Global Non Hydroponic Smart Greenhouse Market

Market Size in USD Billion

USD

2.21 Billion

USD

4.45 Billion

2025

2033

USD

2.21 Billion

USD

4.45 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.21 Billion | |

| USD 4.45 Billion | |

| % | |

|

Non-Hydroponic Smart Greenhouse Market Size

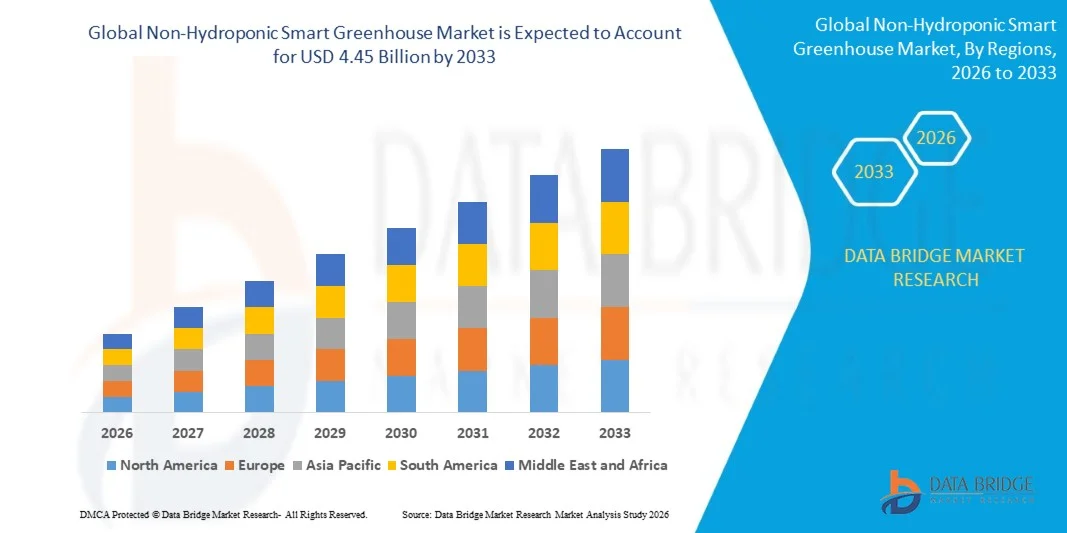

- The global non-hydroponic smart greenhouse market size was valued at USD 2.21 billion in 2025 and is expected to reach USD 4.45 billion by 2033, at a CAGR of 9.10% during the forecast period

- The market growth is largely fuelled by the rising demand for precision agriculture technologies, increasing adoption of climate-controlled greenhouse systems, and growing need for higher crop productivity and quality

- Increasing investments in smart farming solutions such as automated irrigation, climate monitoring, and sensor-based crop management are accelerating the adoption of non-hydroponic smart greenhouse systems

Non-Hydroponic Smart Greenhouse Market Analysis

- The market is experiencing steady growth due to the increasing integration of advanced technologies such as IoT-enabled sensors, artificial intelligence-based monitoring systems, and automated environmental control solutions in greenhouse farming

- Rising global demand for fresh fruits, vegetables, and high-value crops, along with the need to improve agricultural productivity in limited arable land areas, is encouraging growers to adopt non-hydroponic smart greenhouse solutions for efficient soil-based cultivation systems

- North America dominated the non-hydroponic smart greenhouse market with the largest revenue share in 2025, driven by increasing adoption of advanced agricultural technologies and growing investments in controlled environment agriculture

- Asia-Pacific region is expected to witness the highest growth rate in the global non-hydroponic smart greenhouse market, driven by rapid population growth, rising food demand, expanding greenhouse cultivation, and increasing government and private investments in advanced agricultural technologies

- The sensor and control system segment held the largest market revenue share in 2025 driven by the growing adoption of automated monitoring technologies that regulate temperature, humidity, soil moisture, and other environmental conditions within greenhouse facilities. These systems enable real-time data collection and automated adjustments, helping growers optimize crop growth conditions and improve operational efficiency

Report Scope and Non-Hydroponic Smart Greenhouse Market Segmentation

|

Attributes |

Non-Hydroponic Smart Greenhouse Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Certhon (Netherlands) |

|

Market Opportunities |

• Expansion Of Smart Farming Technologies In Emerging Economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Non-Hydroponic Smart Greenhouse Market Trends

“Increasing Adoption of Precision Agriculture and Automation Technologies”

