Global Practice Management Systems Market

Market Size in USD Billion

USD

11.52 Billion

USD

19.07 Billion

2024

2032

USD

11.52 Billion

USD

19.07 Billion

2024

2032

| 2025 - 2032 | |

| USD 11.52 Billion | |

| USD 19.07 Billion | |

| % | |

|

Practice Management Systems Market Size

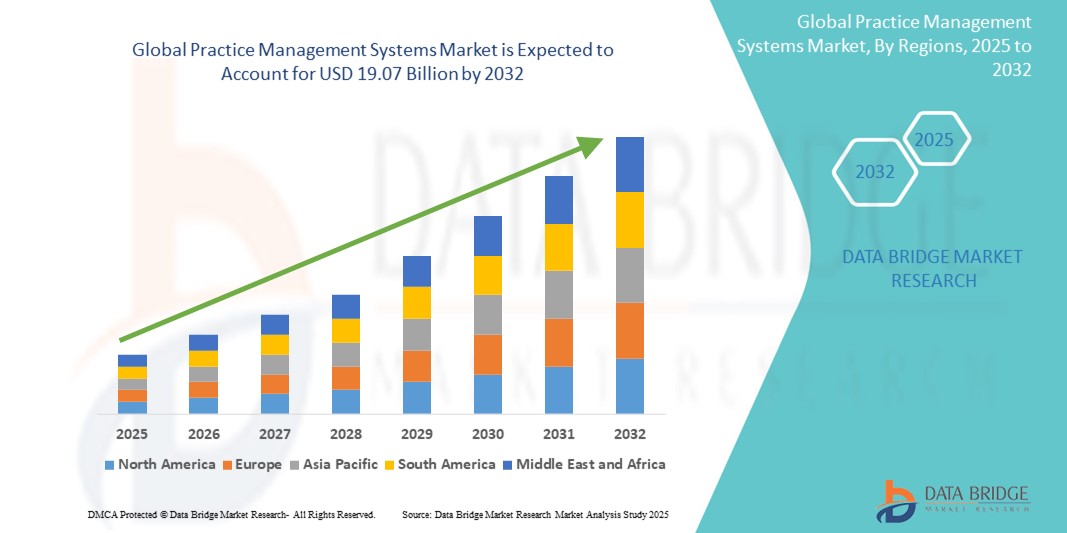

- The global practice management systems market size was valued at USD 11.52 billion in 2024 and is expected to reach USD 19.07 billion by 2032, at a CAGR of 6.50% during the forecast period

- The market growth is largely fueled by the increasing need for efficient healthcare administration, coupled with the rising adoption of electronic health records (EHR) and other digital solutions in healthcare. This leads to increased digitalization and streamlined workflows in medical practices

- Furthermore, rising demand for integrated solutions that combine administrative, clinical, and financial functions, along with technological advancements such as cloud-based platforms and AI integration, is establishing practice management systems as the modern solution for optimizing healthcare operations

Practice Management Systems Market Analysis

- Practice management systems (PMS) are increasingly vital components of modern healthcare operations, offering electronic solutions for managing daily administrative and financial tasks. These systems are crucial for enhancing efficiency, improving patient care, and ensuring regulatory compliance in various healthcare settings

- The escalating demand for practice management systems is primarily fueled by the widespread digitalization of healthcare, growing emphasis on reducing healthcare costs, increasing adoption of electronic health records (EHRs), and a rising preference for integrated and automated solutions for managing patient data, appointments, and billing

- North America dominates the practice management systems market with the largest revenue share of 47.1% in 2024, characterized by early adoption of healthcare IT solutions, high healthcare expenditure, and a strong presence of key industry players

- Asia-Pacific is expected to be the fastest growing region in the practice management systems market during the forecast period due to increasing healthcare digitalization, rising disposable incomes, and growing government initiatives to improve healthcare infrastructure and adopt digital health solutions in emerging economies

- Integrated segment dominates the practice management systems market with a market share of 74.5% in 2024, driven by its comprehensive benefits they offer, including streamlined patient and provider communication, efficient medical billing, and seamless integration with EHR, e-prescription, and patient engagement modules

Report Scope and Practice Management Systems Market Segmentation

|

Attributes |

Practice Management Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Practice Management Systems Market Trends

“Enhanced Efficiency Through AI and Automation”

- A significant and accelerating trend in the global practice management systems market is the deepening integration of artificial intelligence (AI) and automation to streamline administrative and clinical workflows. This fusion of technologies is significantly enhancing operational efficiency and improving patient care

- For instance, AI-powered practice management systems can automate appointment scheduling, sending out reminders, managing rescheduling, and even handling cancellations without human intervention. This not only reduces administrative burden but also minimizes no-shows and optimizes physician availability. Similarly, AI can be leveraged for automated billing and claims processing, identifying coding errors, and ensuring accurate submission, leading to faster reimbursements and improved revenue cycle management

