Global Hepatitis Test Solution Diagnosis Market

Market Size in USD Billion

USD

6.60 Billion

USD

9.42 Billion

2024

2032

USD

6.60 Billion

USD

9.42 Billion

2024

2032

| 2025 - 2032 | |

| USD 6.60 Billion | |

| USD 9.42 Billion | |

| % | |

|

Hepatitis Test Solution/Diagnosis Market Size

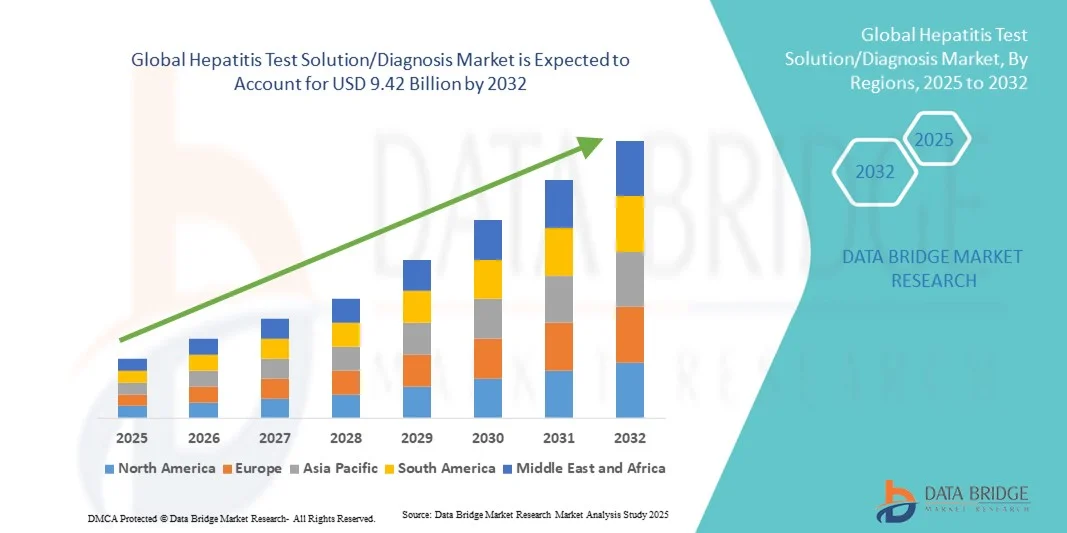

- The global hepatitis test solution/diagnosis market size was valued at USD 6.60 billion in 2024 and is expected to reach USD 9.42 billion by 2032, at a CAGR of 4.55% during the forecast period

- The market growth is largely fueled by the rising prevalence of hepatitis infections worldwide, coupled with increasing awareness about early disease detection and prevention. Technological advancements in diagnostic assays, including rapid tests and molecular diagnostics, are further enhancing the accuracy and efficiency of hepatitis testing across clinical and point-of-care settings

- Furthermore, growing government initiatives for hepatitis screening programs, expanding healthcare infrastructure, and increased adoption of automated and high-throughput testing systems are driving the demand for Hepatitis Test Solution/Diagnosis products. These converging factors are accelerating the uptake of hepatitis diagnostic solutions, thereby significantly boosting the industry's growth.

Hepatitis Test Solution/Diagnosis Market Analysis

- Hepatitis test solutions and diagnostic tools are vital components of modern healthcare systems across both hospital and laboratory settings, owing to their critical role in early detection, disease monitoring, and treatment management of hepatitis infections. Their enhanced accuracy, automation capabilities, and integration with advanced diagnostic platforms ensure efficient and reliable results

- The escalating demand for hepatitis test solutions and diagnosis systems is primarily fueled by the growing global burden of hepatitis infections, increasing awareness about early disease detection, and rising government initiatives promoting routine screening and preventive healthcare. The expanding use of molecular and immunoassay-based diagnostic methods also contributes to higher adoption rates

- North America dominated the hepatitis test solution/diagnosis market with the largest revenue share of 39.6% in 2024, driven by advanced healthcare infrastructure, strong presence of major diagnostic companies, and widespread implementation of screening programs. The U.S. experienced substantial growth in the adoption of hepatitis testing systems across hospitals, diagnostic centers, and public health laboratories. Technological advancements, such as automated analyzers and multiplexed detection platforms, coupled with growing awareness about hepatitis B and C infections, further strengthened regional dominance

- Asia-Pacific is expected to be the fastest-growing region in the hepatitis test solution/diagnosis market during the forecast period, with a projected CAGR of 21.4% from 2025 to 2032, driven by increasing healthcare expenditure, large patient populations, and rising awareness about infectious disease management. Expanding access to diagnostic services in countries such as China, India, and Japan, along with government-led vaccination and screening programs, continues to boost regional growth

