Global Optical Coherence Tomography For Ophthalmology Market

Market Size in USD Million

CAGR :

%

USD

265.96 Million

USD

449.16 Million

2025

2033

USD

265.96 Million

USD

449.16 Million

2025

2033

| 2026 –2033 | |

| USD 265.96 Million | |

| USD 449.16 Million | |

| % | |

|

Optical Coherence Tomography for Ophthalmology Market Size

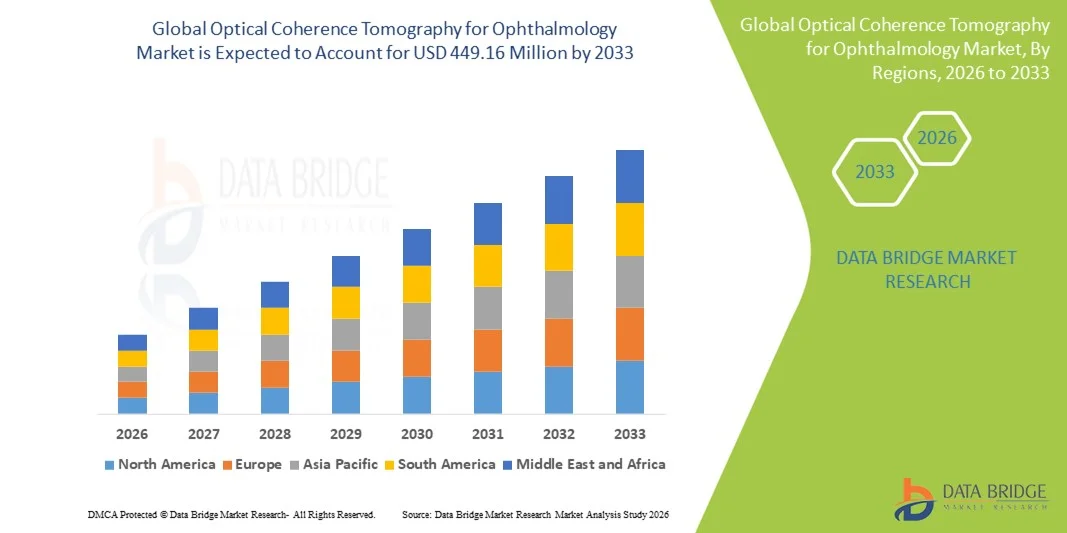

- The global optical coherence tomography for ophthalmology market size was valued at USD 265.96 Million in 2025 and is expected to reach USD 449.16 Million by 2033, at a CAGR of 6.77% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced ophthalmic imaging technologies and continuous technological progress in optical coherence tomography systems, leading to improved diagnostic accuracy and early detection of retinal and anterior segment disorders across hospitals and eye care clinics

- Furthermore, rising demand for non-invasive, high-resolution imaging solutions, along with growing prevalence of age-related eye diseases such as glaucoma, diabetic retinopathy, and macular degeneration, is establishing OCT as a core diagnostic modality in ophthalmology. These converging factors are accelerating the uptake of optical coherence tomography solutions, thereby significantly boosting overall market growth

Optical Coherence Tomography for Ophthalmology Market Analysis

- Optical coherence tomography systems, which provide high-resolution, non-invasive cross-sectional imaging of ocular tissues, are increasingly vital components of modern ophthalmic diagnostics across hospitals and eye care clinics due to their ability to enable early detection and monitoring of retinal and optic nerve disorders

- The escalating demand for OCT systems is primarily fueled by the rising prevalence of eye diseases such as glaucoma, diabetic retinopathy, and age-related macular degeneration, along with increasing adoption of advanced imaging technologies that improve diagnostic accuracy and clinical decision-making

- North America dominated the optical coherence tomography for ophthalmology market with the largest revenue share of approximately 42.5% in 2025, supported by advanced healthcare infrastructure, high adoption of innovative ophthalmic imaging technologies, favorable reimbursement policies, and a strong presence of leading OCT manufacturers, with the U.S. accounting for a major portion of regional demand

- Asia-Pacific is expected to be the fastest-growing region in the optical coherence tomography for ophthalmology market during the forecast period, registering a CAGR of approximately 20.9%, driven by a rapidly aging population, increasing incidence of vision-related disorders, expanding access to eye care services, and rising healthcare investments across emerging economies

- The semi-automatic segment dominated the largest market revenue share of 53.2% in 2025, driven by the widespread use of manual operation with clinical control for accurate imaging

