Global Intravenous Iv Solutions Market

Market Size in USD Billion

CAGR :

%

USD

13.80 Billion

USD

22.49 Billion

2025

2033

USD

13.80 Billion

USD

22.49 Billion

2025

2033

| 2026 - 2033 | |

| USD 13.80 Billion | |

| USD 22.49 Billion | |

| % | |

|

Intravenous (IV) Solutions Market Overview

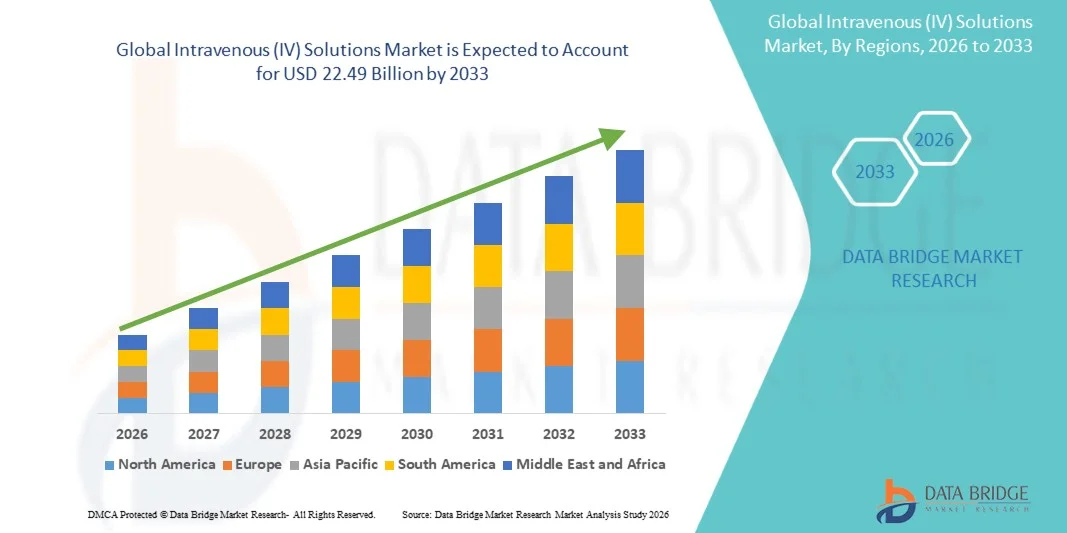

The Intravenous (IV) Solutions Market was valued at USD 13.80 billion in 2025 and is projected to reach USD 22.49 billion by 2033, growing at a CAGR of 6.30% from 2026 to 2033. The market is witnessing steady expansion driven by the rising prevalence of chronic diseases, increasing hospital admissions, and growing demand for clinical nutrition and fluid replacement therapies across both developed and emerging healthcare systems.

The expanding geriatric population, coupled with higher rates of dehydration, cancer, gastrointestinal disorders, and surgical procedures, is significantly boosting the demand for IV solutions in hospitals and ambulatory care settings. In addition, advancements in sterile manufacturing, ready-to-use formulations, and multi-chamber IV bags are improving safety, reducing contamination risks, and enhancing operational efficiency in critical care environments.

Key Market Trends & Insights

- North America dominated the Intravenous (IV) Solutions Market with the largest revenue share of 38.92% in 2025, supported by a well-established hospital infrastructure, high ICU admission rates, and strong presence of major IV therapy manufacturers.

- The Partial Parenteral Nutrition segment led the market with a 41.55% share in 2025, driven by its widespread use in routine hospital care, post-surgical recovery, and moderate malnutrition cases.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 10.21% from 2026 to 2033, fueled by rising healthcare expenditure, expanding hospital networks, and increasing prevalence of chronic diseases in countries such as India and China.

- Total Parenteral Nutrition are the fastest-growing type, projected to register a CAGR of 7.2%, reflecting the surge in rising ICU admissions and severe gastrointestinal disorders.

- The Saline segment dominated the solution category with a 38.42% revenue share in 2025, led by its universal application in hydration, resuscitation, and electrolyte balance management.

- Large Volume Bags accounted for 58.60% of the market, preferred by their extensive use in hydration therapy, electrolyte replacement, and emergency care.

