Global Ocular Pain Market

Market Size in USD Billion

CAGR :

%

USD

1.20 Billion

USD

2.18 Billion

2025

2033

USD

1.20 Billion

USD

2.18 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.20 Billion | |

| USD 2.18 Billion | |

| % | |

|

Ocular Pain Market Overview

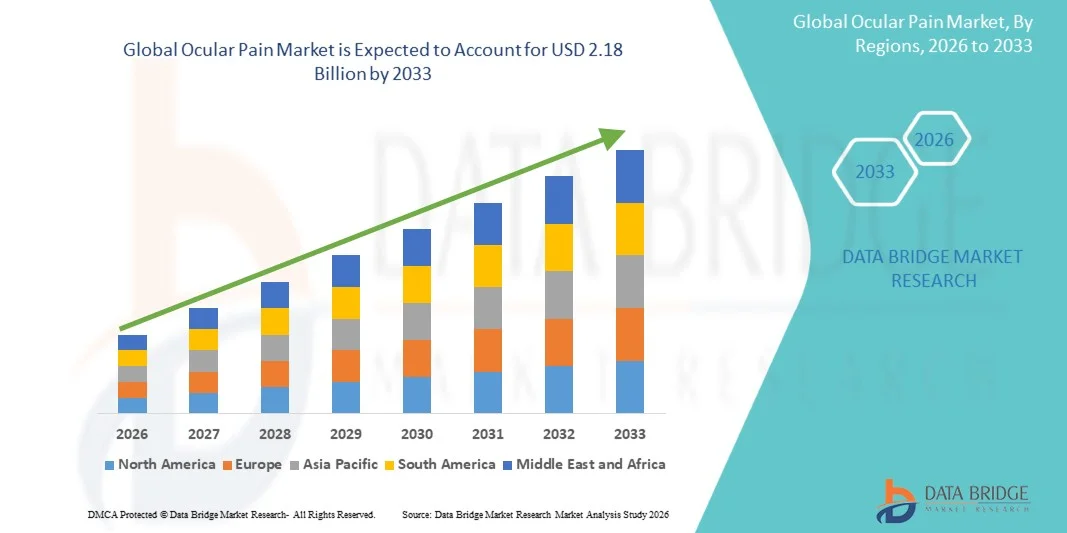

The Ocular Pain Market was valued at USD 1.20 billion in 2025 and is projected to reach USD 2.18 billion by 2033, growing at a CAGR of 7.80% from 2026 to 2033. The Ocular Pain Market is experiencing steady growth driven by the rising prevalence of ocular surface disorders, increasing cases of dry eye disease, infections, glaucoma, and post-surgical eye complications, all of which significantly contribute to eye pain and discomfort. Growing screen time exposure due to digital device usage, aging populations, and increasing environmental pollution are further intensifying the incidence of ocular irritation and chronic eye pain globally.

The market is also witnessing strong expansion due to advancements in ophthalmic diagnostics and the availability of more effective pain management therapies, including lubricating eye drops, anti-inflammatory medications, anesthetic agents, and combination ophthalmic formulations. Increasing awareness regarding early diagnosis and treatment of eye disorders is encouraging patients to seek timely medical intervention, thereby supporting market growth.

Key Market Trends & Insights

- North America dominated the Ocular Pain Market with the largest revenue share of 33% in 2025, supported by advanced ophthalmic care infrastructure, high prevalence of ocular surface disorders, strong adoption of prescription-based ocular therapies, and well-established hospital and specialty clinic networks.

- The topical segment dominated the market with 78.3% share in 2025, due to widespread use of eye drops as first-line therapy for ocular pain management.

- Asia-Pacific is the fastest-growing region in the Ocular Pain Market, projected to expand at a CAGR of 7.5% from 2026 to 2033, fueled by rising prevalence of ocular disorders, increasing healthcare expenditure, rapid expansion of ophthalmology infrastructure, and growing awareness of eye health in countries such as China, India, Japan, and South Korea.