Report Scope and Optical Coherence Tomography for Ophthalmology Market Segmentation

|

Attributes |

Optical Coherence Tomography for Ophthalmology Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Optical Coherence Tomography for Ophthalmology Market Trends

Enhanced Diagnostic Precision Through AI Integration and Automated Imaging

- A major trend in the global Optical Coherence Tomography for Ophthalmology market is the increasing integration of artificial intelligence (AI) with OCT systems. AI-powered OCT is improving diagnostic accuracy and reducing interpretation time, enabling clinicians to detect retinal diseases earlier and with higher confidence

- For instance, AI algorithms are now being used to automatically detect retinal abnormalities, classify disease severity, and provide quantitative analysis of retinal layers. This automation helps ophthalmologists to streamline workflow and deliver faster patient care

- AI integration also supports real-time image enhancement and noise reduction, allowing clearer visualization of retinal structures even in challenging imaging conditions

- The adoption of AI-driven OCT is especially significant in the management of diseases such as diabetic retinopathy, age-related macular degeneration (AMD), glaucoma, and retinal vein occlusion, where early detection is critical

- This trend is reshaping clinical expectations, driving demand for more advanced OCT systems that combine high-resolution imaging, AI analysis, and cloud-based data management

Optical Coherence Tomography for Ophthalmology Market Dynamics

Driver

Growing Prevalence of Retinal Disorders and Rising Demand for Early Diagnosis

- Increasing incidence of retinal diseases such as diabetic retinopathy, glaucoma, and AMD is a key driver for OCT market growth. The global rise in diabetes and aging populations is contributing to higher demand for advanced retinal imaging

- OCT systems offer non-invasive, high-resolution cross-sectional imaging of retinal layers, making them essential for early diagnosis and monitoring of progressive eye disorders

- For instance, Hospitals in the US and Europe widely use OCT for routine retinal screening, especially for diabetic patients

- The expanding adoption of OCT in ophthalmology clinics, hospitals, and diagnostic centers is further boosting market demand

- Increasing awareness about vision care and preventive ophthalmology is encouraging patients to undergo regular eye examinations, supporting the growth of OCT adoption

- Technological advancements, such as swept-source OCT, OCT angiography, and handheld OCT devices, are expanding the clinical applications and improving patient accessibility

Restraint/Challenge

High Equipment Cost and Limited Reimbursement Policies

- One major challenge for OCT market growth is the high initial cost of advanced OCT systems, which can limit adoption, especially in developing regions and smaller clinics

- Many advanced OCT devices require significant capital investment, and limited reimbursement policies for diagnostic imaging can discourage providers from upgrading equipment

- For instance, in several developing countries, reimbursement for OCT diagnostics is limited, making it difficult for clinics to justify the investment

- In addition, training and expertise requirements for interpreting OCT images can be a barrier in regions with fewer specialized ophthalmologists

- Ensuring affordability through cost-effective devices and bundled service models will be essential for broader market penetration

Optical Coherence Tomography for Ophthalmology Market Scope

The market is segmented on the basis of product, technology, type, and end user.

- By Product

On the basis of product, the Optical Coherence Tomography for Ophthalmology market is segmented into handheld OCT devices, tabletop OCT devices, and catheter-based OCT devices. The tabletop OCT devices segment dominated the largest market revenue share of 45.8% in 2025, driven by its high-resolution imaging and wide adoption in hospitals and advanced ophthalmology clinics. Tabletop OCT systems are preferred for their stability, ease of use, and integration with existing diagnostic workflows. These devices provide superior image clarity, enabling accurate retinal and glaucoma diagnosis. Hospitals and large clinics invest heavily in tabletop OCT due to their advanced features and long-term reliability. Their strong presence in developed regions contributes significantly to revenue share. Furthermore, tabletop OCT systems support multi-modality imaging and AI integration, which enhances diagnostic efficiency. These devices are also widely used for clinical trials and research, boosting adoption. As a result, tabletop OCT remains the dominant product segment in the global market.

The handheld OCT devices segment is anticipated to witness the fastest CAGR of 22.4% from 2026 to 2033, driven by growing demand for portable diagnostics in remote and pediatric healthcare settings. Handheld OCT is increasingly used in neonatal and pediatric ophthalmology, where patient cooperation is limited. Its portability enables on-site imaging in outreach programs and rural clinics. Rising prevalence of eye disorders in underserved regions supports adoption. Manufacturers are improving handheld device accuracy, making them comparable to tabletop systems. Reduced cost and ease of transportation also encourage usage. In addition, handheld OCT is becoming essential in emergency and critical care units for rapid eye assessment. Continuous technological advancements, such as wireless connectivity and AI-assisted imaging, further boost growth. Overall, handheld OCT is expected to expand rapidly in emerging markets and mobile healthcare environments.

