Global Linear Particle Accelerators Market

Market Size in USD Billion

CAGR :

%

USD

3.09 Billion

USD

4.83 Billion

2025

2033

USD

3.09 Billion

USD

4.83 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.09 Billion | |

| USD 4.83 Billion | |

| % | |

|

Linear Particle Accelerators Market Size

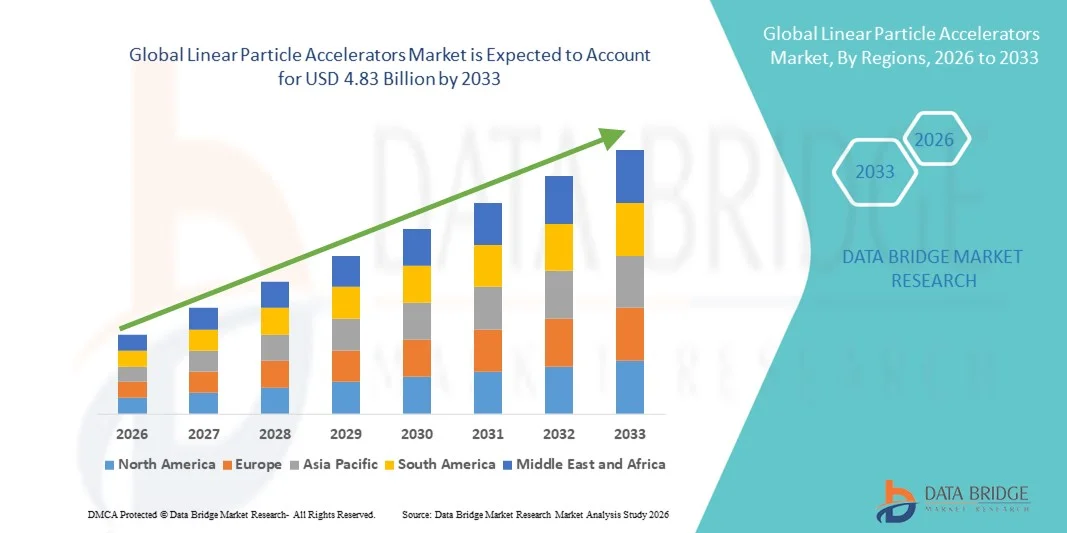

- The global linear particle accelerators market size was valued at USD 3.09 billion in 2025 and is expected to reach USD 4.83 billion by 2033, at a CAGR of 5.76% during the forecast period

- The market growth is largely fueled by the rising adoption of advanced cancer treatment technologies and continuous technological progress in linear particle accelerators, leading to increased deployment across hospitals, radiotherapy centers, and research institutions. Ongoing innovations such as AI-enabled treatment planning, enhanced beam precision, and compact system designs are accelerating digitalization and efficiency in both clinical and research environments

- Furthermore, growing demand for precise, effective, and minimally invasive radiation therapy solutions is establishing linear particle accelerators as the preferred technology for modern oncology treatment and high-energy research applications. These converging factors — including increasing cancer prevalence, expanding healthcare infrastructure, and rising investments in medical technology — are significantly accelerating the uptake of Linear Particle Accelerators solutions, thereby boosting overall market growth

Linear Particle Accelerators Market Analysis

- Linear particle accelerators high‑precision machines that accelerate charged particles in a straight line — are increasingly vital across medical, industrial, and scientific research applications due to their ability to support advanced cancer treatments (e.g., radiation therapy), materials analysis, security screening, and non‑destructive testing. Their precision, versatility, and ongoing technological innovation make them indispensable components of modern healthcare and research infrastructure

- The escalating demand for linear particle accelerators is primarily fueled by the widespread adoption of advanced radiation therapy in oncology, growth in scientific research initiatives, expanding industrial uses, and rising investments in healthcare and high‑tech manufacturing sectors. Rapid technological progress — including AI‑enhanced treatment planning, compact designs, and improved beam control — is making these systems more efficient and accessible, significantly boosting industry growth

- North America dominated the linear particle accelerators market with the largest revenue share of approximately 34.2% in 2025, supported by a well‑established healthcare system, high cancer treatment demand, strong research funding, and the presence of major manufacturers and innovation hubs. The U.S. is a key contributor, benefiting from robust R&D investment and supportive reimbursement frameworks that drive the adoption of new linac technologies

