Global Manual Resuscitators Market

Market Size in USD Million

USD

689.25 Million

USD

1,229.27 Million

2024

2032

USD

689.25 Million

USD

1,229.27 Million

2024

2032

| 2025 - 2032 | |

| USD 689.25 Million | |

| USD 1,229.27 Million | |

| % | |

|

Manual Resuscitators Market Size

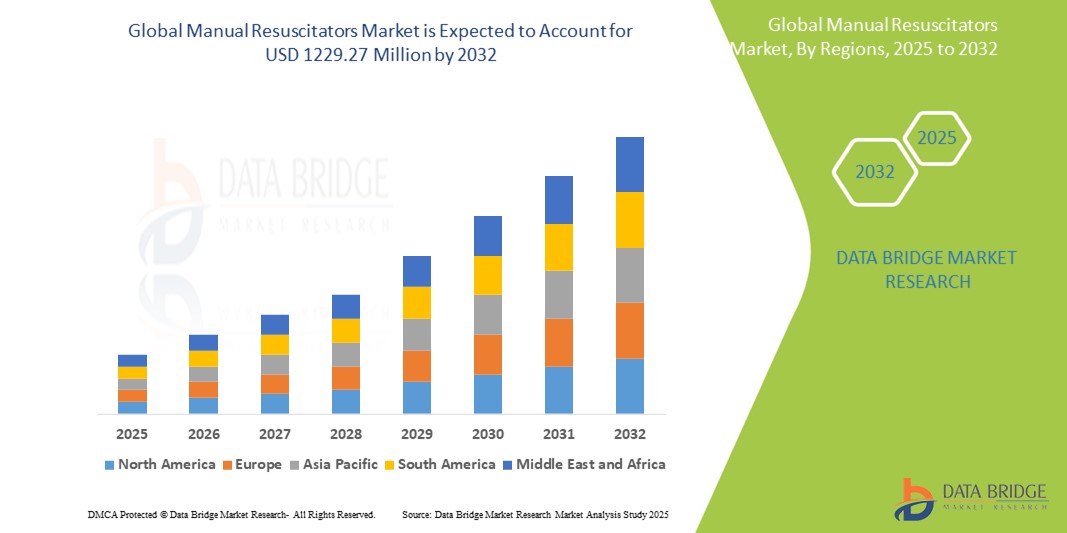

- The global manual resuscitators market size was valued at USD 689.25 million in 2024 and is expected to reach USD 1,229.27 million by 2032, at a CAGR of 7.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of respiratory disorders, rising incidences of cardiac arrest, and the expanding need for emergency care across healthcare facilities and pre-hospital settings

- Furthermore, growing awareness of basic life support techniques and advancements in resuscitator design such as improved portability, ergonomic handling, and disposable variants are reinforcing their adoption in both clinical and field environments. These converging factors are accelerating the uptake of manual resuscitator devices, thereby significantly boosting the industry's growth

Manual Resuscitators Market Analysis

- Manual resuscitators, also known as bag valve masks (BVMs), are essential handheld devices used to provide positive pressure ventilation to individuals who are not breathing or not breathing adequately, playing a critical role in emergency medical response, anesthesia delivery, and critical care settings across hospitals and pre-hospital environments

- The escalating demand for manual resuscitators is primarily fueled by the rising prevalence of respiratory diseases, increasing cases of cardiac arrest, and the growing need for effective emergency response systems in both developed and emerging healthcare infrastructures

- North America dominated the manual resuscitators market with the largest revenue share of 36.98% in 2024, characterized by the presence of advanced healthcare systems, high awareness of life-saving techniques, and a strong presence of established medical device manufacturers, particularly in the U.S., where public access defibrillation programs and CPR training have driven demand for portable resuscitation tools

- Asia-Pacific is expected to be the fastest growing region in the manual resuscitators market during the forecast period due to expanding healthcare access, increasing investments in emergency medical services, and heightened awareness of pre-hospital care

- Self-Inflating Resuscitator segment dominated the manual resuscitators market with a market share of 45.89% in 2024, driven by its widespread use in emergency care scenarios due to simplicity, ease of operation, and compatibility with both adult and pediatric patient care

Report Scope and Manual Resuscitators Market Segmentation

|

Attributes |

Manual Resuscitators Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Manual Resuscitators Market Trends

“Technological Advancements and Portability Enhancements in Emergency Care”

- A significant and accelerating trend in the global manual resuscitators market is the ongoing innovation aimed at improving device portability, usability, and patient safety, particularly in emergency and pre-hospital care settings. This trend is driven by increasing demand for more efficient and reliable resuscitation equipment during critical care and mass casualty situations