- Ocular Pain with Eye Diseases segment led the market with 58% share in 2025, driven by high incidence of conditions such as conjunctivitis, corneal abrasions, blepharitis, and glaucoma-associated ocular discomfort.

- Hospitals segment dominated the End User category with nearly 38% share in 2025, due to strong patient inflow for acute ocular conditions, surgical care, and emergency ophthalmic treatments.

Market Size & Forecast

- Global Market Value (2025): USD 1.20 Billion

- Expected Market Value (2033): USD 2.18 Billion

- Forecast CAGR (2026–2033): 7.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Ocular Pain Market Segmentation

|

Attributes |

Ocular Pain Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Bausch + Lomb (U.S.) |

|

Market Opportunities |

· Expansion of Novel Non-Opioid and Targeted Pain Therapies · Growth in Advanced Drug Delivery Systems and Sustained-Release Technologies · Rising Demand for Digital Eye Care and Integrated Ophthalmology Solutions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Ocular Pain Market Trends

Trend: Rising Burden of Ocular Surface Disorders & Digital Eye Strain

The Ocular Pain Market is witnessing strong growth due to the rising prevalence of dry eye disease, conjunctivitis, blepharitis, and corneal abrasions, which are among the most common causes of ocular discomfort. According to the TFOS DEWS II report (2021 clinical consensus update), dry eye disease affects 5% to 50% of the global population depending on geography and diagnostic criteria, making it a major contributor to chronic ocular pain. Increasing screen exposure and digital device usage have significantly increased digital eye strain (computer vision syndrome), particularly among adults and working professionals. Ophthalmology studies indicate that over 60% of screen users report symptoms such as eye irritation, burning sensation, and pain, directly fueling demand for lubricating eye drops and anti-inflammatory therapies.

Ocular Pain Market Dynamics

Key Market Driver: Rising Prevalence of Ocular Diseases and Aging Population

The global increase in age-related ocular disorders such as glaucoma, cataract, and dry eye syndrome is a major driver of ocular pain treatment demand. The WHO estimates that over 2.2 billion people globally suffer from vision impairment or blindness, with a significant portion linked to preventable or treatable ocular conditions. Aging populations in regions such as North America, Europe, and Japan further increase the burden of chronic ocular discomfort requiring long-term therapy. In addition, increasing prevalence of allergic conjunctivitis and infectious eye diseases is expanding the use of topical anti-inflammatory and antihistamine eye drops.

Key Restraint/Challenge: Side Effects and Limited Long-Term Treatment Options

A significant restraint in the Ocular Pain Market is the long-term safety limitations associated with commonly used therapeutic classes, particularly corticosteroids and certain topical anti-inflammatory agents. Prolonged use of corticosteroid eye drops has been clinically associated with elevated intraocular pressure, risk of secondary glaucoma, and cataract formation, restricting their use in chronic ocular pain management and requiring careful ophthalmic monitoring. In addition, the widespread use of preserved ophthalmic formulations, especially those containing benzalkonium chloride (BAK), contributes to ocular surface toxicity, tear film instability, and epithelial damage, particularly in patients with chronic dry eye disease. This has led to reduced treatment adherence and increased discontinuation rates. Clinical studies in dry eye disease management indicate that 30–40% of patients discontinue topical therapy within 6 months, primarily due to irritation, limited symptomatic relief, and long-term tolerability concerns. This adherence challenge continues to limit sustained market expansion despite rising disease prevalence globally.

