Global Multi Domain Controller Market

Market Size in USD Billion

CAGR :

%

USD

4.40 Billion

USD

26.90 Billion

2024

2032

USD

4.40 Billion

USD

26.90 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.40 Billion | |

| USD 26.90 Billion | |

| % | |

|

Multi Domain Controller Market Size

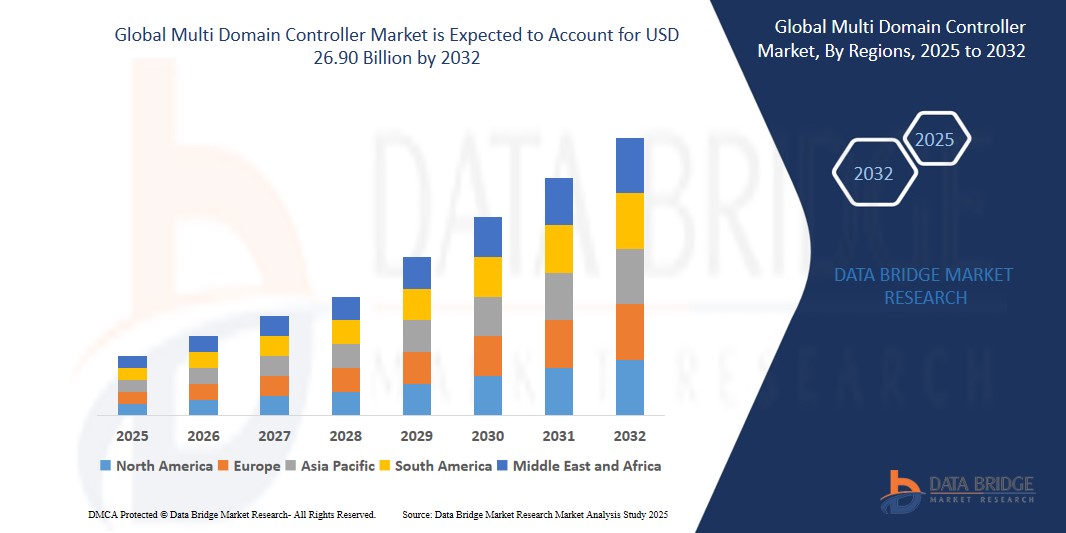

- The Global Multi Domain Controller Market size was valued at USD 4.40 billion in 2024 and is expected to reach USD 26.90 billion by 2032, at a CAGR of 9.0% during the forecast period

- This growth is driven by factors such as the increasing demand for centralized vehicle control systems, rising integration of advanced driver assistance systems, and the shift toward software-defined vehicles in the automotive industry

Multi Domain Controller Market Analysis

- The current multi domain controller market is experiencing rapid expansion due to the increasing complexity of electronic architectures in modern vehicles, prompting a shift toward centralized control units

- This transition not only simplifies vehicle architecture but also supports faster communication between systems, enabling quicker response times and more efficient operation

- Asia-Pacific is expected to dominate the multi domain controllers market due to its advanced automotive industry, early adoption of centralized electronic architectures, and strict regulatory standards.

- North America is expected to be the fastest growing region in the multi domain controller market during the forecast period due to rapid digital transformation, increasing investments in it infrastructure, and the presence of major market players in countries like China, Japan, and India

- The cockpit electronics segment is expected to dominate the multi domain controller market with market share of 24.7% due to the rising demand for integrated infotainment, digital displays, and connected vehicle experiences enhancing driver and passenger interaction. Automakers are increasingly focusing on delivering seamless user experiences through connected and intelligent cockpit environments. This shift enhances comfort, control, and personalization within vehicles, driving strong demand for centralized controller solutions.

Report Scope and Multi Domain Controller Market Segmentation

|

Attributes |

Multi Domain Controller Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Multi Domain Controller Market Trends

“Shift Toward Software-Defined Vehicle Architecture”

- The current multi domain controller market is experiencing a significant trend toward software-defined vehicle architecture, where software plays a central role in vehicle operations rather than traditional hardware-based control systems

- This shift is driven by the need for a more centralized computing platform that allows integration of multiple domains such as infotainment, advanced driver assistance systems, and powertrain control under one unified controller

- Automakers are increasingly adopting this architecture to simplify vehicle electronics, reduce weight, and enable faster updates and enhancements over-the-air, allowing more agile development cycles.

