Global Metagonimiasis Treatment Market

Market Size in USD Billion

CAGR :

%

USD

320.50 Billion

USD

431.92 Billion

2025

2033

USD

320.50 Billion

USD

431.92 Billion

2025

2033

| 2026 - 2033 | |

| USD 320.50 Billion | |

| USD 431.92 Billion | |

| % | |

|

Metagonimiasis Treatment Market Size

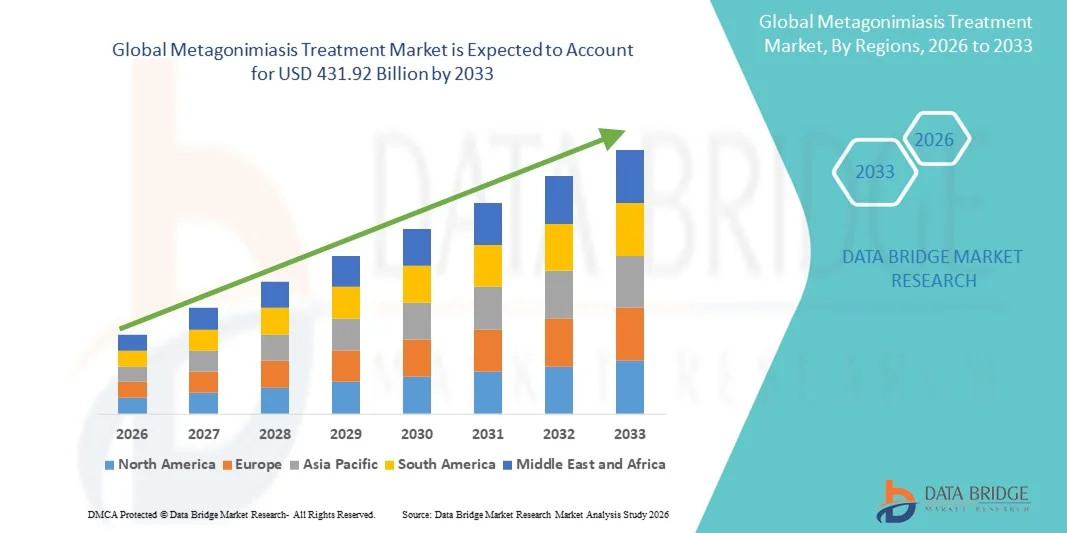

- The global metagonimiasis treatment market size was valued at USD 320.50 billion in 2025 and is expected to reach USD 431.92 billion by 2033, at a CAGR of3.80% during the forecast period

- The market growth is largely fueled by increasing awareness of parasitic infections, advancements in diagnostic techniques, and the development of more effective treatment options for metagonimiasis

- Furthermore, rising healthcare expenditure, expanding access to specialized infectious disease services, and growing public health initiatives aimed at controlling foodborne parasitic infections are driving the adoption of metagonimiasis treatment solutions, thereby significantly boosting the industry's growth

Metagonimiasis Treatment Market Analysis

- Metagonimiasis, a foodborne parasitic infection, poses significant health challenges, and the demand for effective treatment solutions is increasing across hospitals, clinics, and healthcare centers globally due to rising awareness and prevalence of the disease

- The escalating demand for Metagonimiasis Treatment is primarily fueled by advancements in pharmaceutical therapies, improved diagnostic capabilities, and growing initiatives for early detection and management of parasitic infections

- North America dominated the metagonimiasis treatment market with the largest revenue share of 41.2% in 2025, supported by advanced healthcare infrastructure, high awareness of parasitic infections, and the presence of leading pharmaceutical companies specializing in infectious disease treatments, with the U.S. accounting for the majority of treated cases due to early diagnosis and adoption of innovative therapies

- Asia-Pacific is expected to be the fastest growing region in the metagonimiasis treatment market during the forecast period, registering a projected CAGR of around 9.8%, driven by increasing healthcare investments, improving access to infectious disease services, rising awareness about Metagonimiasis, and expanding availability of treatment options in emerging economies such as China, India, and Southeast Asia