- The Nutritional IV Solution segment is the fastest-growing application category, with a CAGR of 7.6%, driven by the rising cases of malnutrition and critical illness.

Market Size & Forecast

- Global Market Value (2025): USD 13.80 Billion

- Expected Market Value (2033): USD 22.49 Billion

- Forecast CAGR (2026–2033): 6.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Intravenous (IV) Solutions Market Segmentation

|

Attributes |

Intravenous (IV) Solutions Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Baxter (U.S.) · B. Braun SE (Germany) · Fresenius Kabi AG (Germany) · ICU Medical, Inc. (U.S.) · Terumo Corporation (Japan) · Otsuka Pharmaceutical Factory, Inc. (Japan) · Grifols S.A. (Spain) · Fresenius SE & Co. KGaA (Germany) · Hospira (U.S.) · Pfizer Inc. (U.S.) · Sichuan Kelun Pharmaceutical Co., Ltd. (China) · Shandong Hualu-Hengsheng Chemical Co., Ltd. (China) · Shanghai Changqiang Medical Industry Co., Ltd. (China) · JW Life Science (South Korea) · SSY Group Limited (Hong Kong) · NIPRO CORPORATION (Japan) · Vifor Pharma (Switzerland) · Amanta Healthcare Ltd. (India) · Well Lead Medical Co., Ltd. (China) · Renolit Healthcare (Germany) |

|

Market Opportunities |

· Expansion of home infusion therapy services · Rising adoption of ready-to-use and premixed IV formulations · Increasing demand for parenteral nutrition in aging populations and cancer care |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Intravenous (IV) Solutions Market Trends

Trend: Rising Demand for Ready-to-Use and Premixed IV Formulations

Healthcare systems are increasingly moving toward ready-to-administer IV solutions to reduce manual preparation steps, minimize contamination risks, and improve efficiency in emergency and intensive care settings. This shift is strongly supported by advances in sterile filling technologies, closed-system transfer devices, and multi-chamber IV bag designs that enhance drug stability and reduce dosing variability. Hospitals are also under pressure to improve patient throughput, which is accelerating the adoption of standardized infusion products that reduce preparation time and human error. For instance, large tertiary care hospitals are increasingly replacing manually compounded electrolyte and glucose solutions with premixed formulations to ensure faster administration in critical care units.

Intravenous (IV) Solutions Market Dynamics

Key Market Driver: Rising Burden of Chronic Diseases and Hospitalizations

The increasing global burden of chronic and acute medical conditions is a major driver for IV solutions demand, as these therapies are essential for hydration, medication delivery, and nutritional support in hospitalized patients. Conditions such as cancer, chronic kidney disease, gastrointestinal disorders, sepsis, and severe infections require frequent intravenous interventions, especially in intensive care and surgical settings. In addition, the aging global population is contributing to higher hospitalization rates and longer treatment durations, further increasing IV fluid consumption across healthcare systems. For instance, oncology patients undergoing chemotherapy and post-operative patients recovering from major surgeries often depend on repeated IV fluid therapy to maintain electrolyte balance and support recovery.

Key Restraint/Challenge: Risk of Contamination and Product Recall Concerns

One of the major challenges in the IV solutions market is the risk of microbial contamination during manufacturing, storage, or administration, which can lead to severe patient safety issues and regulatory scrutiny. Because IV solutions are directly introduced into the bloodstream, even minor contamination can result in serious complications, prompting strict compliance with Good Manufacturing Practices (GMP) and rigorous quality control standards. These requirements increase production costs and operational complexity for manufacturers, while also raising the risk of supply disruptions in case of product recalls. For instance, past recalls of contaminated saline or dextrose solutions have led to temporary shortages in hospitals, forcing healthcare providers to ration supplies or switch to alternative vendors during critical periods.

Key Market Opportunity: Expansion of Home Infusion and Ambulatory Care Services

The growing shift toward decentralized healthcare delivery is creating significant opportunities for IV solution providers in home infusion therapy and outpatient care models. Healthcare systems are increasingly seeking cost-effective alternatives to inpatient hospitalization, especially for long-term treatments such as antibiotic therapy, pain management, and parenteral nutrition. This shift is supported by advancements in portable infusion pumps, improved stability of IV formulations, and telehealth-based patient monitoring systems. For instance, patients requiring long-term intravenous antibiotic treatment for chronic infections are increasingly being treated at home under supervised infusion programs, reducing hospital stay durations and overall healthcare costs while improving patient comfort and compliance.

