Global Heat Pump Market

Market Size in USD Billion

USD

88.50 Billion

USD

184.26 Billion

2024

2032

USD

88.50 Billion

USD

184.26 Billion

2024

2032

| 2025 - 2032 | |

| USD 88.50 Billion | |

| USD 184.26 Billion | |

| % | |

|

Heat Pumps Market Size

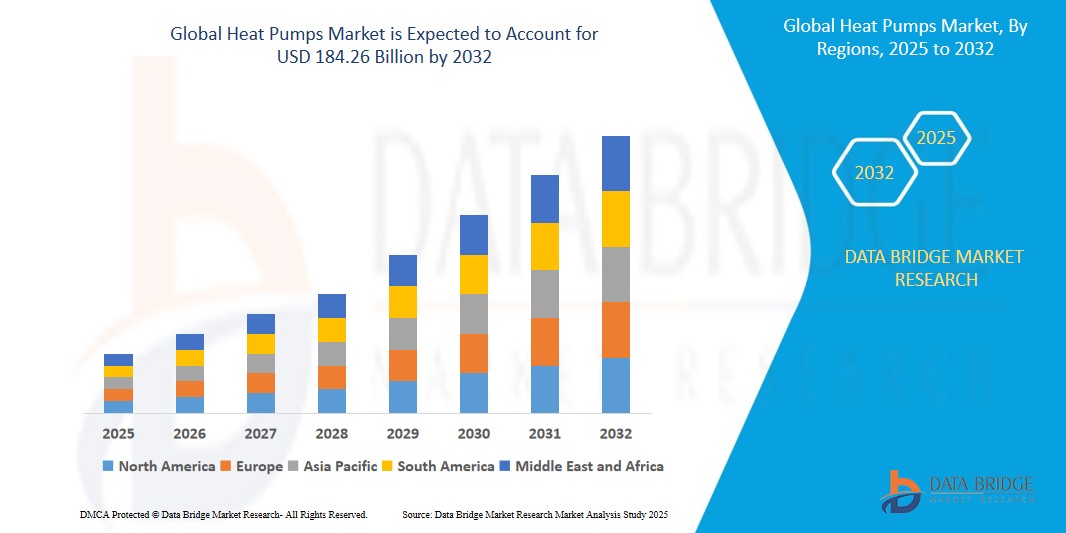

- The global Heat Pumps market size was valued at USD 88.50 billion in 2024 and is expected to reach USD 184.26 billion by 2032, at a CAGR of 9.6% during the forecast period

- This substantial growth is primarily driven by the increasing demand for energy-efficient heating and cooling solutions, rising global emphasis on decarbonization, and the growing adoption of renewable energy technologies in residential and commercial buildings. The surge in construction activities, coupled with advancements in heat pump technologies, is further accelerating market expansion.

- The global commitment to sustainability, supported by significant investments in green building initiatives, government incentives promoting energy efficiency, and a strong presence of leading HVAC manufacturers, is a key contributor to the market’s upward trajectory. Additionally, the growing integration of heat pumps in industrial applications, smart homes, and district heating systems is driving significant demand for advanced heat pump solutions worldwide.

Heat Pumps Market Analysis

- Heat pumps are energy-efficient systems that transfer heat from one location to another, providing heating, cooling, and hot water for various applications. These systems, including air-to-air, air-to-water, water-source, ground-source, and hybrid heat pumps, are critical for applications in residential heating, commercial HVAC, industrial processes, and hospitality sectors.

- The market is significantly fueled by the global push for energy efficiency, with buildings accounting for 30% of global energy consumption in 2023, driving demand for heat pumps to reduce carbon footprints. The rapid adoption of smart home technologies, with over 500 million smart homes projected by 2027, increases demand for heat pumps integrated with IoT and automation systems.