- For instance, leading car manufacturers are collaborating with tech firms to create centralized controllers that manage various functionalities, replacing several electronic control units with a single high-performance domain controller.

- This trend also supports the evolution of connected and autonomous vehicles by allowing seamless communication between systems, improving efficiency, and paving the way for future innovations in mobility

- In conclusion, companies like Tesla and BMW have implemented centralized computing approaches that streamline vehicle electronics and improve overall performance and upgradeability

Multi Domain Controller Market Dynamics

Driver

“Growing Demand for Vehicle Electronics Integration”

- The rising complexity in vehicle design is increasing demand for integrated electronics as consumers expect smart features like navigation, driver assistance, and infotainment in real time

- Traditional vehicles used separate electronic control units for each function but this approach leads to higher costs and added weight, reducing efficiency and increasing production challenges

- Automakers are adopting multi domain controllers to combine various systems into a single unit which simplifies wiring and enables faster subsystem communication for improved reliability

For instance,

- In October 2024, Mercedes-Benz uses a centralized computing architecture in its EQS model to control multiple systems including infotainment, driver assistance, and battery management. The growth of electric vehicles, which rely on synchronized software control, is accelerating the use of such controllers that allow for seamless updates and coordinated performance. In conclusion, multi domain controllers offer a scalable, efficient solution to meet the growing digital demands in modern vehicles while also cutting costs and enhancing performance

Opportunity

“Advancements in Artificial Intelligence Integration”

- Integration of artificial intelligence into vehicle control systems is opening new possibilities for real-time decision-making and adaptive functionality across multiple vehicle domains

- Multi domain controllers act as the central hub for managing systems like safety, navigation, and performance using AI to analyze environments and respond instantly to road conditions

For instance,

- In January 2025, Tesla's Full Self-Driving system uses AI within a centralized architecture to predict behavior and navigate complex driving scenarios autonomously. Predictive maintenance is another benefit where AI monitors system health and alerts users before failures occur, reducing downtime and extending the lifespan of components

- Leading automakers and tech companies are investing in AI-enabled controllers that support features like natural language interaction, gesture control, and self-learning for continuous performance improvements

- In conclusion, AI-powered multi domain controllers represent a major step toward smarter, safer, and more personalized driving experiences while offering a valuable growth avenue for the automotive industry.

Restraint/Challenge

“High System Complexity and Integration Costs”

- The integration of multi domain controllers requires a complex hardware and software setup capable of managing several vehicle functions simultaneously while ensuring safety and security

- Developing these systems demands heavy investment in engineering, testing, and regulatory compliance which raises the initial development cost significantly

For instance,

- In November 2024, Volkswagen’s transition to a unified electronic architecture with Cariad faced delays due to software integration challenges across different supplier modules. Ensuring seamless communication between subsystems developed by various vendors increases the risk of compatibility issues and slows down implementation

- Ensuring seamless communication between subsystems developed by various vendors increases the risk of compatibility issues and slows down implementation

Multi Domain Controller Market Scope

The market is segmented on the basis of vehicle type, application, propulsion type, bit size, level of autonomy, operating system, and bus systems.

|

Segmentation |

Sub-Segmentation |

|

By Vehicle Type |

|

|

By Application |

|

|

By Propulsion Type |

|

|

By Bit Size |

|

|

By Level of Autonomy |

|

|

By Operating System |

|

|

By Bus Systems |

|

In 2025, cockpit segment is projected to dominate the market with a largest share in application segment

The cockpit segment is expected to dominate the multi domain controller market with market share of 24.7% due to the rising demand for integrated infotainment, digital displays, and connected vehicle experiences enhancing driver and passenger interaction. Automakers are increasingly focusing on delivering seamless user experiences through connected and intelligent cockpit environments. This shift enhances comfort, control, and personalization within vehicles, driving strong demand for centralized controller solutions.

The android segment is expected to account for the largest share during the forecast period in multi domain controller Segment

In 2025, the android segment is expected to dominate the market with the largest market due to its open-source nature, flexibility for customization by automakers, and widespread developer support. Its compatibility with a broad range of applications and seamless integration with consumer devices make it a preferred choice for in-vehicle infotainment and smart cockpit systems.