Intravenous (IV) Solutions Market Scope

The Intravenous (IV) solutions market is segmented on the basis of type, solution, bag type, demographic, application, end-users, and distribution channel.

- By Type

On the basis of type, the global IV solutions market is segmented into partial parenteral nutrition and total parenteral nutrition. The Partial Parenteral Nutrition segment dominated the market with a 42.45% share in 2025, owing to its widespread use in routine hospital care, post-surgical recovery, and moderate malnutrition cases. These solutions are widely used for patients who can still partially consume oral nutrition, reducing clinical complexity. They are preferred in general wards due to lower risk of metabolic complications and simpler monitoring requirements. High adoption across adult and geriatric populations strengthens its clinical utility. Cost-effectiveness and ease of administration further support large-scale deployment across healthcare facilities. Continuous demand from inpatient care settings reinforces its dominant position globally.

The Total Parenteral Nutrition segment is projected to register the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by rising ICU admissions and severe gastrointestinal disorders. These solutions are essential for patients who cannot tolerate any oral or enteral feeding, particularly in critical care settings. Increasing prevalence of cancer, Crohn’s disease, and severe trauma cases is significantly expanding patient demand. Advancements in infusion monitoring systems and nutrient formulation are improving safety and clinical outcomes. Expansion of intensive care infrastructure in emerging economies is further accelerating adoption. Growing focus on precision-based clinical nutrition is strongly supporting long-term growth.

- By Solution

On the basis of solution, the global IV solutions market is segmented into saline, dextran, lactated ringer’s, amino acid, vitamins and minerals, heparin and trace elements, and mixed solutions. The Saline segment dominated the market with a 38.42% share in 2025, owing to its universal application in hydration, resuscitation, and electrolyte balance management. It is widely used across emergency departments, surgical procedures, and routine inpatient care. Its low cost, high availability, and compatibility with most injectable drugs make it the most widely used IV fluid globally. Hospitals rely heavily on saline for both acute and maintenance therapy. Its standardized usage across clinical protocols ensures consistent demand. Strong penetration across all healthcare levels reinforces its dominant position.

The Amino Acid Solutions segment is expected to register the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by rising demand for nutritional and metabolic support therapies. These solutions are a core component of total parenteral nutrition in critically ill and malnourished patients. Increasing incidence of cancer, liver disorders, and post-operative complications is significantly boosting usage. Hospitals are increasingly adopting advanced clinical nutrition protocols to improve recovery outcomes. Continuous innovation in formulation is enabling patient-specific nutritional support. Growing awareness of clinical nutrition benefits is further accelerating global adoption.

- By Bag Type

On the basis of bag type, the global IV solutions market is segmented into large volume bags and small volume bags. The Large Volume Bags segment dominated the market with a 58.60% share in 2025, due to their extensive use in hydration therapy, electrolyte replacement, and emergency care. These bags are widely used in inpatient settings for continuous fluid administration. Their ability to deliver high fluid volumes makes them essential in trauma and surgical procedures. Hospitals prefer them due to cost efficiency and suitability for bulk usage. High patient inflow in emergency and ICU departments supports steady demand. Their widespread clinical applicability reinforces dominance across global healthcare systems.

The Small Volume Bags segment is projected to register the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by increasing demand for precise drug delivery and specialty treatments. These bags are widely used in chemotherapy, antibiotic infusion, and pediatric care. Their compact design reduces risk of fluid overload and improves dosing accuracy. Rising adoption in outpatient and ambulatory care settings is significantly supporting growth. Technological advancements in sterile packaging and drug compatibility are enhancing usability. Expansion of home healthcare services is further accelerating market adoption.