• The growing adoption of precision agriculture technologies is significantly shaping the non-hydroponic smart greenhouse market, as growers increasingly integrate automated monitoring, climate control, and sensor-based management systems to improve productivity and resource efficiency. Smart greenhouse solutions are gaining traction due to their ability to regulate temperature, humidity, and irrigation in soil-based cultivation systems, helping farmers enhance crop yield and quality while reducing operational inefficiencies

• Increasing pressure on agricultural production due to rising global population and limited arable land has accelerated the demand for controlled-environment farming solutions. Non-hydroponic smart greenhouses enable efficient soil-based crop cultivation while integrating advanced digital tools such as IoT sensors, artificial intelligence, and remote monitoring platforms. These technologies support better decision-making and allow growers to maintain consistent crop performance under varying climatic conditions

• Technological advancements in smart farming equipment are influencing investment in greenhouse automation and digital agriculture platforms. Manufacturers are focusing on integrating climate control systems, automated irrigation, lighting management, and data-driven analytics into greenhouse infrastructure to improve operational efficiency. These innovations help optimize water usage, energy consumption, and nutrient management, strengthening sustainability and cost-effectiveness in greenhouse operations

• For instance, in 2024, companies such as Netafim in Israel and Richel Group in France expanded smart greenhouse solutions incorporating automated irrigation, sensor-driven climate control, and digital monitoring platforms for soil-based greenhouse cultivation. These systems were introduced to enhance crop productivity and resource efficiency across commercial farming operations in Europe and Asia-Pacific

• While technological adoption continues to increase, sustained market expansion depends on improving affordability, scalability, and farmer awareness of advanced greenhouse management systems. Manufacturers are also focusing on developing integrated platforms that combine automation, climate monitoring, and crop analytics to support efficient soil-based greenhouse cultivation and long-term agricultural sustainability

Non-Hydroponic Smart Greenhouse Market Dynamics

Driver

“Growing Demand for Controlled Environment Agriculture and Higher Crop Productivity”

• Rising global demand for high-quality fruits, vegetables, and specialty crops is a major driver for the non-hydroponic smart greenhouse market. Farmers and commercial growers are increasingly adopting controlled environment agriculture solutions to improve productivity, reduce crop losses, and maintain consistent product quality throughout the year. Soil-based smart greenhouse systems provide enhanced crop management while maintaining traditional cultivation methods preferred in many regions

• Expanding investments in greenhouse infrastructure across developed and emerging economies are supporting market growth. Governments and private organizations are promoting modern farming technologies to strengthen food security, improve agricultural efficiency, and reduce dependency on seasonal farming conditions. Non-hydroponic smart greenhouses allow growers to maintain optimal soil conditions while benefiting from automated climate and irrigation systems

• Agricultural technology providers are actively promoting integrated greenhouse solutions through product innovation, partnerships, and digital platforms. These efforts enable farmers to optimize crop growth conditions using sensor-based monitoring, automated irrigation control, and environmental management systems. Such innovations support higher yields, reduced resource consumption, and improved farm profitability

• For instance, in 2023, companies such as Priva in the Netherlands and Argus Control Systems in Canada introduced advanced climate management and automation technologies designed for soil-based greenhouse farming. These systems enabled growers to monitor environmental conditions, optimize irrigation cycles, and enhance crop productivity in commercial greenhouse operations

• Although the growing need for high-efficiency agriculture supports market growth, wider adoption depends on cost-effective system deployment, improved infrastructure, and greater technical awareness among farmers. Investments in training programs, technology accessibility, and digital agriculture platforms will be essential to support the long-term expansion of the non-hydroponic smart greenhouse market

Restraint/Challenge

“High Initial Investment and Technical Complexity of Smart Greenhouse Systems”

• The relatively high initial investment required for installing smart greenhouse infrastructure remains a key challenge for market growth. Advanced climate control systems, automated irrigation equipment, sensor networks, and digital monitoring platforms involve substantial upfront costs, making adoption difficult for small and medium-scale farmers. Maintenance and system integration costs can also increase operational expenditure

• Limited technical knowledge and lack of skilled workforce in certain agricultural regions further restrict market adoption. Operating automated greenhouse systems requires familiarity with digital tools, data analysis platforms, and climate control technologies. Farmers in developing markets may face difficulties in implementing and maintaining advanced greenhouse management systems due to insufficient technical training and support infrastructure

• Infrastructure and connectivity challenges also impact the deployment of smart greenhouse technologies. Reliable electricity supply, internet connectivity, and access to digital platforms are essential for operating automated greenhouse systems. In rural or remote areas, limitations in technological infrastructure can delay implementation and reduce operational efficiency

