Global Hypoprothrombinemia Treatment Market

Market Size in USD Billion

USD

1.08 Billion

USD

1.53 Billion

2025

2033

USD

1.08 Billion

USD

1.53 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.08 Billion | |

| USD 1.53 Billion | |

| % | |

|

Hypoprothrombinemia Treatment Market Size

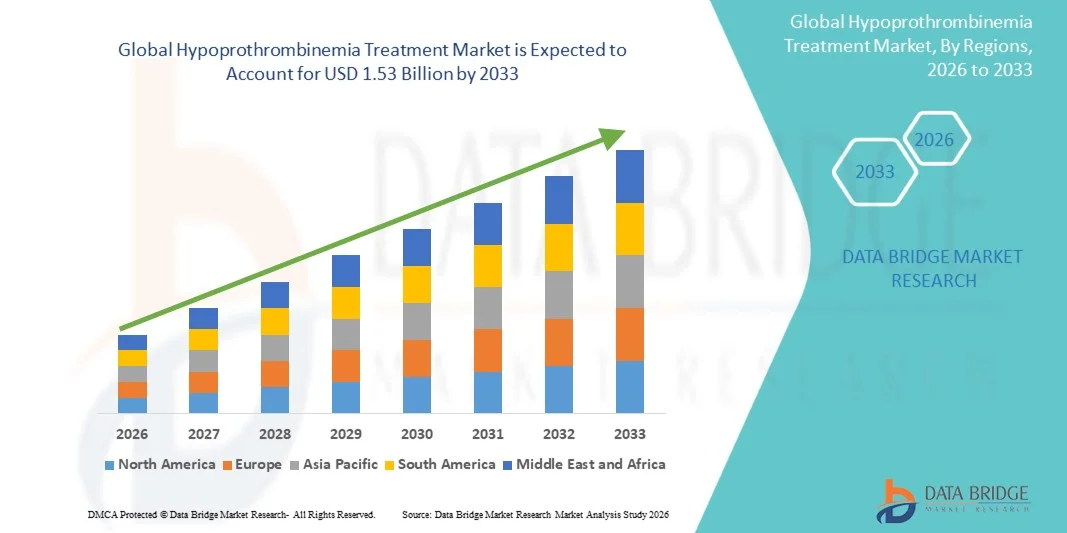

- The global hypoprothrombinemia treatment market size was valued at USD 1.08 billion in 2025 and is expected to reach USD 1.53 billion by 2033, at a CAGR of 4.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of bleeding disorders and coagulation deficiencies, improved diagnostic methods, rising demand for accessible treatment options such as vitamin K supplementation, prothrombin complex concentrates, and recombinant therapies, and enhanced healthcare infrastructure expansion globally

- Furthermore, advancements in treatment technologies including recombinant coagulation factors, personalized medicine approaches, and innovative drug delivery systems combined with an increased focus on home care treatment models and hematology-focused care centers are boosting adoption of hypoprothrombinemia treatments. These converging factors are accelerating the uptake of effective therapies, thereby significantly boosting the industry’s growth.

Hypoprothrombinemia Treatment Market Analysis

- Hypoprothrombinemia treatments, encompassing therapies for True hypoprothrombinemia (Type I Deficiency) and dysprothrombinemia (Type II Deficiency), are increasingly vital components of modern hematology and coagulation management due to their critical role in preventing excessive bleeding, improving patient outcomes, and enabling both acute and long-term care in clinical and home settings

- The escalating demand for hypoprothrombinemia treatments is primarily fueled by the rising prevalence of coagulation disorders, advancements in diagnostic technologies, growing awareness among healthcare providers and patients, and increasing adoption of targeted treatment options such as medications, preventive care, and dietary supplements

- North America dominated the hypoprothrombinemia treatment market with the largest revenue share of 38.5% in 2025, characterized by advanced healthcare infrastructure, high healthcare expenditure, and a strong presence of key pharmaceutical players