- By Demographic

On the basis of demographic, the global IV solutions market is segmented into adult, pediatric, and geriatric populations. The Adult segment dominated the market with a 55.60% share in 2025, due to high hospitalization rates, surgical procedures, and chronic disease burden. Adults represent the largest patient base requiring IV hydration, drug delivery, and nutritional support. Lifestyle-related disorders such as diabetes and cardiovascular diseases further increase IV usage. Hospitals allocate significant resources to adult care units, strengthening consumption levels. High incidence of trauma and emergency cases also contributes to demand. This makes adults the primary consumer base in global IV therapy.

The Geriatric segment is projected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by rapid global population aging. Elderly patients frequently require IV therapy for chronic illness management, dehydration, and malnutrition. Increased susceptibility to infections and recovery complications further drives usage. Expansion of geriatric care infrastructure is supporting specialized treatment delivery. Home-based IV therapy adoption is increasing among elderly populations. Rising life expectancy globally is a key structural driver of long-term growth.

- By Application

On the basis of application, the global IV solutions market is segmented into basic IV solution, nutritional IV solution, blood IV solution, drug IV solution, irrigation IV solution, and others. The Basic IV Solution segment dominated the market with a 40.45% share in 2025, due to its widespread use in hydration and electrolyte balance management. These solutions are essential in emergency care, surgical recovery, and general inpatient treatment. Their standardized formulations ensure consistent usage across hospital departments. High procedural volumes in hospitals drive continuous demand. They are frequently used alongside medications and other therapies. Their cost-effectiveness and universal applicability reinforce dominance.

The Nutritional IV Solution segment is expected to register the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by rising cases of malnutrition and critical illness. These solutions are widely used in total parenteral nutrition for patients unable to consume food orally. Increasing prevalence of cancer and gastrointestinal disorders is significantly driving demand. Hospitals are adopting advanced nutritional therapy protocols to improve patient outcomes. Innovation in nutrient formulations is expanding clinical applications. Growing awareness of clinical nutrition benefits is accelerating global adoption.

- By End-Users

On the basis of end-users, the global IV solutions market is segmented into clinics, hospitals, and others. The Hospital segment dominated the market with a 65.70% share in 2025, due to high patient inflow, advanced care infrastructure, and availability of critical care units. Hospitals handle the majority of surgeries, ICU admissions, and emergency treatments requiring IV therapy. Large-scale procurement systems ensure uninterrupted supply of IV solutions. Skilled healthcare professionals enable safe administration of complex therapies. Advanced procedures such as TPN and drug infusion are primarily hospital-based. Expansion of hospital networks globally reinforces dominance.

The Clinic segment is projected to register the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by the shift toward decentralized healthcare delivery. Increasing outpatient procedures are reducing dependence on hospital-based care. Clinics are increasingly adopting IV therapy for faster treatment turnaround. Home healthcare expansion is further supporting this shift. Technological advancements in portable infusion systems are enabling safe administration. Cost efficiency and patient convenience are major growth drivers.

- By Distribution Channel

On the basis of distribution channel, the global IV solutions market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the market with a 70.75% share in 2025, due to direct supply within inpatient treatment workflows. Most IV solutions are administered in hospitals, making internal procurement systems essential. Bulk purchasing agreements ensure cost efficiency and consistent availability. Integration with hospital protocols supports streamlined inventory management. Emergency and critical care reliance strengthens this channel’s dominance. Established institutional procurement systems further reinforce leadership.

The Online Pharmacy segment is projected to register the fastest growth at a CAGR of 8.0% from 2026 to 2033, driven by rapid healthcare digitization and rising homecare demand. E-pharmacy platforms are improving access to medical supplies for outpatient and chronic patients. Advancements in logistics and cold-chain infrastructure are enabling safe delivery of IV-related products. Telehealth expansion is further strengthening online procurement trends. Increasing digital penetration in emerging markets is accelerating adoption. Convenience, accessibility, and price transparency are key growth drivers.

Intravenous (IV) Solutions Market Regional Analysis

North America dominated the Intravenous (IV) Solutions Market with the largest revenue share of 38.92% in 2025, supported by a well-established hospital infrastructure, high ICU admission rates, and strong presence of major IV therapy manufacturers. The region benefits from widespread adoption of advanced infusion therapies, including total parenteral nutrition and critical care IV treatments across hospitals and specialty clinics. Strong reimbursement frameworks and high healthcare expenditure further support market dominance. Increasing prevalence of chronic diseases such as cancer, diabetes, and cardiovascular disorders continues to drive IV solution demand. Rapid expansion of ICU facilities and emergency care services also strengthens consumption across healthcare institutions. Continuous technological advancements in IV formulations and delivery systems further reinforce North America’s leadership position in the global market.