- Asia‑Pacific is expected to be the fastest‑growing region in the linear particle accelerators market during the forecast period, with rapid expansion driven by increasing healthcare expenditure, rising incidence of cancer, growing research infrastructure, and expanding industrial applications in countries such as China and India

- The Radiation Therapy segment dominated the largest market revenue share of 61.4% in 2025, driven by its widespread use as a primary cancer treatment modality across multiple cancer types

Report Scope and Linear Particle Accelerators Market Segmentation

|

Attributes |

Linear Particle Accelerators Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Linear Particle Accelerators Market Trends

Advancements in Precision Radiation Therapy and Research Applications

- A significant and accelerating trend in the global linear particle accelerators market is the growing adoption of advanced accelerator systems in medical, research, and industrial applications, particularly for high-precision radiation therapy and particle physics research

- For instance, linear particle accelerators are increasingly utilized in modern radiotherapy centers to deliver highly targeted radiation doses for cancer treatment, improving tumor control while minimizing damage to surrounding healthy tissues

- Technological advancements such as improved beam control, enhanced imaging integration, and compact system designs are enabling greater accuracy, operational efficiency, and patient safety

- The increasing use of linear accelerators in academic and government research institutions for nuclear physics, materials science, and radiation-based experiments is further expanding market scope

- Continuous innovation in accelerator components, including radiofrequency systems and beam delivery technologies, is supporting the development of next-generation linear accelerators with improved performance and reliability

- This trend toward more precise, efficient, and application-specific linear accelerator systems is reshaping expectations across healthcare and research sectors, driving sustained demand globally

- As a result, manufacturers are focusing on developing versatile linear particle accelerator platforms that can support multiple clinical and research applications while maintaining high safety and performance standards

Linear Particle Accelerators Market Dynamics

Driver

Rising Cancer Incidence and Expanding Scientific Research Infrastructure

- The increasing global incidence of cancer, coupled with the growing need for advanced and precise radiotherapy solutions, is a major driver of demand for linear particle accelerators

- For instance, in April 2025, Varian Medical Systems announced the introduction of an advanced medical linear accelerator designed to enhance treatment precision and workflow efficiency in oncology centers, supporting improved patient outcomes

- As healthcare providers seek to improve cancer treatment effectiveness, linear accelerators offer advantages such as precise dose delivery, reduced treatment times, and adaptability to complex tumor geometries

- Beyond healthcare, expanding investments in scientific research infrastructure are driving the adoption of linear accelerators for particle physics, materials analysis, and radiation-based testing applications

- Government funding, academic research programs, and public–private partnerships are accelerating the installation of linear accelerators in research laboratories and universities

- In addition, the expansion of healthcare infrastructure in emerging economies and increased access to advanced cancer treatment facilities are further propelling market growth

Restraint/Challenge

High Capital Costs and Technical Complexity

- The high initial capital investment required for purchasing, installing, and commissioning linear particle accelerators presents a significant challenge to market growth, particularly for small hospitals and research facilities

- For instance, several regional healthcare providers in developing countries have delayed the adoption of linear accelerators due to the high costs associated with system procurement, facility shielding, and installation requirements

- Linear particle accelerators also require skilled personnel for operation, calibration, and maintenance, increasing operational costs and limiting adoption in regions with a shortage of trained professionals

- Strict regulatory requirements and safety standards governing radiation equipment further add to the time and cost associated with system deployment

- Ongoing maintenance, software upgrades, and component replacement contribute to long-term ownership costs, which can be a barrier for budget-constrained institutions

- Overcoming these challenges through cost-effective system designs, financing and leasing models, and expanded training programs will be essential for broader market adoption and sustained growth

Linear Particle Accelerators Market Scope

The market is segmented on the basis of type, product, component, therapy, method, application, and end user

- By Type

On the basis of type, the Linear Particle Accelerators market is segmented into Low-energy Machine, Medium-energy Machine, and High-energy Machine. The High-energy Machine segment dominated the largest market revenue share of 45.6% in 2025, driven by its extensive use in advanced cancer treatment and complex radiation therapy procedures. High-energy linear accelerators are capable of delivering precise, deep-tissue radiation doses, making them suitable for treating large and deep-seated tumors. These machines are widely adopted in tertiary hospitals and specialized oncology centers due to their superior treatment accuracy and ability to minimize damage to surrounding healthy tissues. Increasing prevalence of cancer globally, particularly prostate, lung, and colorectal cancers, continues to drive demand. The segment also benefits from continuous technological upgrades, including intensity-modulated radiation therapy (IMRT) and image-guided radiation therapy (IGRT). High installation base in developed healthcare systems further supports dominance. In addition, strong reimbursement frameworks in North America and Europe encourage adoption. Overall, high-energy machines remain the backbone of modern radiation oncology infrastructure.

