Circumvent the Tariff challenges with an agile supply chain Consulting

Supply Chain Ecosystem Analysis now part of DBMR Reports

Global Friction Reducers Market

Market Size in USD Billion

CAGR :

%

USD

2.28 Billion

USD

3.52 Billion

2024

2032

Forecast Period

2025 –2032

Market Size(Base Year)

USD

2.28 Billion

Market Size (Forecast Year)

USD

3.52 Billion

CAGR

%

Major Markets Players

CLARIANT

BASF SE

Croda International Plc

Evonik Industries AG

The Lubrizol Corporation

Global Friction Reducers Market Segmentation, By Type (Synthetic Friction Reducers and Organic Friction Reducers, and Combination Friction Reducers), Particle Size (Nano-scale Friction Reducers, Micro-scale Friction Reducers, and Macro-scale Friction Reducers), Ionic Charge (Anionic Friction Reducers, Cationic Friction Reducers, Non-ionic Friction Reducers, and Amphoteric Friction Reducers), Functionality (Drag Reduction and Wear Reduction), Concentration (Low Concentration and High Concentration), Form (Liquid Friction Reducers, Powder Friction Reducers, and Emulsion Friction Reducers), Application (Hydraulic Fracturing, Drilling Fluids, Stimulation Fluids, Cementing Fluids, Well Stimulation, and Enhanced Oil Recovery (EOR)), Distribution Channel (Direct Sales, Distributors/Wholesalers, Online Retailers, and Others) - Industry Trends and Forecast to 2032

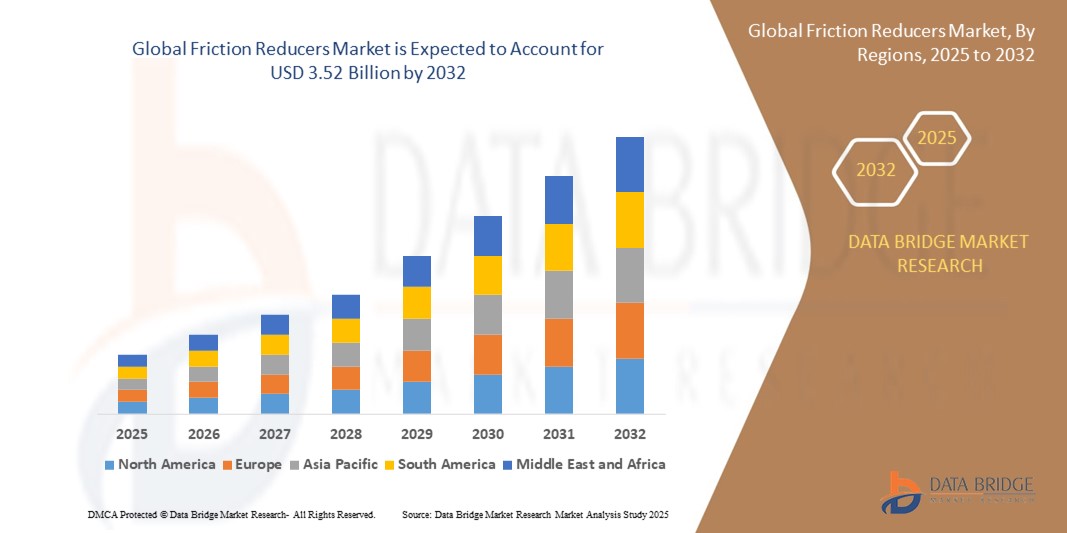

Friction Reducers Market Size

The global friction reducers market size was valued at USD 2.28 billion in 2024 and is expected to reach USD 3.52 billion by 2032,at a CAGR of 5.6% during the forecast period

The market growth is largely fuelled by the increasing demand for enhanced oil and gas recovery techniques and the rising adoption of advanced drilling technologies across key production regions

Growing emphasis on reducing energy consumption and operational costs in the oil and gas industry is driving the increased use of friction reducers, enhancing overall efficiency and productivity

Friction Reducers Market Analysis

The friction reducers market is growing steadily due to increasing demand in industries that require efficient fluid movement, such as oil and gas. Companies are focusing on developing advanced formulations to improve product performance and meet stricter industry standards