- Asia-Pacific is expected to be the fastest-growing region in the hypoprothrombinemia treatment market during the forecast period due to expanding healthcare infrastructure, rising awareness of bleeding disorders, increasing availability of advanced therapies, and supportive government initiatives in countries such as China and India

- Medication segment dominated the hypoprothrombinemia treatment market with a market share of 45.2% in 2025, driven by the widespread use of drugs such as Phytomenadione and Menadoxime

Report Scope and Hypoprothrombinemia Treatment Market Segmentation

|

Attributes |

Hypoprothrombinemia Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Hypoprothrombinemia Treatment Market Trends

“Advancements in Recombinant and Targeted Therapies”

- A significant and accelerating trend in the global hypoprothrombinemia treatment market is the increasing development and adoption of recombinant coagulation factors and targeted therapies, enhancing treatment safety, efficacy, and patient convenience

- For instance, recombinant prothrombin complex concentrates (PCC) are being increasingly used to manage both inherited and acquired coagulation deficiencies, reducing dependency on plasma-derived products

- Targeted therapies enable personalized dosing based on patient-specific coagulation profiles, minimizing adverse effects and improving long-term outcomes, while novel drug delivery systems are facilitating home-based or outpatient administration

- The integration of these advanced therapies into standard treatment protocols is improving accessibility and adherence, allowing clinicians to tailor treatment strategies for acute, chronic, or preventive care

- For instance, companies such as CSL Behring are developing recombinant PCCs with enhanced stability and longer shelf-life, offering healthcare providers more flexible options for both hospital and home administration

- The trend towards more precise, patient-centric, and easy-to-administer treatments is reshaping market expectations, with demand rising across both developed and emerging regions

- For instance, cloud-based coagulation monitoring apps integrated with wearable devices are being piloted to track therapy adherence and effectiveness remotely

Hypoprothrombinemia Treatment Market Dynamics

Driver

“Increasing Prevalence of Coagulation Disorders and Awareness”

- The rising prevalence of bleeding disorders, coupled with growing awareness among patients and healthcare providers, is a significant driver for the increased demand for hypoprothrombinemia treatments

- For instance, in March 2025, Pfizer announced expanded clinical programs for Menadoxime-based therapies to improve accessibility for patients with Type I and Type II deficiencies, expected to drive market growth

- As more patients are diagnosed through advanced coagulation testing, treatment uptake is increasing due to the critical need to prevent severe bleeding events and associated complications

- Furthermore, expansion of hematology-focused healthcare infrastructure and supportive reimbursement policies are making therapies more accessible in both hospital and home settings

- For instance, improved patient education campaigns and disease awareness programs in North America and Europe have led to earlier interventions and higher adoption rates of PCC and FFP therapies

- The combination of increased patient diagnosis, accessibility of advanced therapies, and heightened awareness is substantially propelling the hypoprothrombinemia treatment market globally

- Strong pharmaceutical R&D pipelines focused on novel coagulation therapies are introducing next-generation drugs that are safer and more effective, further stimulating market growth

- For instance, emerging therapies targeting specific coagulation pathways are being fast-tracked in clinical trials to meet unmet patient needs, particularly in pediatric populations

Restraint/Challenge

“High Therapy Costs and Limited Access in Emerging Regions”

- The relatively high cost of advanced hypoprothrombinemia therapies, including recombinant PCCs and specialized medications, poses a significant challenge to broader market penetration

- For instance, limited reimbursement and higher out-of-pocket costs in emerging regions make it difficult for patients to access premium therapies, restricting adoption

- While plasma-derived therapies remain available, safety concerns and limited supply constrain their widespread use, especially in low-income countries where advanced infrastructure is lacking

- Addressing these access and affordability challenges is critical for expanding market reach and ensuring equitable treatment availability across regions

- For instance, patient assistance programs and tiered pricing strategies are being explored by companies such as Grifols to improve accessibility for economically constrained populations

- Overcoming cost and accessibility barriers through policy support, innovative pricing, and expanded distribution channels will be vital for sustaining market growth over the forecast period

- Regulatory hurdles for new therapies, including lengthy clinical trials and complex approval processes, further delay market entry and increase development costs

- For instance, novel recombinant drugs often require multi-country approvals before commercial launch, slowing adoption in several regions and increasing overall market uncertainty

Hypoprothrombinemia Treatment Market Scope

The market is segmented on the basis of type, treatment, product, drugs, route of administration, distribution channel, and end-users.

