Global Gan Power Device Market

Market Size in USD Million

CAGR :

%

USD

378.43 Million

USD

3,562.68 Million

2024

2032

USD

378.43 Million

USD

3,562.68 Million

2024

2032

| 2025 –2032 | |

| USD 378.43 Million | |

| USD 3,562.68 Million | |

| % | |

|

GaN Power Device Market Size

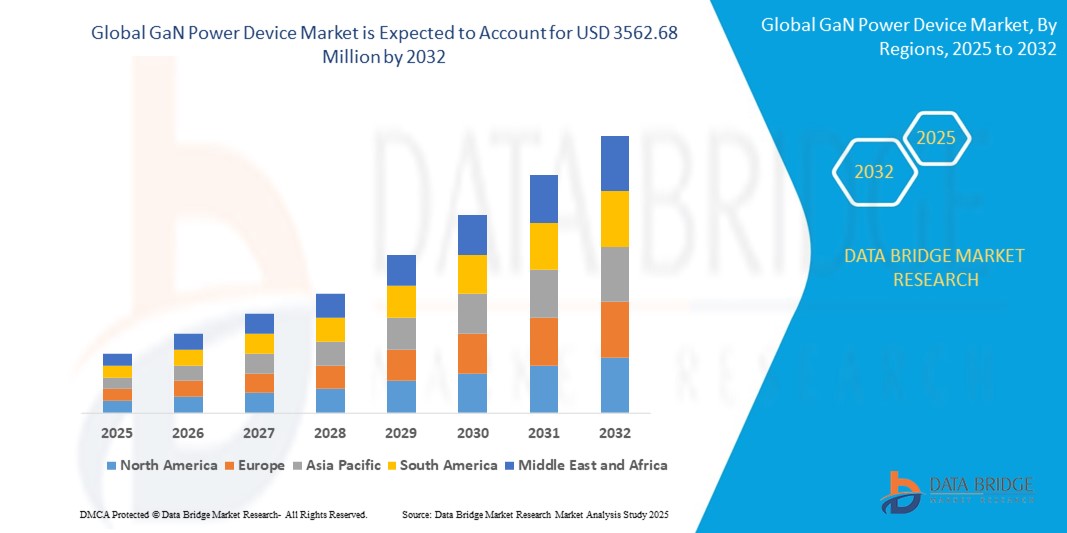

- The Global GaN Power Device Market size was valued at USD 378.43 Million in 2024 and is expected to reach USD 3562.68 Million by 2032, at a CAGR of 32.35% during the forecast period

- The market's robust expansion is primarily driven by the increasing adoption and technological advancements in connected home devices and smart home ecosystems, which are contributing to higher levels of digitalization across residential and commercial environments.

- Additionally, the surge in consumer demand for secure, intuitive, and seamlessly integrated energy and device management solutions is positioning GaN Power Devices as a preferred technology for powering modern smart systems. These overlapping trends are significantly accelerating the deployment of GaN Power Devices, ultimately propelling market growth.

GaN Power Device Market Analysis

- GaN Power Devices, known for their high efficiency and performance, are becoming increasingly essential in modern power electronics applications across residential, commercial, and industrial sectors. Their ability to enable faster switching speeds, reduced power loss, and compact system design makes them ideal for integration into smart home systems, electric vehicles, and renewable energy infrastructure.

- The rising demand for energy-efficient and compact power solutions, coupled with the growing penetration of smart home technology, is a key factor driving the adoption of GaN Power Devices. Moreover, increasing consumer awareness of advanced technologies, heightened security concerns, and the shift toward keyless, automated control systems are strengthening the market position of GaN Power Devices as an integral part of next-generation smart and secure systems.

- North America dominates the GaN Power Device Market with the largest revenue share of 32.77% in 2024, driven by the rising demand for energy-efficient solutions in power electronics, expanding deployment in EVs, 5G infrastructure, and consumer electronics, and strong R&D investments.

- The Asia-Pacific GaN Power Device Market is expected to register the fastest CAGR of 19.33% between 2025 and 2032, owing to rapid urbanization, industrialization, and the surge in consumer electronics.