Key Market Opportunity: Growth of Preservative-Free and Regenerative Ophthalmic Therapies

The Ocular Pain Market is witnessing strong growth opportunities driven by the shift toward preservative-free formulations, targeted biologics, and regenerative ophthalmic therapies designed to improve safety, tolerability, and long-term outcomes. For instance, Novaliq’s CyclASol (cyclosporine A ophthalmic solution) represents a next-generation preservative-free therapy for dry eye disease, offering improved ocular surface compatibility compared to conventional emulsion-based formulations. Similarly, AbbVie’s Restasis (cyclosporine ophthalmic emulsion) continues to demonstrate strong global adoption, reinforcing the demand for immunomodulatory treatments in chronic ocular surface inflammation. In parallel, companies such as Regenxbio are advancing gene therapy platforms targeting ocular surface regeneration and inflammatory eye disorders, while ongoing research into stem cell–based corneal repair and neuro-regenerative ophthalmic treatments is opening new pathways for refractory ocular pain conditions. Furthermore, the post-2021 expansion of tele-ophthalmology services and online pharmacy distribution channels has significantly improved treatment accessibility, particularly in emerging markets. The increased adoption of digital consultation platforms in regions such as Asia-Pacific and Latin America is helping bridge the gap in ophthalmic care delivery, supporting earlier diagnosis and wider penetration of prescription eye pain therapies.

Ocular Pain Market Scope

The Ocular Pain market is segmented on the basis of disease type, type, application, route of administration, drug type, population type, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the Ocular Pain Market is segmented into ocular pain with eye diseases and ocular pain without primary eye diseases. The ocular pain with eye diseases segment dominated the market with 62.4% share in 2025, due to the high global prevalence of underlying ophthalmic conditions such as conjunctivitis, glaucoma, keratitis, dry eye disease, and corneal abrasions. Increasing incidence of diabetes-related eye complications and age-related ocular disorders is significantly driving demand. Rising number of ophthalmology consultations across hospitals and specialty clinics is supporting segment dominance. Strong adoption of anti-inflammatory, antibiotic, and lubricating eye therapies is further boosting market share. Growing geriatric population worldwide is a major contributor. Increasing surgical ophthalmic procedures is generating post-operative pain cases requiring treatment. Expanding access to ophthalmic care in emerging economies is strengthening growth. Awareness about early diagnosis of eye diseases is rising globally. Continuous pharmaceutical innovation in ocular therapeutics is supporting expansion.

The ocular pain without primary eye diseases segment is expected to register the fastest CAGR of 8.9% from 2026 to 2033, driven by rising cases of migraine-associated eye pain, sinusitis-linked ocular discomfort, digital eye strain, and environmental irritation. Increasing screen exposure from smartphones, computers, and digital devices is a key factor. Urban pollution and allergens are contributing significantly to non-disease ocular pain. Growing awareness of functional and neurological causes of eye pain is improving diagnosis rates. Expanding OTC eye care product availability is supporting self-medication trends. Tele-ophthalmology adoption is improving access to care in rural and semi-urban regions. Rising stress levels and lifestyle disorders are increasing incidence. Growth in working-age population is further accelerating demand. AI-based symptom checker tools are improving early detection.

- By Type

On the basis of type, the market is segmented into diagnosis and treatment. The treatment segment dominated the market with 71.8% share in 2025, driven by widespread use of analgesic eye drops, NSAIDs, corticosteroids, antihistamines, and lubricating formulations for managing ocular pain symptoms. High prevalence of chronic eye diseases requiring long-term treatment supports dominance. Strong prescription patterns across hospitals and specialty clinics further reinforce demand. Availability of branded and generic ophthalmic drugs improves accessibility. Increasing post-surgical inflammation cases are contributing to usage. Physicians continue to prefer medication-first approaches for ocular pain management. Strong pharmaceutical pipelines are introducing advanced formulations. Rising outpatient treatment volumes support market expansion. Insurance coverage for ophthalmic drugs strengthens adoption.

The diagnosis segment is expected to grow at the fastest CAGR of 9.4% from 2026 to 2033, driven by increasing adoption of advanced ophthalmic diagnostic tools such as slit-lamp imaging, optical coherence tomography (OCT), and AI-based eye screening systems. Rising awareness of early disease detection is boosting diagnostic uptake. Expanding routine eye screening programs is increasing patient inflow. Growth in tele-ophthalmology platforms is improving accessibility. Increasing geriatric population is driving preventive screening demand. Integration of AI-based diagnostic tools is improving accuracy. Rising healthcare infrastructure in emerging economies supports growth. Early detection of glaucoma and corneal diseases is expanding testing volumes. Digital health platforms are enabling faster diagnosis.