- By Type

On the basis of type, the market is segmented into True Hypoprothrombinemia (Type I Deficiency) and Dysprothrombinemia (Type II Deficiency). The True Hypoprothrombinemia (Type I Deficiency) segment dominated the market with the largest revenue share in 2025, driven by its higher prevalence and urgent need for clinical intervention. Hospitals and specialty clinics frequently stock Prothrombin Complex Concentrates (PCC) and Fresh Frozen Plasma (FFP) to manage acute bleeding episodes. Established treatment protocols and strong insurance coverage in North America and Europe further reinforce this segment’s dominance. Patients with Type I deficiency require both acute and preventive therapy, creating consistent demand for medications. The widespread availability of vitamin K-based therapies ensures that the segment remains the largest contributor to market revenue. Additionally, ongoing R&D and regulatory approvals support its continued growth.

The Dysprothrombinemia (Type II Deficiency) segment is expected to witness the fastest growth from 2026 to 2033, fueled by advancements in diagnostic technologies that enable early detection of functional prothrombin defects. Rising awareness among hematologists and patients is driving adoption of targeted therapies. Emerging markets in Asia-Pacific are witnessing increased screening programs and improved healthcare access. Clinical research on novel drugs for Type II deficiency is creating growth opportunities. Homecare management and telemedicine integration further accelerate adoption. Patient education programs and preventive care initiatives are also contributing to rapid market expansion.

- By Treatment

On the basis of treatment, the market is segmented into medication, preventive care, and supplements. The Medication segment dominated in 2025 with a market share of 45.2%, driven by the widespread use of drugs such as Phytomenadione and Menadoxime for both acute and chronic management. Hospitals and homecare providers rely on medications for proven efficacy, regulatory approval, and ease of administration. High adoption in developed markets ensures sustained dominance. Medications are central to standard treatment protocols in hospitals and specialty clinics. Ongoing R&D in improved formulations enhances patient outcomes and reinforces the segment’s market share. Furthermore, insurance reimbursement and government healthcare programs support consistent usage worldwide.

The Preventive Care and Supplements segment is expected to witness the fastest growth from 2026 to 2033, due to increasing patient preference for long-term management at home. Oral vitamin K and supportive dietary therapies are gaining popularity. E-commerce and online pharmacy channels enhance accessibility in emerging markets. Preventive therapy reduces hospitalization and associated costs, aligning with healthcare efficiency trends. Awareness campaigns emphasizing early intervention are driving adoption. Telehealth and homecare services further accelerate growth in this segment globally.

- By Product

On the basis of product, the market is segmented into Prothrombin Complex Concentrates (PCC) and Fresh Frozen Plasma (FFP) Drugs. The PCC segment dominated the market in 2025 due to its rapid onset of action, lower infusion volumes, and lower infection risk compared to plasma therapy. Hospitals stock PCC to manage acute bleeding events efficiently. Developed markets lead in PCC adoption due to established clinical protocols and reimbursement support. Newer formulations with improved stability strengthen market position. PCC is widely used in critical care and specialty clinics. Continuous physician training and established efficacy reinforce its market dominance.

The FFP Drugs segment is expected to witness the fastest growth from 2026 to 2033, fueled by expanding hospital infrastructure and blood bank facilities in emerging markets. FFP is essential where PCC availability is limited or cost-prohibitive. It plays a critical role in perioperative and acute bleeding management. Efforts to improve storage, shelf-life, and transfusion safety are expanding accessibility. Healthcare spending in Asia-Pacific and Latin America drives adoption. Hospitals increasingly rely on FFP for emergency interventions. Awareness campaigns about plasma therapy benefits accelerate growth further.