- The Blood Tests segment dominated the largest market revenue share of 45.6% in 2024, driven by its essential role in identifying hepatitis infections through detection of viral antigens, antibodies, and liver enzyme levels

Report Scope and Hepatitis Test Solution/Diagnosis Market Segmentation

|

Attributes |

Hepatitis Test Solution/Diagnosis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Hepatitis Test Solution/Diagnosis Market Trends

Enhanced Convenience Through AI and Automated Diagnostic Integration

- A significant and accelerating trend in the global hepatitis test solution/diagnosis market is the deepening integration of artificial intelligence (AI) and automated diagnostic platforms. This technological fusion is significantly enhancing testing accuracy, workflow efficiency, and result interpretation for both healthcare providers and diagnostic laboratories

- For instance, Abbott Laboratories’ Alinity m System integrates with advanced laboratory automation and data analytics software, allowing simultaneous detection and quantification of multiple hepatitis virus strains with minimal manual intervention. Similarly, Roche Diagnostics’ cobas 6800/8800 Systems utilize AI-driven algorithms for high-throughput viral load testing and interpretation, offering a more streamlined and reliable hepatitis diagnostic solution

- AI integration in hepatitis testing enables functions such as learning from patient data patterns to suggest optimal testing strategies, identifying co-infections, and providing predictive insights based on viral load dynamics. For example, certain automated PCR-based platforms use machine learning to reduce false positives and improve detection sensitivity over time. Furthermore, integration with electronic medical record (EMR) systems offers clinicians real-time access to diagnostic data, allowing rapid decision-making and improved patient management

- The seamless integration of hepatitis diagnostic systems with digital healthcare networks and centralized laboratory platforms facilitates unified control over multiple stages of the testing workflow. Through a single interface, users can manage sample preparation, testing, analysis, and reporting — thereby creating an efficient and automated diagnostic environment

- This trend toward more intelligent, connected, and automated testing systems is fundamentally reshaping expectations in the field of infectious disease diagnostics. Consequently, companies such as Siemens Healthineers and Bio-Rad Laboratories are developing AI-enabled diagnostic solutions with automated sample handling, predictive analytics, and cloud-based result management for faster and more accurate hepatitis detection

- The demand for hepatitis testing solutions with enhanced automation, integrated analytics, and advanced data connectivity is growing rapidly across clinical laboratories, hospitals, and public health institutions, as healthcare providers increasingly prioritize accuracy, efficiency, and comprehensive patient management in infectious disease diagnostics

Hepatitis Test Solution/Diagnosis Market Dynamics

Driver

Growing Need Due to Rising Hepatitis Incidence and Advancements in Molecular Diagnostics

- The increasing global prevalence of hepatitis A, B, and C infections, coupled with advancements in diagnostic technology, is a major driver for the growing demand for hepatitis test solutions and diagnosis systems

- For instance, in April 2024, Abbott Laboratories announced the expansion of its ARCHITECT and Alinity i immunoassay platforms with enhanced hepatitis B and C testing capabilities, designed to provide higher sensitivity and faster turnaround times. Such developments by key players are expected to drive the hepatitis diagnostics industry growth during the forecast period

- As healthcare providers aim for early detection and improved management of liver diseases, hepatitis testing solutions offer benefits such as rapid screening, quantitative viral load monitoring, and genotyping — enabling more effective treatment decisions and improved public health outcomes

- Furthermore, the growing emphasis on blood safety, organ transplantation screening, and public health surveillance has made hepatitis testing an essential part of diagnostic infrastructure worldwide. The integration of automated molecular diagnostics and point-of-care (POC) testing devices is further expanding access, especially in resource-limited settings

- The convenience of high-throughput testing, reduced human error, faster reporting, and the ability to process large volumes of samples simultaneously are key factors propelling adoption in both clinical and reference laboratories. The rising demand for multiplex testing platforms capable of detecting multiple hepatitis viruses in one run also contributes to significant market growth

Restraint/Challenge

Concerns Regarding High Test Costs and Limited Accessibility in Low-Income Regions

- Despite technological advancements, high testing costs and limited infrastructure in developing countries pose significant challenges to the broader adoption of hepatitis diagnostic solutions. As molecular and immunoassay-based tests often rely on sophisticated equipment and reagents, they can be expensive for underfunded healthcare systems

- For instance, in many low- and middle-income nations, access to advanced hepatitis viral load testing or genotyping remains limited, restricting early diagnosis and timely treatment initiation. This gap underscores the need for affordable, easy-to-use, and portable diagnostic alternatives