- By Application

On the basis of application, the market includes conjunctivitis, corneal abrasion, blepharitis, sty, iritis, sinusitis, migraines, glaucoma, and others. The conjunctivitis segment dominated the market with 24.6% share in 2025, due to its high global incidence and frequent recurrence caused by bacterial, viral, and allergic infections. Seasonal outbreaks and poor hygiene practices in developing regions significantly contribute to cases. High pediatric and adult prevalence supports dominance. Strong OTC availability of antibiotic and antihistamine eye drops boosts treatment rates. Increasing environmental pollution and allergen exposure are major drivers. Hospitals and retail pharmacies report high patient volumes. Public awareness campaigns are improving diagnosis rates. Easy availability of topical medications strengthens adoption. Rising contact lens usage is also contributing.

The migraine-associated ocular pain segment is expected to grow at the fastest CAGR of 10.2% from 2026 to 2033, driven by increasing neurological disorders and lifestyle-related stress conditions. High digital screen exposure is a major contributing factor. Rising cases of photophobia and visual aura-related pain are boosting demand. Growing awareness of neuro-ophthalmic disorders is improving diagnosis. Expanding use of triptans and combination therapies supports treatment adoption. Tele-neurology and telemedicine platforms are increasing accessibility. Urban stress and sleep disorders are major triggers. Increasing female population prevalence supports growth. Rising outpatient neurology visits are contributing to demand.

- By Route of Administration

On the basis of route of administration, the market is segmented into topical, periocular, intraocular, and oral. The topical segment dominated the market with 78.3% share in 2025, due to widespread use of eye drops as first-line therapy for ocular pain management. High patient compliance and ease of administration support dominance. Strong availability of lubricants, NSAIDs, and antibiotic drops drives adoption. Rapid symptom relief makes topical therapy preferred globally. Hospitals and pharmacies rely heavily on topical formulations. Increasing dry eye and conjunctivitis cases support usage. OTC availability enhances accessibility. Lower systemic side effects favor adoption. Pharmaceutical companies focus heavily on topical drug innovation.

The intraocular segment is expected to grow at the fastest CAGR of 9.1% from 2026 to 2033, driven by increasing use in severe ocular diseases and post-surgical pain management. Advancements in sustained-release implants are supporting growth. Rising glaucoma and retinal disease treatments are increasing demand. Expanding ophthalmic surgical procedures globally is boosting usage. Improved drug delivery technologies are enhancing effectiveness. Hospital-based procedures are increasing adoption rates. Clinical research in ocular therapeutics is expanding. Aging population is increasing surgical needs. Precision-targeted drug delivery systems are improving outcomes.

- By Drug Type

On the basis of drug type, the market is segmented into prescription and over-the-counter (OTC). The prescription segment dominated the market with 66.9% share in 2025, due to strong reliance on ophthalmologist-prescribed medications for moderate to severe ocular pain. Widespread use of antibiotics, corticosteroids, and anti-inflammatory drugs supports dominance. Hospital and specialty clinic prescriptions drive demand. Insurance reimbursement systems favor prescription drugs. Strong clinical protocols reinforce usage. Increasing chronic eye disease burden supports long-term medication use. Pharmaceutical innovation is expanding prescription drug pipelines. Physician preference for controlled therapy enhances adoption. Post-operative care significantly contributes to demand.

The OTC segment is expected to grow at the fastest CAGR of 9.7% from 2026 to 2033, driven by rising self-medication trends and increasing availability of lubricating and soothing eye drops. Expanding retail and online pharmacy networks are improving access. Growing awareness of minor eye irritation management supports adoption. Increasing screen-related eye strain is a major driver. Digital pharmacy platforms are accelerating sales. Consumer preference for convenience and quick relief supports growth. Regulatory approvals for OTC ophthalmic drugs are expanding. E-commerce penetration is improving availability globally. Rural access to eye care products is increasing.