The Medium-energy Machine segment is anticipated to witness the fastest growth rate of 22.4% CAGR from 2026 to 2033, fueled by rising adoption in mid-sized hospitals and regional cancer treatment centers. These machines offer a balance between performance, cost, and clinical versatility, making them suitable for a wide range of cancer treatments. Increasing healthcare investments in emerging economies are driving demand for cost-effective yet technologically advanced radiation therapy solutions. Medium-energy accelerators are easier to install and maintain compared to high-energy systems, which appeals to facilities with limited infrastructure. Technological advancements enabling enhanced dose precision and reduced treatment times further support growth. Growing government initiatives to expand cancer care access also favor this segment. In addition, rising preference for decentralized cancer treatment facilities contributes to adoption. As a result, medium-energy machines are expected to experience rapid expansion during the forecast period.

- By Product

On the basis of product, the Linear Particle Accelerators market is segmented into X-Ray, Electron, Proton, Ion Beam, and Others. The X-Ray segment accounted for the largest market revenue share of 48.1% in 2025, driven by its widespread use in conventional and advanced radiation therapy applications. X-ray linear accelerators are commonly used due to their effectiveness in treating a broad range of cancers and their compatibility with existing radiotherapy infrastructure. The segment benefits from high clinical familiarity among oncologists and established treatment protocols. Continuous improvements in beam modulation and imaging integration enhance treatment precision and patient safety. X-ray systems are also relatively cost-effective compared to proton and ion beam systems, supporting broader adoption. Strong demand from hospitals and cancer centers further reinforces dominance. In addition, reimbursement support for X-ray-based therapies contributes to sustained usage. The extensive global installed base ensures continued revenue generation.

The Proton segment is expected to witness the fastest CAGR of 24.6% from 2026 to 2033, driven by growing demand for highly targeted cancer treatments with minimal side effects. Proton therapy offers superior dose distribution, reducing radiation exposure to surrounding healthy tissues. Rising adoption in pediatric oncology and complex tumor cases is accelerating growth. Increasing investments in proton therapy centers, particularly in North America and Asia-Pacific, support market expansion. Technological advancements are reducing system size and operational costs, making proton therapy more accessible. Growing clinical evidence supporting improved outcomes further boosts adoption. In addition, expanding insurance coverage for proton therapy in select regions enhances market potential.

- By Component

On the basis of component, the Linear Particle Accelerators market is segmented into Robotized Positioned Table and Integrated CT Scanner. The Integrated CT Scanner segment dominated the largest market revenue share of 52.3% in 2025, driven by its critical role in real-time imaging and precise tumor localization during radiation therapy. Integration of CT scanners enables accurate treatment planning and improved patient positioning, enhancing overall treatment outcomes. The increasing adoption of image-guided radiation therapy strongly supports demand. Hospitals and cancer centers prefer integrated systems to streamline workflows and reduce treatment errors. Continuous technological upgrades improve imaging resolution and reduce scan times. Rising emphasis on precision oncology further strengthens adoption. In addition, integrated systems reduce the need for separate imaging devices, lowering operational complexity. This segment remains essential for advanced radiotherapy solutions.

The Robotized Positioned Table segment is projected to grow at the fastest CAGR of 21.1% from 2026 to 2033, driven by increasing demand for automation and enhanced patient positioning accuracy. These systems improve treatment precision by enabling multi-axis movement and real-time adjustments. Growing adoption of stereotactic and high-precision radiation therapies supports growth. Automation reduces setup time and improves patient comfort. Rising investments in smart radiotherapy infrastructure further fuel adoption. As precision requirements increase, robotized positioning solutions are expected to gain significant traction.

- By Therapy

On the basis of therapy, the Linear Particle Accelerators market is segmented into Radio Surgery and Radiation Therapy. The Radiation Therapy segment dominated the largest market revenue share of 61.4% in 2025, driven by its widespread use as a primary cancer treatment modality across multiple cancer types. Radiation therapy is commonly used either as a standalone treatment or in combination with surgery and chemotherapy, enhancing overall treatment effectiveness. Continuous advancements in dose delivery techniques such as IMRT and IGRT have significantly improved treatment precision while reducing damage to surrounding healthy tissues. The increasing global burden of cancer, particularly breast, lung, and colorectal cancers, continues to support sustained demand. Strong clinical acceptance among oncologists and standardized treatment protocols further reinforce dominance. In addition, favorable reimbursement frameworks in developed healthcare systems encourage widespread adoption. The availability of advanced radiation therapy infrastructure in hospitals also supports growth. Rising investments in oncology departments globally further strengthen the segment’s leadership position.

