Global Handheld Surgical Instruments Market

Market Size in USD Billion

CAGR :

%

USD

5.65 Billion

USD

9.57 Billion

2024

2032

USD

5.65 Billion

USD

9.57 Billion

2024

2032

| 2025 –2032 | |

| USD 5.65 Billion | |

| USD 9.57 Billion | |

| % | |

|

Handheld Surgical Instruments Market Size

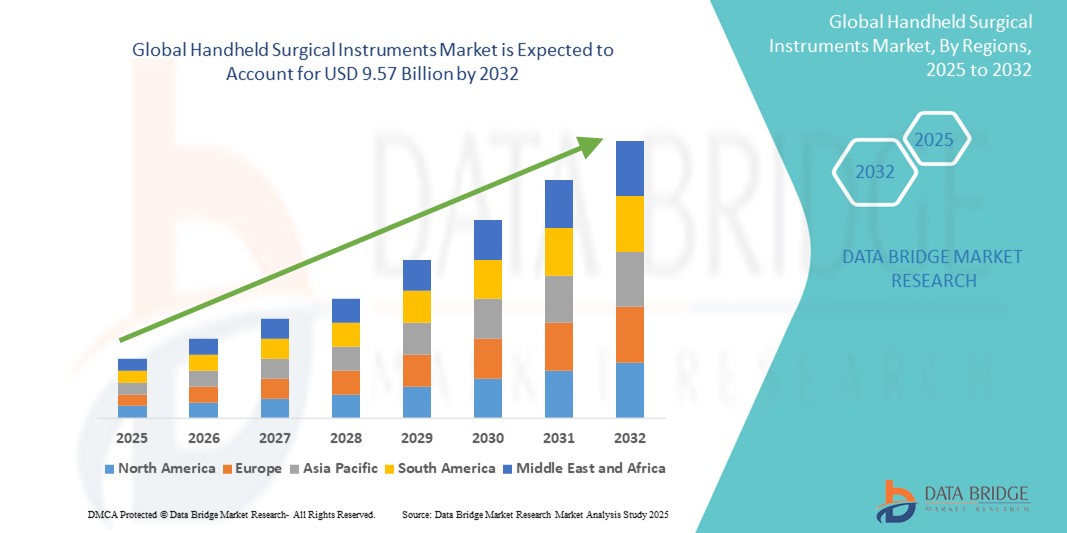

- The global handheld surgical instruments market size was valued at USD 5.65 billion in 2024 and is expected to reach USD 9.57 billion by 2032, at a CAGR of 6.81% during the forecast period

- The market growth is largely fueled by the increasing volume of surgical procedures worldwide, driven by rising incidences of chronic diseases, trauma cases, and age-related conditions, which continue to boost the demand for reliable and precision-driven surgical tools

- Furthermore, rising preference for minimally invasive surgeries, advancements in ergonomic design, and growing investments in healthcare infrastructure are establishing handheld surgical instruments as essential components in modern operating rooms. These converging factors are accelerating the adoption of handheld surgical tools, thereby significantly boosting the industry's growth

Handheld Surgical Instruments Market Analysis

- Handheld surgical instruments, used for performing various surgical tasks such as cutting, dissecting, grasping, and suturing, are increasingly vital tools across numerous surgical specialties in both inpatient and outpatient settings due to their precision, ease of use, and adaptability in minimally invasive as well as open procedures

- The escalating demand for handheld surgical instruments is primarily fueled by the rising number of surgical interventions globally, growing geriatric population, and increasing prevalence of chronic illnesses necessitating operative treatment

- North America dominated the handheld surgical instruments market with the largest revenue share of 40.1% in 2024, characterized by advanced healthcare infrastructure, high surgical procedure volume, and strong presence of major medical device manufacturers, with the U.S. leading due to continuous innovation in surgical tools and increasing focus on surgical efficiency and patient outcomes

- Asia-Pacific is expected to be the fastest growing region in the handheld surgical instruments market during the forecast period due to expanding healthcare access, medical tourism growth, and increasing investment in hospital infrastructure

- Forceps segment dominated the handheld surgical instruments market with a market share of 36.3% in 2024, driven by their broad utility across surgical disciplines, cost-effectiveness, and essential role in tissue handling and wound closure

Report Scope and Handheld Surgical Instruments Market Segmentation

|

Attributes |

Handheld Surgical Instruments Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Handheld Surgical Instruments Market Trends

“Surge in Demand for Minimally Invasive and Robotic-Assisted Procedures”

- A significant and accelerating trend in the global handheld surgical instruments market is the increasing adoption of minimally invasive surgeries (MIS) and robotic-assisted procedures. This shift is transforming surgical practices across multiple specialties, favoring precision, faster recovery, and reduced patient trauma

- For instance, instruments such as laparoscopic scissors and graspers are seeing increased usage due to their compatibility with advanced MIS techniques. Similarly, companies such as B. Braun and Medtronic are developing ergonomically optimized and reusable surgical tools specifically designed for minimally invasive environments

