Global Photovoltaic Materials Market

Market Size in USD Billion

USD

32.52 Billion

USD

78.53 Billion

2024

2032

USD

32.52 Billion

USD

78.53 Billion

2024

2032

| 2025 - 2032 | |

| USD 32.52 Billion | |

| USD 78.53 Billion | |

| % | |

|

Photovoltaic Materials Market Size

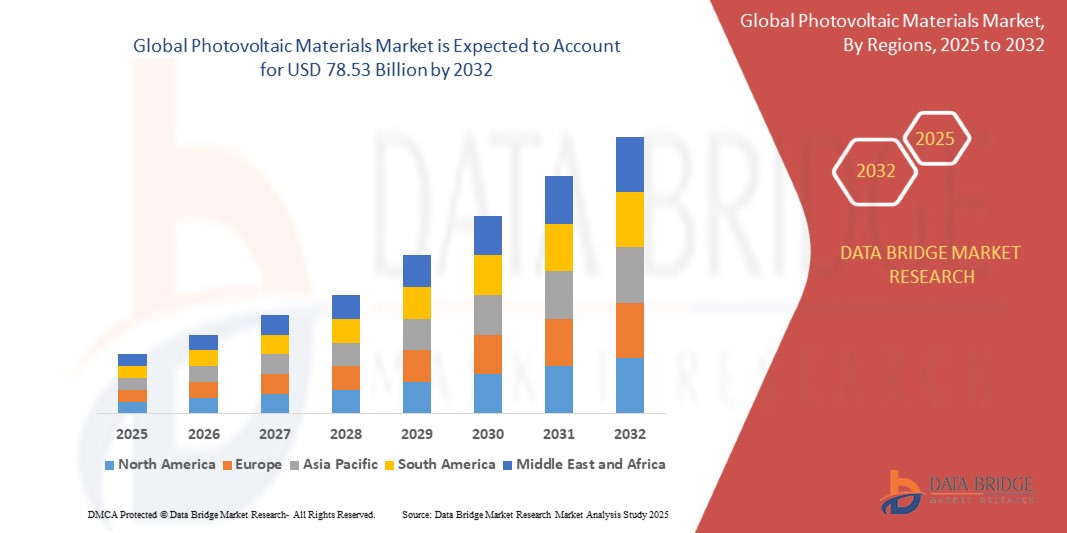

- The global photovoltaic materials market size was valued at USD 32.52 billion in 2024 and is expected to reach USD 78.53 billion by 2032, at a CAGR of 11.65% during the forecast period

- This growth is driven by driven by increasing global demand for renewable energy sources, governmental incentives, and advancements in solar technology

Photovoltaic Materials Market Analysis

- Photovoltaic materials are critical components in solar energy systems, converting sunlight into electrical energy. These materials, such as silicon, perovskites, and thin films, play a significant role in enhancing solar cell efficiency and reducing energy costs. They are widely used in solar power generation, offering solutions for residential, commercial, and industrial applications, thus driving the global shift towards renewable energy sources

- The market is primarily driven by the increasing global demand for clean energy, government initiatives supporting renewable energy adoption, and advancements in photovoltaic material technologies. The growing need to reduce dependence on fossil fuels, coupled with the decline in solar power costs due to innovations such as perovskite solar cells and bifacial panels, is accelerating the adoption of photovoltaic materials

- Asia-Pacific dominates the photovoltaic materials market, led by countries such as China, India, and Japan, where significant investments are being made in solar energy infrastructure. Government policies promoting solar energy, such as subsidies and favorable tariffs, further strengthen the region’s market leadership

- North America is expected to experience the highest growth during the forecast period, driven by a growing demand for renewable energy and solar power. The U.S. and Canada are heavily investing in solar energy technologies, spurred by government incentives and increasing installations of solar panels in residential and commercial sectors

- The crystalline materials segment is expected to dominate the photovoltaic materials market, with a market share of 83.23%, owing to its common use in solar panels, delivers high conversion efficiency, leading to greater energy output and lower material usage