- By Population Type

On the basis of population type, the market is segmented into adults and geriatric. The adult segment dominated the market with 58.7% share in 2025, driven by high exposure to digital devices, occupational eye strain, and environmental pollution. Increasing prevalence of conjunctivitis and migraine-related eye pain supports demand. Urban lifestyle stress is a major contributor. High outpatient treatment rates reinforce dominance. Strong awareness of eye health is increasing consultations. OTC medication use is widespread among adults. Preventive eye care adoption is rising globally. Workplace-related ocular fatigue is increasing cases.

The geriatric segment is expected to grow at the fastest CAGR of 9.2% from 2026 to 2033, driven by age-related ocular disorders such as glaucoma, cataracts, and dry eye syndrome. Increasing global aging population is a key driver. Higher susceptibility to chronic eye pain supports demand. Expanding ophthalmic healthcare infrastructure for elderly care boosts growth. Rising surgical procedures in older adults contribute significantly. Improved healthcare access in developing regions supports adoption. Increasing chronic disease comorbidities further enhance demand.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, home healthcare settings, ophthalmology centers, ambulatory surgical centers, and others. The hospitals segment dominated the market with 42.8% share in 2025, due to advanced diagnostic infrastructure and availability of specialized ophthalmologists. High patient inflow for acute and chronic ocular conditions supports dominance. Strong emergency eye care services drive demand. Increasing surgical procedures boost hospital utilization. Insurance reimbursement systems favor hospital-based care. Integrated treatment pathways strengthen adoption. Government healthcare support enhances capacity. Post-operative care requirements increase hospital dependency.

The home healthcare segment is expected to grow at the fastest CAGR of 10.5% from 2026 to 2033, driven by increasing adoption of tele-ophthalmology and remote monitoring solutions. Rising preference for at-home treatment supports demand. Growing geriatric population is a key factor. Expansion of digital health platforms is boosting accessibility. OTC medication use supports home-based care. Post-pandemic shift toward remote healthcare continues. AI-based eye care apps are improving monitoring. Smartphone penetration is accelerating adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with 46.1% share in 2025, due to high prescription volumes and regulated drug dispensing systems. Strong hospital procurement networks support dominance. Physician-led prescribing ensures compliance. Emergency and post-surgical care drives usage. Insurance-linked distribution strengthens hospital pharmacy role. Bulk procurement systems support stability. Strict regulatory oversight ensures controlled dispensing.

The online pharmacy segment is expected to grow at the fastest CAGR of 11.3% from 2026 to 2033, driven by increasing digital health adoption and telemedicine integration. Rising demand for convenience and privacy supports growth. Smartphone penetration is expanding access. E-prescriptions are boosting online sales. Rural healthcare accessibility is improving significantly. Subscription-based delivery models are gaining traction. Digital pharmacy startups are expanding rapidly. AI-enabled prescription systems improve efficiency.

Ocular Pain Market Regional Analysis

North America dominated the Ocular Pain Market and accounted for the largest revenue share of 33% in 2025, supported by a highly advanced ophthalmic care infrastructure, strong presence of leading pharmaceutical companies, and high prevalence of ocular surface disorders such as dry eye disease, conjunctivitis, blepharitis, and glaucoma-related pain. The region benefits from widespread adoption of prescription-based ocular therapies, including NSAID eye drops, corticosteroids, and immunomodulatory agents. In addition, the presence of well-established hospital networks, specialty ophthalmology clinics, and ambulatory surgical centers supports high diagnosis and treatment rates. Strong regulatory oversight by the U.S. FDA, along with continuous product approvals and innovation in preservative-free formulations, further strengthens market growth. Rising screen exposure, aging population, and increasing cases of digital eye strain continue to drive sustained demand for ocular pain management therapies.