Innovation in friction reducer technologies is enhancing compatibility with different types of fluids, which is broadening their application scope. This is encouraging manufacturers to invest in research and development to stay competitive and cater to evolving market needs

North America dominated the friction reducers market with the largest revenue share of 38.5% in 2024, driven by extensive oil and gas exploration activities and the increasing adoption of advanced hydraulic fracturing technologies

Asia-Pacific region is expected to witness the highest growth rate in the global friction reducers market, driven by rapid expansion in oil and gas exploration activities, increasing hydraulic fracturing operations, and supportive government initiatives promoting energy development

The synthetic segment dominated the market with the largest revenue share of 52.5% in 2024, attributed to its high efficiency and widespread use in hydraulic fracturing operations

Report Scope and Friction Reducers Market Segmentation

Attributes

Friction Reducers Key Market Insights

Segments Covered

By Type: Synthetic Friction Reducers and Organic Friction Reducers, and Combination Friction Reducers

By Particle Size: Nano-scale Friction Reducers, Micro-scale Friction Reducers, and Macro-scale Friction Reducers

By Ionic Charge: Anionic Friction Reducers, Cationic Friction Reducers, Non-ionic Friction Reducers, and Amphoteric Friction Reducers

By Functionality: Drag Reduction and Wear Reduction

By Concentration: Low Concentration and High Concentration

By Form: Liquid Friction Reducers, Powder Friction Reducers, and Emulsion Friction Reducers

By Application: Hydraulic Fracturing, Drilling Fluids, Stimulation Fluids, Cementing Fluids, Well Stimulation, and Enhanced Oil Recovery (EOR)

By Distribution Channel: Direct Sales, Distributors/Wholesalers, Online Retailers, and Others

Rising Demand for Eco-Friendly Friction Reducers Due to Strict Regulations.

Growing Use of Advanced Polymers to Improve Fracturing Efficiency.

Value Added Data Infosets

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.

Friction Reducers Market Trends

“Growing Adoption of Environmentally Friendly Friction Reducers”

There is an increasing trend toward the development and use of eco-friendly friction reducers, driven by stricter environmental regulations and sustainability goals across industries

Manufacturers are investing in bio-based and biodegradable friction reducers to reduce the environmental impact of hydraulic fracturing and other industrial processes

For instance, companies such as Halliburton and Baker Hughes have introduced greener formulations that minimize toxic residues and improve biodegradability, catering to eco-conscious clients

The shift towards sustainable products also helps companies comply with regional regulations, such as those in North America and Europe, where environmental standards are more stringent

This trend not only supports environmental protection but also opens new market opportunities, encouraging further innovation in greener friction reducer technologies and applications

Friction Reducers Market Dynamics

Driver

“Increasing Demand for Efficient Oil and Gas Extraction Techniques”

The growing demand for enhanced oil and gas extraction efficiency is driving the friction reducers market, as these additives reduce friction between fracturing fluid and the wellbore, enabling higher flow rates and lower pumping pressures

This improved efficiency results in faster drilling times, reduced energy consumption, and lower operational costs, which is essential for maximizing profitability in energy production

Oil and gas companies are increasingly investing in advanced technologies to optimize production from existing reservoirs and unlock unconventional resources

For instance, ExxonMobil’s expansion in the Permian Basin where friction reducers support high-volume hydraulic fracturing operations

The rising use of horizontal drilling and multi-stage fracturing techniques, especially in shale-rich regions such as the U.S. Marcellus Shale, further boosts demand for friction reducers to handle complex well designs and higher fluid volumes

Friction reducers enhance fluid mobility and hydrocarbon recovery rates, making them indispensable in modern drilling operations aiming to meet growing global energy needs while controlling costs and improving sustainability

Restraint/Challenge

“Environmental Concerns and Regulatory Challenges Related to Friction Reducers”

One significant challenge for the friction reducers market is the environmental concerns related to hydraulic fracturing fluids, including friction reducers, which often contain synthetic polymers that can persist in the environment and risk soil and water quality

Despite progress in eco-friendly formulations, proper disposal and treatment of fracturing wastewater remain costly and complex, with stringent regulations increasing compliance expenses for oil and gas companies

Regulatory restrictions on chemical usage in sensitive regions can limit the application of some friction reducer types, affecting market accessibility and growth potential

Public opposition, for instance protests in regions such as Pennsylvania and the U.K. over water contamination fears, heightens pressure on the industry to develop safer, less harmful products

Manufacturers face the challenge of balancing high-performance requirements with environmental sustainability by investing in research to innovate friction reducers that reduce ecological impact while maintaining efficiency, with failure to do so risking project delays, reduced adoption, and higher operational costs

Friction Reducers Market Scope

The market is segmented on the basis of type, particle size, ionic charge, functionality, concentration, form, application, and distribution channel.

