Global Frozen Vegetables Market

Market Size in USD Billion

CAGR :

%

USD

21.35 Billion

USD

31.74 Billion

2024

2032

USD

21.35 Billion

USD

31.74 Billion

2024

2032

| 2025 –2032 | |

| USD 21.35 Billion | |

| USD 31.74 Billion | |

| % | |

|

Frozen Vegetables Market Size

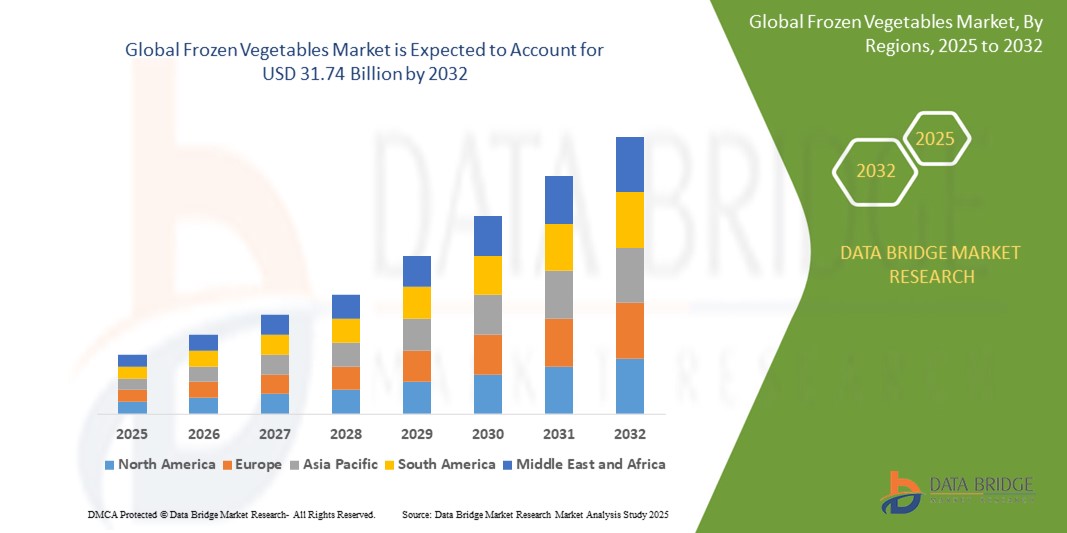

- The global frozen vegetables market size was valued at USD 21.35 billion in 2024 and is expected to reach USD 31.74 billion by 2032, at a CAGR of 5.08% during the forecast period

- The market growth is primarily driven by increasing consumer demand for convenient, long-shelf-life food products, rising awareness of nutritional benefits, and the growing popularity of plant-based diets

- Growing consumer preference for healthy and time-saving meal solutions, coupled with advancements in freezing technologies, is further propelling demand for frozen vegetables across both retail and food service sectors

Frozen Vegetables Market Analysis

- The frozen vegetables market is experiencing robust growth due to rising consumer demand for nutritious, easy-to-prepare food options and the expansion of cold chain infrastructure globally

- Increasing adoption in both premium and budget-conscious consumer segments is encouraging manufacturers to innovate with organic, non-GMO, and value-added frozen vegetable products

- North America holds the largest revenue share of 35.2% in 2024, driven by a well-established food processing industry, high consumer awareness of health benefits, and widespread retail availability

- Asia-Pacific is projected to be the fastest-growing region during the forecast period, fueled by rapid urbanization, increasing disposable incomes, and growing demand for convenient food products in countries such as China, India, and Southeast Asian nations

- The peas segment dominates the largest market revenue share of 35.6% in 2024, driven by their widespread use in various cuisines, long shelf life, and ease of incorporation into meals

Report Scope and Frozen Vegetables Market Segmentation

|

Attributes |

Frozen Vegetables Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Frozen Vegetables Market Trends

“Rising Preference for Organic Frozen Vegetables”

- Organic frozen vegetables are gaining traction due to increasing consumer demand for healthier, chemical-free food options

