Global Minimally Invasive And Non Invasive Medical Imaging

Market Size in USD Billion

USD

80.48 Billion

USD

117.82 Billion

2025

2033

USD

80.48 Billion

USD

117.82 Billion

2025

2033

| 2026 - 2033 | |

| USD 80.48 Billion | |

| USD 117.82 Billion | |

| % | |

|

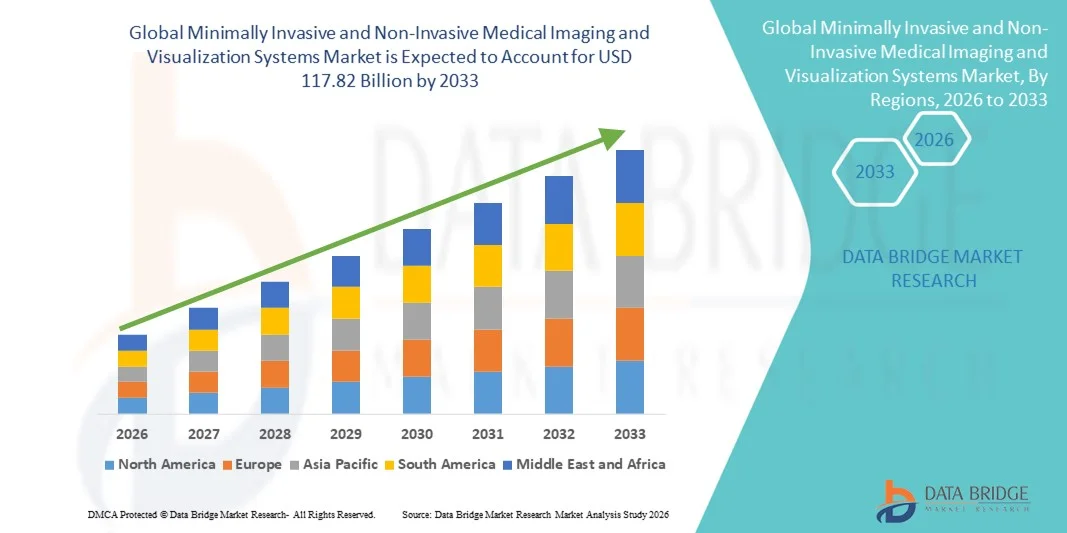

Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Size

- The global minimally invasive and non-invasive medical imaging and visualization systems market size was valued at USD 80.48 billion in 2025 and is expected to reach USD 117.82 billion by 2033, at a CAGR of 4.88% during the forecast period

- The market growth is largely fueled by rapid technological advancements in medical imaging and visualization systems, along with the increasing adoption of minimally invasive and non-invasive diagnostic and interventional procedures, driving higher utilization across hospitals, diagnostic centers, and specialty clinics. Continuous innovation in imaging modalities, including high-resolution imaging, real-time visualization, and AI-assisted image analysis, is accelerating digital transformation in healthcare settings

- Furthermore, rising demand for early and accurate disease diagnosis, reduced patient trauma, shorter recovery times, and improved clinical outcomes is establishing minimally invasive and non-invasive medical imaging and visualization systems as the preferred solution for modern healthcare delivery. These converging factors are accelerating the uptake of Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems, thereby significantly boosting the overall market growth

Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Analysis

- Minimally invasive and non-invasive medical imaging and visualization systems, which enable precise diagnosis and real-time visualization without extensive surgical intervention, are becoming critical components of modern healthcare delivery across hospitals, diagnostic imaging centers, and specialty clinics. Their ability to improve diagnostic accuracy, reduce patient risk, and support image-guided procedures is driving widespread adoption globally

- The escalating demand for these systems is primarily fueled by the rising prevalence of chronic diseases, growing preference for minimally invasive procedures, and continuous technological advancements such as AI-enabled image analysis, 3D/4D visualization, and hybrid imaging platforms. These innovations enhance clinical outcomes, shorten hospital stays, and improve workflow efficiency, making them the preferred choice for healthcare providers

