Global Pc As A Service Market

Market Size in USD Billion

USD

116.42 Billion

USD

2,635.42 Billion

2025

2033

USD

116.42 Billion

USD

2,635.42 Billion

2025

2033

| 2026 - 2033 | |

| USD 116.42 Billion | |

| USD 2,635.42 Billion | |

| % | |

|

Personal Computer (PC) as a Service Market Size

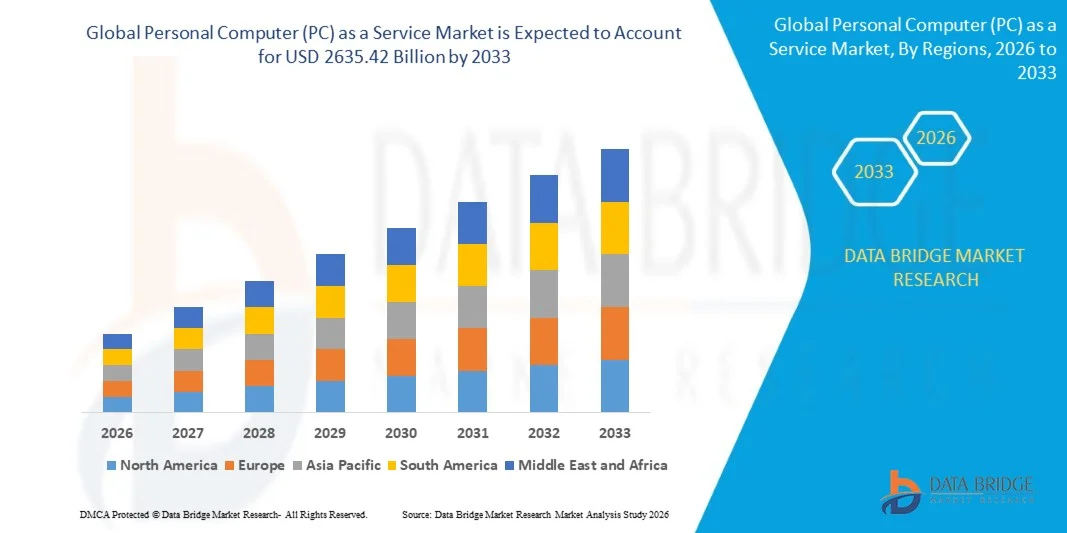

- The global Personal Computer (PC) as a Service market size was valued at USD 116.42 billion in 2025 and is expected to reach USD 2635.42 billion by 2033, at a CAGR of 47.69% during the forecast period

- The market growth is largely fueled by the increasing adoption of subscription-based IT solutions and technological advancements in PC lifecycle management, leading to more efficient and scalable IT infrastructure for enterprises of all sizes

- Furthermore, rising demand from organizations for flexible, cost-effective, and fully managed computing solutions is establishing PC as a Service as the preferred model for device procurement and IT management. These converging factors are accelerating the uptake of PCaaS offerings, thereby significantly boosting the industry’s growth

Personal Computer (PC) as a Service Market Analysis

- Personal Computer (PC) as a Service is a subscription-based IT model where organizations acquire hardware, software, and management services under a unified subscription plan. These solutions include device provisioning, software updates, endpoint security, and lifecycle management, enabling enterprises to streamline IT operations and reduce upfront capital expenditure

- The escalating demand for Personal Computer (PC) as a Service is primarily fueled by the shift toward hybrid and remote work models, increasing digital transformation initiatives, and the need for predictable IT costs and simplified device management. Enterprises are increasingly leveraging Personal Computer (PC) as a Service to ensure secure, scalable, and productivity-enhancing IT infrastructure across multiple locations

- North America dominated the Personal Computer (PC) as a Service market with a share of 38.4% in 2025, due to the widespread adoption of subscription-based IT solutions and the growing emphasis on workforce mobility and remote work

- Asia-Pacific is expected to be the fastest growing region in the Personal Computer (PC) as a Service market during the forecast period due to increasing digitalization, rising enterprise IT budgets, and adoption of hybrid work models in countries such as China, Japan, and India

