clinical efficacy in inhibiting abnormal retinal neovascularization and preventing vision loss in diabetic patients.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by rising diabetic population, improving healthcare access, expanding screening programs, and increasing awareness of diabetic eye complications in China and India

- Vitrectomy Surgery are the fastest-growing treatment type, projected to register a CAGR of 7.1%, reflecting the surge in cases of advanced proliferative diabetic retinopathy associated with retinal detachment and severe vitreous hemorrhage.

- The Optical Coherence Tomography (OCT) segment dominated the diagnosis type category with a 41.33% revenue share in 2025, led by high-resolution, non-invasive imaging capability for detecting retinal thickness changes and early microvascular abnormalities.

- Anti-VEGF Agents accounted for 46.18% of the market, preferred by their strong therapeutic effectiveness in reducing abnormal blood vessel growth and preventing retinal damage.

- The Corticosteroids segment is the fastest-growing drug class category, with a CAGR of 6.7%, driven by their effectiveness in managing inflammation and diabetic macular edema associated with proliferative diabetic retinopathy.

Market Size & Forecast

- Global Market Value (2025): USD 3.20 Billion

- Expected Market Value (2033): USD 5.58 Billion

- Forecast CAGR (2026–2033): 7.2%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Proliferative Diabetic Retinopathy Market Segmentation

|

Attributes |

Proliferative Diabetic Retinopathy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Genentech, Inc. (U.S.) · Regeneron Pharmaceuticals, Inc. (U.S.) · Novartis AG (Switzerland) · AbbVie Inc. (U.S.) · Bayer AG (Germany) · Roche Holding AG (Switzerland) · Bausch + Lomb Corporation (Canada) · Alcon Inc. (Switzerland) · Santen Pharmaceutical Co., Ltd. (Japan) · Apellis Pharmaceuticals, Inc. (U.S.) · Kodiak Sciences Inc. (U.S.) · Ocular Therapeutix, Inc. (U.S.) · Eyepoint Pharmaceuticals, Inc. (U.S.) · Oxurion NV (Belgium) · REGENXBIO Inc. (U.S.) · Chugai Pharmaceutical Co., Ltd. (Japan) · Sun Pharmaceutical Industries Ltd. (India) · Intas Pharmaceuticals Ltd. (India) · Biocon Limited (India) · Daiichi Sankyo Company, Limited (Japan) |

|

Market Opportunities |

· Expanding adoption of AI-powered retinal screening tools in primary care and teleophthalmology platforms · Rising unmet treatment needs in emerging economies · Increasing integration of sustained-release drug delivery implants |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Proliferative Diabetic Retinopathy Market Trends

Trend: Rising Adoption of Anti-VEGF and Combination Therapies in Clinical Practice

Ophthalmology treatment is rapidly shifting toward anti-VEGF agents as the primary standard of care for proliferative diabetic retinopathy due to their ability to reduce abnormal retinal blood vessel growth and prevent vision loss. Clinicians are increasingly combining anti-VEGF injections with laser photocoagulation and corticosteroid therapies to achieve better anatomical and functional outcomes, especially in advanced disease stages. The emergence of personalized treatment strategies based on patient response, imaging biomarkers, and disease severity is further improving long-term management efficiency. In parallel, advanced retinal imaging techniques such as OCT angiography are enabling precise monitoring of treatment response and disease progression, improving clinical decision-making and reducing unnecessary interventions. For instance, the widespread clinical integration of drugs such as aflibercept, ranibizumab, and off-label bevacizumab across major ophthalmic hospitals has significantly transformed standard retinal care protocols and improved vision preservation outcomes globally.

