Global Flexible Substrates Market

Market Size in USD Billion

USD

3.47 Billion

USD

8.08 Billion

2025

2033

USD

3.47 Billion

USD

8.08 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.47 Billion | |

| USD 8.08 Billion | |

| % | |

|

Flexible Substrates Market Overview

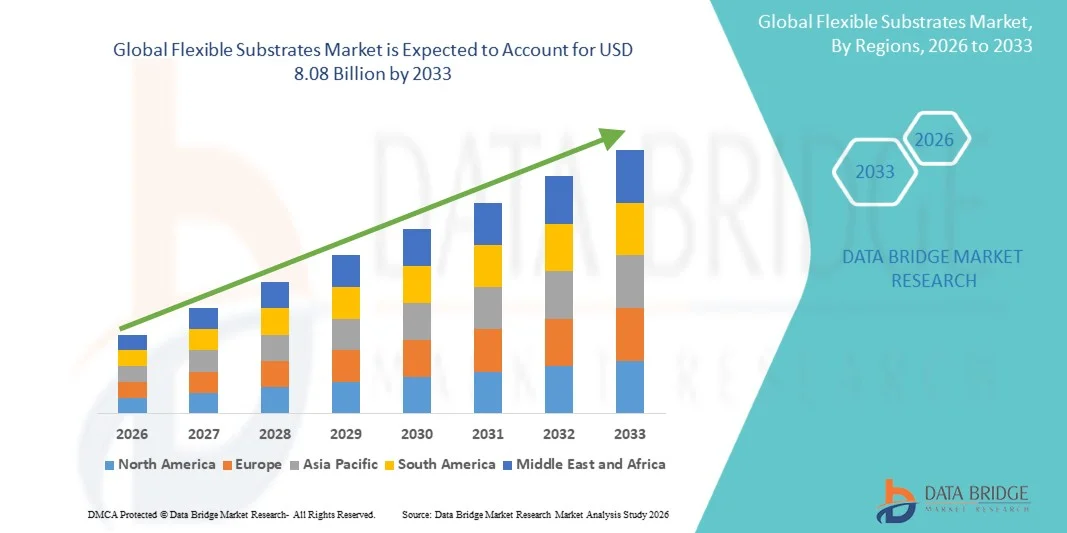

The Flexible Substrates Market was valued at USD 3.47 billion in 2025 and is projected to reach USD 8.08 billion by 2033, growing at a CAGR of 11.15% from 2026 to 2033. The market is experiencing robust and accelerating growth driven by rising global demand for lightweight and bendable electronics, rapid advancements in flexible display technologies including foldable smartphones and rollable screens, and expanding adoption of thin-film photovoltaics in renewable energy applications. The proliferation of wearable devices, Internet of Things (IoT) sensors, and next-generation medical monitoring solutions is further intensifying demand for high-performance flexible substrate materials across diverse end-use industries.

The growing integration of flexible substrates across consumer electronics, healthcare, automotive, and energy sectors is compelling substrate manufacturers to develop advanced polymer films, metal foils, and flexible glass solutions that meet increasingly demanding performance requirements. Innovations in polyimide (PI) and polyethylene naphthalate (PEN) film technologies, combined with the development of ultra-thin bendable glass and high-conductivity metal foils, are enabling new design possibilities across flexible display, flexible PCB, and thin-film solar applications. In addition, growing regulatory emphasis on sustainable and recyclable electronics materials, combined with increasing government investment in flexible electronics research and development programs, is further accelerating the adoption of advanced flexible substrate technologies across global markets.

Key Market Trends & Insights

- North America dominated the Flexible Substrates Market with the largest revenue share of approximately 42.7% in 2025, supported by the rapid growth of consumer electronics, advanced medical device manufacturing, and strong investment in flexible display and printed electronics research. The presence of leading technology companies and a robust ecosystem of substrate material suppliers and flexible electronics manufacturers further consolidates regional leadership.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of approximately 14.5% from 2026 to 2033, supported by expanding consumer electronics manufacturing in China, South Korea, and Japan, rising adoption of flexible OLED displays in smartphone production, government-backed investment in flexible electronics infrastructure, and increasing penetration of thin-film photovoltaic installations across the region.

- The Plastic segment held the largest market revenue share of approximately 63.2% in 2025, driven by the dominant adoption of polyimide (PI), polyethylene terephthalate (PET), and polyethylene naphthalate (PEN) films across flexible display, flexible PCB, and wearable sensor applications. Plastic substrates offer an unmatched combination of flexibility, lightweight performance, cost-effectiveness, and compatibility with high-throughput roll-to-roll manufacturing processes that make them the preferred substrate material across the majority of flexible electronics applications globally.

- The Metal segment accounted for approximately 20.1% of market revenue in 2025, with stainless steel and aluminum foil substrates finding strong adoption in thin-film photovoltaic applications, high-temperature sensor systems, and ruggedized industrial flexible electronics requiring superior thermal conductivity and mechanical barrier performance. The Metal segment is expected to grow at the fastest CAGR of approximately 11.8% from 2026 to 2033, driven by expanding thin-film solar cell manufacturing and growing automotive flexible electronics demand.

- The Flexible segment held the largest market revenue share of approximately 58.4% in 2025, reflecting the core demand for fully bendable and rollable substrate solutions across flexible display, wearable electronics, and flexible sensor applications where unrestricted mechanical deformation is a fundamental product performance requirement.

- The Semi-Flexible segment accounted for approximately 26.8% of market revenue in 2025, driven by applications in automotive electronics, industrial sensors, and medical monitoring devices where controlled partial flexibility and enhanced mechanical durability under repeated moderate bending cycles are required. The Semi-Flexible segment is projected to register a CAGR of approximately 12.3% from 2026 to 2033.