Multi Domain Controller Market Regional Analysis

“Asia-Pacific Holds the Largest Share in the Multi Domain Controller Market”

- Asia-Pacific leads the global multi-domain controller market due to China’s dominance in automotive production, with the country manufacturing over 26 million vehicles in 2023, the highest globally (OICA)

- Rapid integration of autonomous and connected vehicle tech in Japan and South Korea is driving demand for MDCs, with Hyundai and Toyota increasingly adopting centralized architectures in recent models like Hyundai Ioniq 6 and Toyota bZ4X

- Government mandates such as China’s GB/T standards and India’s AIS-140 for vehicle tracking and safety are accelerating the shift to MDC-based E/E architectures

- The region’s booming EV market, led by BYD and Tata Motors, is relying on MDCs to manage vehicle control units more efficiently, with BYD selling over 3 million EVs in 2023 alone

- Asian OEMs like Denso and Huawei are investing heavily in MDC R&D, with Denso unveiling its latest integrated ECU platform at the Tokyo Mobility Show 2023 to enhance in-vehicle computing

“North America is Projected to Register the Highest CAGR in the Multi Domain Controller Market”

- North America is projected to register the highest CAGR in the multi-domain controller market driven by increasing adoption of ADAS and autonomous vehicle technologies by companies like Tesla and Ford

- Automakers like General Motors and Stellantis are investing in centralized vehicle architectures using MDCs to streamline ECUs as seen in GM’s Ultifi platform and Stellantis’s STLA Brain

- The National Highway Traffic Safety Administration (NHTSA) and EPA mandates on vehicle safety and emissions are prompting OEMs to integrate MDCs for better system coordination and compliance

- North America is witnessing rapid tech innovation with companies like Nvidia and Qualcomm providing automotive SoCs enabling advanced MDCs for seamless integration across multiple vehicle domains

- Strategic partnerships like Tesla and Samsung’s collaboration for advanced controllers in next-gen EVs highlight the region’s momentum in MDC deployment aligned with the surge in electric vehicle adoption

Multi Domain Controller Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Continental AG (Germany)

- Visteon Corporation (U.S.)

- Robert Bosch GmbH (Germany)

- Aptiv (Ireland)

- Panasonic Corporation (Japan)

- ZF Friedrichshafen AG (Germany)

- Magna International Inc. (Canada)

- Lear Corporation (U.S.)

- Faurecia (France)

- Autoliv Inc (Sweden)

- Sasken Technologies Ltd (India)

- Magneti Marelli S.p.A. (Italy)

- HARMAN International (U.S.)

- NXP Semiconductors (Netherlands)

- Hitachi Ltd. (Japan)

- Texas Instruments Incorporated (U.S.)

- Mitsubishi Electric Corporation (Japan)

- NVIDIA Corporation (U.S.)

- Infineon Technologies AG (Germany)

- STMicroelectronics (Switzerland)

Latest Developments in Global Multi Domain Controller Market

- In January 2023, Ambarella introduced the CV3-AD685, a high-performance AI domain controller SoC designed for L2+ to L4 autonomous vehicles. It features a 20x faster neural vector processor and integrates advanced image processing and radar capabilities. The CV3-AD685 enables centralized processing for multi-sensor perception, fusion, and path planning, offering a single-chip solution for autonomous driving systems

- In February 2023, Ambarella partnered with Hyperview, an autonomous driving tech company, to develop high-performance computing platforms for autonomous driving. Hyperview selected Ambarella's CV3-AD family of AI central domain controller SoCs to integrate with its software stack, aiming to provide production-ready perception, automated driving, and parking solutions for Tier-1 suppliers and OEMs

- In November 2022, Continental and Ambarella formed a strategic partnership to offer advanced driver assistance systems (ADAS) solutions based on Ambarella's CV3 AI domain controller SoC family. This collaboration combines Continental's software and hardware expertise with Ambarella's AI capabilities to provide scalable mobility system solutions for Level 2+ to Level 4 automated vehicles

- In December 2023, Ambarella unveiled a full software stack optimized for its CV3-AD central AI domain controller family. The stack, based on deep learning AI processing, includes modules for environmental perception, sensor fusion, and vehicle path planning. It is designed to minimize power consumption and processing load, accelerating OEM development and offering scalability for L2+ and higher autonomy levels

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.