- North America dominated the minimally invasive and non-invasive medical imaging and visualization systems market with the largest revenue share of approximately 38.5% in 2025, supported by advanced healthcare infrastructure, high adoption of cutting-edge imaging technologies, strong reimbursement frameworks, and the presence of leading medical device manufacturers. The U.S. accounted for the majority share in the region, driven by high procedure volumes, early adoption of AI-integrated imaging systems, and continuous investments in diagnostic innovation

- Asia-Pacific is expected to be the fastest-growing region in the minimally invasive and non-invasive medical imaging and visualization systems market during the forecast period, registering a projected CAGR of around 9.9%. This growth is attributed to expanding healthcare infrastructure, rising healthcare expenditure, increasing awareness of early disease diagnosis, and growing adoption of advanced imaging technologies across China, India, and Southeast Asian countries

- The ultrasound segment dominated the market with the largest revenue share of approximately 34.6% in 2025, driven by its non-invasive nature, cost-effectiveness, and widespread clinical use

Report Scope and Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Segmentation

|

Attributes |

Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Trends

Enhanced Clinical Precision Through AI-Enabled Imaging and Advanced Visualization Technologies

- A significant and accelerating trend in the global minimally invasive and non-invasive medical imaging and Visualization Systems market is the growing integration of artificial intelligence (AI), real-time image processing, and advanced visualization software to enhance diagnostic accuracy, procedural efficiency, and clinical decision-making across multiple medical specialties

- For instance, in November 2023, GE HealthCare launched its AI-powered Precision Ultrasound software upgrades, designed to improve image clarity, automate measurements, and support minimally invasive diagnostic procedures in cardiology, obstetrics, and critical care settings

- AI-enabled imaging systems assist clinicians by automatically detecting anatomical structures, highlighting abnormalities, and reducing interpretation variability, which is particularly valuable in minimally invasive procedures such as endoscopy, laparoscopy, and image-guided interventions

- Advanced visualization platforms, including 3D imaging, augmented reality (AR), and real-time navigation systems, are increasingly being integrated into operating rooms, enabling surgeons to visualize complex anatomical details during minimally invasive procedures with greater confidence.

- This shift toward intelligent imaging and visualization solutions is reshaping clinician expectations, driving demand for systems that not only capture images but also provide actionable insights to improve procedural outcomes and reduce complication rates

- As a result, leading companies such as Siemens Healthineers, Philips Healthcare, and Olympus are investing heavily in AI-driven imaging platforms and software upgrades to strengthen their global competitive positioning

Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Dynamics

Driver

Rising Demand for Minimally Invasive Procedures and Early Disease Detection

- The increasing global preference for minimally invasive and non-invasive diagnostic and therapeutic procedures is a major driver for the growth of advanced medical imaging and visualization systems, as these approaches reduce patient trauma, shorten hospital stays, and lower overall healthcare costs

- For instance, in June 2024, Philips Healthcare announced the expansion of its Azurion image-guided therapy platform, aimed at supporting minimally invasive cardiovascular and neurological procedures by providing high-resolution real-time imaging and improved workflow efficiency

- The growing burden of chronic diseases such as cardiovascular disorders, cancer, and gastrointestinal conditions is fueling the need for early and accurate diagnosis, further increasing adoption of advanced imaging technologies

- Technological advancements in ultrasound, endoscopy, MRI, CT, and hybrid imaging systems are enabling clinicians to perform complex procedures with greater precision while minimizing invasiveness

- In addition, increasing investments in hospital infrastructure modernization and ambulatory surgical centers across both developed and emerging economies are supporting widespread adoption of advanced visualization systems

- Collectively, these factors are driving sustained global demand for minimally invasive and non-invasive medical imaging and visualization systems across diagnostic and interventional applications