U.S. Intravenous (IV) Solutions Market Insight

The U.S. IV solutions market is witnessing strong growth due to rising hospital admissions, increasing prevalence of chronic diseases, and expanding demand for critical care and surgical procedures. The country’s advanced healthcare infrastructure, along with high adoption of evidence-based infusion therapies, is driving widespread usage of IV solutions across hospitals and specialty clinics. Strong presence of leading pharmaceutical and medical supply companies further strengthens product availability and innovation. Increasing use of total parenteral nutrition and targeted drug infusion therapies is supporting market expansion. Growing emphasis on improving patient outcomes and reducing hospital stay duration is accelerating adoption across healthcare facilities. In addition, continuous advancements in infusion technologies and clinical nutrition are reinforcing market growth.

Europe Intravenous (IV) Solutions Market Insight

The Europe IV solutions market remains a major contributor to global revenue, driven by well-established public healthcare systems, high hospital standards, and strong adoption of standardized infusion therapy protocols. Widespread use of IV solutions in surgical care, elderly care, and chronic disease management supports steady regional demand. Strong regulatory frameworks ensure safe and efficient use of IV therapies across healthcare institutions. Increasing aging population across major countries is further driving long-term infusion therapy requirements. Growing adoption of clinical nutrition and advanced IV formulations is supporting improved patient care outcomes. Continuous investment in healthcare infrastructure modernization further strengthens Europe’s position in the global market.

U.K. Intravenous (IV) Solutions Market Insight

The U.K. IV solutions market is experiencing steady growth, supported by strong public healthcare infrastructure and rising demand for hospital-based infusion therapies. Increasing cases of chronic illnesses and surgical procedures are driving consistent usage of IV fluids across clinical settings. Emphasis on cost-efficient healthcare delivery is encouraging standardized use of IV solutions in hospitals. Growing adoption of nutritional IV therapies and advanced drug infusion systems is further supporting market expansion. Integration of digital healthcare systems is improving supply chain efficiency and inventory management. Continuous focus on improving patient safety and treatment efficiency is strengthening market growth.

Germany Intravenous (IV) Solutions Market Insight

The Germany IV solutions market is expanding steadily due to strong hospital infrastructure, advanced medical research capabilities, and high adoption of innovative clinical therapies. Widespread use of IV solutions in intensive care, surgery, and chronic disease management ensures stable demand. Germany’s aging population is significantly increasing long-term infusion therapy requirements. Strong pharmaceutical manufacturing base supports consistent product availability and innovation. Increasing use of advanced nutritional and electrolyte solutions is improving clinical outcomes. Government focus on healthcare efficiency and patient safety continues to support structured market growth.

Asia-Pacific Intravenous (IV) Solutions Market Insight

The Asia-Pacific IV solutions market is expected to witness rapid growth, driven by expanding healthcare infrastructure, rising hospital admissions, and increasing burden of chronic diseases. Growing investments in healthcare systems across China, India, and Southeast Asia are significantly boosting demand. Rising awareness of clinical nutrition, hydration therapy, and emergency care is supporting market adoption. Increasing use of cost-effective generic IV solutions is improving accessibility across developing economies. Expansion of ICU facilities and emergency care centers is further accelerating demand. Continuous healthcare modernization and population growth are positioning Asia-Pacific as the fastest-growing region globally.

Japan Intravenous (IV) Solutions Market Insight

The Japan IV solutions market is witnessing steady growth due to a rapidly aging population and highly developed healthcare infrastructure. Increasing prevalence of chronic diseases and long-term hospitalization needs are driving consistent demand for IV therapies. Strong adoption of advanced clinical nutrition and infusion practices supports high-quality patient care. Hospitals are increasingly using IV solutions for elderly care and post-surgical recovery. Technological advancements in healthcare delivery systems are improving treatment efficiency. Continuous focus on patient safety and precision medicine is further strengthening market growth.