- AI integration further enables features such as learning patient patterns to predict potential no-shows, offering proactive outreach, and providing more intelligent insights into clinic performance. For instance, AI-driven solutions can analyze vast amounts of patient data to generate personalized treatment plans and recommendations, while also enhancing the accuracy and efficiency of electronic health record (EHR) documentation through speech-to-text transcription and AI-driven suggestions for clinical notes. Voice control capabilities are also emerging, allowing healthcare professionals to dictate notes or access information hands-free, freeing them to focus more on patient interaction

- The seamless integration of practice management systems with AI and broader healthcare IT platforms facilitates centralized control over various aspects of practice operations. Through a single interface, users can manage patient demographics, appointments, billing, clinical documentation, and even integrate with telehealth solutions, creating a unified and automated healthcare delivery experience

- This trend towards more intelligent, intuitive, and interconnected practice management systems is fundamentally reshaping expectations for healthcare administration. Consequently, companies are developing AI-enabled solutions with features such as predictive analytics for resource allocation and personalized patient engagement tools

- The demand for practice management systems that offer seamless AI and automation integration is growing rapidly across various healthcare settings, as providers increasingly prioritize efficiency, cost reduction, and comprehensive digital functionality to deliver high-quality patient care

Practice Management Systems Market Dynamics

Driver

“Growing Need Due to Increasing Administrative Burden and Digitalization in Healthcare”

- The increasing administrative burden on healthcare providers, coupled with the accelerating digitalization of the healthcare industry, is a significant driver for the heightened demand for practice management systems

- For instance, healthcare organizations are facing mounting pressure to manage complex billing processes, insurance claims, appointment scheduling, and patient communications efficiently. In August 2023, HCA Healthcare and Google Cloud announced a partnership agreement for the use of generative AI technology in hospitals, signaling a move towards leveraging technology to streamline operations. Such strategies by key companies and healthcare systems are expected to drive the practice management systems industry growth in the forecast period

- As healthcare providers seek to reduce operational costs, minimize errors, and improve overall efficiency, practice management systems offer advanced features such as automated appointment reminders, electronic claims submission, and comprehensive revenue cycle management, providing a compelling upgrade over manual or disparate systems

- Furthermore, the growing adoption of electronic health records (EHRs) and the desire for integrated healthcare ecosystems are making practice management systems an integral component of these systems, offering seamless integration with EHRs, e-prescribing, and patient engagement platforms.

- The convenience of streamlined workflows, enhanced patient engagement tools, and the ability to manage various administrative and financial tasks through a single, integrated platform are key factors propelling the adoption of practice management systems across hospitals, physician offices, and other healthcare settings. The trend towards cloud-based solutions and the increasing availability of user-friendly PMS options further contribute to market growth

Restraint/Challenge

“Concerns Regarding Data Security, Interoperability, and High Initial Costs”

- Concerns surrounding the cybersecurity vulnerabilities of healthcare IT systems, including practice management systems, pose a significant challenge to broader market penetration. As these systems handle highly sensitive patient data (ePHI), they are prime targets for cyberattacks such as ransomware, phishing, and data breaches, raising anxieties among healthcare providers and patients about privacy and compliance

- For instance, high-profile reports of breaches in healthcare organizations, such as the 2024 attack on Change Healthcare, have made some providers hesitant to fully embrace interconnected digital solutions. Addressing these cybersecurity concerns through robust encryption, secure authentication protocols, regular software updates, and comprehensive employee training is crucial for building trust. Companies are increasingly investing in advanced security features and compliance certifications to reassure potential buyers

- In addition, a significant challenge lies in interoperability – the ability of different healthcare IT systems to seamlessly exchange and interpret data. While practice management systems are designed to integrate with Electronic Health Records (EHRs) and other platforms, achieving true interoperability can be complex due to varying data standards, legacy systems, and proprietary interfaces. This can lead to fragmented data, inefficiencies, and hinder the holistic view of patient care

- Furthermore, the relatively high initial cost of implementing and customizing advanced practice management systems can be a barrier to adoption for smaller practices or those with limited budgets. While cloud-based solutions have made some options more accessible, premium features, extensive customization, and ongoing maintenance, training, and support can still represent a substantial investment

- While prices are gradually becoming more competitive, the perceived premium for comprehensive healthcare IT solutions can still hinder widespread adoption, especially for practices that do not immediately recognize the long-term ROI or are reluctant to disrupt existing workflows. Overcoming these challenges through enhanced cybersecurity measures, industry-wide standardization for interoperability, comprehensive vendor support, and the development of more affordable and scalable PMS options will be vital for sustained market growth

Practice Management Systems Market Scope

The market is segmented on the basis of product type, component, delivery mode, and end users.