- The Oral segment dominated the largest market revenue share of 63.5% in 2025, due to widespread preference for tablets and oral solutions for primary therapy

Report Scope and Metagonimiasis Treatment Market Segmentation

|

Attributes |

Metagonimiasis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Metagonimiasis Treatment Market Trends

Rising Prevalence and Increased Awareness of Parasitic Infections

- A significant trend in the global metagonimiasis treatment market is the growing recognition of metagonimiasis as a public health concern in endemic regions of Asia, particularly in Korea, Japan, and parts of Southeast Asia

- For instance, in 2023, South Korea reported a rise in metagonimiasis cases linked to consumption of raw freshwater fish, prompting enhanced surveillance programs

- Increased epidemiological surveillance and reporting of foodborne parasitic infections are helping healthcare providers and governments identify high-risk populations more accurately

- The expansion of diagnostic facilities and improved laboratory capabilities are allowing for earlier detection and timely treatment of infections

- Public health campaigns and awareness programs emphasizing safe food handling and consumption of properly cooked fish are contributing to preventive measures

- These initiatives are also creating higher demand for effective therapeutic options, as patients and clinicians are becoming more aware of treatment protocols

- The trend towards integrated disease management, including preventive education and pharmaceutical interventions, is shaping the market landscape

- Rising research interest in new anti-parasitic compounds and combination therapies is further bolstering market activity

Metagonimiasis Treatment Market Dynamics

Driver

Increasing Incidence of Metagonimiasis and Expanding Therapeutic Options

- The increasing prevalence of metagonimiasis infections, particularly in regions with high consumption of freshwater fish, is a key driver for the market

- For instance, in 2022, Japan’s Ministry of Health reported increased demand for praziquantel following several regional outbreaks

- In response, pharmaceutical companies are expanding their product portfolios with anthelmintic therapies such as praziquantel and albendazole, enhancing treatment accessibility

- Improved healthcare infrastructure in endemic countries is enabling broader distribution of anti-parasitic drugs

- Rising government initiatives and funding for parasitic disease control programs are also supporting market growth

- Healthcare professionals are increasingly adopting standardized treatment protocols, leading to consistent demand for approved medications

- Continuous research and clinical studies exploring safer dosing regimens and combination therapy options are strengthening market confidence

- The growing availability of oral and intravenous formulations is improving patient compliance, which further drives adoption

Restraint/Challenge

Limited Awareness in Non-Endemic Regions and Drug Accessibility Issues

- Despite growth in endemic areas, low awareness of metagonimiasis in non-endemic regions limits global market expansion

- For instance, in 2021, cases in the U.S. were underdiagnosed due to limited clinician familiarity with the infection

- Inadequate diagnostic facilities and underreporting of cases in some developing countries hinder timely treatment initiation

- The high cost of certain anti-parasitic medications can be a barrier for price-sensitive patients, particularly in rural areas

- Shortages of some specialized formulations, such as pediatric doses, create challenges for consistent patient care

- Healthcare providers face difficulties in maintaining stock of medications due to distribution inefficiencies and logistical issues

- Resistance concerns, though still limited, pose a potential challenge to long-term efficacy of standard therapies

- Addressing these barriers through awareness campaigns, affordable medication programs, and expanded distribution networks will be vital for sustained market growth

Metagonimiasis Treatment Market Scope

The market is segmented on the basis of Treatment, Diagnosis, Dosage, Route of Administration, Symptoms, End-Users, and Distribution Channel.