- The power device segment held the largest market revenue share in 2024, driven by widespread use in high-efficiency power conversion systems. Within this, discrete power devices dominate due to their deployment in electric vehicles and industrial equipment where compact, high-speed switching is essential.

Report Scope and GaN Power Device Market Segmentation

|

Attributes |

GaN Power Device Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

GaN Power Device Market Trends

“Rising Demand for Energy-Efficient Power Solutions Across Industries”

- The global push toward energy-efficient technologies is significantly driving the adoption of Gallium Nitride (GaN) power devices across various sectors, including electric vehicles (EVs), renewable energy, industrial automation, and consumer electronics. Compared to traditional silicon-based devices, GaN devices offer superior efficiency, faster switching speeds, and smaller form factors—making them ideal for applications requiring high power density and thermal management.

- For instance, in February 2024, Infineon Technologies AG introduced a new line of GaN-based transistors targeting high-efficiency power conversion in consumer electronics and automotive charging applications. These devices reduce switching losses and heat generation, enabling lighter, smaller, and more efficient systems. Their application is particularly prominent in data centers, where power savings and compactness are crucial.

- Furthermore, with governments worldwide emphasizing carbon neutrality, industries are transitioning to energy-efficient systems. GaN’s ability to reduce energy loss during power conversion aligns well with these sustainability goals, thereby accelerating market growth.

GaN Power Device Market Dynamics

Driver

“Growing Integration of GaN Devices in 5G Infrastructure”

- The rapid global rollout of 5G networks is another major driver of the GaN Power Device Market. GaN's inherent advantages in high-frequency performance, thermal conductivity, and power efficiency make it an ideal candidate for 5G base stations, RF front-end modules, and satellite communication.

- In March 2024, Qorvo, Inc. unveiled new GaN RF solutions aimed at enhancing 5G base station performance. These devices support higher bandwidth, faster data transmission, and better heat management, all of which are critical for the densification of 5G infrastructure.

- As telecom operators increasingly require compact and reliable components to support small cell deployments and mmWave frequencies, GaN RF power devices stand out as a technologically advanced alternative to traditional LDMOS and silicon-based RF technologies.

Restraint/Challenge

“High Cost and Complex Manufacturing Process”

- Despite their advantages, GaN power devices face a major restraint in terms of cost and manufacturing complexity. Producing GaN devices involves expensive substrate materials such as silicon carbide (SiC) or sapphire and advanced fabrication techniques, which increase the overall production cost compared to silicon devices.

- Moreover, the GaN fabrication ecosystem is still maturing, with limited foundry availability and lower production yields contributing to higher unit costs. These cost factors make it challenging for GaN devices to penetrate cost-sensitive markets, such as low-end consumer electronics or budget automotive segments.

- Additionally, manufacturers must invest in new packaging technologies and thermal management systems to fully harness GaN’s capabilities, which further adds to the overall system cost. These challenges can slow down adoption, especially among small and medium-sized device manufacturers with limited R&D budgets.

GaN Power Device Market Scope

The GaN Power Device Market is segmented on the basis of device type, voltage range, application, vertical, technology, wafer material, and wafer size.

- By Device Type

On the basis of device type, the market is segmented into power device, RF power device, GaN power modules, GaN power discrete devices, and GaN power ICs. The power device segment held the largest market revenue share in 2024, driven by widespread use in high-efficiency power conversion systems. Within this, discrete power devices dominate due to their deployment in electric vehicles and industrial equipment where compact, high-speed switching is essential.

The GaN power ICs segment is projected to register the fastest CAGR from 2025 to 2032, supported by rising demand in 5G and IoT applications. Subsegments such as MMIC and hybrid ICs offer high performance and integration, appealing to designers seeking compact power solutions..

- By Voltage Range

Based on voltage range, the GaN Power Device Market is segmented into <200 Volt, 200–600 Volt, and >600 Volt. The 200–600 Volt segment captured the largest revenue share in 2024 due to its applicability across EV chargers, data centers, and industrial power supplies. These devices provide a balance between performance, thermal management, and cost.