- By Technology

On the basis of technology, the Optical Coherence Tomography for Ophthalmology market is segmented into time domain OCT, frequency domain OCT, spatial encoded frequency, spectral-domain, and swept-source. The spectral-domain OCT segment dominated the largest market revenue share of 47.6% in 2025, driven by its high imaging speed and superior resolution for retinal diagnosis. Spectral-domain OCT is widely used in retinal clinics and hospitals due to its reliable performance in diagnosing macular degeneration and diabetic retinopathy. The technology enables fast acquisition of high-quality images, which improves patient throughput. It also supports advanced analytics and AI-based diagnostic tools. Many leading OCT manufacturers focus on spectral-domain systems, strengthening their market dominance. Clinical preference for spectral-domain OCT remains strong due to established evidence and long-term adoption. In addition, integration with ophthalmic EMR systems increases its utility in large healthcare facilities. As a result, spectral-domain OCT holds the largest revenue share in 2025.

The swept-source OCT segment is expected to witness the fastest CAGR of 23.1% from 2026 to 2033, fueled by its deeper tissue penetration and enhanced imaging speed. Swept-source OCT is increasingly used for posterior segment imaging and glaucoma assessment. It provides accurate axial length measurement and supports advanced IOL planning. The growing adoption of swept-source OCT in premium eye care centers is driving market growth. Increasing research and development in swept-source technology is expanding its clinical applications. Also, its compatibility with multimodal imaging platforms enhances adoption. The growing trend of personalized ophthalmic diagnostics further accelerates demand. As a result, swept-source OCT is expected to experience rapid expansion in the forecast period.

- By Type

On the basis of type, the Optical Coherence Tomography for Ophthalmology market is segmented into semi-automatic and fully automatic. The semi-automatic segment dominated the largest market revenue share of 53.2% in 2025, driven by the widespread use of manual operation with clinical control for accurate imaging. Semi-automatic OCT devices are preferred in hospitals and diagnostic centers where trained technicians perform scans. The ability to adjust imaging parameters manually provides high flexibility and better control in complex cases. This type is especially popular in retinal and glaucoma clinics where detailed image capture is essential. Semi-automatic systems are also cost-effective compared to fully automatic solutions, supporting adoption in developing regions. Many clinics prefer semi-automatic devices due to existing staff expertise and workflow familiarity. Moreover, semi-automatic OCT offers better customization for complex patients. As a result, it remains the dominant segment in 2025.

The fully automatic segment is anticipated to witness the fastest CAGR of 21.9% from 2026 to 2033, driven by the growing demand for AI-enabled imaging and simplified workflow. Fully automatic OCT devices are preferred in high-volume settings such as large hospitals and surgical centers. These systems reduce operator dependency and provide faster scan acquisition. Increasing integration of AI for automatic diagnosis and report generation boosts adoption. Fully automatic OCT is also gaining traction in clinics aiming to reduce training requirements. The demand for remote ophthalmic screening and telemedicine is accelerating growth. As a result, fully automatic OCT devices are expected to expand rapidly during the forecast period.

- By End User

On the basis of end user, the Optical Coherence Tomography for Ophthalmology market is segmented into hospitals, clinics, ASCs, physicians’ offices, and others. The hospitals segment accounted for the largest market revenue share of 41.9% in 2025, driven by high patient volumes and advanced ophthalmic infrastructure. Hospitals invest in OCT systems to support large-scale retinal and glaucoma screening. The presence of skilled ophthalmologists and strong diagnostic capabilities enhances adoption. In addition, hospitals are central hubs for clinical trials and research, increasing OCT utilization. High budget allocation and strong reimbursement support further drive hospital adoption. The need for multi-modal imaging in tertiary care settings strengthens market dominance. Hospitals also focus on premium patient care and accurate diagnostics, supporting OCT investment. As a result, hospitals remain the largest end-user segment.

The clinics segment is expected to witness the fastest CAGR of 22.6% from 2026 to 2033, driven by the expansion of specialty ophthalmology centers and outpatient services. Clinics are increasingly adopting OCT systems to improve diagnostic efficiency and patient experience. Rising prevalence of eye disorders and growing outpatient surgery demand are key growth drivers. Lower cost of ownership and improved portability make OCT suitable for clinics. Clinics also benefit from AI-enabled diagnostic tools, which reduce dependency on specialist interpretation. The expansion of private eye care chains in emerging markets further boosts adoption. As a result, clinics are expected to grow rapidly during the forecast period.