By Type

On the basis of type, the friction reducers market is segmented into synthetic friction reducers, organic friction reducers, and combination friction reducers. The synthetic segment dominated the market with the largest revenue share of 52.5% in 2024, attributed to its high efficiency and widespread use in hydraulic fracturing operations.

Organic friction reducers is expected to witness the fastest growth from 2025 to 2032, due to rising environmental concerns, while combination friction reducers are expected to grow at the fastest rate from 2025 to 2032, benefiting from their balanced performance and versatility in diverse applications.

By Particle Size

On the basis of particle size, the market is segmented into nano-scale, micro-scale, and macro-scale friction reducers. The nano-scale segment held the largest revenue share of 45.3% in 2024, driven by enhanced drag reduction properties and fluid stability. Micro-scale friction reducers maintain steady demand for cost-effective performance.

Macro-scale friction reducers is expected to witness the fastest growth from 2025 to 2032, due to their suitability in specific drilling environments requiring larger particles. Their ability to perform effectively in challenging formations makes them increasingly preferred by operators managing complex wells.

By Ionic Charge

On the basis of ionic charge, the market is segmented into anionic, cationic, non-ionic, and amphoteric friction reducers. Anionic friction reducers led the market with a 48.7% share in 2024, favored for their compatibility with high-salinity fluids.

Amphoteric friction reducers is expected to witness the fastest growth from 2025 to 2032, supported by their adaptability across varying pH levels and reservoir conditions. This versatility allows their application in diverse geographic regions and fluid chemistries, broadening market adoption.

By Functionality

On the basis of functionality, the market is divided into drag reduction and wear reduction segments. Drag reduction friction reducers commanded the largest market revenue share of 61.2% in 2024, as they improve hydraulic fracturing efficiency by lowering fluid friction.

Wear reduction friction reducers is expected to witness the fastest growth from 2025 to 2032, for protecting equipment and reducing maintenance costs, projected to witness strong growth during the forecast period. Their use contributes to prolonging equipment life and minimizing downtime, which is critical for operational efficiency.

By Concentration

On the basis of concentration, the market is segmented into low concentration and high concentration friction reducers. High concentration friction reducers held the larger share of 57.8% in 2024, preferred for their superior drag reduction over extended fracturing stages.

Low concentration types is expected to witness the fastest growth from 2025 to 2032, due to their cost-effectiveness and reduced chemical usage in certain operational scenarios. This makes them attractive for operators seeking sustainable solutions without compromising performance.

By Form

On the basis of form, the friction reducers market is segmented into liquid, powder, and emulsion types. Liquid friction reducers dominated with a 54.9% market share in 2024, valued for ease of handling and rapid dissolution in fluids.

Emulsion friction reducers is expected to witness the fastest growth from 2025 to 2032, due to their stable dispersion in fracturing fluids. Their enhanced compatibility with various fluid systems improves overall fracturing efficiency and reduces operational risks.

By Application

On the basis of application, the market is segmented into hydraulic fracturing, drilling fluids, stimulation fluids, cementing fluids, well stimulation, and enhanced oil recovery. Hydraulic fracturing accounted for the largest revenue share of 62.7% in 2024, driven by the rise of unconventional resource extraction.

Enhanced oil recovery is expected to witness the fastest growth from 2025 to 2032, as operators focus on maximizing reservoir output. Increasing demand for energy security is pushing the adoption of advanced recovery techniques that rely heavily on friction reducers.

By Distribution Channel

On the basis of distribution channel, the market is segmented into direct sales, distributors/wholesalers, online retailers, and others. Direct sales dominated the market with a share of 50.3% in 2024, due to strong manufacturer relationships with major oilfield companies.

Distributors and online retailers is expected to witness the fastest growth from 2025 to 2032, catering to wider geographic and smaller-scale customers. Their expanding reach improves accessibility of friction reducers to remote or emerging markets, driving overall market expansion.