The Radio Surgery segment is expected to witness the fastest CAGR of 23.0% from 2026 to 2033, driven by the increasing preference for non-invasive, high-precision cancer treatment options. Radiosurgery enables delivery of highly focused radiation doses with sub-millimeter accuracy, minimizing exposure to surrounding healthy tissues. Growing adoption in the treatment of brain tumors, spine tumors, and functional neurological disorders supports rapid growth. Technological advancements such as stereotactic radiosurgery and real-time imaging integration further enhance treatment outcomes. Increasing demand for outpatient and shorter-duration treatment procedures boosts adoption. Rising awareness among patients regarding minimally invasive therapies also contributes to expansion. Expanding availability of radiosurgery-capable linear accelerators in specialized centers supports market growth. As precision oncology gains traction, radiosurgery is expected to witness accelerated adoption globally.

- By Method

On the basis of method, the Linear Particle Accelerators market is segmented into Dedicated and Non-Dedicated. The Dedicated segment held the largest market revenue share of 54.7% in 2025, driven by its optimized design for specific treatment protocols and superior operational efficiency. Dedicated systems are engineered to deliver consistent performance for defined radiotherapy applications, ensuring high treatment accuracy. These systems are widely deployed in high-volume oncology centers and tertiary hospitals managing complex cancer cases. Dedicated accelerators support streamlined workflows, reducing treatment time and improving patient throughput. The ability to integrate advanced imaging and motion management technologies further enhances their clinical value. Strong demand from specialized cancer hospitals and academic medical centers supports dominance. In addition, reliable performance and long-term operational stability make dedicated systems a preferred investment. Growing emphasis on precision treatment reinforces sustained adoption of dedicated linear accelerators.

The Non-Dedicated segment is anticipated to grow at the fastest CAGR of 20.8% from 2026 to 2033, driven by flexibility, cost advantages, and multi-purpose usability. These systems are capable of supporting multiple treatment applications, making them attractive to small and mid-sized hospitals. Lower installation and operational costs further encourage adoption, particularly in emerging markets. Increasing healthcare investments in developing regions support deployment of versatile radiotherapy solutions. Non-dedicated systems enable facilities to expand oncology services without large capital expenditure. Growing demand for decentralized cancer care also supports growth. Technological improvements are enhancing the performance capabilities of non-dedicated accelerators. As access to cancer treatment expands globally, this segment is expected to grow rapidly.

- By Application

On the basis of application, the Linear Particle Accelerators market is segmented into Prostate Cancer, Breast Cancer, Lung Cancer, Head and Neck Cancers, Colorectal Cancers, and Others. The Breast Cancer segment accounted for the largest market revenue share of 29.3% in 2025, driven by the high global incidence of breast cancer and the widespread use of radiation therapy as a standard treatment option. Radiation therapy is commonly administered post-surgery to reduce recurrence risk, supporting consistent treatment volumes. Early detection and screening programs significantly increase the number of patients requiring radiotherapy. Advancements in targeted radiation techniques improve clinical outcomes and patient safety. Strong awareness initiatives and government-supported screening programs further drive adoption. Favorable reimbursement policies also support treatment accessibility. Hospitals and cancer centers prioritize breast cancer radiotherapy infrastructure due to high patient volumes. These factors collectively contribute to the segment’s dominant market position.

The Prostate Cancer segment is expected to witness the fastest CAGR of 22.7% from 2026 to 2033, driven by the rising incidence of prostate cancer among aging male populations worldwide. Increasing preference for non-surgical and minimally invasive treatment options supports adoption of radiation therapy. Technological advancements enabling precise dose delivery reduce side effects and improve patient outcomes. Growing awareness about early diagnosis and treatment further fuels demand. Expanding access to advanced cancer care facilities in emerging markets supports growth. In addition, the integration of image-guided and stereotactic techniques enhances treatment effectiveness. Favorable clinical outcomes and patient convenience drive preference for radiotherapy. As prostate cancer prevalence continues to rise, this segment is expected to expand rapidly.