- For instance, Ambu’s SPUR II resuscitator is a widely adopted single-use solution designed with ergonomic features and integrated pressure relief valves to prevent lung over-inflation, thereby enhancing patient safety and minimizing complications during manual ventilation

- Advances in materials and compact design are also gaining traction. Modern resuscitators now feature lightweight silicone or PVC construction, foldable self-inflating bags for space-saving storage, and enhanced grip designs to support prolonged use by emergency responders. Devices such as Laerdal’s Bag Valve Mask (BVM) come with adjustable PEEP valves and oxygen reservoirs to optimize oxygen delivery, catering to both adult and pediatric patients

- Integration with monitoring systems and accessories is further elevating the utility of manual resuscitators. Some models now include built-in manometers and capnography ports, allowing real-time monitoring of ventilation pressure and patient CO₂ levels during resuscitation. These features are becoming essential in intensive care units and transport scenarios

- In addition, the rise in public training programs in CPR and first aid has driven demand for easy-to-use, color-coded resuscitators with standardized instructions, expanding the usability of these devices to trained non-medical personnel in public access settings

- This trend toward compact, ergonomic, and safety-focused manual resuscitator solutions is transforming the market landscape. Manufacturers such as Medline Industries and Smiths Medical are increasingly focusing on innovation and user-centric design, making manual resuscitators more accessible and effective in diverse healthcare environments.

- The demand for advanced manual resuscitators that combine usability with clinical precision is growing steadily across emergency services, hospitals, and ambulatory care, as global healthcare systems prioritize preparedness and rapid response capability

Manual Resuscitators Market Dynamics

Driver

“Rising Demand for Emergency Respiratory Support Across Diverse Healthcare Settings”

- The increasing global burden of respiratory disorders, cardiac arrests, and medical emergencies is a significant driver for the growing demand for manual resuscitators across both hospital and pre-hospital environments

- For instance, in February 2024, Intersurgical Ltd. introduced a new line of single-use resuscitator kits with integrated oxygen reservoirs and pressure-limiting valves, aiming to enhance safety in emergency respiratory care. These advancements align with the broader healthcare objective of improving resuscitation outcomes while minimizing infection risks

- As healthcare systems worldwide expand emergency medical services and improve critical care infrastructure, manual resuscitators serve as indispensable tools for immediate respiratory intervention, especially in out-of-hospital cardiac arrests, transport settings, and intensive care units

- In addition, the growing emphasis on training healthcare workers, paramedics, and even non-medical personnel in basic life support (BLS) and advanced cardiac life support (ACLS) has heightened awareness and usage of manual resuscitators. Many governments and healthcare organizations are investing in accessible and standardized resuscitation tools as part of broader emergency preparedness programs

- The versatility of manual resuscitators—usable across adult, pediatric, and neonatal patients—combined with their ease of use, disposability options, and cost-effectiveness, positions them as essential devices in both high-resource and resource-constrained settings

- Furthermore, increasing demand for infection control in healthcare environments post-pandemic has further propelled the use of single-use, sterile manual resuscitators, contributing to their adoption. The continuous development of ergonomic, compact, and feature-rich resuscitators is expected to sustain this momentum across the global market

Restraint/Challenge

“Risk of Improper Use and Limited Monitoring Capabilities”

- The potential for improper use of manual resuscitators, especially by inadequately trained personnel in emergency or high-stress situations, poses a significant challenge to market growth. As manual resuscitation depends heavily on user skill, inconsistent ventilation rates and pressures can lead to adverse patient outcomes such as lung injury or inadequate oxygenation

- For instance, clinical reports have highlighted cases where incorrect use of manual resuscitators resulted in complications such as barotrauma or gastric insufflation, raising concerns among healthcare providers about reliability and safety in emergency scenarios

- Addressing these concerns requires enhanced user training, improved device designs featuring pressure relief valves and visual feedback, and adoption of devices with integrated monitoring capabilities. While premium models from companies such as Ambu and Laerdal offer these features, their higher costs limit widespread availability, particularly in low-resource settings

- Furthermore, manual resuscitators generally lack continuous ventilation monitoring and automation found in mechanical ventilators, which restricts their use for prolonged respiratory support in intensive care or transport environments

- In addition, the increased shift towards single-use manual resuscitators to reduce infection risks post-pandemic leads to higher recurring costs and environmental concerns due to medical waste generation

- Overcoming these challenges through innovation, training, and cost-effective product offerings is critical for sustained adoption and market expansion across healthcare settings worldwide

Manual Resuscitators Market Scope

The market is segmented on the basis of product, modality, material, technology, patient type, application, end user, and distribution channel.