Optical Coherence Tomography for Ophthalmology Market Regional Analysis

- North America dominated the optical coherence tomography for ophthalmology market with the largest revenue share of approximately 42.5% in 2025. This strong position is supported by advanced healthcare infrastructure, high adoption of innovative ophthalmic imaging technologies, favorable reimbursement policies, and a strong presence of leading OCT manufacturers

- The market accounted for a major portion of the regional demand. The region also faces a high prevalence of eye diseases such as age-related macular degeneration (AMD), diabetic retinopathy, and glaucoma, which increases the need for advanced OCT diagnostics

- In addition, the rapid adoption of AI-integrated OCT systems and OCT angiography is improving diagnostic accuracy and patient outcomes, further driving market growth

U.S. Optical Coherence Tomography for Ophthalmology Market Insight

The U.S. optical coherence tomography for ophthalmology market captured the largest revenue share in 2025 within North America. This growth is driven by a strong focus on early diagnosis and advanced eye care services. Rapid adoption of cutting-edge imaging systems, high healthcare spending, and well-established ophthalmology clinics and hospitals are major factors supporting market growth. Furthermore, favorable reimbursement policies and continuous technological innovation in OCT devices are accelerating the market expansion in the U.S.

Europe Optical Coherence Tomography for Ophthalmology Market Insight

The Europe optical coherence tomography for ophthalmology market is projected to expand at a substantial CAGR during the forecast period, driven by well-developed healthcare infrastructure, increasing public awareness about eye diseases, and the growing prevalence of retinal disorders. Strict regulations related to medical diagnostics and the increasing adoption of advanced imaging systems in hospitals and diagnostic centers are supporting market growth. The demand for OCT devices is also rising due to increasing cases of diabetes-related eye complications and glaucoma across the region.

U.K. Optical Coherence Tomography for Ophthalmology Market Insight

The U.K. optical coherence tomography for ophthalmology market is anticipated to grow at a noteworthy CAGR, supported by increasing demand for early detection of retinal diseases and the growing use of advanced ophthalmic imaging technologies. High adoption of modern diagnostic tools in both public and private healthcare sectors, along with increasing government initiatives for vision care, is expected to drive market growth. The U.K. is also seeing a rise in OCT usage in optometry clinics, improving access to advanced retinal diagnostics.

Germany Optical Coherence Tomography for Ophthalmology Market Insight

Germany’s optical coherence tomography for ophthalmology market is expected to expand significantly during the forecast period, driven by a strong focus on healthcare innovation and advanced diagnostic technologies. The country’s robust healthcare infrastructure and high investment in medical equipment encourage the adoption of OCT devices in hospitals and specialty clinics. Growing awareness about eye care and preventive ophthalmology is further boosting demand for OCT systems.

Asia-Pacific Optical Coherence Tomography for Ophthalmology Market Insight

Asia-Pacific optical coherence tomography for ophthalmology market is expected to be the fastest-growing region in the optical coherence tomography for ophthalmology market during the forecast period, registering a CAGR of approximately 20.9%. This rapid growth is driven by a rapidly aging population, increasing incidence of vision-related disorders, expanding access to eye care services, and rising healthcare investments across emerging economies. Growing healthcare infrastructure, rising disposable income, and an increasing number of ophthalmology clinics are fueling the adoption of OCT devices in countries like China, India, and Japan. Increasing awareness about eye care and early disease diagnosis is also supporting market growth in the region.

Japan Optical Coherence Tomography for Ophthalmology Market Insight

Japan’s optical coherence tomography for ophthalmology market is gaining momentum due to a high prevalence of age-related eye disorders and strong technological advancement in medical devices. The country’s aging population and high healthcare expenditure are increasing demand for advanced retinal imaging systems. Japan is also witnessing adoption of OCT angiography and AI-enabled OCT solutions, enhancing early detection of retinal diseases.

China Optical Coherence Tomography for Ophthalmology Market Insight

China optical coherence tomography for ophthalmology market accounted for the largest market revenue share in Asia-Pacific in 2025, supported by rising healthcare investments, growing number of eye care clinics, and increasing adoption of advanced diagnostic imaging devices. The country’s expanding middle-class population and high prevalence of diabetes-related eye diseases are driving demand for OCT systems. Increasing government focus on improving healthcare access and medical infrastructure is also supporting OCT market growth.