- The integration of handheld instruments with robotic-assisted systems enables enhanced surgeon control and improved patient outcomes. Many instruments now come equipped with modular designs that allow seamless interchangeability during procedures, offering greater flexibility and efficiency in the operating room

- Furthermore, innovations in material science such as the use of high-grade stainless steel, titanium, and antimicrobial coatings are improving instrument durability, precision, and infection control. Advanced forceps and needle holders now incorporate textured grips and ergonomic handles, significantly enhancing surgeon comfort and control during long procedures

- This trend toward more advanced, ergonomic, and adaptable surgical tools is reshaping expectations in both developed and emerging markets. Companies such as Integra LifeSciences and Stryker are increasingly focusing on customizable and surgeon-specific toolkits to support surgical efficiency and precision

- The growing demand for tools compatible with image-guided and endoscopic systems across disciplines such as orthopedics, cardiology, and neurology continues to fuel innovation in the handheld surgical instruments segment

Handheld Surgical Instruments Market Dynamics

Driver

“Rising Surgical Volume and Expanding Healthcare Access”

- The increasing global burden of chronic diseases, trauma, and age-related conditions is driving a surge in surgical interventions, fueling demand for high-quality handheld surgical instruments

- For instance, in 2024, Zimmer Biomet expanded its surgical instruments portfolio with the launch of advanced orthopedic instruments designed for both traditional and MIS procedures demonstrating how key players are innovating to meet rising deman

- In addition, the expansion of healthcare services in emerging economies, along with growing investments in hospital infrastructure and surgical training programs, is contributing to broader instrument utilization in both public and private healthcare settings

- As the number of ambulatory surgical centers and outpatient procedures increases, the need for portable, efficient, and sterilizable instruments becomes even more critical, positioning handheld surgical instruments as essential components of modern healthcare delivery

- The trend toward value-based care and outcome-focused healthcare systems is also boosting demand for instruments that enhance surgical efficiency, reduce complications, and support faster patient recovery

Restraint/Challenge

“Sterilization and Reusability Concerns Amid Cost Pressures”

- Despite their essential role, handheld surgical instruments face challenges related to sterilization, reuse, and cost containment, particularly in low-resource settings or high-volume facilities. Improper reprocessing can lead to contamination risks and surgical site infections, raising concerns about patient safety

- For instance, several global healthcare institutions have reported increased scrutiny around sterilization practices, especially for complex instruments with intricate designs that are harder to clean thoroughly

- In addition, rising regulatory standards surrounding surgical instrument validation and maintenance are placing pressure on healthcare providers to invest in advanced sterilization equipment and rigorous reprocessing protocols

- While reusable instruments offer long-term cost benefits, the initial acquisition cost remains high, especially for high-precision tools. On the other hand, single-use instruments help mitigate infection risks but raise concerns around medical waste and recurring procurement expenses

- Overcoming these challenges will require balancing cost-efficiency with safety and regulatory compliance, through innovations in instrument design, materials, and sterilization technology enabling broader adoption across diverse healthcare settings

Handheld Surgical Instruments Market Scope

The market is segmented on the basis of product, application, and end user.

- By Product

On the basis of product, the handheld surgical instruments market is segmented into forceps, retractors, dilators, graspers, scalpels, cannulas, dermatomes, trocars, and others. The forceps segment dominated the market with the largest market revenue share of 36.3% in 2024, driven by its essential role across a wide range of surgical procedures, including tissue manipulation, dissection, and suturing. Surgeons rely heavily on forceps for their versatility, ergonomic design, and consistent performance, making them a staple in operating rooms worldwide. Continued innovation in single-use and reusable forceps with enhanced grip and precision has further supported market growth.

The graspers segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by the rising adoption of minimally invasive and laparoscopic surgeries. Graspers are crucial for holding and maneuvering delicate tissues and organs, especially in confined surgical environments. Their integration into advanced MIS toolkits and robotic-assisted procedures is driving increasing demand across specialties such as gynecology, general surgery, and urology.

- By Application

On the basis of application, the handheld surgical instruments market is segmented into neurosurgery, cardiovascular, orthopaedic, plastic and reconstructive surgery, obstetrics and gynaecology, wound care, audiology, thoracic surgery, urology, and others. The orthopaedic segment held the largest share in 2024 due to the high volume of joint replacements, fracture repairs, and trauma-related surgeries. The growing elderly population and increasing sports-related injuries globally are also contributing to consistent demand for handheld surgical instruments in orthopaedics.

The plastic and reconstructive surgery segment is projected to experience the fastest CAGR from 2025 to 2032, driven by the increasing number of cosmetic and aesthetic procedures worldwide. Rising demand for precision instruments with delicate handling capabilities and enhanced control is fueling product development in this segment.

- By End User

On the basis of end user, the handheld surgical instruments market is segmented into hospitals, clinics, ambulatory surgical centres, and others. The hospitals segment dominated the market in 2024, accounting for the highest revenue share due to their broad procedural capabilities, high patient inflow, and access to advanced surgical tools. Hospitals are the primary centers for complex surgeries and emergency interventions, leading to continuous procurement of diverse surgical instruments.