Proliferative Diabetic Retinopathy Market Dynamics

Key Market Driver: Rising Global Diabetes Burden Driving Retinal Complication Cases

The continuous rise in global diabetes prevalence is the most critical factor fueling the proliferative diabetic retinopathy market, as prolonged uncontrolled blood sugar levels directly damage retinal blood vessels and lead to disease progression. Increasing urbanization, sedentary lifestyles, obesity, and aging populations are significantly expanding the patient pool at risk of vision-threatening complications. As a result, healthcare systems are placing greater emphasis on early detection and preventive screening programs to reduce blindness-related economic and social burdens. Governments and health organizations are actively expanding diabetic retinopathy screening coverage through primary care integration and mobile screening units.

For instance, large-scale national screening initiatives such as the U.K. NHS Diabetic Eye Screening Programme and India’s community-based diabetic eye camps are significantly improving early diagnosis rates and enabling timely intervention, reducing the risk of irreversible vision loss.

Key Restraint/Challenge: High Cost and Limited Accessibility of Advanced Retinal Treatments

Despite strong technological advancements, the market faces a major challenge in the form of high treatment costs and limited accessibility, particularly in developing and resource-constrained regions. Repeated anti-VEGF injections over long treatment cycles impose a significant financial burden on patients, often requiring monthly or bi-monthly administration in severe cases. In addition, advanced surgical interventions such as vitrectomy require specialized equipment and highly trained retina surgeons, which are not widely available outside major urban centers. Diagnostic tools such as OCT and fundus fluorescein angiography also add to overall treatment expenses, limiting widespread adoption.

For instance, in several low- and middle-income countries, patients experience delayed access to vitrectomy and anti-VEGF therapy due to insufficient retinal care infrastructure and high out-of-pocket costs, leading to preventable progression to severe vision impairment or blindness.

Key Market Opportunity: Expansion of AI-Based Screening and Tele-Ophthalmology Platforms

The integration of artificial intelligence and tele-ophthalmology is creating a transformative opportunity in proliferative diabetic retinopathy management by enabling scalable, cost-effective, and early-stage disease detection. AI algorithms trained on retinal images can rapidly identify microaneurysms, neovascularization, and hemorrhages with high accuracy, supporting non-specialist healthcare workers in screening large diabetic populations. Telemedicine platforms further enhance accessibility by enabling remote consultation between primary care centers and retina specialists, reducing diagnostic delays and improving referral efficiency. Cloud-based imaging databases are also helping build large datasets for continuous algorithm improvement and population-level disease tracking.

For instance, AI-driven retinal screening programs deployed in community clinics and pharmacy-based eye screening units are significantly improving early detection rates and reducing the burden on tertiary ophthalmic centers, particularly in underserved rural regions.

Proliferative Diabetic Retinopathy Market Scope

The proliferative diabetic retinopathy market is segmented on the basis of treatment type, diagnosis, drug class, and end user.

- By Treatment Type

On the basis of treatment type, the Proliferative Diabetic Retinopathy Market is segmented into anti-VEGF therapy, laser photocoagulation, vitrectomy surgery, corticosteroid therapy, and combination therapy. The Anti-VEGF Therapy segment dominated the market with a 44.87% share in 2025, owing to its strong clinical efficacy in inhibiting abnormal retinal neovascularization and preventing vision loss in diabetic patients. These therapies are widely used as first-line treatment across hospitals and specialty eye clinics due to their proven ability to improve visual acuity and reduce disease progression. Increasing adoption of drugs such as ranibizumab, aflibercept, and bevacizumab has strengthened treatment outcomes across both early and advanced stages of disease. Expanding reimbursement coverage and rising ophthalmologist preference for intravitreal injections are further supporting segment dominance. Continuous clinical advancements and long-acting formulations are improving patient compliance and reducing injection frequency. However, high treatment costs and repeated dosing requirements remain key limitations in long-term care management.

The Vitrectomy Surgery segment is projected to register the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by increasing cases of advanced proliferative diabetic retinopathy associated with retinal detachment and severe vitreous hemorrhage. This surgical intervention is essential for patients who do not respond adequately to pharmacological treatments. Improvements in minimally invasive vitrectomy techniques and advanced surgical visualization systems are significantly enhancing procedural safety and outcomes. Rising availability of specialized retinal surgeons and expansion of ophthalmic surgical centers are further supporting growth. Increasing diabetes prevalence and late-stage disease diagnosis in emerging markets are also contributing to higher surgical demand. Technological advancements in microsurgical instruments and postoperative care are improving recovery rates and expanding adoption globally.