- Addressing these challenges through cost-effective assay development, decentralized testing models, and public–private partnerships is crucial for improving global hepatitis control. Companies such as Cepheid and Hologic are actively developing cartridge-based molecular testing solutions that require minimal infrastructure while maintaining high accuracy. In addition, collaborations with global health organizations like the World Health Organization (WHO) and Gavi, the Vaccine Alliance, are expanding diagnostic accessibility in underserved regions

- While prices are gradually decreasing due to technological innovation and government-led screening programs, the high cost of consumables and maintenance of automated systems remains a challenge for smaller laboratories. Moreover, the lack of skilled personnel for advanced molecular testing can hinder implementation in certain areas

- Overcoming these challenges through increased funding, awareness programs, capacity-building initiatives, and the introduction of low-cost rapid diagnostic kits will be essential for sustaining market expansion and achieving global hepatitis elimination targets

Hepatitis Test Solution/Diagnosis Market Scope

The market is segmented on the basis of Tests, Disease Type, Technology, and End-User.

- By Tests

On the basis of tests, the Hepatitis Test Solution/Diagnosis market is segmented into Blood Tests, Imaging Tests, and Liver Biopsy. The Blood Tests segment dominated the largest market revenue share of 45.6% in 2024, driven by its essential role in identifying hepatitis infections through detection of viral antigens, antibodies, and liver enzyme levels. Blood tests such as ELISA, rapid immunoassays, and molecular-based assays are widely adopted due to their accuracy, cost-effectiveness, and suitability for large-scale screening programs. Hospitals and diagnostic laboratories rely heavily on blood testing for initial diagnosis and disease monitoring. Increased government-led screening initiatives, especially for hepatitis B and C, further strengthen segment dominance. Technological advancements have improved assay sensitivity and specificity, reducing false results and enabling early-stage detection. The rising use of automated analyzers and multiplex systems enhances throughput and workflow efficiency, making blood tests indispensable across healthcare settings globally.

The Imaging Tests segment is anticipated to witness the fastest CAGR of 21.3% from 2025 to 2032, driven by the growing use of ultrasound, CT scans, and MRI for assessing liver damage and fibrosis levels in hepatitis patients. Advancements in imaging software and non-invasive diagnostic technologies are boosting adoption. The increasing preference for non-invasive monitoring solutions among patients, combined with hospital adoption of advanced imaging equipment, supports strong growth. Integration of imaging data with laboratory results enhances diagnostic precision and clinical decision-making, fueling this segment’s expansion throughout the forecast period.

- By Disease Type

On the basis of disease type, the Hepatitis Test Solution/Diagnosis market is segmented into Hepatitis B, Hepatitis C, and Others. The Hepatitis B segment dominated the largest market revenue share of 42.7% in 2024, driven by the high global prevalence of chronic hepatitis B infection and increased awareness of early screening and vaccination programs. Public health initiatives across North America, Europe, and Asia-Pacific have expanded testing coverage. Diagnostic advancements, including quantitative viral load testing and genotyping, further enhance clinical management. Continuous government campaigns and inclusion of hepatitis B tests in national immunization programs sustain segment leadership. Hospitals and clinics rely on HBV DNA quantification for treatment evaluation, reinforcing demand for molecular-based solutions. The availability of automated, high-throughput HBV testing systems ensures consistent and reliable performance in clinical settings. Growing collaborations between assay developers and healthcare agencies further boost accessibility and adoption worldwide.

The Hepatitis C segment is expected to witness the fastest CAGR of 22.5% from 2025 to 2032, driven by rising global prevalence, improved screening initiatives, and technological advancements in molecular and immunoassay diagnostics. Increasing focus on early detection and effective treatment monitoring drives testing demand. Expanding research into antiviral therapies and companion diagnostics supports further market growth. Integration of PCR and rapid diagnostic tests enables more efficient diagnosis of both acute and chronic infections, positioning the segment as a key growth driver in the global market.

- By Technology

On the basis of technology, the Hepatitis Test Solution/Diagnosis market is segmented into ELISA, Rapid Diagnostic Test (RDT), PCR, INAAT, and Others. The ELISA segment held the largest market revenue share of 40.9% in 2024, owing to its high accuracy, scalability, and widespread use in detecting hepatitis antigens and antibodies. ELISA-based assays are the standard diagnostic tools in hospitals and laboratories due to their cost-effectiveness and high throughput. Continuous technological refinements have reduced turnaround time while maintaining sensitivity and specificity. Widespread availability of ELISA kits from leading diagnostic manufacturers strengthens market penetration. Integration with automation systems and microplate readers further enhances workflow efficiency. The method’s compatibility with a variety of sample types and its role in both screening and confirmatory testing underpin its continued dominance. Growing awareness of preventive healthcare and increased routine screening programs in developing economies further stimulate demand for ELISA-based tests globally.