- Hardware segment dominated the market with a market share of 48% in 2025, due to the increasing demand for ready-to-deploy PCs with pre-configured specifications and enhanced performance. Organizations prefer hardware-inclusive Personal Computer (PC) as a Service solutions to reduce upfront capital expenditure and simplify lifecycle management through leasing models. The growing focus on employee productivity and efficient IT infrastructure further fuels demand for hardware offerings

Report Scope and Personal Computer (PC) as a Service Market Segmentation

|

Attributes |

Personal Computer (PC) as a Service Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Personal Computer (PC) as a Service Market Trends

“Growth of Subscription-Based PC and Managed IT Solutions”

- A prominent trend in the Personal Computer (PC) as a Service market is the increasing shift toward subscription-based PC models and managed IT solutions, driven by the rising need for flexible, scalable, and cost-efficient computing infrastructures in enterprises. This shift allows organizations to access the latest hardware and software without upfront capital expenditure while benefiting from integrated support and lifecycle management

- For instance, Dell Technologies and HP Inc. offer comprehensive Personal Computer (PC) as a Service solutions that include device procurement, deployment, management, and refresh cycles for businesses of various sizes. These solutions enable companies to streamline IT operations and reduce the burden of in-house hardware management

- The adoption of Personal Computer (PC) as a Service is growing rapidly among remote and hybrid work environments, where flexible device provisioning and centralized management ensure productivity and security. Enterprises are increasingly leveraging these services to quickly onboard employees with standardized, secure devices

- Small and medium-sized businesses are embracing Personal Computer (PC) as a Service to gain access to enterprise-grade computing capabilities without the financial strain of large capital investments. This trend is facilitating digital transformation initiatives and enabling faster technology adoption across sectors

- Cloud integration and virtual desktop infrastructure (VDI) are enhancing the value proposition of Personal Computer (PC) as a Service by enabling seamless access to corporate applications and data from anywhere. This integration supports operational continuity and improves overall IT efficiency

- The market is witnessing strong growth in managed IT services bundled with Personal Computer (PC) as a Service offerings, which include software updates, security monitoring, and asset tracking. This combination is positioning Personal Computer (PC) as a Service as a comprehensive IT solution that aligns with modern business needs

Personal Computer (PC) as a Service Market Dynamics

Driver

“Rising Demand for Flexible and Cost-Effective IT Services”

- The growing need for adaptable IT infrastructures and cost-efficient hardware management is driving the demand for Personal Computer (PC) as a Service, enabling businesses to scale operations without large capital expenditures. Personal Computer (PC) as a Service offers lifecycle management, support services, and hardware refresh options that enhance operational efficiency

- For instance, Lenovo’s Personal Computer (PC) as a Service offerings provide managed devices and support services that allow enterprises to reduce IT overhead while ensuring the latest technology is available to employees. These services improve device uptime, reduce maintenance burdens, and optimize total cost of ownership

- The shift toward hybrid work models is intensifying demand for flexible device deployment and remote management capabilities. Organizations prefer Personal Computer (PC) as a Service to quickly provision, secure, and manage devices across dispersed teams

- Enterprises are increasingly seeking predictable IT expenditure models that Personal Computer (PC) as a Service delivers through subscription-based plans. This financial predictability helps in budgeting, resource planning, and avoiding unexpected capital investments

- Rising focus on digital transformation and IT modernization initiatives is encouraging businesses to adopt managed PC solutions. The integration of device management, security, and support in Personal Computer (PC) as a Service strengthens IT governance and overall workforce productivity

Restraint/Challenge

“High Setup Costs and Integration Complexity”

- The Personal Computer (PC) as a Service market faces challenges from high initial setup costs associated with device procurement, onboarding, and integration into existing IT environments. Organizations must align hardware, software, and support frameworks, which can involve significant technical and financial resources

- For instance, deploying HP’s Personal Computer (PC) as a Service solutions in large enterprises requires careful planning to integrate with legacy IT systems and ensure seamless workflow continuity. This process demands skilled IT teams and can extend deployment timelines

- The complexity of integrating Personal Computer (PC) as a Service with diverse enterprise applications and security protocols presents additional challenges. Ensuring compatibility with existing IT infrastructure and maintaining data security adds layers of operational effort

- Managing service-level agreements (SLAs), asset tracking, and support logistics for large-scale deployments increases operational complexity. Enterprises must maintain coordination between internal IT teams and service providers to meet performance and compliance expectations

- The market continues to encounter constraints related to balancing customization needs with standardized service offerings. These challenges necessitate careful strategy and resource allocation, influencing adoption pace and overall market growth

Personal Computer (PC) as a Service Market Scope

The market is segmented on the basis of offering, enterprise type, and end-user industry.