U.S. Ocular Pain Market Insight

The U.S. Ocular Pain market is witnessing strong growth due to the rising burden of dry eye disease and allergic conjunctivitis, along with increasing utilization of prescription ophthalmic drugs. According to clinical estimates, dry eye disease affects tens of millions of adults in the U.S., making it one of the most common causes of ocular discomfort. Strong adoption of advanced therapies such as cyclosporine-based drugs (Restasis), lifitegrast (Xiidra), and newer anti-inflammatory formulations is driving market expansion. In addition, the country’s well-developed healthcare system, high ophthalmology consultation rates, and strong insurance coverage support treatment accessibility. Increasing digital device usage and growing demand for minimally invasive ocular therapies further contribute to market growth.

Europe Ocular Pain Market Insight

Europe remains a significant contributor to the Ocular Pain Market, supported by strong healthcare systems, high awareness of eye health, and increasing prevalence of age-related ocular disorders. Countries such as Germany, France, and the U.K. show high adoption of prescription eye drops and advanced ophthalmic treatments. The region benefits from strong regulatory frameworks under the European Medicines Agency (EMA), ensuring rapid availability of innovative therapies. Rising cases of dry eye disease linked to aging populations and environmental pollution are further driving demand for long-term ocular pain management solutions.

U.K. Ocular Pain Market Insight

The U.K. Ocular Pain market is growing steadily due to increasing incidence of dry eye syndrome and allergic eye conditions, along with strong adoption of prescription and over-the-counter ophthalmic solutions. The presence of advanced healthcare infrastructure under the NHS system ensures broad patient access to ophthalmic care. Growing awareness of eye health, combined with increasing use of lubricating eye drops and anti-inflammatory therapies, is supporting market expansion. In addition, ongoing research collaborations between academic institutions and pharmaceutical companies are strengthening innovation in ocular pain treatment approaches.

Germany Ocular Pain Market Insight

Germany represents one of the largest ophthalmology markets in Europe, driven by a strong healthcare system and high prevalence of chronic eye disorders. The country shows significant adoption of advanced prescription therapies and hospital-based ophthalmic treatments. Increasing cases of age-related macular degeneration, dry eye disease, and post-surgical ocular pain are driving demand. Germany also benefits from strong pharmaceutical R&D activity, with companies focusing on preservative-free formulations and novel anti-inflammatory drugs, supporting long-term market growth.

Asia-Pacific Ocular Pain Market Insight

The Asia-Pacific region is the fastest-growing market, projected to expand at a CAGR of 7.5% from 2026 to 2033, driven by rising prevalence of ocular disorders, increasing healthcare expenditure, and rapid expansion of ophthalmology infrastructure across emerging economies. Growing cases of dry eye disease, conjunctivitis, and digital eye strain are significantly contributing to market demand. Expanding access to ophthalmic care in countries such as China, India, Japan, and South Korea, along with rising awareness of eye health, is accelerating treatment adoption. Additionally, increasing availability of affordable OTC eye drops and prescription therapies is improving market penetration.

Japan Ocular Pain Market Insight

Japan’s ocular pain market is growing steadily due to its rapidly aging population and high prevalence of dry eye disease and ocular surface inflammation. The country has one of the highest rates of ophthalmology consultations globally, supporting strong adoption of both prescription and OTC eye care products. Increasing use of advanced therapies such as immunomodulatory eye drops and preservative-free formulations is driving market expansion. Japan’s strong pharmaceutical innovation ecosystem and focus on precision medicine further support development of next-generation ocular pain treatments.

China Ocular Pain Market Insight

China is emerging as one of the fastest-growing markets for ocular pain treatment due to rapid urbanization, increasing screen exposure, and rising awareness of eye health. The growing prevalence of dry eye disease and allergic conjunctivitis is significantly boosting demand for ocular pain therapies. Expansion of healthcare infrastructure, increasing availability of ophthalmic medications, and rising adoption of advanced prescription eye drops and OTC lubricants are supporting market growth. Government initiatives to improve healthcare access and increasing investment in ophthalmology services are further strengthening China’s position in the global market.

Ocular Pain Market Share

The Ocular Pain industry is primarily led by well-established companies, including:

- Bausch + Lomb (U.S.)