- By End User

On the basis of end user, the Linear Particle Accelerators market is segmented into Radiology Clinics, Hospitals, and Other End Users. The Hospitals segment dominated the largest market revenue share of 58.9% in 2025, driven by the availability of advanced oncology infrastructure and comprehensive cancer care services. Hospitals manage high patient volumes and complex cancer cases requiring multidisciplinary treatment approaches. The presence of specialized oncology departments supports widespread deployment of linear accelerators. Strong investments in radiotherapy equipment and technology upgrades further reinforce dominance. Hospitals also benefit from established reimbursement mechanisms and skilled medical professionals. Integration of imaging, diagnostics, and treatment within hospital settings enhances clinical efficiency. Growing government and private funding for hospital-based cancer care supports sustained adoption. As primary cancer treatment centers, hospitals continue to lead market demand.

The Radiology Clinics segment is projected to grow at the fastest CAGR of 21.5% from 2026 to 2033, driven by the increasing shift toward outpatient cancer treatment and decentralized healthcare delivery. Clinics offer cost-effective and accessible radiotherapy services, reducing patient burden. Growing private investment in diagnostic and treatment centers supports rapid expansion. Shorter waiting times and patient convenience further drive preference for clinic-based treatment. Clinics increasingly adopt advanced linear accelerators to expand service offerings. Rising demand for outpatient radiotherapy procedures supports growth. Expanding insurance coverage for clinic-based treatments also contributes to adoption. As healthcare systems evolve, radiology clinics are expected to play a growing role in cancer treatment delivery.

Linear Particle Accelerators Market Regional Analysis

- North America dominated the linear particle accelerators market with the largest revenue share of approximately 34.2% in 2025, supported by a well-established healthcare infrastructure, high demand for advanced cancer treatment solutions, strong government and private research funding, and the presence of major manufacturers and innovation hubs

- The region benefits from widespread adoption of advanced radiotherapy technologies across hospitals and cancer treatment centers, where linear particle accelerators are extensively used for precision radiation therapy

- High healthcare expenditure, favorable reimbursement frameworks, and strong collaboration between research institutions and industry players continue to support sustained demand for linear particle accelerators in both clinical and research applications

U.S. Linear Particle Accelerators Market Insight

The U.S. linear particle accelerators market captured the largest revenue share in 2025 within North America, driven by high cancer prevalence, early adoption of advanced radiation therapy technologies, and substantial investments in healthcare infrastructure. The country’s strong focus on research and development, supported by government funding agencies and academic institutions, accelerates innovation in linac design and performance. In addition, the presence of leading manufacturers and a large installed base of radiotherapy systems continue to propel market expansion across hospitals, specialty cancer centers, and research laboratories.

Europe Linear Particle Accelerators Market Insight

The Europe linear particle accelerators market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising cancer incidence, increasing demand for precise and efficient radiotherapy solutions, and strong public healthcare systems. Government initiatives aimed at modernizing oncology infrastructure and expanding access to advanced cancer treatment are supporting market growth. The region is also witnessing increased deployment of linear particle accelerators in academic and government research institutions for nuclear physics and materials science applications.

U.K. Linear Particle Accelerators Market Insight

The U.K. linear particle accelerators market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by the modernization of National Health Service (NHS) oncology facilities and increasing investment in advanced radiation therapy technologies. Growing awareness of early cancer diagnosis and the need for precise treatment delivery are encouraging the adoption of next-generation linear accelerators. In addition, ongoing research activities and collaborations between universities and healthcare providers are contributing to market development.

Germany Linear Particle Accelerators Market Insight

The Germany linear particle accelerators market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, technological innovation, and a high focus on research and development. Germany’s leadership in medical technology manufacturing and its emphasis on precision medicine are driving the adoption of advanced linear particle accelerators across hospitals and research centers. The country also benefits from increased government funding for scientific research and radiation-based applications.

Asia-Pacific Linear Particle Accelerators Market Insight

The Asia-Pacific linear particle accelerators market is expected to be the fastest-growing region during the forecast period, driven by rising healthcare expenditure, increasing cancer prevalence, and rapid expansion of healthcare infrastructure in countries such as China, India, and Japan. Growing investments in oncology centers, coupled with expanding research capabilities and industrial applications of particle accelerators, are accelerating market growth. The region is also benefiting from government initiatives aimed at improving access to advanced cancer treatment technologies.