The ambulatory surgical centres (ASCs) segment is expected to register the fastest growth from 2025 to 2032. The increasing shift towards outpatient procedures, coupled with the need for cost-effective and time-efficient surgeries, is boosting the demand for high-quality, portable surgical instruments in ASCs. These centres benefit from lower overhead costs and quicker turnover rates, making them a rapidly expanding avenue for instrument manufacturers

Handheld Surgical Instruments Market Regional Analysis

- North America dominated the handheld surgical instruments market with the largest revenue share of 40.1% in 2024, characterized by advanced healthcare infrastructure, high surgical procedure volume, and strong presence of major medical device manufacturers

- Healthcare providers in the region prioritize the use of precision-driven, ergonomic, and reusable surgical tools to support a wide range of complex and minimally invasive procedures

- This widespread adoption is further supported by favorable reimbursement policies, increasing healthcare expenditure, and ongoing technological advancements in surgical instruments, establishing North America as a key hub for both innovation and utilization in the handheld surgical instruments market

U.S. Handheld Surgical Instruments Market Insight

The U.S. handheld surgical instruments market captured the largest revenue share of 83% in 2024 within North America, fueled by the high volume of surgical procedures and well-established healthcare infrastructure. The nation’s growing elderly population, coupled with increased prevalence of chronic diseases, drives the demand for both traditional and minimally invasive surgical instruments. Strong presence of key medical device companies, continuous technological innovations, and robust investments in surgical training and hospital modernization further propel market expansion.

Europe Handheld Surgical Instruments Market Insight

The Europe handheld surgical instruments market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising surgical interventions and the region’s strong emphasis on healthcare quality and safety standards. Aging populations and rising demand for orthopedic, cardiovascular, and reconstructive procedures are fueling market growth. In addition, the region’s push toward reusable, precision-based instruments and growing preference for day-care surgeries contribute to the increasing demand across both public and private healthcare institutions.

U.K. Handheld Surgical Instruments Market Insight

The U.K. handheld surgical instruments market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by advancements in healthcare delivery and growing demand for outpatient and elective surgeries. Rising cases of chronic illnesses, improvements in hospital infrastructure, and the National Health Service’s (NHS) focus on cost-effective surgical solutions are boosting adoption. The U.K.'s emphasis on sterilization standards and instrument traceability further promotes high-quality instrument usage across hospitals and surgical centers.

Germany Handheld Surgical Instruments Market Insight

The Germany handheld surgical instruments market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s reputation for medical innovation and adherence to strict regulatory and sterilization protocols. Germany’s leadership in surgical research and manufacturing supports strong domestic production of precision instruments. Demand is particularly strong in orthopaedic, neurosurgery, and cardiovascular procedures, with hospitals and specialty clinics favoring durable and ergonomically designed surgical tools.

Asia-Pacific Handheld Surgical Instruments Market Insight

The Asia-Pacific handheld surgical instruments market is poised to grow at the fastest CAGR of 23.4% during the forecast period of 2025 to 2032, driven by expanding access to healthcare, rising surgical volumes, and improving hospital infrastructure across countries such as China, Japan, and India. Government investments in public health, the rising number of private hospitals, and increased medical tourism are fueling demand. In addition, local manufacturing and growing awareness of sterile surgical practices are improving instrument affordability and availability across the region

Japan Handheld Surgical Instruments Market Insight

The Japan handheld surgical instruments market is gaining momentum due to its technologically advanced healthcare system and a rapidly aging population that requires frequent surgical interventions. The market benefits from high standards in surgical precision and the integration of ergonomic, lightweight tools in both traditional and robotic-assisted surgeries. Demand is particularly notable in cardiovascular, orthopedic, and neurosurgical applications, supported by Japan’s focus on high-quality, minimally invasive instruments.

India Handheld Surgical Instruments Market Insight

The India handheld surgical instruments market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to the country’s expanding healthcare sector, increased insurance penetration, and a large patient base requiring surgical care. Rapid urbanization, rising disposable income, and government initiatives to improve surgical access in rural areas are contributing to growth. The presence of cost-effective local manufacturers and growing demand for outpatient procedures in tier-1 and tier-2 cities is further boosting the market.

Handheld Surgical Instruments Market Share

The handheld surgical instruments industry is primarily led by well-established companies, including:

- Bausch Health Companies Inc. (Canada)

- B. Braun SE (Germany)

- Biotronik (Germany)

- Medtronic (Ireland)

- BD (U.S.)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- Integra LifeSciences Corporation (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Edwards Lifesciences Corporation (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Zimmer Biomet (U.S.)

- CooperSurgical, Inc. (U.S.)

- Smith+Nephew (U.K.)

- TOPCON CORPORATION (Japan)

- Novartis AG (Switzerland)

- Danaher Corporation (U.S.)

- Aspen Surgical Products, Inc. (U.S.)

- Thompson Surgical (U.S.)

- KLS Martin Group (Germany)

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.