• By Offering

On the basis of offering, the Personal Computer (PC) as a Service market is segmented into hardware, software and software maintenance, and services. The hardware segment dominated the largest market revenue share of 48% in 2025, driven by the increasing demand for ready-to-deploy PCs with pre-configured specifications and enhanced performance. Organizations prefer hardware-inclusive Personal Computer (PC) as a Service solutions to reduce upfront capital expenditure and simplify lifecycle management through leasing models. The growing focus on employee productivity and efficient IT infrastructure further fuels demand for hardware offerings. Vendors offering hardware along with bundled support and warranty services gain preference among enterprises seeking predictable operational costs.

The software and software maintenance segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by enterprises’ increasing adoption of cloud-based applications and continuous software updates. For instance, companies such as Dell Technologies provide software management packages within Personal Computer (PC) as a Service, enabling real-time monitoring, patch management, and endpoint security. Organizations increasingly rely on software maintenance services to ensure seamless device performance and compliance with security protocols. The demand is particularly strong in sectors with high regulatory requirements, where software reliability and timely updates are critical. The integration of software management with analytics and remote support enhances operational efficiency, boosting adoption in both SMBs and large enterprises.

• By Enterprise Type

On the basis of enterprise type, the Personal Computer (PC) as a Service market is segmented into small and medium-sized enterprises (SMEs) and large enterprises. Large enterprises dominated the largest market revenue share in 2025, driven by their need for scalable IT infrastructure and centralized management of large employee workforces. Personal Computer (PC) as a Service provides these organizations with predictable costs, easy device deployment, and uniform IT policies across multiple locations. Enterprises increasingly adopt Personal Computer (PC) as a Service to reduce the burden on internal IT teams while ensuring device standardization and lifecycle management. Solutions catering to large enterprises often include enhanced security features, remote monitoring, and managed services, making them highly attractive for corporate environments.

The small and medium-sized enterprises segment is expected to witness the fastest CAGR from 2026 to 2033, fueled by the growing adoption of flexible subscription-based PC solutions. For instance, HP’s Personal Computer (PC) as a Service offerings allow SMEs to access high-performance hardware without heavy upfront investment, providing predictable costs and scalable infrastructure. SMEs prefer Personal Computer (PC) as a Service solutions to support remote workforces and hybrid working models, ensuring business continuity and productivity. The ability to integrate hardware, software, and support services within a single subscription package further accelerates adoption in SMEs.

• By End User Industry

On the basis of end-user industry, the Personal Computer (PC) as a Service market is segmented into banking, financial services, and insurance (BFSI), government, education, healthcare and life sciences, IT and telecommunications, and others. The IT and telecommunications industry dominated the largest market revenue share in 2025, driven by the sector’s rapid digital transformation and demand for high-performance computing devices. Enterprises in IT and telecom increasingly adopt Personal Computer (PC) as a Service to ensure fast deployment of devices, simplified IT management, and compliance with security protocols. Personal Computer (PC) as a Service also enables centralized monitoring, software updates, and remote troubleshooting, which are critical in IT-heavy environments.

The healthcare and life sciences industry is expected to witness the fastest growth from 2026 to 2033, fueled by the rising need for secure, compliant, and reliable computing solutions. For instance, Lenovo’s Personal Computer (PC) as a Service offerings for healthcare organizations provide integrated software management, endpoint security, and device lifecycle support, ensuring adherence to regulatory requirements such as HIPAA. The growth is further supported by the increasing adoption of telemedicine, research analytics, and digital patient management systems, which require high-performance PCs with robust support services. The ability to scale subscriptions based on workforce size and usage patterns makes Personal Computer (PC) as a Service highly attractive in healthcare and life sciences.