Restraint/Challenge

High System Costs and Limited Access in Resource-Constrained Settings

- One of the key challenges facing the global minimally invasive and non-invasive medical imaging and visualization systems market is the high capital cost associated with advanced imaging equipment, including AI-enabled platforms, 3D visualization systems, and image-guided intervention suites

- For instance, in 2022, several public hospitals in low- and middle-income countries reported delays in adopting advanced imaging technologies due to budget constraints and high maintenance costs, limiting access to minimally invasive diagnostic solutions in these regions

- The cost of system installation, regular software upgrades, specialized consumables, and skilled personnel training further adds to the overall financial burden for healthcare providers

- In addition, stringent regulatory approval processes and compliance requirements can slow product commercialization and increase development costs for manufacturers

- Limited availability of trained radiologists, surgeons, and technicians capable of operating advanced imaging and visualization systems also restricts adoption, particularly in rural and underserved areas

- Overcoming these challenges through cost-effective system designs, scalable imaging platforms, training initiatives, and public-private partnerships will be critical to expanding global market penetration and ensuring equitable access to advanced medical imaging technologies

Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Scope

The market is segmented on the basis of type, application, and end users.

- By Type

On the basis of type, the Global Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems market is segmented into ultrasound, CT imaging, X-ray imaging, MRI imaging, nuclear imaging, and others. The ultrasound segment dominated the market with the largest revenue share of approximately 34.6% in 2025, driven by its non-invasive nature, cost-effectiveness, and widespread clinical use. Ultrasound systems are extensively used across cardiology, obstetrics, gynecology, and emergency care. The absence of ionizing radiation makes ultrasound a preferred modality for repeated imaging. Portable and point-of-care ultrasound systems are increasingly adopted in hospitals and clinics. Technological advancements such as 3D/4D imaging and AI-assisted diagnostics enhance diagnostic accuracy. High demand from developing regions due to affordability supports market dominance. Increasing use in minimally invasive procedures further drives adoption. Broad availability across healthcare settings strengthens its leading position.

The MRI imaging segment is expected to witness the fastest growth, registering a CAGR of 9.8% from 2026 to 2033. Growth is driven by rising demand for high-resolution imaging and superior soft tissue contrast. MRI is increasingly used in neurology, oncology, and musculoskeletal diagnostics. Advancements in high-field MRI and faster scanning technologies are improving workflow efficiency. Increasing prevalence of neurological and chronic disorders supports demand. Growing investments in advanced diagnostic infrastructure boost adoption. Expansion of minimally invasive surgical planning applications accelerates growth. Rising awareness of radiation-free imaging further strengthens MRI uptake globally.

- By Application

On the basis of application, the market is segmented into neurology, cardiology, gastrointestinal, orthopaedic, gynaecological, and others. The cardiology segment dominated the market with a revenue share of approximately 29.8% in 2025, driven by the global rise in cardiovascular diseases. Imaging modalities such as ultrasound, CT, and MRI are critical for cardiac diagnosis and intervention planning. Increasing aging population significantly contributes to demand. Non-invasive cardiac imaging reduces procedural risks and improves patient outcomes. Growing use of echocardiography and CT angiography supports segment dominance. High diagnostic accuracy and rapid assessment capabilities enhance adoption. Continuous innovation in cardiac visualization systems strengthens market presence. Expansion of cardiac care centers further drives demand.

The neurology segment is projected to grow at the fastest rate, with a CAGR of 10.4% from 2026 to 2033. Growth is driven by increasing prevalence of neurological disorders such as stroke, Alzheimer’s disease, and Parkinson’s disease. MRI and CT imaging play a critical role in brain diagnostics. Rising demand for early and accurate diagnosis supports adoption. Technological advancements in functional MRI and brain mapping enhance clinical value. Increasing research in neuroimaging accelerates market growth. Expanding awareness of neurological health boosts imaging utilization. Growth in minimally invasive neurosurgical procedures further fuels demand.