Friction Reducers Market Regional Analysis

North America dominated the friction reducers market with the largest revenue share of 38.5% in 2024, driven by extensive oil and gas exploration activities and the increasing adoption of advanced hydraulic fracturing technologies

The region’s focus on improving extraction efficiency and reducing environmental impact encourages the use of high-performance friction reducers in shale formations

Supportive regulatory frameworks and investment in upstream technologies further bolster market growth, with major players emphasizing sustainable formulations and optimized chemical usage

U.S. Friction Reducers Market Insight

The U.S. friction reducers market captured the largest revenue share of 82% in North America in 2024, propelled by the rapid growth of unconventional oil and gas production. Operators prioritize friction reducers that enhance fluid flow and reduce operational costs in hydraulic fracturing. The rising demand for eco-friendly and cost-effective chemical additives, combined with stringent environmental regulations, drives innovation in friction reducer formulations. In addition, the presence of leading chemical manufacturers and ongoing drilling activities contribute significantly to market expansion.

Europe Friction Reducers Market Insight

The Europe friction reducers market is expected to witness the fastest growth from 2025 to 2032, supported by increasing offshore drilling projects and the shift toward environmentally compliant fracturing fluids. Rising emphasis on reducing chemical waste and improving operational efficiency propels the adoption of friction reducers. The market also benefits from government policies promoting cleaner technologies and the increasing use of bio-based and synthetic friction reducers in conventional and unconventional wells.

U.K. Friction Reducers Market Insight

The U.K. friction reducers market is expected to witness the fastest growth from 2025 to 2032, driven by offshore oil and gas exploration in the North Sea and rising investments in well stimulation techniques. The focus on reducing environmental footprint through optimized chemical additives encourages the use of advanced friction reducers. Regulatory compliance and operational cost management remain key factors influencing market demand in the region.

Germany Friction Reducers Market Insight

The Germany friction reducers market is expected to witness the fastest growth from 2025 to 2032, fuelled by growing investments in upstream oil and gas infrastructure and increasing demand for efficient fracturing fluids. Germany’s strong chemical industry base supports innovation in friction reducer technologies, including biodegradable and environmentally friendly formulations. In addition, rising awareness of ecological impacts and regulatory pressures drive the adoption of safer and high-performance friction reducers.

Asia-Pacific Friction Reducers Market Insight

The Asia-Pacific friction reducers market is expected to witness the fastest growth from 2025 to 2032, led by expanding oil and gas exploration in China, India, and Southeast Asia. Increasing government support for unconventional resource development and rising energy demand boost market growth. The region benefits from growing local manufacturing capabilities and cost-effective chemical solutions, facilitating wider adoption across onshore and offshore drilling operations.

China Friction Reducers Market Insight

The China’s friction reducers market is growing rapidly due to intensified shale gas development and the adoption of advanced hydraulic fracturing technologies. The government’s push for energy security and cleaner extraction methods supports the demand for efficient friction reducers. Moreover, collaborations between international and local chemical manufacturers help improve product quality and availability, driving market expansion.

Japan Friction Reducers Market Insight

The Japan friction reducers market is expected to witness the fastest growth from 2025 to 2032, driven by the country’s emphasis on enhancing oil and gas production efficiency amid limited domestic reserves. Japan’s advanced technological landscape and focus on innovation support the adoption of high-performance friction reducers in well stimulation and hydraulic fracturing operations. In addition, increasing investments in offshore energy projects and strict environmental regulations encourage the use of environmentally friendly friction reducer formulations. The aging energy infrastructure also fuels demand for chemicals that improve operational safety and equipment longevity.

Friction Reducers Market Share

The Friction Reducers industry is primarily led by well-established companies, including:

Latest Developments in Global Friction Reducers Market

In May 2022, Innospec Oilfield Services launched AquaBourne, a new water-based friction reducer designed without oil or surfactants. This formulation uses a water carrier fully compatible with fresh, flowback, or high TDS produced water, resulting in a clear, colorless solution with very low suspended solids. This innovation offers improved environmental compatibility and enhanced performance in hydraulic fracturing operations, supporting cleaner and more efficient extraction processes in the oil and gas market

In June 2021, Kemira completed the installation of advanced production units for emulsion polymers and biobased acrylamide monomers at its Mobile, Alabama manufacturing facility. These emulsion polymers are mainly targeted for water-intensive applications such as friction reducers used in the oil and gas sector. This development strengthens Kemira’s production capacity and supports the supply of high-quality, sustainable chemicals, contributing to the growing demand for efficient and eco-friendly friction reduction solutions

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

Interactive Data Analysis Dashboard

Company Analysis Dashboard for high growth potential opportunities

Research Analyst Access for customization & queries

Competitor Analysis with Interactive dashboard

Latest News, Updates & Trend analysis

Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.