- By Drugs

On the basis of drugs, the market is segmented into Phytomenadione, Menadoxime, and Others. The Phytomenadione segment dominated in 2025 due to its established efficacy, low cost, and wide availability. It is widely used for both Type I and Type II deficiencies. Oral and parenteral formulations make it suitable for hospital, homecare, and preventive applications. National essential medicines lists include Phytomenadione, ensuring consistent demand. Hospitals, specialty clinics, and homecare programs rely on this drug for acute and preventive therapy. Clinical trust and regulatory approvals maintain its dominance globally.

The Menadoxime segment is expected to witness the fastest growth from 2026 to 2033, due to its enhanced efficacy in patients unresponsive to standard vitamin K therapy. Adoption is rapidly increasing in specialty clinics and hospitals in North America and Europe. Clinical trials and research on novel delivery methods are expanding therapeutic applications. Emerging markets are integrating Menadoxime into preventive care regimens. Hematologists are increasingly aware of its targeted benefits. Telehealth and patient monitoring programs support rapid adoption.

- By Route of Administration

On the basis of route, the market is segmented into oral and parenteral. The Parenteral segment dominated in 2025, driven by rapid onset of action for acute treatment and emergency management. Hospitals and specialty clinics rely on intravenous or intramuscular administration for accurate dosing. Parenteral therapy is preferred for PCC and FFP drugs. High efficacy and safety profiles sustain adoption in developed markets. Optimized formulations ensure longer shelf-life and stability. Continuous training for healthcare providers reinforces parenteral administration dominance.

The Oral segment is expected to witness the fastest growth from 2026 to 2033, due to ease of self-administration and suitability for long-term preventive care. Patients prefer oral vitamin K and supplements for home use. Online pharmacy distribution and telemedicine monitoring boost adoption in emerging markets. Oral administration reduces hospital visits and healthcare costs. Awareness campaigns for chronic therapy management drive uptake. Patient education and adherence programs further accelerate oral therapy adoption globally.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated in 2025 due to direct access to acute therapies and emergency interventions. Critical care units and hematology wards rely on hospital pharmacies for PCC, FFP, and medications. Developed markets contribute major revenue share. Insurance coverage supports hospital-based distribution. Hospitals ensure proper storage, dosing, and administration. Integration with clinical protocols reinforces dominance.

The Online Pharmacy segment is expected to witness the fastest growth from 2026 to 2033, due to convenience and direct-to-patient delivery of oral therapies and supplements. Telemedicine prescriptions facilitate homecare adoption. E-commerce platforms enhance accessibility in remote and underserved regions. Patients prefer online ordering for preventive and chronic therapies. Partnerships with digital adherence platforms accelerate growth. Emerging markets are seeing rising adoption due to internet penetration and logistics improvements.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty clinics, and others. The Hospitals segment dominated in 2025, driven by high demand for acute and emergency coagulation therapies. Hospitals stock PCC, FFP, and medications for critical care. Developed regions with advanced infrastructure contribute major market share. Hospitals integrate clinical trials and adoption of new therapies. Insurance coverage and reimbursement policies support hospital usage. Hospitals ensure accurate and timely administration of treatments.

The Homecare segment is expected to witness the fastest growth from 2026 to 2033, due to patient preference for self-administered oral and parenteral therapies. Chronic and preventive management can now be managed at home with telehealth support. Convenience, reduced hospital visits, and cost efficiency drive adoption. Emerging markets are improving homecare infrastructure and awareness. Patient-friendly kits and digital support tools enhance adherence. Homecare adoption is accelerating globally, especially in preventive care programs.