- By End Users

On the basis of end users, the market is segmented into hospitals and clinics, diagnostic centres, and academic institutes and research organizations. Hospitals and clinics dominated the market with the largest revenue share of approximately 46.3% in 2025, driven by high patient volumes and advanced diagnostic capabilities. These settings require comprehensive imaging systems for diagnosis, treatment planning, and monitoring. Availability of skilled radiologists supports higher utilization rates. Integration of imaging systems with electronic health records enhances workflow efficiency. Hospitals invest heavily in advanced MRI, CT, and ultrasound systems. Growing demand for minimally invasive procedures strengthens adoption. Emergency and critical care imaging further contributes to dominance. Continuous infrastructure upgrades support sustained market leadership.

The diagnostic centres segment is expected to grow at the fastest pace, recording a CAGR of 9.6% from 2026 to 2033. Growth is driven by increasing outsourcing of imaging services by hospitals. Diagnostic centres offer cost-effective and specialized imaging services. Rising patient preference for standalone diagnostic facilities supports growth. Expansion of private diagnostic chains in emerging markets accelerates adoption. Advanced imaging equipment investments improve service quality. Faster turnaround times enhance patient satisfaction. Growing preventive healthcare awareness further drives demand. Increasing insurance coverage supports diagnostic centre expansion.

Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Regional Analysis

- North America dominated the minimally invasive and non-invasive medical imaging and visualization systems market with the largest revenue share of approximately 38.5% in 2025, supported by advanced healthcare infrastructure, high adoption of cutting-edge imaging technologies, favorable reimbursement frameworks, and the strong presence of leading medical device manufacturers

- The region benefits from widespread utilization of minimally invasive diagnostic and interventional procedures, particularly in cardiology, oncology, neurology, and gastroenterology, driving sustained demand for advanced imaging and visualization platforms

- Continuous investments in hospital modernization, outpatient surgical centers, and image-guided therapy suites further reinforce North America’s leadership position in the global market

U.S. Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Insight

The U.S. minimally invasive and non-invasive medical imaging and visualization systems market accounted for the largest share of over 80% of North America’s market revenue in 2025, driven by high procedure volumes, early adoption of AI-assisted imaging and visualization systems, and strong investment in diagnostic innovation. The country’s robust clinical research ecosystem, high prevalence of chronic diseases, and rapid uptake of minimally invasive surgical techniques continue to propel demand for advanced imaging modalities across hospitals and specialty clinics.

Europe Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Insight

The Europe minimally invasive and non-invasive medical imaging and visualization systems market is expected to grow at a steady CAGR during the forecast period, supported by increasing adoption of minimally invasive procedures, rising emphasis on early disease detection, and ongoing healthcare digitization initiatives across the region. Strong regulatory frameworks promoting patient safety, along with public healthcare investments, are driving demand for high-precision imaging and visualization systems in both diagnostic and interventional settings. Growth is evident across Western and Northern Europe, particularly in countries with well-established healthcare systems and aging populations.

U.K. Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Insight

The U.K. minimally invasive and non-invasive medical imaging and visualization systems market is anticipated to expand at a notable CAGR, driven by increasing adoption of minimally invasive diagnostic techniques, rising burden of chronic diseases, and ongoing investments by the National Health Service (NHS) to modernize diagnostic imaging infrastructure. The emphasis on reducing hospital stay durations and improving procedural efficiency is accelerating the deployment of advanced visualization and imaging systems across public and private healthcare facilities.

Germany Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Insight

Germany minimally invasive and non-invasive medical imaging and visualization systems market is expected to witness considerable growth during the forecast period, supported by its technologically advanced healthcare infrastructure, strong medical device manufacturing base, and high adoption of precision imaging technologies. The country’s focus on innovation, clinical accuracy, and early diagnosis continues to drive demand for advanced minimally invasive and non-invasive imaging and visualization systems across hospitals and research institutions.