- These products retain nutritional value and flavor, appealing to health-conscious consumers seeking convenience without compromising quality

- In regions with busy lifestyles, such as the U.S. and Europe, organic frozen vegetables are favored for their long shelf life and ease of preparation

- Premium and health-focused brands are increasingly offering organic frozen vegetable options to cater to this demand

- For instance, companies such as Birds Eye and Cascadian Farm offer organic frozen vegetable ranges, emphasizing sustainability and quality

- Retailers are incorporating organic frozen vegetable bundles in meal kits and subscription services to attract eco-conscious buyers

Frozen Vegetables Market Dynamics

Driver

“Growing Demand for Convenience and Nutritional Food Options”

- Rising consumer awareness about the benefits of nutrient-rich diets is driving demand for frozen vegetables, which retain vitamins and minerals through quick-freezing technology

- Frozen vegetables offer convenience for time-pressed consumers, reducing prep time while maintaining nutritional quality, making them popular in urban areas such as the U.S., Europe, and India

- These products contribute to healthier eating habits by providing year-round access to a variety of vegetables, regardless of seasonal availability

- Food service industries, such as restaurants and catering services, are increasingly adopting frozen vegetables to streamline operations and reduce food waste

- For instance, major fast-food chains such as McDonald’s use frozen vegetables in select menu items to ensure consistency and quality

- The rise of plant-based diets and veganism is further fueling the adoption of frozen vegetables, as they serve as versatile ingredients for meat-free meals, enhancing market growth

Restraint/Challenge

“Regulatory Restrictions on Food Safety and Labeling”

- Stringent regulations on food safety, storage, and labeling standards can limit market growth and complicate compliance for manufacturers and distributors

- Different countries have varying requirements for frozen food labeling, including nutritional content and organic certification, creating challenges for global standardization

- Non-compliance with safety standards, such as improper freezing or contamination risks, can lead to product recalls, damaging brand reputation

- For instance, the European Union and U.S. enforce strict guidelines on frozen food storage temperatures, requiring consistent cold chain logistics

- These regulations increase operational costs for manufacturers and may deter smaller players from entering the market, limiting overall market expansion

Frozen Vegetables Market Scope

The market is segmented on the basis of type, distribution channel, end user, and nature.

- By Type

On the basis of type, the global frozen vegetables market is segmented into beans, corn, peas, mushroom, cauliflower, green beans, asparagus, broccoli, carrot, potato, and others. The peas segment dominates the largest market revenue share of 35.6% in 2024, driven by their widespread use in various cuisines, long shelf life, and ease of incorporation into meals. Peas are favored for their nutritional value and versatility in both home cooking and food service applications. The market also sees strong demand for peas due to their availability in multiple packaging formats and compatibility with diverse dietary preferences.

The broccoli segment is anticipated to witness the fastest growth rate of 19.8% from 2025 to 2032, fueled by increasing consumer awareness of its health benefits, including high vitamin and antioxidant content. Broccoli’s rising popularity in plant-based diets and its use in ready-to-eat meals and meal kits contribute to its rapid market expansion.

- By Distribution Channel

On the basis of distribution channel, the global frozen vegetables market is segmented into direct and indirect. The indirect segment, encompassing supermarkets, hypermarkets, and online retailers, held the largest market revenue share in 2024, driven by the widespread availability of frozen vegetables in retail stores and the growing popularity of e-commerce platforms. Indirect channels offer convenience, a wide variety of products, and competitive pricing, making them a preferred choice for consumers.

The direct segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the rise of farm-to-table models and direct-to-consumer sales through farmers' markets and subscription-based services. Direct channels appeal to consumers seeking fresher, locally sourced frozen vegetables with transparent supply chains.

- By End User

On the basis of end user, the global frozen vegetables market is segmented into food service industry and retail customers. The retail customers segment held the largest market revenue share in 2024, driven by the increasing demand for convenient, time-saving meal solutions among households. The growing trend of home cooking, coupled with the need for long-shelf-life products, boosts the adoption of frozen vegetables among retail consumers.