- By Type

On the basis of type, the Metagonimiasis Treatment market is segmented into Anthelminthics, Electrolyte Therapy, and Others. The Anthelminthics segment dominated the largest market revenue share of 52.3% in 2025, driven by the established efficacy of drugs such as praziquantel and albendazole in treating metagonimiasis. Anthelminthics are considered first-line therapy and are widely prescribed due to their rapid action against intestinal flukes, leading to high patient compliance. Hospitals and clinics prioritize this segment due to its availability, ease of administration, and low complication rate. The segment also benefits from the growing prevalence of metagonimiasis in endemic regions of Asia, prompting routine use. Research studies continue to support the effectiveness of standard anthelmintic regimens, reinforcing confidence among healthcare providers. Pharmaceutical companies are expanding production capacities to meet the growing demand, while government health programs subsidize costs in affected regions. Training programs for healthcare professionals emphasize the timely prescription of anthelmintics, further consolidating market share. Public health initiatives promoting awareness of intestinal parasites are increasing prescription volumes. Strategic collaborations between manufacturers and hospitals improve supply chain reliability. The segment's dominance is reinforced by robust clinical evidence and widespread adoption. Continuous monitoring for drug resistance also drives research-backed improvements in formulations. Overall, the Anthelminthics segment is a cornerstone of the Metagonimiasis Treatment market, sustaining high revenue consistently.

The Electrolyte Therapy segment is expected to witness the fastest CAGR of 10.9% from 2026 to 2033, driven by its critical role in managing dehydration and electrolyte imbalances associated with severe diarrhea caused by metagonimiasis. Electrolyte solutions are increasingly used alongside primary treatment to improve patient recovery and reduce hospitalization duration. Hospitals in endemic regions are adopting IV and oral rehydration therapies more systematically, leading to stronger uptake. The rise in awareness about supportive care among clinicians is boosting demand. Government programs promoting oral rehydration therapy in rural areas further accelerate market expansion. Technological advancements in ready-to-use electrolyte formulations improve patient compliance. Hospitals and clinics are increasingly stocking these therapies to manage outbreaks efficiently. The segment also benefits from growing pediatric and geriatric patient populations who are more vulnerable to dehydration. Educational campaigns by NGOs emphasize the importance of electrolyte replacement, driving end-user adoption. Pharmaceutical companies are launching innovative packaging and dosage forms to enhance convenience. Overall, the segment’s rapid growth is underpinned by clinical necessity, accessibility, and increasing awareness globally.

- By Diagnosis

On the basis of diagnosis, the Metagonimiasis Treatment market is segmented into Laboratory Tests, Physical Examination, Ova and Parasites Stool Test, and Others. The Ova and Parasites Stool Test segment dominated the largest market revenue share of 48.5% in 2025, due to its high accuracy and widespread use in endemic regions for detecting metagonimiasis infections. Routine stool testing is considered standard practice in hospitals and clinics, allowing early detection and timely intervention. Diagnostic laboratories widely offer ova and parasite tests, ensuring consistent availability. The segment’s dominance is reinforced by government-mandated surveillance programs in countries like Korea and Japan. Stool tests are cost-effective and suitable for large-scale screening, contributing to their widespread adoption. Clinical guidelines recommend repeat stool examinations to confirm treatment efficacy, driving repeat demand. The simplicity of sample collection and rapid turnaround for results further enhance utilization. Hospitals and clinics rely heavily on these tests to guide treatment decisions. The presence of trained laboratory technicians ensures accurate results, increasing confidence among physicians. Research continues to improve staining and microscopy methods, improving test sensitivity. Patient awareness campaigns encourage routine testing, particularly in high-risk communities. The segment’s strong clinical relevance solidifies its market-leading position.

The Laboratory Tests segment is expected to witness the fastest CAGR of 9.7% from 2026 to 2033, fueled by the increasing adoption of advanced diagnostic technologies such as PCR and immunofluorescence assays. These methods offer higher sensitivity and specificity than conventional tests, enabling early detection. Hospitals in urban and semi-urban regions are increasingly investing in molecular diagnostic tools. Rising prevalence of asymptomatic infections is encouraging proactive laboratory screening. Diagnostic companies are launching compact, automated systems for faster results. Integration with electronic medical records improves monitoring and follow-up treatment. Training programs for lab personnel expand usage across multiple healthcare settings. Government initiatives to modernize diagnostic infrastructure in endemic areas support growth. Advanced laboratory tests are being adopted for research studies, enhancing epidemiological data. The segment benefits from growing awareness among clinicians about the importance of precise diagnostics. Overall, laboratory-based diagnostics are gaining traction due to their accuracy, reliability, and growing adoption in modern healthcare.