Asia-Pacific Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Insight

- Asia-Pacific is projected to be the fastest-growing regional market, registering a CAGR of approximately 9.9% during the forecast period, driven by expanding healthcare infrastructure, rising healthcare expenditure, and increasing awareness of early disease diagnosis

- Rapid urbanization, improving access to advanced medical technologies, and government initiatives to strengthen healthcare systems are accelerating adoption across China, India, Japan, and Southeast Asian countries

- The growing number of hospitals, diagnostic centers, and ambulatory surgical facilities is further supporting market expansion in the region

Japan Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Insight

Japan’s minimally invasive and non-invasive medical imaging and visualization systems market is gaining momentum due to its aging population, high demand for minimally invasive diagnostic and therapeutic procedures, and strong emphasis on technological innovation. Advanced imaging systems that enhance procedural precision and reduce patient discomfort are increasingly adopted across hospitals and specialty clinics, supporting steady market growth.

China Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Insight

China minimally invasive and non-invasive medical imaging and visualization systems market accounted for the largest revenue share within Asia-Pacific in 2025, driven by rapid healthcare infrastructure development, increasing government investment in medical technology, and rising demand for early and accurate diagnosis. The country’s expanding hospital network, growing medical tourism sector, and strong presence of domestic and international imaging system manufacturers are key factors propelling market growth.

Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market Share

The Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems industry is primarily led by well-established companies, including:

• GE HealthCare (U.S.)

• Siemens Healthineers (Germany)

• Philips Healthcare (Netherlands)

• Canon Medical Systems (Japan)

• FUJIFILM Holdings Corporation (Japan)

• Samsung Medison (South Korea)

• Hitachi Healthcare (Japan)

• Mindray Medical International (China)

• Hologic, Inc. (U.S.)

• Carestream Health (U.S.)

• Shimadzu Corporation (Japan)

• Esaote S.p.A. (Italy)

• Agfa-Gevaert Group (Belgium)

• Koninklijke Philips N.V. (Netherlands)

• Toshiba Medical Systems (Japan)

• Analogic Corporation (U.S.)

• United Imaging Healthcare (China)

• Planmed Oy (Finland)

• Neusoft Medical Systems (China)

• Ziehm Imaging (Germany)

Latest Developments in Global Minimally Invasive and Non-Invasive Medical Imaging and Visualization Systems Market

- In November 2022, Philips unveiled its AI-powered MR SmartSpeed and advanced imaging portfolio at RSNA 2022, including improvements to MR and CT systems aimed at increasing image quality, speeding workflows, and enhancing diagnostics across oncology, cardiology, and interventional imaging. The announcement highlighted AI reconstructions and workflow automation to support minimally invasive procedures

- In September 2023, GE Healthcare entered a strategic partnership to enhance near-infrared fluorescence (NIRF) imaging systems with advanced AI algorithms designed to improve image analysis speed and diagnostic accuracy, signaling growing integration of artificial intelligence into non-invasive imaging platforms

- In October 2023, Siemens Healthineers launched the Magnetom Flow 1.5T MRI platform, a virtually helium-free MRI system designed to improve sustainability and diagnostic imaging performance, representing an innovation in non-invasive MRI technology

- In February 2025, Philips showcased a suite of next-generation AI-driven imaging systems at Arab Health 2025, including the helium-free BlueSeal 1.5T MRI with Smart Reading automated reporting and AI-enabled CT 5300 with Precise Image AI reconstruction, targeting improved workflow efficiency, diagnostic confidence, and lower radiation dose

- In March 2025, GE Healthcare and NVIDIA announced a collaboration to develop AI-powered X-ray and ultrasound systems using NVIDIA’s Isaac for Healthcare platform. This partnership is expected to significantly enhance diagnostic accuracy and efficiency in non-invasive imaging applications worldwide

- In May 2025, the global endoscopy visualization systems market highlighted advances in AI-powered 4K and 3D imaging technologies, such as narrow-band imaging and fluorescence visualization, which are being increasingly adopted to improve visualization and early disease detection during minimally invasive procedures

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.