- By Diagnosis

On the basis of diagnosis, the Proliferative Diabetic Retinopathy Market is segmented into optical coherence tomography (OCT), fundus fluorescein angiography (FFA), fundus photography, and other imaging modalities. The Optical Coherence Tomography (OCT) segment dominated the market with a 41.33% share in 2025, due to its high-resolution, non-invasive imaging capability for detecting retinal thickness changes and early microvascular abnormalities. OCT is widely adopted in ophthalmology clinics and hospitals for routine screening, disease monitoring, and treatment evaluation. Its ability to provide cross-sectional retinal imaging has made it the gold standard for assessing disease progression in diabetic retinopathy. Integration with AI-based image analysis tools is further improving diagnostic accuracy and workflow efficiency. Increasing availability of portable OCT devices is also expanding access in outpatient settings. Continuous technological upgrades are strengthening its role as a primary diagnostic tool in retinal care.

The Fundus Fluorescein Angiography (FFA) segment is expected to witness the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by its critical role in identifying retinal vascular leakage and neovascularization in advanced PDR cases. This imaging technique provides detailed visualization of blood flow abnormalities, making it essential for treatment planning in severe disease stages. Growing use in combination with OCT imaging is enhancing diagnostic precision and clinical decision-making. Increasing prevalence of advanced diabetic eye complications is boosting demand in tertiary care centers. Technological improvements in imaging contrast agents and digital angiography systems are further supporting adoption. Rising awareness among ophthalmologists regarding early vascular changes is accelerating clinical utilization globally.

- By Drug Class

On the basis of drug class, the Proliferative Diabetic Retinopathy Market is segmented into anti-VEGF agents, corticosteroids, and others. The Anti-VEGF Agents segment dominated the market with a 46.18% share in 2025, driven by their strong therapeutic effectiveness in reducing abnormal blood vessel growth and preventing retinal damage. These drugs are considered the cornerstone of modern PDR treatment and are widely used in both monotherapy and combination regimens. Increasing adoption of biosimilars is improving affordability and expanding patient access across emerging markets. Strong clinical evidence supporting visual acuity improvement has led to widespread physician preference. Continuous pipeline innovation in long-acting and dual-action biologics is further strengthening market dominance. Expanding regulatory approvals for new formulations is enhancing treatment accessibility across healthcare systems.

The Corticosteroids segment is projected to register the fastest growth at a CAGR of 6.7% from 2026 to 2033, driven by their effectiveness in managing inflammation and diabetic macular edema associated with proliferative diabetic retinopathy. These drugs are increasingly used as adjunct therapy in patients who show inadequate response to anti-VEGF treatment. Development of sustained-release steroid implants is improving treatment duration and reducing injection frequency. Rising adoption in combination therapy protocols is further expanding clinical applications. Growing prevalence of chronic diabetic complications is increasing demand for long-term inflammatory control. Improved safety profiles and controlled delivery systems are enhancing physician acceptance globally.

- By End User

On the basis of end user, the Proliferative Diabetic Retinopathy Market is segmented into hospitals, ophthalmology clinics, ambulatory surgical centers (ASCs), and diagnostic imaging centers. The Hospitals segment dominated the market with a 46.33% share in 2025, owing to the availability of advanced ophthalmic infrastructure, skilled retina specialists, and comprehensive treatment facilities. Hospitals are the primary centers for complex diagnostic evaluation, intravitreal injections, and vitrectomy procedures. High patient inflow and strong reimbursement frameworks further strengthen hospital dominance in retinal disease management. Integration of advanced imaging systems and AI-based diagnostic tools is improving treatment efficiency. Increasing hospital investments in ophthalmology departments are expanding service capabilities. Continuous technological upgrades are reinforcing their leadership in advanced retinal care delivery.