Report Scope and Photovoltaic Materials Market Segmentation

|

Attributes |

Photovoltaic Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework |

Photovoltaic Materials Market Trends

“Advancements in Perovskite Solar Cells for Higher Efficiency and Cost Reduction”

- The development of perovskite solar cells is driving innovation in photovoltaic materials, offering the potential for higher efficiency at lower production costs compared to traditional silicon-based cells

- Perovskite materials are lightweight, flexible, and can be manufactured using simpler processes, significantly reducing the overall cost of solar panels and expanding their use in various applications, including building-integrated photovoltaics (BIPV)

- Researchers and manufacturers are now focusing on improving the stability and scalability of perovskite cells to make them viable for mass production and long-term use

- For instance, in March 2025, Oxford Photovoltaics announced a breakthrough in perovskite solar technology that achieved a record efficiency of 28%, bringing it closer to commercial viability

- This trend is expected to lead to widespread adoption of low-cost, high-performance solar technologies, enhancing the efficiency of photovoltaic systems globally and accelerating the transition to renewable energy

Photovoltaic Materials Market Dynamics

Driver

“Government Incentives and Global Solar Power Expansion”

- Governments around the world are implementing favorable policies, tax incentives, and subsidies to promote the adoption of solar energy, directly boosting the demand for photovoltaic materials.

- The global solar power market is expanding rapidly due to targets set by countries for carbon neutrality and renewable energy investments, creating significant demand for solar panels and photovoltaic components

- Many countries are introducing feed-in tariffs, solar tax credits, and subsidized installations, creating a favorable market environment for the adoption of photovoltaic materials

- For instance, in December 2024, the European Union introduced a 10-year solar energy incentive plan aiming to install over 100 GW of solar capacity, fueling demand for photovoltaic materials across the region

- This driver highlights how policy support and global energy goals are creating a conducive environment for the growth of the photovoltaic materials market

Opportunity

“Rise in Demand for Solar Energy Storage Solutions”

- As the adoption of solar power grows, there is increasing demand for solar energy storage solutions, providing an opportunity for photovoltaic materials manufacturers to collaborate with battery technology providers

- Solar energy storage systems allow users to store excess energy generated during peak sunlight hours, ensuring continuous power supply even when the sun isn’t shining, thus enhancing solar system reliability

- The integration of photovoltaic materials with advanced energy storage technologies, such as lithium-ion batteries, is expected to create innovative solutions for residential, commercial, and industrial applications

- For instance, in January 2025, Tesla launched a new solar roof system with integrated energy storage solutions, allowing consumers to harness and store solar energy efficiently

- This opportunity emphasizes how advancements in energy storage technology are creating a growing synergy with photovoltaic materials, leading to more efficient solar power systems

Restraint/Challenge

“Supply Chain Disruptions and Raw Material Shortages”

- The photovoltaic materials market faces challenges due to supply chain disruptions, particularly the availability of key raw materials such as silicon, silver, and indium, which are essential in the production of solar panels

- The global semiconductor shortage and trade tensions have led to delays in the procurement of high-quality materials, affecting production timelines and raising costs for manufacturers

- In addition, fluctuating raw material prices and dependence on specific regions for key supplies create uncertainties in the supply chain, potentially increasing costs and causing delays

- For instance, in August 2024, Global Solar Manufacturing reported delays in solar panel production due to shortages in high-purity silicon, resulting in longer delivery times for large-scale solar projects

- Overcoming this challenge will require innovative sourcing strategies and increased investment in alternative materials and manufacturing techniques to reduce reliance on specific raw materials and ensure market stability

Photovoltaic Materials Market Scope

The market is segmented on the basis of materials, product, and application.

|

Segmentation |

Sub-Segmentation |

|

By Materials |

|

|

By Product |

|

|

By Application |

|

In 2025, the crystalline materials is projected to dominate the market with a largest share in materials segment

The crystalline materials segment is expected to dominate the photovoltaic materials market with the largest share of 83.23% in 2025 due to its common use in solar panels, delivers high conversion efficiency, leading to greater energy output and lower material usage.

The utility is expected to account for the largest share during the forecast period in application market

In 2025, the utility segment is expected to dominate the photovoltaic materials market with the largest share of 44% due to large-scale energy generation capacity of utility-scale solar farms drives significant demand for extensive photovoltaic materials.