- By Dosage

On the basis of dosage, the market is segmented into Tablet, Injection, and Others. The Tablet segment dominated the largest market revenue share of 61.4% in 2025, attributed to its convenience, cost-effectiveness, and patient preference for oral administration. Tablets are widely available for anthelmintic therapy and are suitable for both adults and pediatric patients. The segment benefits from extensive manufacturing and distribution networks ensuring accessibility. Compliance is higher due to ease of dosing and non-invasive administration. Hospitals and clinics recommend tablets as first-line therapy. Government health programs frequently provide tablet-based formulations in endemic regions. Tablets also facilitate standardization of dosage, minimizing risk of under- or over-treatment. Pharmaceutical innovations continue to improve tablet palatability and absorption rates. The segment’s dominance is supported by robust clinical evidence for efficacy and safety. Training of healthcare providers emphasizes tablet use, reinforcing adoption. The segment’s high revenue share reflects its combination of practicality, affordability, and broad acceptance.

The Injection segment is expected to witness the fastest CAGR of 8.6% from 2026 to 2033, driven by the need for rapid therapeutic intervention in severe or complicated cases of metagonimiasis, particularly in hospitalized patients. Injectable formulations provide higher bioavailability and faster action, making them essential for acute presentations. Hospitals and emergency care centers are increasingly stocking injectable options. The segment benefits from ongoing development of prefilled syringes and ready-to-use IV formulations for convenience. Growing awareness of severe dehydration and systemic complications boosts adoption. Medical training programs highlight injectable therapy for critically ill patients. Pharmaceutical companies are enhancing production capacity to meet hospital demand. Injectable therapy is increasingly used in combination with supportive care like electrolyte therapy. Overall, the segment’s growth is propelled by clinical necessity, ease of administration in critical care, and increasing adoption in hospitals.

- By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Intravenous, and Others. The Oral segment dominated the largest market revenue share of 63.5% in 2025, due to widespread preference for tablets and oral solutions for primary therapy. Oral administration is convenient for outpatient treatment, enhancing patient compliance. Hospitals, clinics, and retail pharmacies prioritize oral formulations for their cost-effectiveness. Public health initiatives frequently distribute oral drugs in endemic regions. Oral therapy aligns with standard treatment protocols recommended by WHO and national health authorities. Pharmaceutical manufacturers continue to optimize oral bioavailability and dosing schedules. Patients prefer oral routes due to non-invasive administration. Standardization and ease of storage further contribute to adoption. Oral therapy is integral in both prophylactic and treatment programs. The segment is reinforced by extensive clinical use, regulatory approval, and accessibility. Education campaigns promote oral drug adherence among patients. The segment’s high revenue share reflects convenience, reliability, and broad acceptance.

The Intravenous segment is expected to witness the fastest CAGR of 7.9% from 2026 to 2033, driven by hospitalization of severe cases requiring rapid onset of action and supportive care. IV therapy is increasingly used alongside electrolyte replacement and other interventions. Hospitals in endemic regions are expanding IV treatment capacity. Injectable solutions ensure precise dosing for critical patients. The segment benefits from technological advancements in infusion systems and ready-to-use formulations. Emergency care protocols in endemic countries encourage IV administration for acute complications. Growing awareness among healthcare providers about severe infection management boosts adoption. Combination therapy with IV anthelmintics enhances recovery outcomes. The segment’s growth is supported by clinical necessity, improved healthcare infrastructure, and rising hospitalization rates for severe infections.

- By Symptoms

On the basis of symptoms, the Global Metagonimiasis Treatment market is segmented into Abdominal Pain, Dehydration, Inflammation of the Intestines around the Infected Areas, Diarrhea, and Others. The Abdominal Pain segment accounts for a significant share of treatment focus, as abdominal discomfort is often the earliest and most frequently reported symptom in patients with metagonimiasis. Early intervention to manage abdominal pain improves patient compliance and allows timely initiation of primary therapy. Hospitals and clinics prioritize analgesics and supportive care in this segment to enhance patient comfort and treatment adherence. Public health awareness campaigns also encourage patients to seek care promptly when experiencing abdominal pain, contributing to higher treatment uptake. The segment benefits from robust clinical guidelines recommending symptomatic management alongside anthelmintic therapy, reinforcing its consistent market presence.