China Intravenous (IV) Solutions Market Insight

The China IV solutions market is growing rapidly due to expanding healthcare infrastructure, rising hospital capacity, and increasing burden of chronic and infectious diseases. Strong government investment in healthcare modernization is significantly boosting demand for IV therapies. Widespread use of IV solutions in emergency care, surgery, and intensive care supports strong market expansion. Increasing adoption of nutritional and drug infusion therapies is further driving growth. Rising awareness of clinical nutrition and improved healthcare access is enhancing utilization rates. Rapid urbanization and healthcare system upgrades are positioning China as one of the fastest-growing markets globally.

Intravenous (IV) Solutions Market Share

The Intravenous (IV) solutions industry is primarily led by well-established companies, including:

- Baxter (U.S.)

- Braun SE (Germany)

- Fresenius Kabi AG (Germany)

- ICU Medical, Inc. (U.S.)

- Terumo Corporation (Japan)

- Otsuka Pharmaceutical Factory, Inc. (Japan)

- Grifols S.A. (Spain)

- Fresenius SE & Co. KGaA (Germany)

- Hospira (U.S.)

- Pfizer Inc. (U.S.)

- Sichuan Kelun Pharmaceutical Co., Ltd. (China)

- Shandong Hualu-Hengsheng Chemical Co., Ltd. (China)

- Shanghai Changqiang Medical Industry Co., Ltd. (China)

- JW Life Science (South Korea)

- SSY Group Limited (Hong Kong)

- NIPRO CORPORATION (Japan)

- Vifor Pharma (Switzerland)

- Amanta Healthcare Ltd. (India)

- Well Lead Medical Co., Ltd. (China)

- Renolit Healthcare (Germany)

Latest Developments in Intravenous (IV) Solutions Market

- In August 2025, the U.S. Food and Drug Administration (FDA) announced the resolution of the nationwide shortage of 0.9% sodium chloride intravenous (IV) solutions, restoring stable supply across hospitals and healthcare facilities. The shortage had previously caused hospitals to ration IV fluids, prioritizing critical care and emergency use due to supply chain disruptions and manufacturing constraints. The recovery was supported by increased production from major manufacturers and improved distribution coordination across the healthcare system. Hospitals were advised to transition back to normal usage protocols after extended conservation measures. This development significantly improved confidence in IV supply chain stability

- In August 2025, Reuters reported that the U.S. IV injectable saline shortage was officially declared resolved by the FDA, marking a major stabilization point for hospital supply chains. The announcement indicated that production and distribution of IV saline had returned to adequate levels following months of disruption. Hospitals had previously faced severe constraints, leading to delayed elective procedures and strict conservation policies. The recovery was driven by improved manufacturing output and coordinated supply efforts from key industry players. Despite resolution, authorities continued monitoring other injectable shortages

- In July 2025, Baxter International reported financial and operational impacts linked to earlier IV fluid shortages and supply disruptions caused by manufacturing constraints at its key facilities. The company noted that hospital demand patterns for IV solutions remained affected due to ongoing conservation practices adopted during the shortage period. Reduced consumption volumes reflected slower normalization of clinical usage across healthcare systems. The disruption highlighted dependency on centralized production sites for IV fluids

- In November 2024, widespread shortages of sterile IV fluids intensified in the United States following significant disruption at a major manufacturing facility supplying large volumes of IV solutions. Hospitals across multiple regions reported constrained access to saline and other essential IV products. Healthcare providers were forced to postpone non-urgent procedures and implement strict conservation strategies. The shortage placed pressure on emergency and critical care departments, where IV fluids are essential for patient stabilization. Regulatory agencies and manufacturers coordinated emergency response measures, including alternative sourcing and production scaling

- In January 2022, ICU Medical completed its acquisition of Smiths Medical, expanding its global portfolio of infusion therapy and intravenous (IV) solutions products. The acquisition strengthened capabilities in IV administration sets, vascular access devices, and infusion systems used in hospital care. It significantly increased manufacturing scale and global distribution reach for critical care consumables. The combined entity enhanced innovation in drug delivery and IV therapy technologies. The consolidation improved supply chain efficiency across healthcare institutions

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.