The food service industry segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the rising use of frozen vegetables in restaurants, hotels, and catering services. Frozen vegetables offer cost-effectiveness, consistent quality, and reduced preparation time, making them a preferred choice for food service providers.

- By Nature

On the basis of nature, the global frozen vegetables market is segmented into organic and conventional. The conventional segment accounted for the largest market revenue share in 2024, driven by its cost-effectiveness and widespread availability across various distribution channels. Conventional frozen vegetables remain popular due to their affordability and established supply chains catering to mass markets.

The organic segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by growing consumer preference for healthier, pesticide-free, and environmentally sustainable food options. The rising demand for organic frozen vegetables is supported by increasing awareness of clean-label products and sustainable farming practices.

Frozen Vegetables Market Regional Analysis

- North America holds the largest revenue share of 35.2% in 2024, driven by a well-established food processing industry, high consumer awareness of health benefits, and widespread retail availability

- Consumers in the region value the ease of storage, long shelf life, and nutritional retention offered by frozen vegetables

- This widespread adoption is further supported by high disposable incomes, a health-conscious population, and the growing preference for plant-based and ready-to-cook food products, establishing frozen vegetables as a favored solution for both household and food service applications

U.S. Frozen Vegetables Market Insight

The U.S. is expected to witness the fastest growth rate in the North America frozen vegetables market, driven by high consumer awareness of healthy eating habits and the convenience of frozen products. The U.S. leads the region, fueled by the growing demand for organic and non-GMO frozen vegetables, supported by well-established retail infrastructure and increasing online grocery shopping. The rise in vegan and vegetarian diets, along with innovations in product offerings such as pre-seasoned or meal-kit-style frozen vegetables, is boosting market growth.

Europe Frozen Vegetables Market Insight

The European frozen vegetables market is projected to grow at a substantial CAGR during the forecast period, driven by stringent food safety regulations and a strong emphasis on sustainable and organic food products. Increasing urbanization, coupled with busy lifestyles, is fostering the adoption of frozen vegetables for their convenience and nutritional benefits. The region sees significant demand in both household and foodservice sectors, with countries such as Germany, France, and the U.K. leading due to their robust cold chain infrastructure and preference for eco-friendly packaging.

U.K. Frozen Vegetables Market Insight

The U.K. frozen vegetables market is anticipated to grow at a noteworthy CAGR, propelled by rising health consciousness and the growing trend of plant-based diets. Concerns over food waste and the demand for sustainable, long-shelf-life products are encouraging consumers to opt for frozen vegetables. The U.K.'s well-developed retail and e-commerce sectors, combined with increasing demand for organic and locally sourced frozen produce, are expected to drive market growth.

Germany Frozen Vegetables Market Insight

The German frozen vegetables market is expected to expand at a considerable CAGR, fueled by growing consumer awareness of health, sustainability, and convenience. Germany’s advanced cold chain infrastructure and focus on innovation in food processing promote the adoption of frozen vegetables, particularly in ready-to-cook and organic segments. The integration of frozen vegetables into meal kits and the preference for eco-conscious packaging align with local consumer expectations, further driving market growth.

Asia-Pacific Frozen Vegetables Market Insight

The Asia-Pacific frozen vegetables market is poised to grow at the fastest CAGR of over 20% in 2024, driven by rapid urbanization, rising disposable incomes, and increasing demand for convenient food options in countries such as China, India, and Japan. Government initiatives promoting food security and advancements in cold chain logistics are accelerating the adoption of frozen vegetables. The region’s growing middle class and shifting dietary preferences towards healthier and plant-based foods are key factors propelling market expansion.

Japan Frozen Vegetables Market Insight

The Japan frozen vegetables market is gaining momentum due to the country’s high-tech food processing industry and increasing consumer preference for convenience. The demand for frozen vegetables is driven by Japan’s aging population, which seeks easy-to-prepare, nutritious food options. The integration of frozen vegetables into ready-to-eat meals and the focus on high-quality, minimally processed products are fueling growth. In addition, Japan’s advanced retail infrastructure and growing e-commerce platforms are enhancing market accessibility.