The Ambulatory Surgical Centers (ASCs) segment is expected to witness the fastest growth at a CAGR of 7.0% from 2026 to 2033, driven by rising demand for cost-effective, outpatient-based retinal treatments. ASCs offer reduced treatment costs, shorter waiting times, and efficient surgical workflows for procedures such as intravitreal injections and minor vitreoretinal surgeries. Increasing shift from inpatient hospital care to outpatient settings is accelerating adoption. Technological advancements enabling minimally invasive procedures are further supporting ASC growth. Expanding healthcare infrastructure in emerging economies is increasing accessibility to specialized eye care services. Growing patient preference for convenient and affordable treatment settings is also boosting segment expansion.

Proliferative Diabetic Retinopathy Market Regional Analysis

North America dominated the Proliferative Diabetic Retinopathy Market with the largest revenue share of 36.12% in 2025, supported by advanced ophthalmic care infrastructure, high diabetes prevalence, and strong adoption of anti-VEGF therapies and retinal imaging technologies. The region also benefits from early disease screening programs, favorable reimbursement frameworks, and widespread availability of retina specialists and advanced diagnostic imaging systems. Increasing investments in ophthalmic research, growing awareness of diabetic eye complications, and rapid integration of AI-based retinal screening technologies continue to strengthen North America’s leadership position in the global market.

U.S. Proliferative Diabetic Retinopathy Market Insight

The U.S. proliferative diabetic retinopathy market is witnessing strong growth due to rising diabetes prevalence, advanced ophthalmic care infrastructure, and high adoption of anti-VEGF therapies and retinal laser procedures. The country’s well-established healthcare system, strong presence of retina specialists, and extensive reimbursement coverage are driving demand across hospitals and specialty eye clinics. In addition, growing integration of AI-based retinal screening tools and OCT imaging technologies is improving early diagnosis and accelerating treatment initiation, further strengthening market expansion across clinical settings and research institutions.

Europe Proliferative Diabetic Retinopathy Market Insight

The Europe proliferative diabetic retinopathy market remains a major contributor to global revenue, driven by strong government-supported screening programs, advanced ophthalmic research, and widespread access to retinal treatment facilities. The region benefits from structured diabetic eye screening initiatives, high awareness of vision care, and increasing adoption of combination therapies such as anti-VEGF and laser photocoagulation. In addition, continuous investments in digital ophthalmology and AI-enabled diagnostic platforms are enhancing early detection and treatment outcomes across hospitals and specialty eye care centers.

U.K. Proliferative Diabetic Retinopathy Market Insight

The U.K. proliferative diabetic retinopathy market is experiencing steady growth, supported by the National Health Service (NHS) diabetic eye screening program, increasing diabetes cases, and strong adoption of advanced retinal imaging technologies. Rising use of anti-VEGF injections and expanding access to specialized ophthalmology services are contributing to improved disease management. Furthermore, integration of tele-ophthalmology services and AI-assisted screening systems is enhancing early detection efficiency and reducing the burden on tertiary care centers, positioning the U.K. as a key innovation hub in retinal disease management.

Germany Proliferative Diabetic Retinopathy Market Insight

The Germany proliferative diabetic retinopathy market is expanding steadily due to its advanced healthcare infrastructure, strong pharmaceutical presence, and increasing focus on early diagnosis of diabetic complications. Hospitals and ophthalmology clinics are increasingly adopting OCT imaging, fundus photography, and minimally invasive retinal procedures for improved patient outcomes. In addition, continuous advancements in biologic therapies and strong emphasis on clinical research and innovation are further driving treatment adoption and improving disease management across the country.