Hypoprothrombinemia Treatment Market Regional Analysis

- North America dominated the hypoprothrombinemia treatment market with the largest revenue share of 38.5% in 2025, characterized by advanced healthcare infrastructure, high healthcare expenditure, and a strong presence of key pharmaceutical players

- Patients and healthcare providers in the region highly value access to advanced therapies such as Prothrombin Complex Concentrates (PCC), Fresh Frozen Plasma (FFP), and recombinant drugs, which provide rapid and effective management of acute bleeding episodes

- This widespread adoption is further supported by comprehensive insurance coverage, government healthcare programs, and high investment in hematology research, establishing North America as the largest market for both hospital-based and homecare treatments

U.S. Hypoprothrombinemia Treatment Market Insight

The U.S. hypoprothrombinemia treatment market captured the largest revenue share of 78% in 2025 within North America, driven by the well-established healthcare infrastructure, advanced diagnostic facilities, and high patient awareness of coagulation disorders. Patients increasingly prioritize timely access to Prothrombin Complex Concentrates (PCC), Fresh Frozen Plasma (FFP), and vitamin K therapies to manage acute and chronic bleeding episodes. The growing trend of homecare management and telemedicine support allows patients to self-administer oral and parenteral treatments, improving adherence and convenience. Hospitals and specialty clinics maintain robust demand for emergency therapies, particularly in surgical and hematology departments. Additionally, strong insurance coverage and government healthcare programs further facilitate the adoption of both preventive and acute treatments. The integration of digital patient monitoring platforms also enhances treatment outcomes, sustaining the market’s growth trajectory.

Europe Hypoprothrombinemia Treatment Market Insight

The Europe hypoprothrombinemia treatment market is projected to expand at a substantial CAGR during the forecast period, primarily driven by stringent healthcare regulations, increasing prevalence of coagulation disorders, and well-developed hospital infrastructure. Rising urbanization and growing awareness about preventive care are fostering the adoption of oral supplements and vitamin K therapies. European patients and healthcare providers highly value integrated treatment protocols that combine hospital-based and homecare therapies. The market is witnessing growth across hospitals, specialty clinics, and homecare applications, with an increasing focus on patient-friendly oral and parenteral medications. Additionally, government initiatives promoting preventive health and reimbursement schemes are supporting increased adoption of treatments. The growing emphasis on research and clinical trials in hematology further stimulates market expansion.

U.K. Hypoprothrombinemia Treatment Market Insight

The U.K. hypoprothrombinemia treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing focus on hematology care, early diagnosis of coagulation disorders, and preventive treatment awareness. Concerns regarding severe bleeding complications encourage both hospitals and homecare providers to ensure timely availability of PCC, FFP, and vitamin K therapies. The U.K.’s advanced healthcare infrastructure and strong telemedicine integration support self-administration of oral and parenteral treatments at home. Patients are increasingly prioritizing convenience, adherence, and preventive care, while specialty clinics expand services for chronic management. Additionally, robust e-commerce and pharmacy networks improve accessibility to medications and supplements. Rising awareness programs and clinical support initiatives further stimulate market growth in the U.K.

Germany Hypoprothrombinemia Treatment Market Insight

The Germany hypoprothrombinemia treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of coagulation disorders and demand for advanced therapeutic solutions. Hospitals and specialty clinics in Germany are adopting PCC, FFP, and novel vitamin K formulations for acute, chronic, and preventive care. The country’s well-developed infrastructure, coupled with a focus on innovation and patient safety, promotes adoption of homecare therapy programs. Parenteral and oral treatment routes are increasingly used for convenience and adherence. Germany emphasizes sustainable and technologically advanced healthcare solutions, which further boosts demand for high-quality therapies. Research initiatives in hematology and preventive programs support continued market expansion.

Asia-Pacific Hypoprothrombinemia Treatment Market Insight

The Asia-Pacific hypoprothrombinemia treatment market is poised to grow at the fastest CAGR of 23% during the forecast period from 2026 to 2033, driven by rising urbanization, increasing healthcare expenditure, and technological advancements in countries such as China, Japan, and India. The region’s growing awareness about coagulation disorders and early diagnosis programs is increasing adoption of PCC, FFP, and oral vitamin K therapies. Homecare programs and telemedicine platforms are expanding patient reach, making preventive care more accessible. Additionally, the development of domestic pharmaceutical manufacturing and affordable treatment options is enhancing market penetration. Hospitals, specialty clinics, and retail pharmacies are witnessing increased demand. Government initiatives promoting digital healthcare and preventive treatment further accelerate regional growth.