The PCR segment is projected to witness the fastest CAGR of 23.1% from 2025 to 2032, fueled by the increasing need for molecular-level detection and quantification of viral RNA/DNA. PCR-based assays offer superior accuracy and sensitivity, making them indispensable for confirming infection and monitoring treatment response. Technological advancements, including real-time and multiplex PCR, allow simultaneous detection of multiple hepatitis virus strains, enhancing diagnostic precision. Growing adoption in research laboratories, hospitals, and public health initiatives, along with falling equipment costs and automation, are driving the segment’s rapid expansion.

- By End User

On the basis of end user, the Hepatitis Test Solution/Diagnosis market is segmented into Hospitals, Diagnostic Laboratories, Blood Banks, Clinics, and Others. The Hospitals segment dominated the largest market revenue share of 46.2% in 2024, attributed to the growing adoption of advanced diagnostic equipment and the need for rapid, accurate results in patient care. Hospitals serve as primary centers for hepatitis screening, treatment, and management, handling large patient volumes and conducting confirmatory tests. Strong infrastructure, skilled personnel, and government support for screening programs reinforce dominance. Increasing integration of automated testing platforms and digital health systems improves diagnostic efficiency. Partnerships between hospitals and diagnostic companies enhance accessibility to high-quality tests. Continuous introduction of new biomarkers and advanced detection assays supports hospital-based laboratories in delivering precise diagnostics and effective disease monitoring.

The Diagnostic Laboratories segment is expected to witness the fastest CAGR of 22.8% from 2025 to 2032, driven by the expansion of private and public testing facilities worldwide. Growing preference for outsourcing testing services, rising healthcare awareness, and increasing hepatitis screening campaigns contribute to segment growth. Laboratories are rapidly adopting automated and multiplexed platforms to manage high testing volumes efficiently. Integration with digital reporting systems and AI-driven analysis enhances workflow and accuracy. Collaborations between diagnostic centers, pharmaceutical companies, and research institutions further support technological advancement and accessibility, positioning diagnostic laboratories as the fastest-growing end-user segment globally.

Hepatitis Test Solution/Diagnosis Market Regional Analysis

- North America dominated the hepatitis test solution/diagnosis market with the largest revenue share of 39.6% in 2024, driven by advanced healthcare infrastructure, the strong presence of major diagnostic companies, and widespread implementation of hepatitis screening programs across hospitals, laboratories, and public health agencies

- The region’s growth is further supported by favorable reimbursement frameworks, increasing awareness regarding hepatitis B and C infections, and the adoption of automated, high-throughput analyzers and multiplexed detection platforms

- Moreover, government-backed initiatives for early disease detection and large-scale testing campaigns have strengthened North America’s leadership in the global market. The presence of key diagnostic players such as Abbott Laboratories, Roche Diagnostics, and Bio-Rad Laboratories further enhances technological innovation and product availability, ensuring widespread accessibility and quality assurance in testing services

U.S. Hepatitis Test Solution/Diagnosis Market Insight

The U.S. hepatitis test solution/diagnosis market captured the largest revenue share within North America in 2024, fueled by rising adoption of advanced immunoassay and molecular diagnostic systems, and robust national screening programs supported by the Centers for Disease Control and Prevention (CDC). Increasing awareness regarding viral hepatitis transmission, availability of high-sensitivity test kits, and the integration of automated analyzers in hospitals and diagnostic laboratories are key factors propelling market expansion. Furthermore, ongoing efforts to eliminate hepatitis infections through public health campaigns and funding initiatives have strengthened diagnostic testing uptake across the nation.

Europe Hepatitis Test Solution/Diagnosis Market Insight

The Europe hepatitis test solution/diagnosis market is projected to witness steady growth throughout the forecast period, driven by rising government initiatives for disease surveillance, advanced diagnostic capabilities, and well-established healthcare systems. The region’s strong regulatory framework promotes quality testing and accurate reporting, while the prevalence of hepatitis infections in Eastern Europe continues to stimulate demand for screening solutions. Increasing collaborations between diagnostic manufacturers and public health agencies are expected to further enhance accessibility and testing efficiency across hospitals and laboratories.