- Technological advancements, such as inverter-driven compressors, low-GWP refrigerants, and hybrid heat pump systems, are enhancing efficiency, performance, and environmental sustainability, supporting applications in cold climates and high-demand industrial settings. Government initiatives, such as the EU’s REPowerEU plan and the U.S. Inflation Reduction Act, are fostering innovation and adoption through subsidies and regulatory support.

- Europe dominates the market with a commanding 38.7% revenue share in 2024, valued at USD 34.25 billion, driven by stringent energy efficiency regulations and widespread adoption in residential and commercial sectors. Asia-Pacific is expected to witness the fastest growth rate, with a projected CAGR of 10.5% from 2025 to 2032, propelled by rapid urbanization and government support in China and Japan.

- Among product types, the air-to-air heat pumps segment held the largest market share of 45.2% in 2024, valued at USD 39.98 billion, attributed to their cost-effectiveness, ease of installation, and widespread use in residential and small commercial applications.

Report Scope and Heat Pumps Market Segmentation

|

Attributes |

Heat Pumps Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.

|

Heat Pumps Market Trends

“Low-GWP Refrigerants, Smart Heat Pumps, Hybrid Systems, and Cold-Climate Solutions”

- The adoption of low-global warming potential (GWP) refrigerants, such as R32 and R454B, is a prominent trend, with over 30% of new heat pump deployments in 2024 using eco-friendly refrigerants, aligning with global environmental regulations like the EU F-Gas Regulation.

- The rise of smart heat pumps integrated with IoT and automation systems, with 25% of new installations in 2024 featuring remote control and energy monitoring, is gaining traction in residential and commercial buildings for optimized energy use.

- Increasing focus on hybrid heat pump systems, with 15% of new deployments in 2024 combining heat pumps with gas boilers, offering flexibility and cost savings in regions with fluctuating energy prices.

- The adoption of cold-climate heat pumps is growing rapidly, with a 20% increase in demand in 2024, driven by advancements in inverter technology and enhanced performance in sub-zero temperatures, particularly in Europe and North America.

- Integration of heat pumps with renewable energy sources, such as solar panels and geothermal systems, is expanding, with 18% of new installations in 2024 designed for hybrid renewable energy applications in residential and industrial settings.

- Growing consumer demand for energy-efficient and sustainable heating solutions, driven by rising energy costs and environmental awareness, is fueling innovation in heat pump designs and applications worldwide.

Heat Pumps Market Dynamics

Driver

“Energy Efficiency Demand, Decarbonization Goals, Urbanization, Government Incentives, and Technological Advancements”

- The growing demand for energy-efficient heating and cooling solutions, with buildings consuming 40% of global energy in 2023, drives significant adoption of heat pumps to reduce energy costs and carbon emissions in residential and commercial sectors.

- The global push for decarbonization, with over 70 countries committing to net-zero emissions by 2050, fuels the need for heat pumps as a sustainable alternative to fossil fuel-based heating systems.

- Rapid urbanization and construction activities, with global construction output projected to reach USD 15 trillion by 2030, increase demand for heat pumps in new residential, commercial, and industrial buildings.

- Government incentives, such as the EU’s REPowerEU plan, the U.S. Inflation Reduction Act, and China’s carbon neutrality policies, provide substantial subsidies, tax credits, and regulatory support for heat pump adoption, fostering market growth.

- Advancements in heat pump technologies, such as inverter-driven compressors, low-GWP refrigerants, and smart controls, enhance efficiency, reliability, and performance, enabling applications in diverse climates and high-demand settings.

- The rising demand for smart home and building automation, with 65% of new residential buildings in 2023 incorporating smart HVAC systems, drives the integration of heat pumps with IoT and energy management platforms.

Restraint/Challenge

“High Installation Costs, Skilled Labor Shortages, Energy Price Volatility, Regulatory Compliance, and Consumer Awareness”

- The high upfront cost of heat pump installation, particularly for ground-source and hybrid systems, poses a challenge to adoption among cost-sensitive consumers and small businesses, limiting market scalability.