Asia-Pacific Proliferative Diabetic Retinopathy Market Insight

The Asia-Pacific proliferative diabetic retinopathy market is expected to witness rapid growth, driven by a rising diabetic population, improving healthcare infrastructure, and increasing awareness of diabetic eye diseases in countries such as China, India, and Japan. Growing investments in ophthalmic screening programs, expanding access to retinal specialists, and increasing adoption of cost-effective treatment options are supporting regional market expansion. In addition, rising integration of AI-based diagnostic tools and telemedicine platforms is improving early detection rates and accelerating treatment adoption across urban and semi-urban areas.

Japan Proliferative Diabetic Retinopathy Market Insight

The Japan proliferative diabetic retinopathy market is witnessing consistent growth due to its aging population, high diabetes prevalence, and advanced ophthalmic healthcare system. The country has strong adoption of cutting-edge retinal imaging technologies and anti-VEGF therapies for effective disease management. Moreover, increasing use of robotic-assisted ophthalmic procedures, AI-enabled diagnostic systems, and continuous innovation in retinal treatment approaches are further enhancing clinical outcomes and supporting market growth across hospitals and specialized eye care centers.

China Proliferative Diabetic Retinopathy Market Insight

The China proliferative diabetic retinopathy market is growing rapidly, driven by a large diabetic population, expanding healthcare infrastructure, and increasing government focus on chronic disease management and vision care. Rising adoption of anti-VEGF therapies, expanding ophthalmology service networks, and growing availability of advanced diagnostic tools are significantly improving treatment access. In addition, increasing investments in AI-based screening platforms, tele-ophthalmology solutions, and domestic pharmaceutical development are positioning China as one of the fastest-growing markets for proliferative diabetic retinopathy globally.

Proliferative Diabetic Retinopathy Market Share

The proliferative diabetic retinopathy industry is primarily led by well-established companies, including:

- Genentech, Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Novartis AG (Switzerland)

- AbbVie Inc. (U.S.)

- Bayer AG (Germany)

- Roche Holding AG (Switzerland)

- Bausch + Lomb Corporation (Canada)

- Alcon Inc. (Switzerland)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Apellis Pharmaceuticals, Inc. (U.S.)

- Kodiak Sciences Inc. (U.S.)

- Ocular Therapeutix, Inc. (U.S.)

- Eyepoint Pharmaceuticals, Inc. (U.S.)

- Oxurion NV (Belgium)

- REGENXBIO Inc. (U.S.)

- Chugai Pharmaceutical Co., Ltd. (Japan)

- Sun Pharmaceutical Industries Ltd. (India)

- Intas Pharmaceuticals Ltd. (India)

- Biocon Limited (India)

- Daiichi Sankyo Company, Limited (Japan)

Latest Developments in Proliferative Diabetic Retinopathy Market

- In March 2024, Roche announced new clinical and real-world evidence supporting the long-term durability and extended dosing potential of Vabysmo in retinal vascular diseases, including diabetic retinopathy, reinforcing its role as a next-generation therapy in anti-VEGF treatment evolution

- In February 2024, Regenxbio reported updated clinical trial results for RGX-314, an investigational one-time gene therapy for diabetic retinopathy, demonstrating sustained reduction in retinal fluid leakage and reduced need for repeated anti-VEGF injections, signaling a potential paradigm shift in long-term retinal disease management

- In August 2023, the U.S. FDA approved Eylea HD (aflibercept 8 mg) developed by Regeneron Pharmaceuticals, enabling longer dosing intervals for retinal diseases including diabetic retinopathy, reducing injection burden and improving patient compliance in chronic eye disease management

- In January 2022, the U.S. FDA approved Vabysmo (faricimab-svoa) developed by Genentech/Roche, a first-of-its-kind bispecific antibody targeting both Ang-2 and VEGF-A pathways, offering extended dosing intervals and improved outcomes for diabetic retinopathy and related retinal vascular diseases

- In June 2021, the U.S. FDA approved Byooviz (ranibizumab-nuna), the first biosimilar to Lucentis developed by Samsung Bioepis and Biogen, for the treatment of retinal diseases including diabetic retinopathy conditions, expanding access to cost-effective anti-VEGF therapy options in ophthalmology

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.