China Frozen Vegetables Market Insight

The China frozen vegetables market accounted for the largest revenue share in the Asia-Pacific region in 2024, driven by rapid urbanization, an expanding middle class, and growing consumer preference for convenient and healthy food options. China’s robust cold chain infrastructure and strong domestic manufacturing base for frozen foods are key growth drivers. The increasing popularity of frozen vegetables in urban households, foodservice sectors, and online retail platforms, coupled with government support for food safety and sustainability, is propelling the market forward.

Frozen Vegetables Market Share

The frozen vegetables industry is primarily led by well-established companies, including:

- Amy's Kitchen, Inc. (U.S.)

- Bellisio Foods, Inc. (U.S.)

- Conagra Brands, Inc. (U.S.)

- Findus Group (Sweden)

- Goya Foods, Inc. (U.S.)

- Kraft-Heinz, Inc. (U.S.)

- General Mills Inc. (U.S.)

- Nestlé (U.S.)

- WK Kellogg Co (U.S.)

- B&G Foods, Inc. (U.S.)

- Unilever Food Solutions (India)

- McCain Foods Limited (U.S.)

- Associated British Foods plc (U.K.)

- Ajinomoto Co,Inc. (U.S.)

- Lantmannen (Poland)

Latest Developments in Global Frozen Vegetables Market

- In April 2025, McCain Foods India partnered with Philips to launch India’s first range of frozen snacks designed exclusively for air fryers. This collaboration combines McCain’s expertise in frozen foods with Philips’ pioneering air fryer technology, delivering crispy fries and vegetable blends that replicate restaurant-style taste and texture at home. The Sure Crisp™ technology ensures golden crispness without deep frying, catering to the growing adoption of air fryers in modern kitchens. The launch is supported by a digital campaign, highlighting family moments and shared cooking experiences

- In March 2024, Campbell Soup Company completed the USD 2.7 billion acquisition of Sovos Brands, Inc., integrating premium frozen entrées and sauces into its portfolio. This strategic move enhances Campbell’s Meals & Beverages division, adding market-leading brands such as Rao’s, Michael Angelo’s, and Noosa. The acquisition strengthens Campbell’s presence in the frozen food market, expanding its product diversity and market reach. To drive growth, Campbell formed a Distinctive Brands unit, combining Pacific Foods with Sovos’ brands

- In March 2024, BigBasket, a TATA Enterprise, collaborated with Chef Sanjeev Kapoor to introduce Precia, a frozen foods brand featuring frozen vegetables, snacks, and sweets. Utilizing Individual Quick Freezing (IQF) technology, Precia preserves authentic flavors and nutritional value, ensuring high-quality meal solutions. The brand aims to achieve INR 100 crore in online sales by 2026, addressing the growing demand for convenient, premium frozen foods. BigBasket emphasizes ethical sourcing, partnering directly with farmers for fair compensation

- In April 2023, Nestlé and PAI Partners established a joint venture for Nestlé’s frozen pizza business in Europe, creating a dedicated player in the competitive frozen food market. The business, generating around CHF 400 million annually, operates under brands such as Wagner, Buitoni, and Garden Gourmet across Germany, Italy, France, Spain, Switzerland, Portugal, Austria, Belgium, and the Netherlands. Headquartered in Germany, the venture includes manufacturing facilities in Nonnweiler, Germany, and Benevento, Italy. Nestlé retains a non-controlling stake, ensuring continued involvement in growth and value creation

- In January 2021, Mother Dairy expanded its Safal frozen vegetable range, introducing Drumsticks and Cut Okra to cater to urban consumers seeking convenient, ready-to-cook options. These pre-cut, preservative-free vegetables offer year-round availability, aligning with the growing demand for time-saving meal solutions. The launch strengthens Mother Dairy’s retail presence, ensuring high-quality, hygienically packed frozen products. In addition, the company introduced Haldi Paste Cubes, a nutritious immunity booster made from fresh turmeric rhizomes

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Frozen Vegetables Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Frozen Vegetables Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Frozen Vegetables Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.