- Shortages of skilled labor for heat pump installation and maintenance, with a projected deficit of 300,000 HVAC technicians globally by 2026, pose challenges to implementation and service quality in key markets.

- Volatility in energy prices, particularly in regions dependent on electricity for heat pumps, increases operational costs for end-users, impacting adoption rates in price-sensitive markets.

- Stringent regulatory requirements, such as the EU F-Gas Regulation and U.S. EPA refrigerant standards, increase compliance costs and complexity for manufacturers, particularly in transitioning to low-GWP refrigerants.

- Rapid technological obsolescence, driven by continuous advancements in heat pump efficiency and refrigerants, pressures manufacturers to invest heavily in R&D, reducing profitability for smaller players.

- Limited consumer awareness about heat pump benefits, particularly in developing regions, creates challenges for market penetration and adoption, requiring extensive education and marketing efforts.

Heat Pumps Market Scope

The Global Heat Pump Market is segmented based on product type, technology, application, end-user, distribution channel.

- By Product Type

On the basis of product type, the market is segmented by air-to-air heat pumps, air-to-water heat pumps, water-source heat pumps, ground-source heat pumps, and hybrid heat pumps. The air-to-air heat pumps segment dominated with a 45.2% revenue share in 2024, valued at USD 39.98 billion, driven by their cost-effectiveness and widespread use in residential and small commercial applications.

The ground-source heat pumps segment is expected to grow at the fastest CAGR of 10.8% from 2025 to 2032, fueled by their high efficiency and growing adoption in sustainable buildings.

- By Technology

On the basis of technology, the market is segmented by electric heat pumps and gas-driven heat pumps. The electric heat pumps segment held the largest share of 82.5% in 2024, driven by their energy efficiency and compatibility with renewable energy sources. The gas-driven heat pumps segment is expected to grow at the fastest CAGR of 9.9% from 2025 to 2032, fueled by demand in regions with access to natural gas.

- By Application

On the basis of application, the market is segmented by residential, commercial, and industrial. The residential segment accounted for the largest revenue share of 55.6% in 2024, driven by demand for heating and cooling in households. The industrial segment is expected to grow at the fastest CAGR of 10.3% from 2025 to 2032, fueled by adoption in manufacturing and process heating.

- By End-User

On the basis of end-user, the market is segmented by households, commercial buildings, manufacturing facilities, hospitality, and others. The households segment dominated with a 50.8% revenue share in 2024, driven by residential heating and cooling demand.

The commercial buildings segment is expected to grow at the fastest CAGR of 10.1% from 2025 to 2032, fueled by green building initiatives.

- By Distribution Channel

On the basis of distribution channel, the market is segmented by direct sales, distributors, and online retail. The distributors segment held the largest share of 60.3% in 2024, driven by established HVAC supply chains.

The online retail segment is expected to grow at the fastest CAGR of 11.0% from 2025 to 2032, fueled by e-commerce growth.

Heat Pumps Market Regional Analysis

Europe Heat Pump Market Insight

Europe led the market with a commanding 38.7% revenue share in 2024, valued at USD 34.25 billion, driven by stringent energy efficiency regulations, widespread adoption in residential and commercial buildings, and strong government support. The region’s focus on decarbonization, led by the EU’s REPowerEU plan, solidifies its dominance in the global heat pump market.

Germany Heat Pump Market Insight

Germany held the largest individual country share within Europe in 2024, driven by its leadership in energy-efficient building technologies and significant government subsidies for heat pump installations. The country’s Energiewende initiative and demand for heat pumps in residential and industrial applications fuel market growth.

France Heat Pump Market Insight

France accounted for a significant portion of the European market in 2024, supported by its focus on renewable energy and green building standards. Government incentives like MaPrimeRénov’ and demand for air-to-water heat pumps in residential sectors drive market expansion.

Asia-Pacific Heat Pump Market Insight

Asia-Pacific is poised to grow at the fastest CAGR of 10.5% from 2025 to 2032, driven by rapid urbanization, increasing construction activities, and government support for energy efficiency. The region accounted for 32.4% of the market in 2024, with strong demand in China and Japan, supported by key players like Daikin and Mitsubishi Electric.