Japan Hypoprothrombinemia Treatment Market Insight

The Japan hypoprothrombinemia treatment market is gaining momentum due to a high-tech healthcare ecosystem, an aging population, and rising patient preference for preventive and homecare therapies. Hospitals and specialty clinics are adopting PCC, FFP, and oral vitamin K to manage acute and chronic coagulation deficiencies. Integration of telemedicine platforms allows safe self-administration and remote monitoring, supporting patient adherence. The emphasis on convenience and quality care is driving adoption in both residential and clinical settings. Japan’s regulatory framework ensures access to innovative therapies. Growing awareness among patients about chronic management and preventive care is boosting market demand. The combination of technological adoption and government healthcare support contributes to steady growth.

India Hypoprothrombinemia Treatment Market Insight

The India hypoprothrombinemia treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, increasing healthcare access, and high awareness of bleeding disorders. India is witnessing rising adoption of PCC, FFP, and oral vitamin K therapies across hospitals, specialty clinics, and homecare programs. The country’s expanding middle class and rising disposable incomes are driving demand for both preventive and acute treatments. Government initiatives, including health insurance schemes and digital health programs, are supporting broader access. Affordable domestic manufacturing and online pharmacy distribution further enhance market reach. The push toward preventive care, patient education, and telemedicine platforms is expected to accelerate market growth across India.

Hypoprothrombinemia Treatment Market Share

The Hypoprothrombinemia Treatment industry is primarily led by well-established companies, including:

- Takeda Pharmaceutical Company Limited (Japan)

- Pfizer Inc. (U.S.)

- Intas Pharmaceuticals Ltd. (India)

- Grifols S.A. (Spain)

- Baxter (U.S.)

- Octapharma AG (Switzerland)

- CSL Behring (U.S.)

- Hualan Biological Engineering Co., Ltd (China)

- Shanghai RAAS Blood Products Co., Ltd (China)

- LFB S.A. (France)

- Green Cross Corporation (South Korea)

- Bio Products Laboratory Ltd (U.K.)

- Prothya Biosolutions B.V. (Netherlands)

- China Biologic Products Holdings Inc (U.S.)

- Meheco Xinxing Pharma (China)

- Kedrion Biopharma (Italy)

- Emergent BioSolutions (U.S.)

- Haemonetics Corporation (U.S.)

- Physician’s Total Care (U.S.)

- ZoomRx Analytics (U.S.)

What are the Recent Developments in Global Hypoprothrombinemia Treatment Market?

- In March 2025, British researchers launched the Prophesy‑2 trial, a major multi‑center randomized study in the U.K. to directly compare Prothrombin Complex Concentrate (PCC) with Fresh Frozen Plasma (FFP) for managing bleeding in adults after cardiac surgery, aiming to generate high‑quality evidence on clinical and cost effectiveness of PCC versus standard FFP treatment

- In March 2025, results from the FARES‑II Phase 3 clinical trial presented at the American College of Cardiology Annual Scientific Session showed that four‑factor Prothrombin Complex Concentrate (4F‑PCC) significantly reduced major bleeding and transfusion needs compared with frozen plasma in adult cardiac surgery patients, indicating potential shifts in clinical guidelines toward PCC‑based coagulation management

- In August 2024, the Journal of the American Medical Association (JAMA) Network Open published outcomes highlighting the effectiveness of Balfaxar® for warfarin reversal in surgical patients, reinforcing clinical confidence in this PCC therapy’s ability to restore coagulation factors in high‑risk bleeding scenarios

- In January 2024, Octapharma USA officially announced the availability of Balfaxar® in the U.S., indicating that hospitals and medical providers now have access to this newly approved 4F‑PCC product for urgent coagulation reversal in clinical settings nationwide

- In July 2023, Octapharma’s Balfaxar® (a non‑activated four‑factor prothrombin complex concentrate) received U.S. FDA approval for the urgent reversal of acquired coagulation factor deficiency induced by vitamin K antagonist (warfarin) therapy, offering a new option for adults needing emergency surgery or invasive procedures

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.