Optical Coherence Tomography for Ophthalmology Market Share

The Optical Coherence Tomography for Ophthalmology industry is primarily led by well-established companies, including:

- Carl Zeiss Meditec (Germany)

- Heidelberg Engineering (Germany)

- Topcon Corporation (Japan)

- NIDEK Co., Ltd. (Japan)

- Canon Medical Systems (Japan)

- Optovue (U.S.)

- Alcon (Switzerland)

- Johnson & Johnson Vision (U.S.)

- Bausch + Lomb (U.S.)

- Canon (Japan)

- Optos (U.K.)

- OptoVue (U.S.)

- Tomey Corporation (Japan)

- Carl Zeiss (Germany)

- Quantel Medical (France)

- Optikon (Italy)

Latest Developments in Global Optical Coherence Tomography for Ophthalmology Market

- In August 2023, Heidelberg Engineering launched an upgraded Spectralis OCT 2 platform, which incorporated enhanced imaging capabilities and deep-learning analysis tools to assist in more precise diagnosis and disease monitoring of glaucoma and other retinal conditions. This upgrade brought new software algorithms and improved hardware responsiveness that expanded clinical utility, particularly in large eye care centers and research hospitals. Adoption of Spectralis OCT 2 contributed to Heidelberg’s leadership in advanced ophthalmic imaging technologies

- In September 2023, Orbis International partnered with Heidelberg Engineering Inc. to expand vision services and training programs, including OCT education, especially in underserved regions. The partnership focused on enabling clinicians in developing countries to use advanced OCT technologies more effectively through webinars, funded teaching opportunities, and resource support. This collaboration enhanced OCT training outreach and supported broader global access to advanced ocular diagnostics

- In September 2023, Topcon Healthcare expanded its AI integration efforts in OCT by partnering with RetInSight GmbH, aiming to integrate RetInSight’s AI-based retinal biomarker analysis with Topcon’s OCT imaging systems. This collaboration sought to enhance the diagnostic precision and automated analysis capabilities of OCT devices, especially in chronic retinal disease screening workflows

- In June 2024, NIDEK Co., Ltd. launched its RS-1 Glauvas OCT system, a next-generation ophthalmic OCT device featuring 250 kHz scan speed and deep, wide-area imaging capabilities, along with integrated deep-learning analytics to assist clinicians in managing glaucoma and retinal diseases more effectively. The launch expanded NIDEK’s presence in high-performance imaging for eye care and demonstrated increasing industry emphasis on AI-assisted ocular diagnostics

- In May 2024, ZEISS Medical Technology announced enhancements to its CIRRUS 6000 OCT platform, including an expanded U.S. OCT reference database and enhanced cybersecurity features, strengthening its data-driven imaging solutions for ophthalmologists and enabling more secure and integrated clinical workflows. These enhancements reinforced the platform’s competitive edge in advanced retinal imaging and patient data handling

- In July 2024, Heidelberg Engineering received FDA clearance for the SPECTRALIS OCTA Module with SHIFT technology, which significantly reduced image acquisition times by up to 50% while delivering high-resolution OCT angiography imaging. This regulatory milestone expanded the clinical usability and adoption potential of advanced OCTA imaging in the U.S. market, supporting rapid vascular assessments in retinal disease management

- In May 2025, Intalight received CE Mark approval for its DREAM OCT platform, enabling commercialization throughout Europe. This next-generation swept-source OCT system offered ultrawide-field and super-depth imaging with integrated OCT angiography capabilities, enhancing retinal diagnostics and contributing to broader adoption of advanced OCT technologies in European ophthalmic practices

- In July 2024, EssilorLuxottica confirmed the acquisition of an 80% stake in Heidelberg Engineering, a major strategic consolidation that unified one of the world’s largest eyewear/eyecare services groups with a key OCT imaging technology provider. This acquisition (announced mid-2024 and finalized in late 2024) is expected to expand direct clinical channel access for OCT innovations through EssilorLuxottica’s global clinical and retail ecosystem

- In May 2025, Optos announced that global sales of its MonacoPro integrated ultra-widefield and OCT imaging solutions surpassed a major adoption milestone, reflecting strong clinical demand for combined imaging platforms that streamline workflow and improve diagnostic insights. Concurrently, Optos launched a comprehensive U.S. OCT/ultra-widefield imaging reference database to support AI-driven analysis and improved diagnostic precision in clinical settings

- In March 2025, Alcon announced its acquisition of Cylite, a developer of hyperparallel “whole-eye” OCT imaging intellectual property, signaling a strategic commitment to advancing full-eye OCT imaging capabilities for improved surgical planning and ophthalmic diagnostic workflows. This acquisition positions Alcon to integrate cutting-edge OCT IP into broader surgical and diagnostic portfolios

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.