Claudio Rondena

Group Business Development & Strategic Marketing Director, C.O.C Farmaceutici SRL

"This morning we were involved in the first part, the data presentation of MKT analysis, selected abstract from your work. The board team was really impressed and very appreciated, as well."

David Manning - Thermo Fisher Scientific

Director, Global Strategic Accounts,

Dear Ricky, I want to thank you for the excellent market analysis (LIMS INSTALLED BASE DATA) that you and your team delivered, especially end of year on short notice.

Sachin and Shraddha captured the requirements, determined their path forward and executed quickly.

You, Sachin and Shraddha have been a pleasure to work with – very responsive, professional and thorough.

Your work is much appreciated.

Manager - Market Analytics,

Uriah D. Avila - Zeus Polymer Solutions

Thank you for all the assistance and the level of detail in the market report. We are very pleased with the results and the customization. We would like to continue to do business.

Business Development Manager,

(Pharmaceuticals Partner for Nasal Sprays) | Renaissance Lakewood LLC

DBMR was attentive and engaged while discussing the Global Nasal Spray Market. They understood what we were looking for and was able to provide some examples from the report as requested. DBMR Service team has been responsive as needed. Depending on what my colleagues were looking for, I will recommend your services and would be happy to stay connected in case we can utilize your research in the future.

Business Intelligence and Analytics,

Ipsen Biopharm Limited

We are impressed by the CENTRAL PRECOCIOUS PUBERTY (CPP) TREATMENT report - so a BIG thanks to you colleagues.

Competition Analyst,

Basler Web

I just wanted to share a quick note and let you know that you guys did a really good job. I’m glad I decided to work with you. I shall continue being associated with your company as long as we have market intelligence needs.

Marketing Director,

Buhler Group

It was indeed a good experience, would definitely recommend and come back for future prospects.

COO,

A global leader providing Drug Delivery Services

DBMR did an outstanding job on the Global Drug Delivery project, We were extremely impressed by the simple but comprehensive presentation of the study and the quality of work done. This report really helped us to access untapped opportunities across the globe.

Marketing Director,

Philips Healthcare

The study was customized to our targets and needs with well-defined milestones. We were impressed by the in-depth customization and inclusion of not only major but also minor players across the globe. The DBMR Market position grid helped us to analyze the market in different dimension which was very helpful for the team to get into the minute details.

Product manager,

Fujifilms

Thankful to the team for the amazing coordination, and helping me at the last moment with my presentation. It was indeed a comprehensive report that gave us revenue impacting solution enabling us to plan the right move.

Investor relations,

GE Healthcare

Thank you for the report, and addressing our needs in such short time. DBMR has outdone themselves in this project with such short timeframe.

Market Analyst,

Medincell

We found the results of this study compelling and will help our organization validate a market we are considering to enter. Thank you for a job well done.

Andrew - Senior Global Marketing Manager,

Medtronic (US)

I want to thank you for your help with this report – It’s been very helpful in our business planning and it well organized.

Amarildo - Manager, Global Strategic Alignment

MasterCard

We believe the work done by Data Bridge Team for our requirements in the North America Loyalty Management Market was fantastic and would love to continue working with your team moving forward.

Tor Hammer

Green Nexus LLc

Thank you for your quick response to this unfortunate circumstance. Please extend my thanks to your reach team. I will be contacting you in the future with further projects

I acknowledge the difficulty given by the very short warning for this report, and I think that its quality and your delivering time have been very satisfying.

Obviously, as a provider Data Bridge Market Research will be considered as a plus for future needs of Nippon Gases.

Yuki Kopyl (Asian Business Development Department)

UENO FOOD TECHNO INDUSTRY, LTD. (JAPAN)

Xylose report was very useful for our team. Thank you very much & hope to work with you again in the future