- By Product

On the basis of product, the manual resuscitators market is segmented into self-inflating resuscitators, flow-inflating resuscitators, and T-piece resuscitators. The self-inflating resuscator segment dominated the market with the largest revenue share of 45.89% in 2024, owing to its portability, ease of use without an external gas source, and widespread adoption in emergency and pre-hospital care settings.

The flow-inflating resuscitor segment is anticipated to witness the fastest growth rate during the forecast period, driven by increasing applications in neonatal care and anesthesia where precise ventilation control is crucial.

- By Modality

On the basis of modality, the market is segmented into disposable and reusable manual resuscitators. The reusable segment held the largest market share in 2024, favored for its cost-effectiveness and durability, especially in budget-conscious healthcare settings.

The disposable segment is expected to record the fastest growth during forecast period, propelled by heightened infection control concerns and the preference for hygienic single-use devices post-pandemic.

- By Material

On the basis of material, the market is segmented into silicon, PVC, and rubber. PVC-based manual resuscitators dominated the market in 2024 due to their affordability and widespread availability.

The silicon segment is projected to grow at the fastest CAGR during the forecast period, owing to its superior biocompatibility, durability, and increasing use in neonatal and pediatric resuscitation.

- By Technology

On the basis of technology, the market includes pop-off valve, PEEP valve, pneumatic, double wall, mask, and others. The pop-off valve segment dominated the market in 2024 as a critical safety feature preventing excess airway pressure during ventilation.

The PEEP valve segment is expected to witness the fastest growth during the forecast period, due to growing awareness of positive end-expiratory pressure benefits in critical care settings.

- By Patient Type

On the basis of patient type, the market is segmented into adult, paediatric, and infant resuscitators. The adult segment accounted for the largest revenue share in 2024, driven by the prevalence of respiratory emergencies in adult populations.

The infant segment is expected to experience the fastest growth rate during forecast period, fueled by increasing neonatal care initiatives and rising birth rates in developing regions.

- By Application

On the basis of application, the market includes COPD, cardiopulmonary arrest, anesthesia, asthma, and others. The cardiopulmonary arrest segment dominated the market in 2024, given the urgent need for manual ventilation during cardiac emergencies.

The anesthesia segment is forecasted to grow fastest during forecast period, reflecting increasing surgical procedures globally and reliance on manual resuscitators in anesthesia ventilation support.

- By End User

On the basis of end user, the market is segmented into hospitals, ambulatory surgical centers, military, specialized diagnostic centers, and emergency transport vehicles. Hospitals dominated the market in 2024 due to high patient inflow and comprehensive critical care services.

The emergency transport vehicle segment is projected to grow at the fastest rate during the forecast period, driven by expanding emergency medical services and trauma care worldwide.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tenders, retail sales, and online sales. Direct tenders held the largest market share in 2024, primarily due to institutional bulk purchases by healthcare facilities.

Online sales are expected to witness the fastest growth in 2025 to 2032, supported by rising e-commerce adoption and easier access to medical devices in emerging markets.

Manual Resuscitators Market Regional Analysis

- North America dominated the manual resuscitators market with the largest revenue share of 36.98% in 2024, driven by the presence of advanced healthcare systems, high awareness of life-saving techniques, and a strong presence of established medical device manufacturers

- The region benefits from increased healthcare spending, well-established hospital networks, and a strong presence of key manufacturers offering both disposable and reusable resuscitators tailored for varied clinical needs

- In addition, the growing number of surgeries and the emphasis on preparedness for critical care and trauma response across hospitals and emergency transport systems support sustained demand, reinforcing North America’s leadership in the global manual resuscitators market

U.S. Manual Resuscitators Market Insight

The U.S. manual resuscitators market captured the largest revenue share of 82% in 2024 within North America, driven by a well-established emergency care infrastructure and high adoption of advanced respiratory care devices. The prevalence of chronic respiratory diseases and rising surgical procedures necessitate efficient ventilation support, boosting demand. In addition, the presence of leading manufacturers and a strong emphasis on preparedness for emergency medical services support robust market penetration across hospitals and EMS units.

Europe Manual Resuscitators Market Insight

The Europe manual resuscitators market is projected to grow at a steady CAGR during the forecast period, fueled by aging populations and increasing rates of respiratory illnesses. Stringent healthcare regulations and rising investments in public health systems are driving the demand for reliable resuscitation devices. The market also benefits from widespread training programs for emergency responders and the integration of disposable manual resuscitators in infection control protocols across healthcare settings.