Japan Linear Particle Accelerators Market Insight

The Japan linear particle accelerators market is gaining steady momentum due to the country’s advanced healthcare system, strong focus on precision medicine, and increasing demand for high-quality cancer treatment. Japan’s emphasis on technological innovation and research excellence supports the adoption of advanced linear accelerators in both clinical and scientific research settings. In addition, the aging population is increasing demand for effective and precise radiotherapy solutions, further supporting market growth.

China Linear Particle Accelerators Market Insight

The China linear particle accelerators market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid expansion of healthcare infrastructure, rising cancer incidence, and strong government investment in medical technology and research facilities. China’s focus on developing domestic manufacturing capabilities and expanding access to advanced oncology treatment is accelerating the installation of linear particle accelerators across hospitals and research institutes. The country’s push toward strengthening scientific research and industrial applications of accelerator technologies further contributes to sustained market growth.

Linear Particle Accelerators Market Share

The Linear Particle Accelerators industry is primarily led by well-established companies, including:

- Varian Medical Systems (U.S.)

- Elekta AB (Sweden)

- Accuray Incorporated (U.S.)

- Siemens Healthineers (Germany)

- Hitachi, Ltd. (Japan)

- Mitsubishi Heavy Industries (Japan)

- Toshiba Energy Systems & Solutions (Japan)

- IBA (Ion Beam Applications) (Belgium)

- Shinva Medical Instrument Co., Ltd. (China)

- Canon Medical Systems Corporation (Japan)

- Sumitomo Heavy Industries (Japan)

- ViewRay Technologies (U.S.)

- Mevion Medical Systems (U.S.)

- Nordion (Canada)

- Research Instruments GmbH (Germany)

- Thales Group (France)

- Advanced Oncotherapy (U.K.)

- Sordina IORT Technologies (Italy)

- Danfysik (Denmark)

- General Electric Healthcare (U.S.)

Latest Developments in Global Linear Particle Accelerators Market

- In May 2024, Elekta AB, a leading medical technology and oncology equipment provider, announced the launch of its Elekta Evo AI-powered adaptive CT-Linear Accelerator (CT-Linac) at the Annual Congress of the European Society for Radiotherapy and Oncology (ESTRO 2024). The Elekta Evo system incorporates next-generation high-definition AI-enhanced imaging and online adaptive radiation therapy capabilities, enabling clinicians to tailor treatment plans in real time and improve targeting accuracy while minimizing healthy tissue exposure. This launch underscores Elekta’s commitment to advancing personalized and precise cancer care using cutting-edge machine learning and imaging technologies

- In June 2024, Leo Cancer Care, a UK-based radiotherapy innovation company, signed a strategic collaboration with TibaRay Inc. to co-develop a next-generation upright linear accelerator combining TibaRay’s advanced linac technology with Leo’s upright patient positioning and imaging system. The partnership aims to introduce an innovative photon therapy solution with rapid dose delivery and improved patient comfort, signaling a shift in radiotherapy design that could transform clinical workflows and expand patient access to advanced treatments

- In September 2024, Elekta’s AI-powered adaptive CT-Linac, Elekta Evo, received the CE mark certification for sale and marketing in Europe, making the technology commercially available in key oncology markets. The CE mark highlights regulatory approval for the Evo’s advanced adaptive and image-guided radiation therapy functions, enabling wider clinical deployment across European cancer centers

- In September 2025, IHH Healthcare expanded its collaboration with Leo Cancer Care to introduce upright radiotherapy solutions, including upright linear accelerators and enhanced particle therapy platforms, across its hospital network in Asia. This expansion reflects strengthening global partnerships aimed at advancing accessibility to innovative radiotherapy technologies and improving patient care outcomes in diverse healthcare systems

- In October 2025, Leo Cancer Care announced plans to integrate TibaRay’s advanced linear accelerators into its future “Grace” photon therapy platform. The integration is intended to explore higher dose rate delivery and new treatment paradigms such as FLASH radiotherapy, offering more compact, efficient, and potentially more effective treatment options in next-generation radiotherapy systems

- In December 2025, Elekta showcased its Elekta Evo AI-powered online adaptive CT-Linac at the Association of Medical Physicists of India (AMPICON) 2025 in Guwahati, marking a significant regional introduction of this advanced linear accelerator technology. The demonstration highlights Elekta’s efforts to expand access to adaptive radiation therapy in emerging markets and support precision oncology with real-time imaging and treatment adaptation for complex cancer cases

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.