- Alcon Inc. (Switzerland)

- Johnson & Johnson Vision Care, Inc. (U.S.)

- Novartis AG (Switzerland)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Allergan (AbbVie Inc.) (U.S.)

- Bayer AG (Germany)

- Pfizer Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- AstraZeneca plc (U.K.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Ocuphire Pharma, Inc. (U.S.)

- Kala Pharmaceuticals, Inc. (U.S.)

- Graybug Vision, Inc. (U.S.)

- Ocular Therapeutix, Inc. (U.S.)

- Aerie Pharmaceuticals (Alcon) (U.S.)

- Nicox S.A. (France)

- Thea Pharma (France)

- Sentiss Pharma Pvt. Ltd. (India)

- Entod Pharmaceuticals (India)

- Cipla Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Abbott Laboratories (U.S.)

- Harrow Health, Inc. (U.S.)

- SIFI S.p.A. (Italy)

- Viatris Inc. (U.S.)

- Lupin Limited (India)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- GlaxoSmithKline plc (U.K.)

- Nicox Ophthalmics (France)

- Vistagen Therapeutics, Inc. (U.S.)

Latest Developments in Ocular Pain Market

- In October 2021, Ocular Therapeutix announced FDA approval of DEXTENZA (dexamethasone ophthalmic insert) for the treatment of ocular itching associated with allergic conjunctivitis, expanding its earlier indication for post-operative ocular pain and inflammation. The intracanalicular insert provides sustained drug release for up to 30 days and represents a shift toward long-acting, office-administered therapies that improve compliance and reduce treatment burden in ocular pain management

- In February 2022, the U.S. FDA approved the first generic version of Restasis (cyclosporine ophthalmic emulsion) for patients with keratoconjunctivitis sicca (dry eye disease), a condition strongly associated with ocular discomfort and chronic eye pain. The approval expanded patient access to lower-cost anti-inflammatory ophthalmic therapy, improving long-term management of ocular surface pain and inflammation

- In September 2022, Santen Pharmaceutical and UBE Corporation received FDA approval for OMLONTI (omidenepag isopropyl ophthalmic solution) for reducing elevated intraocular pressure in glaucoma and ocular hypertension patients. Although primarily indicated for IOP reduction, the therapy plays a key role in preventing pain-associated complications of glaucoma, a major contributor to chronic ocular discomfort worldwide

- In September 2023, Ocuphire Pharma and Viatris received FDA approval for RYZUMVI (phentolamine ophthalmic solution 0.75%) for pharmacologically induced mydriasis. The therapy improves recovery of pupil function following diagnostic eye procedures, reducing post-procedure discomfort and transient ocular pain symptoms in clinical ophthalmology settings

- In March 2024, Formosa Pharmaceuticals and Eyenovia received FDA approval for APP13007 (clobetasol propionate ophthalmic suspension 0.05%) for the treatment of post-operative ocular pain and inflammation. Clinical trials demonstrated significant reduction in post-cataract surgery pain and inflammation, marking one of the most important recent launches in steroid-based ocular pain therapy in over 15 years

- In February 2024, OKYO Pharma received FDA clearance of its Investigational New Drug (IND) application for OK-101 for neuropathic corneal pain (NCP), enabling clinical trials in one of the most severe and underserved ocular pain conditions. This milestone highlights increasing innovation targeting nerve-related ocular pain syndromes with no approved curative therapies

- In March 2024, the FDA approval of APP13007 was further highlighted as a breakthrough for postoperative ocular pain management, demonstrating statistically significant pain relief and inflammation reduction in Phase III trials. The launch is expected to expand treatment options for cataract and refractive surgery patients experiencing acute ocular pain

- In May 2025, Alcon received FDA approval for TRYPTYR (dry eye disease treatment), a novel eye drop that stimulates natural tear production and rapidly improves ocular surface discomfort. The therapy represents a new class of neurostimulation-based ocular surface pain management, addressing a large unmet need in dry eye–related ocular pain affecting tens of millions of patients globally

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.