U.K. Manual Resuscitators Market Insight

The U.K. manual resuscitators market is expected to witness significant growth, driven by the rising incidence of cardiopulmonary conditions and increased focus on emergency response systems. Government-backed healthcare initiatives, combined with efforts to modernize ambulance and hospital equipment, are encouraging the adoption of both reusable and disposable manual resuscitators. Moreover, training of medical staff and first responders in basic life support is enhancing market demand.

Germany Manual Resuscitators Market Insight

The Germany manual resuscitators market is poised for notable growth, supported by the country's highly developed healthcare system and emphasis on medical device innovation. Strong clinical protocols for resuscitation and increased adoption of automated monitoring systems are encouraging healthcare providers to upgrade manual ventilation tools. The demand for silicon-based and ergonomic resuscitators is rising due to their durability, safety, and patient comfort features.

Asia-Pacific Manual Resuscitators Market Insight

The Asia-Pacific manual resuscitators market is set to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by expanding healthcare access and infrastructure across emerging economies such as China, India, and Indonesia. Rising awareness of emergency care, along with government initiatives to improve critical care services, is boosting adoption. The growing focus on low-cost, high-quality resuscitation devices is further propelling regional market expansion.

Japan Manual Resuscitators Market Insight

The Japan manual resuscitators market is advancing steadily due to a mature healthcare system and strong emphasis on patient safety. The market is driven by the increasing elderly population, higher surgical volumes, and the integration of advanced medical technologies in hospitals. Demand is particularly growing for compact and disposable resuscitators, especially in emergency kits and ambulatory settings, reflecting a preference for hygiene and ease of use.

India Manual Resuscitators Market Insight

The India manual resuscitators market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to the country’s rapidly expanding healthcare infrastructure and rising respiratory disease burden. Increased investment in emergency and trauma care centers, coupled with government support for primary healthcare, is enhancing access to life-saving ventilation equipment. Local manufacturing capabilities and growing awareness are further supporting market growth across urban and rural regions.

Manual Resuscitators Market Share

The Manual Resuscitators industry is primarily led by well-established companies, including:

- Ambu A/S (Denmark)

- Laerdal Medical (Norway)

- Medtronic (Ireland)

- Teleflex Incorporated. (U.S.)

- Medline Industries, Inc. (U.S.)

- WEINMANN Emergency Medical Technology GmbH + Co. KG (Germany)

- Allied Healthcare Products, Inc. (U.S.)

- Hopkins Medical Products (U.S.)

- HUM GmbH (Germany)

- Besmed Health Business Corp. (Taiwan)

- Shining World Health Care Co., Ltd. (Taiwan)

- GaleMed Corporation (Taiwan)

- Me.Ber. srl (Italy)

- BLS Systems Limited (Canada)

- Ventlab Corporation (U.S.)

- Cardinal Health, Inc. (U.S.)

- Drägerwerk AG & Co. KGaA (Germany)

- Fisher & Paykel Healthcare Corporation Limited (New Zealand)

What are the Recent Developments in Global Manual Resuscitators Market?

- In January 2023, Ambu A/S, a Danish medical device company, announced the upcoming launch of the Ambu Bag Auto A300, an automated manual resuscitator designed for use by untrained staff. This device aims to provide consistent and accurate ventilation without requiring extensive handling training, enhancing emergency response capabilities in various healthcare settings

- In March 2023, Medtronic, a global leader in healthcare technology, introduced the Oxylator LP, a new manual resuscitator designed for user convenience and minimal maintenance. This device is particularly suited for homecare solutions, offering an efficient option for patients requiring respiratory support outside traditional clinical environments

- In February 2023, Fisher & Paykel Healthcare, a New Zealand-based company specializing in respiratory care products, announced the forthcoming release of the AirLife Traveller, a portable manual resuscitator. Its lightweight design facilitates easy transportation, making it an ideal choice for ambulances and mobile healthcare providers

- In May 2023, Mercury Medical secured a group purchasing agreement with Premier, Inc. for its Neo-Tee® Disposable Infant T-Piece Resuscitators. This agreement allows Premier members to access specially negotiated pricing and terms for respiratory therapy products, enhancing the availability of advanced neonatal resuscitation devices across healthcare facilities.

- In April 2022, Dynarex Corporation, a prominent producer of medical equipment, launched the Dynarex Resp-O2, an innovative collection of respiratory treatment supplies. This product line aims to provide superior respiratory care solutions, addressing the growing demand for effective resuscitation equipment in various medical settings

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.