The Dehydration segment is expected to witness the fastest growth due to the critical role of fluid and electrolyte replacement in patient recovery. Severe diarrhea associated with metagonimiasis often leads to dehydration, especially in children and elderly populations. Intravenous (IV) and oral rehydration therapies are increasingly adopted by hospitals in endemic regions, improving treatment outcomes and reducing hospitalization durations. Government programs promoting oral rehydration therapy in rural and underserved areas further drive demand. The introduction of ready-to-use formulations and innovative packaging enhances accessibility and patient compliance. Educational initiatives by NGOs emphasizing hydration management also support adoption. Overall, the segment’s rapid growth is underpinned by clinical necessity, supportive care awareness, and increasing accessibility globally.

- By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, and Others. The Hospital segment dominated the largest market revenue share of 57.8% in 2025, due to the presence of specialized departments, trained healthcare professionals, and availability of comprehensive care for complicated metagonimiasis cases. Hospitals handle severe infections requiring hospitalization, monitoring, and combination therapies. They also provide IV and injection-based therapy, enhancing revenue share. Hospital pharmacies ensure availability of full-dose therapies. National health programs often channel drugs through hospitals. Hospitals benefit from high patient inflow in endemic regions. The segment’s dominance is reinforced by established clinical guidelines. Training and research programs in hospitals support continuous adoption. Hospitals also implement infection control and preventive strategies. The high revenue reflects centralized care, complex case management, and multi-route therapy availability.

The Clinic segment is expected to witness the fastest CAGR of 11.2% from 2026 to 2033, driven by the rise of outpatient treatment centers and increased access to diagnostic and oral treatment facilities. Clinics offer convenience, shorter wait times, and personalized care. Growing urbanization supports expansion of clinics. Clinics are increasingly adopting tablet-based therapies and lab diagnostics. Telemedicine integration enhances clinic reach in rural areas. Awareness campaigns target clinics for early diagnosis and treatment. Clinics are collaborating with pharmacies for better drug availability. Private healthcare infrastructure expansion fuels segment growth. Clinic-based management ensures follow-up care, boosting adoption. Rising middle-class healthcare demand supports rapid CAGR. Overall, clinics are fast-growing due to accessibility, efficiency, and patient convenience.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment dominated the largest market revenue share of 49.7% in 2025, due to direct access to prescription medications and comprehensive therapeutic management for inpatients. Hospitals handle severe and complicated cases, ensuring drug dispensing in controlled settings. Hospital pharmacies offer full-dose therapy, IV preparations, and combination treatments. National health initiatives often utilize hospital pharmacies for drug distribution. High patient inflow in hospitals reinforces dominance. Centralized supply chains ensure consistent availability. Clinical guidelines recommend hospital-based drug dispensing. Hospital pharmacies provide professional guidance on therapy adherence. The segment benefits from structured inventory and quality control. Partnerships between manufacturers and hospitals strengthen supply. The segment’s high revenue is sustained by critical care demand and comprehensive drug access.

The Online Pharmacy segment is expected to witness the fastest CAGR of 12.8% from 2026 to 2033, driven by increasing adoption of e-commerce for healthcare products and home delivery of medications. Online platforms offer convenience, competitive pricing, and broader geographic reach. Patient awareness campaigns encourage home-based therapy adherence. Telemedicine integration supports prescription fulfillment. Digital pharmacies are expanding services in endemic regions. Online delivery reduces travel and waiting times for patients. Increased smartphone penetration boosts adoption. Marketing campaigns by online pharmacy providers drive consumer engagement. Expansion of secure payment systems facilitates transactions. Partnerships with healthcare providers improve prescription accuracy. Overall, growth is fueled by convenience, affordability, and technology-driven access.