Personal Computer (PC) as a Service Market Regional Analysis

- North America dominated the Personal Computer (PC) as a Service market with the largest revenue share of 38.4% in 2025, driven by the widespread adoption of subscription-based IT solutions and the growing emphasis on workforce mobility and remote work

- Enterprises in the region increasingly prefer PCaaS for predictable IT costs, simplified device management, and centralized monitoring, enabling seamless integration with existing IT infrastructure and cloud services

- The strong presence of major vendors, high technological awareness, and increasing investment in digital transformation initiatives are further fueling market growth, making PCaaS a preferred solution for both SMEs and large enterprises

U.S. Personal Computer (PC) as a Service Market Insight

The U.S. Personal Computer (PC) as a Service market captured the largest revenue share in 2025 within North America, fueled by the rapid adoption of cloud computing, hybrid work models, and scalable subscription-based IT services. Organizations are prioritizing operational efficiency and reduced IT overhead through Personal Computer (PC) as a Service, which provides hardware, software, and support in a single package. The growing demand for remote device management, software updates, and endpoint security, coupled with integration capabilities with enterprise applications, is significantly contributing to market expansion.

Europe Personal Computer (PC) as a Service Market Insight

The Europe Personal Computer (PC) as a Service market is projected to expand at a substantial CAGR during the forecast period, primarily driven by the need for cost-effective IT infrastructure and digital workplace transformation. Increasing urbanization, growing adoption of cloud-based services, and stringent data security regulations are encouraging enterprises to adopt Personal Computer (PC) as a Service. European organizations value the flexibility, centralized device management, and predictable subscription costs offered by Personal Computer (PC) as a Service, supporting adoption across large enterprises and SMEs.

U.K. Personal Computer (PC) as a Service Market Insight

The U.K. Personal Computer (PC) as a Service market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by rising demand for flexible IT solutions and the adoption of hybrid and remote working models. Organizations are increasingly implementing Personal Computer (PC) as a Service to ensure business continuity, reduce capital expenditure, and enable secure device management. The strong digital infrastructure, coupled with increasing investments in IT modernization, continues to drive market growth in both corporate and public sectors.

Germany Personal Computer (PC) as a Service Market Insight

The Germany Personal Computer (PC) as a Service market is expected to expand at a considerable CAGR during the forecast period, driven by enterprises’ focus on IT efficiency, digital transformation, and compliance with data protection regulations. Germany’s advanced technological ecosystem, coupled with increasing IT budgets, supports the deployment of Personal Computer (PC) as a Service across various industries. Businesses are leveraging Personal Computer (PC) as a Service to simplify lifecycle management, integrate endpoint security, and enable standardized IT policies across multiple offices.

Asia-Pacific Personal Computer (PC) as a Service Market Insight

The Asia-Pacific Personal Computer (PC) as a Service market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing digitalization, rising enterprise IT budgets, and adoption of hybrid work models in countries such as China, Japan, and India. Organizations are increasingly implementing Personal Computer (PC) as a Service to support scalable IT infrastructure and remote workforce management. Furthermore, the presence of global and regional Personal Computer (PC) as a Service providers and government initiatives promoting technology adoption are expanding accessibility and affordability across SMEs and large enterprises.

Japan Personal Computer (PC) as a Service Market Insight

The Japan Personal Computer (PC) as a Service market is gaining momentum due to the country’s strong emphasis on digital workplace solutions, enterprise automation, and IT modernization. Organizations prioritize Personal Computer (PC) as a Service to streamline device management, enhance endpoint security, and support hybrid work environments. The integration of Personal Computer (PC) as a Service with cloud services and enterprise applications, combined with a focus on productivity and operational efficiency, is driving market growth in both corporate and public sectors.

China Personal Computer (PC) as a Service Market Insight

The China Personal Computer (PC) as a Service market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid enterprise digitalization, high adoption of subscription-based IT models, and the presence of leading domestic and international Personal Computer (PC) as a Service providers. Chinese organizations increasingly prefer Personal Computer (PC) as a Service to reduce IT management complexity, optimize costs, and ensure secure and scalable device deployment. The government’s push towards smart enterprises and digital transformation initiatives further accelerates the adoption of Personal Computer (PC) as a Service solutions across industries.