China Heat Pump Market Insight

China led the Asia-Pacific market in 2024, driven by its massive construction sector, government policies promoting carbon neutrality, and growing adoption of heat pumps in residential and commercial buildings. The country’s focus on renewable energy integration supports market growth.

Japan Heat Pump Market Insight

Japan held a notable share in 2024, driven by its leadership in energy-efficient technologies and high demand for air-to-water heat pumps in residential applications. Government subsidies and a strong HVAC industry contribute to market expansion.

North America Heat Pump Market Insight

North America held a 22.8% market share in 2024, driven by increasing demand for energy-efficient HVAC systems and government incentives. The region’s focus on sustainable building practices and cold-climate heat pump adoption, particularly in the United States, supports market growth.

United States Heat Pump Market Insight

The United States led the North American market in 2024, driven by the Inflation Reduction Act’s tax credits and rebates for heat pump installations. Demand for air-to-air and ground-source heat pumps in residential and commercial buildings fuels market growth.

Canada Heat Pump Market Insight

Canada accounted for a growing share in 2024, supported by its focus on energy efficiency and cold-climate heat pump adoption. Government programs like the Canada Greener Homes Grant drive demand in residential sectors.

Heat Pumps Market Share

- The Heat Pumps industry is primarily led by well-established companies, including:

- Daikin Industries, Ltd. (Japan)

- Mitsubishi Electric Corporation (Japan)

- Carrier Global Corporation (United States)

- Trane Technologies plc (Ireland)

- LG Electronics Inc. (South Korea)

- Panasonic Corporation (Japan)

- NIBE Industrier AB (Sweden)

- Bosch Thermotechnology (Germany)

- Vaillant Group (Germany)

- Danfoss A/S (Denmark)

- Lennox International Inc. (United States)

- Fujitsu General Limited (Japan)

- Stiebel Eltron GmbH & Co. KG (Germany)

- Gree Electric Appliances, Inc. (China)

- Midea Group Co., Ltd. (China)

- Hitachi, Ltd. (Japan)

Latest Developments in Global Heat Pumps Market

- In November 2023, Daikin Industries introduced the Altherma 4 air-to-water heat pump, engineered to deliver high energy efficiency with an eco-friendly R32 refrigerant. The unit offers a 20% improvement in operational efficiency compared to previous models and has been adopted in over 100 residential projects across Europe. This launch reinforces Daikin’s commitment to sustainable home heating solutions.

- In January 2024, Mitsubishi Electric rolled out the Ecodan Smart heat pump, featuring integrated IoT-enabled controls for real-time monitoring and energy optimization. This innovation reduces energy consumption by 15%, providing an efficient solution for modern smart homes. The product has quickly gained market traction in Japan and North America, particularly among energy-conscious consumers.

- In March 2024, Carrier Global Corporation announced a strategic partnership with Bosch to co-develop hybrid heat pumps for commercial applications. Designed for flexibility and reduced environmental impact, the new systems cut emissions by up to 25%. Deployed in both the U.S. and Germany, the partnership aims to address growing demand for sustainable HVAC solutions in commercial real estate.

- In June 2024, NIBE Industrier launched a next-generation ground-source heat pump equipped with inverter technology, specifically designed for high efficiency in colder climates. The unit improves heating performance by 18% and has already been adopted in residential and institutional projects across Sweden and Canada, solidifying NIBE’s position in the geothermal heating segment.

- In August 2024, LG Electronics introduced a new air-to-air heat pump featuring a low Global Warming Potential (GWP) refrigerant, fully certified for EU F-Gas compliance. This environmentally friendly solution is optimized for residential use and is gaining popularity in eco-conscious markets such as France and the UK, supporting the transition to greener home energy systems.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Heat Pump Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Heat Pump Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Heat Pump Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.