• For instance, in 2024, greenhouse technology providers supplying equipment to growers in regions such as Southeast Asia and Latin America reported slower adoption rates due to high equipment costs and limited technical expertise among farmers. Some growers also faced challenges integrating automated systems with existing greenhouse infrastructure, affecting operational efficiency and return on investment

• Overcoming these challenges will require cost optimization, improved financing options, and expanded technical training for farmers. Collaboration between greenhouse technology providers, governments, and agricultural institutions can help improve accessibility, strengthen digital infrastructure, and accelerate adoption of advanced soil-based greenhouse farming solutions worldwide

Non-Hydroponic Smart Greenhouse Market Scope

The market is segmented on the basis of component, material, offering, application, and end user.

• By Component

On the basis of component, the non-hydroponic smart greenhouse market is segmented into HVAC Systems, LED Grow Lights, Irrigation System, Valves and Pumps, Sensor and Control System, and Others. The sensor and control system segment held the largest market revenue share in 2025 driven by the growing adoption of automated monitoring technologies that regulate temperature, humidity, soil moisture, and other environmental conditions within greenhouse facilities. These systems enable real-time data collection and automated adjustments, helping growers optimize crop growth conditions and improve operational efficiency.

The LED grow lights segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for energy-efficient lighting solutions that support plant growth and productivity in controlled greenhouse environments. LED grow lights provide adjustable light spectra and lower power consumption, making them suitable for enhancing photosynthesis and supporting year-round crop production.

• By Material

On the basis of material, the non-hydroponic smart greenhouse market is segmented into Polyethylene, Polycarbonate, and Others. The polyethylene segment held the largest market revenue share in 2025 driven by its cost-effectiveness, flexibility, and strong light transmission properties that support efficient crop cultivation. Polyethylene greenhouse coverings are widely used due to their affordability and ease of installation, making them suitable for large-scale greenhouse farming.

The polycarbonate segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its superior durability, thermal insulation, and impact resistance. Polycarbonate materials help maintain stable internal greenhouse temperatures while providing strong structural protection, making them increasingly preferred for advanced smart greenhouse installations.

• By Offering

On the basis of offering, the non-hydroponic smart greenhouse market is segmented into Hardware, Software, and Services. The hardware segment held the largest market revenue share in 2025 driven by the widespread deployment of greenhouse infrastructure components such as sensors, climate control systems, irrigation equipment, and lighting systems. These hardware solutions form the foundation of smart greenhouse operations and support automated environmental management.

The software segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of digital agriculture platforms that enable remote monitoring, predictive analytics, and automated control of greenhouse conditions. Software platforms help growers analyze environmental data, optimize resource usage, and improve decision-making in greenhouse management.

• By Applications

On the basis of applications, the non-hydroponic smart greenhouse market is segmented into Vegetables, Flowers and Ornamentals, Fruit Plants, Nursery Crops, and Others. The vegetables segment held the largest market revenue share in 2025 driven by the high global demand for fresh and high-quality vegetables such as tomatoes, cucumbers, and leafy greens cultivated in greenhouse environments. Smart greenhouse technologies help growers maintain optimal conditions for vegetable production while improving yield and crop consistency.

The fruit plants segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing cultivation of high-value fruits in controlled greenhouse environments. Smart greenhouse systems help regulate climate and irrigation conditions required for fruit plant growth, improving productivity and supporting year-round production.

• By End User

On the basis of end user, the non-hydroponic smart greenhouse market is segmented into Commercial Growers, Research and Educational Institutes, Retail Gardens, and Others. The commercial growers segment held the largest market revenue share in 2025 driven by the increasing adoption of smart greenhouse technologies to enhance crop productivity, reduce resource consumption, and support large-scale agricultural operations. Commercial growers benefit from automated systems that improve efficiency and enable consistent crop production.

The research and educational institutes segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing investments in agricultural research, greenhouse experimentation, and training programs related to advanced farming technologies. These institutes use smart greenhouse systems to study plant growth patterns, climate control methods, and innovative cultivation techniques for future agricultural development.