Personal Computer (PC) as a Service Market Share

The Personal Computer (PC) as a Service industry is primarily led by well-established companies, including:

- Lenovo (China)

- HP India Sales Private Limited (India)

- Dell Inc. (U.S.)

- CompuCom Systems Inc. (U.S.)

- Microsoft (U.S.)

- Hemmersbach Holding GmbH (Germany)

- Service IT Direct (U.K.)

- StarHub (Singapore)

- Telia (Sweden)

- Arrow Electronics Inc. (U.S.)

- Utopic Software (U.S.)

- SHI International Corp (U.S.)

- Softcat plc (U.K.)

- CSA (Australia)

- PC Connection Inc. (U.S.)

- ATEA Group (Norway)

- Zones LLC (U.S.)

- Intel Corporation (U.S.)

- XMA LTD (U.K.)

- CHG-MERIDIAN (Germany)

- Innova Solutions (U.S.)

- Capgemini (France)

- RAM-Tech PC Solutions LLC (U.S.)

- SYNNEX Corporation (U.S.)

- Panasonic Corporation (Japan)

- Computacentre (UK) Ltd (U.K.)

Latest Developments in Global Personal Computer (PC) as a Service Market

- In December 2025, Asus India announced plans to raise AI-enabled laptop penetration to 30% by the end of 2026 through subscription bundles with system integrators. This initiative is expected to significantly drive PCaaS adoption in India, as organizations and educational institutions can access high-performance, AI-capable devices without heavy upfront investment. The subscription bundles make it easier for SMEs and schools to deploy advanced technology while ensuring ongoing support, updates, and warranty coverage. This move also signals a broader market trend where hardware vendors are leveraging PCaaS models to increase device reach and integrate AI capabilities, positioning subscription-based solutions as a strategic enabler for workforce productivity and digital transformation initiatives

- In October 2025, Microsoft ended support for Windows 10, creating a global surge in device refresh demand. This development is accelerating the PCaaS market worldwide, as enterprises seek cost-effective, zero-upfront-cost subscription solutions to replace legacy devices. Organizations are motivated to ensure compliance with updated software, enhance endpoint security, and enable employees with modern operating systems and productivity tools. The end-of-support scenario has also increased awareness among IT decision-makers about the benefits of managed PCaaS solutions, including automated updates, centralized device monitoring, and predictable subscription costs, making PCaaS a preferred option for global enterprises looking to modernize their IT infrastructure efficiently

- In July 2025, the EU Ecodesign Regulation entered into enforcement, mandating higher energy efficiency and sustainable design for electronic devices. This regulatory shift is promoting the adoption of PCaaS models in Europe that incorporate centralized take-back programs and managed lifecycle services. Enterprises are increasingly seeking subscription solutions that help meet ESG goals, reduce e-waste, and optimize device usage while lowering total cost of ownership. The regulation reinforces the attractiveness of PCaaS for companies prioritizing sustainability, as subscription providers can offer fully managed devices, automated updates, and environmentally responsible disposal, aligning IT infrastructure management with broader corporate responsibility objectives

- In March 2025, Canalys reported that India’s PC market grew 8.1% year on year, highlighting robust demand for computing devices across enterprises, SMEs, and educational institutions. This growth underlines a strong market opportunity for PCaaS providers, as subscription-based models allow organizations to scale device deployment in line with expanding digital needs. Businesses can leverage flexible financing, device management, and bundled software services to meet increasing IT requirements without large capital expenditures. The report also indicates that Indian enterprises are rapidly embracing digital transformation, with PCaaS emerging as a key enabler to support hybrid work models, remote operations, and workforce productivity improvements

- In January 2025, Google, Temasek, and Bain documented Southeast Asia’s USD 300 billion digital economy, emphasizing subscription financing as a critical enabler for SMEs to acquire digital tools. This finding highlights the potential for PCaaS adoption in the region, as subscription models allow businesses to access high-performance PCs, software, and managed services without upfront costs. SMEs benefit from predictable operational expenses, simplified IT management, and scalable infrastructure that can grow with business needs. The report reinforces that as Southeast Asia continues to digitize rapidly, PCaaS will play a central role in supporting business modernization, IT accessibility, and the broader development of a digital-first economy across industries

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Pc As A Service Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Pc As A Service Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Pc As A Service Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.