U.K. Hepatitis Test Solution/Diagnosis Market Insight

The U.K. hepatitis test solution/diagnosis market is anticipated to grow at a notable CAGR during the forecast period, supported by the National Health Service’s (NHS) continued efforts to eliminate hepatitis infections and improve early detection rates. The country’s emphasis on diagnostic automation and point-of-care testing has led to the adoption of rapid, multiplexed hepatitis testing systems across healthcare facilities. Additionally, strong government-led awareness campaigns and funding for infectious disease control contribute to the U.K.’s consistent market growth.

Germany Hepatitis Test Solution/Diagnosis Market Insight

The Germany hepatitis test solution/diagnosis market is expected to expand steadily, driven by high diagnostic standards, the presence of key biotechnology firms, and growing demand for precision diagnostic tools. Germany’s focus on healthcare digitalization, combined with increasing adoption of laboratory automation, has encouraged the use of molecular and serological assays for hepatitis detection. Continuous innovation in assay technologies and strong investments in public health initiatives further strengthen the market outlook.

Asia-Pacific Hepatitis Test Solution/Diagnosis Market Insight

The Asia-Pacific hepatitis test solution/diagnosis market is poised to grow at the fastest CAGR of 21.4% from 2025 to 2032, driven by rising healthcare expenditure, increasing disease awareness, and expanding diagnostic infrastructure in developing economies. Countries such as China, India, and Japan are leading this growth through large-scale hepatitis screening programs and government-backed vaccination drives. The growing accessibility of affordable testing kits and the establishment of diagnostic laboratories across urban and rural regions are enhancing regional penetration. Furthermore, the presence of local manufacturers offering cost-effective testing solutions supports the region’s position as a rapidly expanding diagnostic hub.

Japan Hepatitis Test Solution/Diagnosis Market Insight

The Japan hepatitis test solution/diagnosis market is gaining momentum owing to its advanced healthcare system, early disease detection initiatives, and growing focus on preventive healthcare. Government-led campaigns for hepatitis elimination, combined with the adoption of high-performance diagnostic technologies, are driving testing volumes. Japan’s aging population and the need for efficient chronic disease management further contribute to the increasing demand for accurate hepatitis testing solutions.

China Hepatitis Test Solution/Diagnosis Market Insight

The China hepatitis test solution/diagnosis market accounted for the largest share in the Asia-Pacific region in 2024, supported by the country’s vast patient pool, rising urbanization, and government programs targeting hepatitis elimination. Strong domestic manufacturing capabilities, rapid healthcare modernization, and growing investments in infectious disease control have led to the widespread availability of testing services across public and private healthcare settings. Additionally, the development of rapid, point-of-care, and multiplexed hepatitis testing platforms by local and international players is significantly contributing to China’s dominance in the regional market.

Hepatitis Test Solution/Diagnosis Market Share

The Hepatitis Test Solution/Diagnosis industry is primarily led by well-established companies, including:

• Abbott (U.S.)

• F. Hoffmann-La Roche Ltd (Switzerland)

• Siemens Healthineers AG (Germany)

• Danaher Corporation (U.S.)

• Bio-Rad Laboratories, Inc. (U.S.)

• Qiagen N.V. (Netherlands)

• Thermo Fisher Scientific Inc. (U.S.)

• Ortho Clinical Diagnostics (U.S.)

• Grifols, S.A. (Spain)

• DiaSorin S.p.A. (Italy)

• bioMérieux SA (France)

• BD (U.S.)

• Hologic, Inc. (U.S.)

• Cepheid (U.S.)

• Orasure Technologies, Inc. (U.S.)

Latest Developments in Global Hepatitis Test Solution/Diagnosis Market

- In May 2022, Abbott launched the ARCHITECT HBsAg Next Qualitative Assay in India. This chemiluminescent microparticle immunoassay (CMIA) enhances early detection of hepatitis B virus (HBV) infections in human serum and plasma samples. It aids in improving patient outcomes and maintaining safe blood supplies

- In November 2023, Roche introduced the Elecsys Anti-HEV IgM and IgG immunoassays for the detection of hepatitis E virus (HEV) infections. These automated serology tests are designed to identify acute and past HEV infections and are recommended in the WHO 2023 Essential Diagnostics List

- In October 2023, Egypt became the first country to achieve the “gold tier” status on the path to elimination of hepatitis C, as per WHO criteria. This milestone indicates that Egypt has fulfilled the programmatic requirements to reduce new hepatitis C infections and deaths to levels that position the country to end the hepatitis C epidemic

- In March 2025, the Hepatitis Evaluation to Amplify Testing (HEAT) Project was launched. This initiative aims to support programs by combining epidemiological data and laboratory capacity assessments with a modeling tool to inform the development of national hepatitis B and/or hepatitis C testing and treatment strategies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.