Non-Hydroponic Smart Greenhouse Market Regional Analysis

• North America dominated the non-hydroponic smart greenhouse market with the largest revenue share in 2025, driven by increasing adoption of advanced agricultural technologies and growing investments in controlled environment agriculture

• Growers in the region increasingly prioritize efficient crop production, climate-controlled cultivation, and automated greenhouse management systems to improve yield and resource efficiency

• This widespread adoption is further supported by strong technological infrastructure, increasing demand for locally produced fresh food, and the presence of major greenhouse technology providers, establishing smart greenhouse systems as a preferred solution for commercial farming operations

U.S. Non-Hydroponic Smart Greenhouse Market Insight

The U.S. non-hydroponic smart greenhouse market captured the largest revenue share in 2025 within North America, fueled by the rapid adoption of precision agriculture technologies and the increasing demand for high-quality fruits and vegetables. Commercial growers are increasingly implementing automated climate control systems, sensor-based monitoring platforms, and advanced irrigation technologies to improve crop productivity and resource management. The presence of large-scale greenhouse farms, combined with strong investments in agricultural innovation and digital farming solutions, further supports the expansion of the non-hydroponic smart greenhouse market in the country.

Europe Non-Hydroponic Smart Greenhouse Market Insight

The Europe non-hydroponic smart greenhouse market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by strong government support for sustainable agriculture and increasing adoption of modern greenhouse technologies. Rising demand for organic and locally grown produce is encouraging farmers to adopt controlled environment farming systems. The region is also experiencing growing investments in smart farming infrastructure, with greenhouse technologies being integrated into both commercial farming operations and agricultural research facilities.

U.K. Non-Hydroponic Smart Greenhouse Market Insight

The U.K. non-hydroponic smart greenhouse market is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing demand for sustainable agricultural practices and year-round crop production. Farmers and greenhouse operators are increasingly adopting automated irrigation systems, environmental monitoring technologies, and digital farm management tools to improve productivity. The country’s focus on food security, combined with strong adoption of agricultural technology, continues to encourage the development of modern greenhouse farming solutions.

Germany Non-Hydroponic Smart Greenhouse Market Insight

The Germany non-hydroponic smart greenhouse market is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing technological innovation in agriculture and the growing demand for efficient food production systems. Germany’s strong emphasis on sustainability and energy-efficient greenhouse technologies encourages the adoption of automated climate control and smart monitoring systems. The country’s advanced manufacturing capabilities and agricultural research initiatives also support the expansion of smart greenhouse infrastructure.

Asia-Pacific Non-Hydroponic Smart Greenhouse Market Insight

The Asia-Pacific non-hydroponic smart greenhouse market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing population, rising food demand, and expanding investments in modern agricultural infrastructure across developing economies. Countries across the region are adopting smart greenhouse technologies to improve agricultural productivity and address challenges related to climate variability and limited arable land. Government initiatives promoting smart farming and digital agriculture are also encouraging wider adoption of advanced greenhouse systems.

Japan Non-Hydroponic Smart Greenhouse Market Insight

The Japan non-hydroponic smart greenhouse market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced agricultural technology adoption and growing demand for efficient food production systems. Japanese growers are increasingly implementing automated greenhouse systems equipped with climate monitoring, irrigation control, and data-driven crop management technologies. The need to address labor shortages in agriculture and maintain high crop productivity is further encouraging the use of smart greenhouse solutions.

China Non-Hydroponic Smart Greenhouse Market Insight

The China non-hydroponic smart greenhouse market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s rapid agricultural modernization and increasing investments in greenhouse farming infrastructure. China has emerged as a major market for smart agricultural technologies, with greenhouse cultivation expanding across commercial farms and urban agriculture projects. Government initiatives supporting smart farming, combined with rising demand for high-quality food products, continue to drive the adoption of non-hydroponic smart greenhouse systems in the country.

Non-Hydroponic Smart Greenhouse Market Share

The Non-Hydroponic Smart Greenhouse industry is primarily led by well-established companies, including:

• Certhon (Netherlands)

• Argus Control Systems Limited (Canada)

• Rough Brothers Inc. (U.S.)

• NETAFIM (Israel)

• Sensaphone (U.S.)

• Cultivar (U.S.)

• Heliospectra AB (Sweden)

• Motorleaf (Canada)

• NEXUS Co Ltd (U.S.)

• LOGIQS B.V (Netherlands)

• LumiGrow (U.S.)

• IoTConnect (U.S.)

• Pure Harvest Smart Farms, Ltd (U.A.E.)

• SAVEER BIOTECH LIMITED (India)

• AmHydro (U.S.)

• Agra Tech, Inc. (U.S.)

• Micro Grow Greenhouse Systems (U.S.)

• Emerald Kingdom Greenhouse, LLC (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Non Hydroponic Smart Greenhouse Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Non Hydroponic Smart Greenhouse Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Non Hydroponic Smart Greenhouse Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.