- By Product Type

On the basis of product type, the global practice management systems market is segmented into integrated and standalone systems. The integrated segment held the largest market share of 74.5% in 2024, driven by its comprehensive benefits, including streamlined patient management, improved productivity, and seamless integration of EHR, e-prescription, patient engagement, and billing systems. Healthcare providers are increasingly adopting these comprehensive solutions to centralize data and enhance overall operational efficiency.

The standalone segment is anticipated to witness considerable growth over the forecast period, attributed to the flexibility they offer, particularly for smaller practices that may initially focus solely on administrative and billing functions such as scheduling. These systems allow physicians more freedom to access specific facets of practice and business management.

- By Component

On the basis of component, the market is segmented into software and services. The software segment accounted for the largest revenue share in 2024, primarily due to the increasing adoption of digital solutions to optimize clinical and administrative functions. Software solutions are crucial for facilitating patient scheduling, billing, coding, and record-keeping, which are essential for efficient practice management. The continuous product upgrades and intuitive user interfaces further contribute to its dominance

The services segment is expected to witness the fastest CAGR from 2025 to 2032, due to as healthcare organizations require ongoing support for implementation, training, maintenance, and customization of their practice management systems. The complexity of these systems and the need for specialized expertise drive the demand for professional services.

- By Delivery Mode

On the basis of delivery mode, the market is segmented into web-based, cloud-based, and on-premise-based. The cloud-based segment captured the largest market share in 2024, driven by the easy accessibility of data through the web, automation of daily medical tasks, lower upfront investment, higher scalability, reduced IT overhead, and enhanced data security and compliance features offered by reputable cloud vendors. Cloud solutions enable remote access, which is crucial for modern, distributed healthcare teams and telehealth integration

The on-premise-based segment is expected to witness a fastest growth, due to its higher initial costs for hardware and software, limited remote accessibility, and the need for in-house IT management for updates and maintenance. However, it still holds relevance for organizations with strict data localization requirements or those preferring full control over their infrastructure

- By End User

On the basis of end users, the market is segmented into hospitals, physician offices, healthcare payers, pharmacies, and others. Hospitals held the largest share in the market in 2024, as these institutions require comprehensive solutions to manage high patient volumes, complex billing processes, and intricate scheduling across multiple departments and providers. PMS in hospitals facilitates efficient planning and confirmation of appointments and streamlines overall administrative workflows

The physician offices segment is anticipated to be the fastest-growing category during the forecast period. This growth is attributed to the increasing number of doctors establishing independent practices and the rising need for assistance in managing change, effective revenue cycle management, and implementing well-defined organizational structures within their medical practices to enhance productivity and operations

Practice Management Systems Market Regional Analysis

- North America dominates the practice management systems market with the largest revenue share of 47.1% in 2024, driven by early adoption of healthcare IT solutions, high healthcare expenditure, and a strong presence of key industry players

- Consumers and healthcare providers in the region highly value the efficiency, improved patient care, and seamless integration offered by practice management systems with other digital health solutions such as EHRs and telehealth platforms

- This widespread adoption is further supported by favorable government initiatives, such as EHR incentive programs by Medicaid and Medicare, a technologically advanced healthcare workforce, and the growing preference for streamlined administrative and clinical workflows

U.S. Practice Management Systems Market Insight

The U.S. practice management systems market captured the largest revenue share of 76.2% within North America in 2024, fueled by the swift uptake of integrated healthcare IT solutions and the expanding trend of digital transformation in healthcare. Healthcare providers are increasingly prioritizing the enhancement of operational efficiency and patient care through intelligent, automated systems. The growing preference for cloud-based PMS, combined with robust demand for solutions integrating with EHRs, telehealth, and AI-powered features, further propels the practice management systems industry. Moreover, the increasing focus on value-based care and government initiatives promoting digital health adoption are significantly contributing to the market's expansion

Europe Practice Management Systems Market Insight

The Europe practice management systems market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the escalating need for efficient healthcare administration, strict data privacy regulations (such as GDPR), and the increasing adoption of EHRs across the region. The increase in digitalization of healthcare, coupled with the demand for integrated solutions, is fostering the adoption of practice management systems. European healthcare providers are also drawn to the benefits these systems offer in terms of reduced administrative burden and improved patient outcomes. The region is experiencing significant growth across various healthcare settings, with PMS being incorporated into both public and private health institutions