The >600 Volt segment is anticipated to grow at the fastest CAGR through 2032, fueled by rising demand in high-voltage grid systems and electric mobility infrastructure where higher voltages improve efficiency and reduce system size.

- By Application

On the basis of application, the market is segmented into power drives, supply and inverter, and radio frequency. The supply and inverter segment accounted for the largest market revenue share in 2024, particularly in switch-mode power supply and EV charging subsegments, where GaN’s efficiency and high-frequency capabilities lower overall system costs.

The radio frequency segment is projected to see the fastest growth through 2032, with demand rising in RF front-end modules, radars, and satellite systems. These devices support next-gen telecom and defense systems by offering superior gain and power density.

- By Vertical

Based on vertical, the market is segmented into telecommunications, industrial, automotive, renewable, consumer and enterprise, military, defense and aerospace, and medical. The telecommunications segment held the highest market share in 2024, driven by the deployment of 5G base stations and data centers requiring compact and energy-efficient power amplifiers.

The automotive segment is expected to witness the fastest CAGR from 2025 to 2032, supported by growing EV penetration and the increasing need for compact, lightweight, and efficient power systems in electric drivetrains and onboard chargers.

- By Technology

On the basis of technology, the GaN Power Device Market is segmented into 4H-SiC MOSFET, HEMT, and others. The HEMT (High Electron Mobility Transistor) segment leads the market in 2024, valued for its high-frequency operation, low on-resistance, and superior thermal performance, making it ideal for both RF and power conversion applications.

- By Wafer Material

The market is segmented into GaN on SiC and GaN on Si. GaN on Si dominates the market with the highest revenue share in 2024, due to its lower production cost and suitability for high-volume consumer applications.

GaN on SiC is anticipated to grow rapidly due to its advantages in thermal conductivity and high-voltage performance, supporting applications in aerospace, defense, and satellite communication.

- By Wafer Size

Based on wafer size, the market is segmented into less than 150 mm, 150 mm–500 mm, and more than 500 mm. The 150 mm–500 mm segment held the largest share in 2024, favored for its balance of maturity and yield in mass production.

The more than 500 mm segment is expected to witness the highest CAGR through 2032 as leading fabs invest in larger wafer formats to scale production, reduce costs, and meet rising demand across EVs and industrial automation.

GaN Power Device Market Regional Analysis

- North America dominates the GaN Power Device Market with the largest revenue share of 32.77% in 2024, driven by the rising demand for energy-efficient solutions in power electronics, expanding deployment in EVs, 5G infrastructure, and consumer electronics, and strong R&D investments.

- The region’s technologically advanced landscape and growing focus on sustainable power systems are supporting the widespread adoption of GaN Power Devices. Increasing applications across defense, aerospace, and industrial automation further strengthen market growth.

- Supportive government policies, significant capital flow into semiconductor development, and the presence of leading players are creating a conducive environment for rapid growth in this region.

U.S. GaN Power Device Market Insight

The U.S. GaN Power Device Market accounted for 81% of North America’s revenue share in 2024, fueled by strong penetration of EVs, data centers, and wireless infrastructure. Increasing adoption of GaN transistors and ICs for high-frequency, high-efficiency applications is a major contributor. The U.S. is also witnessing rapid growth in renewable energy systems, where GaN devices offer compact size and superior thermal performance, further bolstering market expansion.

Europe GaN Power Device Market Insight

The Europe GaN Power Device Market is set to grow at a notable CAGR during the forecast period, driven by green energy initiatives, stringent emissions regulations, and the rising trend of electric mobility. Adoption of GaN Power Devices is gaining traction in EV charging, photovoltaic inverters, and industrial power supplies. Increasing investment in 5G and telecom infrastructure also supports the market.

U.K. GaN Power Device Market Insight

The U.K. GaN Power Device Market is projected to expand at a strong CAGR, backed by the country’s efforts to lead in clean energy and digital infrastructure. Rising demand for next-gen power electronics in aerospace and defense, as well as the transition to electrified transport, is accelerating GaN adoption. The U.K.’s strategic emphasis on reducing carbon footprints supports continued market growth.