Photovoltaic Materials Market Regional Analysis

“Asia-Pacific Holds the Largest Share in the Photovoltaic Materials Market”

- Asia-Pacific dominates the global photovoltaic materials market, fueled by rapid urbanization, growing energy demands, and substantial investments in solar power infrastructure

- China dominates the regional market, owing to its massive solar panel manufacturing capacity, government subsidies, and aggressive renewable energy targets under its national energy policies

- Rising installations of solar energy systems across residential, commercial, and utility-scale applications are significantly driving demand for photovoltaic materials in countries such as India, Japan, and South Korea

- Supportive government policies and ambitious carbon neutrality goals are further propelling market growth, solidifying Asia-Pacific’s position as the global leader in the photovoltaic materials secto

“North America is projected to register the Highest CAGR in the Photovoltaic Materials Market”

- North America is expected to witness the highest growth in the photovoltaic materials market, driven by expanding solar energy adoption, supportive renewable energy policies, and rising demand for sustainable power generation solutions

- U.S. and Canada are major contributors, backed by increasing investments in solar infrastructure, federal incentives such as the Inflation Reduction Act, and a shift toward decarbonization across industries

- The U.S., in particular, is witnessing a surge in utility-scale and residential solar installations, driving the demand for efficient photovoltaic materials with improved performance and cost-effectiveness

- Government initiatives promoting clean energy transition, coupled with rising awareness about climate change, are accelerating the market’s expansion across North America, making it the fastest-growing region in the global photovoltaic materials sector

Photovoltaic Materials Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- KANEKA CORPORATION (Japan)

- KYOCERA Corporation (Japan)

- Mitsubishi Electric Corporation (Japan)

- DuPont (U.S.)

- American Elements (U.S.)

- 1366 Technologies (U.S.)

- Merck KGaA (Germany)

- Honeywell International Inc. (U.S.)

- COVEME s.p.a. (Italy)

- Targray (Canada)

- Novaled GmbH (Germany)

- Ferrotec (USA) Corporation (U.S.)

- Wacker Chemie AG (Germany)

- ARMOR (France)

- Tata Power Solar Systems Ltd. (India)

- Panasonic Corporation (Japan)

- SHARP CORPORATION (Japan)

- First Solar (U.S.)

- RENESOLA (China)

- Yingli Solar (China)

- Duke Energy Corporation (U.S.)

- Allesun (China)

Latest Developments in Global Photovoltaic Materials Market

- In July 2024, Jinko Solar announced that it had become the primary supplier of solar panels for a major solar energy project developed by Adani Green Energy Ltd (AGEL) in the Kutch region of Gujarat, India. The company supplied approximately 2381 MW of panels, including 1370 MW of Tiger Neo Bifacial modules and 1011 MW of Tiger Pro Bifacial modules. Deliveries began in August 2023 and were completed by January 2024. This milestone reinforced Jinko Solar’s position as a global leader in large-scale solar deployments

- In May 2023, DuPont revealed plans to introduce its latest Tedlar frontsheet materials at the 2023 SNEC International Photovoltaic Power Generation and Smart Energy Exhibition, held at the Shanghai New International Expo Center, Booth W4-555. The objective was to demonstrate the advanced capabilities of its materials to partners and end-users in the photovoltaic industry. This launch emphasized DuPont’s commitment to innovation and sustainability in solar technology

- In March 2023, JinkoSolar introduced its new liquid cooling energy storage system tailored for commercial and industrial (C&I) applications and showcased it at PV Japan 2023. The system is designed to enhance energy storage efficiency and cooling performance. This development marked a step forward in JinkoSolar’s expansion into advanced energy storage solutions

- In January 2022, JinkoSolar launched the second-generation Tiger Neo, offering improved power efficiency and enhanced performance under various environmental conditions. This upgraded module targets both residential and commercial solar markets. The release of the second-generation Tiger Neo highlighted JinkoSolar’s continuous innovation in solar module technology

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Photovoltaic Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Photovoltaic Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Photovoltaic Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.