U.K. Practice Management Systems Market Insight

The U.K. practice management systems market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating trend of healthcare digitalization and a desire for heightened efficiency and cost reduction. In addition, the increasing complexity of healthcare regulations and the need for seamless data exchange are encouraging both hospitals and physician offices to choose integrated PMS solutions. The UK’s embrace of cloud-based solutions, alongside its strong focus on improving patient pathways and outcomes, is expected to continue to stimulate market growth

Germany Practice Management Systems Market Insight

The Germany practice management systems market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of digital health solutions and the demand for technologically advanced, efficient systems. Germany’s well-developed healthcare infrastructure, combined with its emphasis on data security and patient privacy, promotes the adoption of practice management systems, particularly in large hospitals and ambulatory care centers. The integration of PMS with EHRs and other healthcare IT systems is also becoming increasingly prevalent, with a strong preference for secure, interoperable, and privacy-focused solutions aligning with local consumer and regulatory expectation

Asia-Pacific Practice Management Systems Market Insight

The Asia-Pacific practice management systems market is poised to grow at the fastest CAGR during the forecast period, driven by increasing healthcare expenditure, rising disposable incomes, and rapid technological advancements in countries such as China, Japan, and India. The region's growing inclination towards digital healthcare, supported by government initiatives promoting e-health and universal healthcare coverage, is driving the adoption of practice management systems. Furthermore, as APAC countries continue to invest in modernizing their healthcare infrastructure, the affordability and accessibility of PMS are expanding to a wider range of healthcare providers.

Japan Practice Management Systems Market Insight

The Japan practice management systems market is gaining momentum due to the country’s high-tech culture, rapid aging population, and demand for efficient healthcare delivery. The Japanese market places a significant emphasis on quality of care and data accuracy, and the adoption of practice management systems is driven by the increasing number of integrated healthcare facilities and the push for digital transformation. The integration of PMS with EHR systems and other healthcare IT solutions is fueling growth. Moreover, Japan's aging population is likely to spur demand for more streamlined and accessible healthcare administrative solutions in both hospital and clinic settings.

India Practice Management Systems Market Insight

The India practice management systems market accounted for a significant market revenue share in Asia Pacific in 2024, attributed to the country's expanding healthcare sector, rapid urbanization, and high rates of technological adoption. India stands as a rapidly growing market for digital health solutions, and practice management systems are becoming increasingly popular across hospitals, clinics, and diagnostic centers. The push towards digital India initiatives and the availability of affordable, scalable PMS options, alongside a growing ecosystem of domestic and international healthcare IT providers, are key factors propelling the market in India.

Practice Management Systems Market Share

The practice management systems industry is primarily led by well-established companies, including:

- athenahealth (U.S.)

- Greenway Health, LLC (U.S.)

- Veradigm LLC (U.S.)

- CollaborateMD Inc (U.S.)

- Pegasystems Inc. (U.S.)

- InfoMC (U.S.)

- Incedo Inc. (U.S.)

- HealthTec Software, Inc. (U.S.)

- GE HealthCare (U.S.)

- Oracle (U.S.)

- Epic Systems Corporation (U.S.)

- MCKESSON CORPORATION (U.S.)

- Productivity-Quality Systems, Inc. (U.S.)

- AdvantEdge Healthcare Solutions (U.S.)

- Henry Schein, Inc. (U.S.)

- G2, Inc. (U.S.)

- Medical Information Technology, Inc. (U.S.)

- NXGN Management, LLC (U.S.)

- AllegianceMD Software, Inc. (U.S.)

Latest Developments in Global Practice Management Systems Market

- In April 2023, Microsoft Corp. and Epic announced the extension of their strategic partnership to develop and integrate generative AI into healthcare. This collaboration aims to leverage AI to enhance various aspects of healthcare, including potentially improving practice management workflows and data analysis

- In April 2023, A healthcare technology startup, Suno, announced the release of its AI-powered practice management software. This development highlights the increasing focus on leveraging AI and machine learning to automate and optimize various administrative and clinical processes, such as appointment setting, reporting, and medical billing

- In March 2023, Practo, a leading integrated healthcare company, announced that their practice management software, Ray, is now compliant with the Ayushman Bharat Digital Mission (ABDM), a digital integrated health platform by the Government of India. This signifies a move towards greater interoperability and digital integration within healthcare systems, particularly in emerging markets

- In February 2023, The government of Nova Scotia, Canada, signed a USD 365.0 million contract to bring electronic healthcare records to the province. While not directly a PMS development, this substantial investment in EHRs strongly supports the growth of integrated practice management systems, as PMS often works in conjunction with EHRs to streamline administrative and clinical functions

- In January 2023, PatientClick, Inc. launched a new AI-powered practice management software. This new software offers automation in various tasks such as scheduling, credit card processing, automatic eligibility checks, and patient reminders, demonstrating the industry's drive towards more intelligent and automated solutions for healthcare providers

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.