Germany GaN Power Device Market Insight

The Germany GaN Power Device Market is anticipated to grow significantly due to its position as a key hub for automotive and industrial innovation. High focus on EV development, grid stability, and IoT integration fuels the use of GaN components in power converters and fast-charging systems. Additionally, Germany’s leadership in smart factory automation is increasing demand for compact, high-efficiency power solutions.

Asia-Pacific GaN Power Device Market Insight

The Asia-Pacific GaN Power Device Market is expected to register the fastest CAGR of 19.33% between 2025 and 2032, owing to rapid urbanization, industrialization, and the surge in consumer electronics. Countries like China, Japan, South Korea, and India are at the forefront of semiconductor production and are heavily investing in EVs, 5G, and AI technologies that require GaN-based power solutions.

Japan GaN Power Device Market Insight

The Japan GaN Power Device Market is expanding steadily, driven by the nation’s focus on miniaturization and energy conservation. GaN devices are increasingly deployed in automotive electronics, consumer appliances, and robotics. With a high-tech manufacturing ecosystem and strong demand for low-loss, high-efficiency components, Japan is poised to be a major contributor to regional growth.

China GaN Power Device Market Insight

The China GaN Power Device Market held the largest revenue share in Asia-Pacific in 2024, supported by massive investments in smart manufacturing, electric mobility, and telecommunications. China's aggressive push toward smart city development, coupled with strong government support for the domestic semiconductor industry, is accelerating GaN adoption. The presence of major OEMs and ODMs further enhances market penetration across sectors.

GaN Power Device Market Share

The GaN Power Device industry is primarily led by well-established companies, including:

- Cree, Inc. (now Wolfspeed)(United States)

- Infineon Technologies AG(Germany)

- Qorvo, Inc.(United States)

- MACOM(United States)

- Microsemi (part of Microchip Technology)(United States)

- Mitsubishi Electric Corporation (Japan)

- Efficient Power Conversion Corporation (EPC)(United States)

- GaN Systems(Canada)

- Navitas Semiconductor(United States)

- Toshiba Electronic Devices & Storage Corporation(Japan)

- Exagan (France)

- VisIC Technologies(Israel)

- Integra Technologies, Inc.(United States)

- Transphorm Inc.(United States)

- GaNpower(China)

- Analog Devices, Inc.(United States)

- Panasonic Corporation (Japan)

- Texas Instruments Incorporated (United States)

- Ampleon(Netherlands)

- Northrop Grumman(United States)

- Dialog Semiconductor (part of Renesas) (United Kingdom)

Latest Developments in Global GaN Power Device Market

- In April 2024, Infineon Technologies AG launched a new portfolio of high-efficiency GaN power transistors designed to enhance power conversion efficiency in electric vehicles and renewable energy systems. This initiative underscores Infineon’s focus on advancing sustainable energy solutions by leveraging GaN technology to reduce energy losses and improve thermal management in critical applications.

- In March 2024, Qorvo, Inc. introduced its next-generation GaN RF power devices optimized for 5G infrastructure, supporting higher frequency bands and increased power density. This development reflects Qorvo’s commitment to enabling faster and more reliable wireless communication networks as global 5G adoption accelerates.

- In February 2024, Navitas Semiconductor announced a strategic collaboration with a leading EV manufacturer to integrate GaN power ICs into onboard chargers and inverters. This partnership aims to deliver faster charging times and improved vehicle efficiency, driving innovation in the electric vehicle market.

- In January 2024, GaN Systems unveiled a new compact GaN power module tailored for consumer electronics and fast wireless charging applications. The module’s small form factor and high efficiency cater to the growing demand for lightweight and portable charging solutions.

- In January 2024, Mitsubishi Electric Corporation expanded its GaN device manufacturing capabilities by investing in a new fabrication facility focused on silicon carbide (SiC) wafer substrates. This expansion is intended to meet increasing demand for high-performance GaN power devices across industrial and automotive sectors.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Gan Power Device Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Gan Power Device Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Gan Power Device Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.