Metagonimiasis Treatment Market Regional Analysis

- North America dominated the metagonimiasis treatment market with the largest revenue share of 41.2% in 2025

- Supported by advanced healthcare infrastructure, high awareness of parasitic infections, and the presence of leading pharmaceutical companies specializing in infectious disease treatments

- The U.S. accounted for the majority of treated cases due to early diagnosis and adoption of innovative therapies

U.S. Metagonimiasis Treatment Market Insight

The U.S. metagonimiasis treatment market captured the largest revenue share within North America in 2025, driven by increased awareness of parasitic infections, availability of advanced therapeutic options, and strong clinical infrastructure. Rapid adoption of innovative treatment approaches, including combination therapies and newer anthelminthics, is propelling the market. Additionally, robust research and clinical trials in leading hospitals and specialty centers further support market expansion.

Europe Metagonimiasis Treatment Market Insight

The Europe metagonimiasis treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing focus on infectious disease control, rising public health awareness, and well-established healthcare systems. Countries such as Germany, France, and the U.K. are witnessing growth due to government initiatives, growing healthcare expenditure, and the adoption of advanced therapeutics.

U.K. Metagonimiasis Treatment Market Insight

The U.K. metagonimiasis treatment market is expected to grow steadily, driven by rising awareness about parasitic infections, government health campaigns, and the presence of specialized infectious disease treatment centers. Growing diagnostic capabilities and easy access to medications are also supporting market growth.

Germany Metagonimiasis Treatment Market Insight

The Germany metagonimiasis treatment market is projected to expand at a considerable CAGR, fueled by advanced healthcare infrastructure, strong focus on infectious disease research, and increasing adoption of innovative therapeutics in both hospital and clinic settings.

Asia-Pacific Metagonimiasis Treatment Market Insight

The Asia-Pacific metagonimiasis treatment market is poised to grow at the fastest CAGR of around 9.8% during the forecast period, driven by increasing healthcare investments, improving access to infectious disease services, rising awareness about Metagonimiasis, and expanding availability of treatment options in emerging economies such as China, India, and Southeast Asia.

Japan Metagonimiasis Treatment Market Insight

The Japan metagonimiasis treatment market is gaining momentum due to increasing awareness of parasitic infections, strong healthcare infrastructure, and high adoption of innovative therapies. Government initiatives promoting public health and preventive care are further supporting market growth.

China Metagonimiasis Treatment Market Insight

The China metagonimiasis treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising healthcare expenditure, growing awareness of parasitic infections, and availability of affordable treatment options. Expansion of healthcare facilities and increasing government initiatives for infectious disease control are key growth factors.

Metagonimiasis Treatment Market Share

The Metagonimiasis Treatment industry is primarily led by well-established companies, including:

• Gilead Sciences (U.S.)

• GlaxoSmithKline (U.K.)

• Janssen Pharmaceuticals (Belgium)

• Pfizer (U.S.)

• Bayer AG (Germany)

• Roche (Switzerland)

• Novartis (Switzerland)

• Sanofi (France)

• Astellas Pharma (Japan)

• Takeda Pharmaceutical (Japan)

• Cipla (India)

• Sun Pharmaceutical (India)

• Hikma Pharmaceuticals (U.K.)

• Merck & Co. (U.S.)

• AbbVie (U.S.)

Latest Developments in Global Metagonimiasis Treatment Market

- In March 2024, a review titled “Small intestinal flukes of the genus Metagonimus (Digenea: Heterophyidae) in Europe and the Middle East: a review of parasites with zoonotic potential” was published

- In August 2024, researchers reported “innovative molecular and immunological approaches” for diagnosis of heterophyid fluke infections (trematodes related to fish-borne fluke infections) in fish from Egyptian markets — pointing to improved detection methods in intermediate hosts

- In June 2025, a study published in a major journal provided “further evidence for plausible transmission of fishborne trematodiases in the United States,” showing that some game fish carry parasites capable of infecting humans and are consumed raw

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.