- The Displays segment held the largest market revenue share of approximately 46.2% in 2025, driven by the massive and growing demand for flexible OLED display substrates in foldable smartphones, flexible smartwatch displays, rollable television panels, and curved automotive infotainment systems. The continued expansion of flexible display production capacity by Samsung Display, LG Display, BOE Technology, and their peers is sustaining dominant demand from this application segment globally.

- The Printed Circuit Boards (PCBs) segment accounted for approximately 22.6% of application revenue in 2025, driven by widespread adoption of flexible PCBs in consumer electronics miniaturization, wearable devices, medical instruments, and aerospace electronics where flexible circuit routing provides critical space-saving and weight reduction advantages versus rigid PCB alternatives. The PCBs segment is projected to grow at a CAGR of approximately 12.6% from 2026 to 2033.

Market Size & Forecast

- Global Market Value (2025): USD 3.47 Billion

- Expected Market Value (2033): USD 8.08 Billion

- Forecast CAGR (2026–2033): 11.15%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Flexible Substrates Market Segmentation

|

Attributes |

Flexible Substrates Key Market Insights |

|

Segments Covered |

· By Substrate Type: Plastic, Metal, and Glass · By Type: Flexible, Semi-Flexible, and Rigid · By Application: Displays, Printed Circuit Boards (PCBs), Thin-film Photovoltaics (Solar Cells), Medical and Healthcare Devices, Sensors, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Corning Incorporated (U.S.) |

|

Market Opportunities |

• Expanding Adoption of Flexible OLED Displays in Foldable Smartphones and Next-Generation Consumer Electronics • Growing Integration of Flexible Substrates in Medical Wearables and Implantable Healthcare Device Applications |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Flexible Substrates Market Trends

Trend: Rapid Proliferation of Foldable and Flexible Display Technologies Driving Substrate Demand

The Flexible Substrates Market is being significantly reshaped by the accelerating commercial adoption of foldable smartphones, rollable display panels, and curved automotive infotainment systems, all of which depend on high-performance flexible substrate materials capable of withstanding repeated bending cycles without degradation. The widespread commercialization of flexible OLED display technologies by leading manufacturers including Samsung Display, LG Display, and BOE Technology Group is generating sustained high-volume demand for polyimide (PI) and ultra-thin flexible glass substrates with exceptional optical clarity, barrier properties, and mechanical resilience.

Industry data from 2024 indicates that global shipments of flexible OLED display panels exceeded 850 million units, predominantly driven by premium smartphone applications, with foldable device adoption growing rapidly across major consumer electronics markets in Asia-Pacific, North America, and Europe. Substrate manufacturers are responding to the display industry’s performance requirements by developing next-generation ultra-thin polyimide films with improved thermal stability above 400°C, enhanced barrier coatings reducing water vapor transmission rates to below 10⁻⁶ g/m²/day, and thinner glass substrates approaching 30 microns that can achieve bending radii of 5 millimeters without fracture. These material advances are enabling display panel manufacturers to achieve thinner, lighter, and more durable flexible displays that support more compelling foldable and rollable consumer device designs.

The automotive display segment is emerging as a significant secondary driver of flexible substrate demand, as vehicle manufacturers increasingly adopt curved and flexible display panels for dashboard instrumentation, center console touchscreens, and rear seat entertainment systems. The integration of flexible substrate technology into automotive-grade display applications requires substrate materials meeting stringent automotive reliability standards including extended temperature cycling, vibration resistance, and UV stability, driving premium substrate development and qualification programs across leading substrate manufacturers worldwide.

Flexible Substrates Market Dynamics

Key Market Driver: Accelerating Demand for Wearable Electronics and IoT Applications

The rapid global proliferation of wearable electronic devices including smartwatches, fitness trackers, hearables, smart glasses, and medical biosensors is creating unprecedented demand for flexible substrate materials that enable lightweight, body-conforming electronic form factors incompatible with conventional rigid printed circuit board technology. Flexible substrates serve as the foundational enabling material for wearable electronics, providing the mechanical bendability, biocompatibility, and electrical performance necessary for devices that must maintain functionality through continuous mechanical deformation during everyday physical activities.

The global wearable device market reached an estimated 600-million-unit shipment volume in 2024, with strong growth projected through the forecast period as healthcare monitoring applications, fitness and wellness tracking, and connected smart textile applications expand. Each wearable device incorporates multiple flexible substrate components including flexible PCBs for circuit routing, flexible display panels for user interfaces, and flexible sensor arrays for biometric monitoring, creating compound demand multiplication across the flexible substrates value chain. Substrate suppliers are investing heavily in developing thinner, lighter, and more conformable materials with improved wash and sweat resistance for textile-integrated wearable applications.

Industry analysis of leading wearable device manufacturers indicates that flexible substrate material costs represent 12–18% of total device bill of materials, creating strong commercial incentive for substrate suppliers to develop cost-optimized materials through roll-to-roll manufacturing process innovations. Advances in roll-to-roll coating, printing, and lamination technologies are enabling continuous high-throughput flexible substrate production at significantly lower per-unit costs compared to batch sheet processing, supporting broader market adoption across volume-sensitive consumer wearable applications.

Key Restraint/Challenge: High Manufacturing Costs and Performance Reliability Limitations

The Flexible Substrates Market faces significant constraints related to the elevated manufacturing cost of high-performance flexible substrate materials compared to conventional rigid alternatives, combined with ongoing technical challenges in achieving the long-term reliability and durability required for demanding industrial, automotive, and medical applications. Advanced polyimide films and ultra-thin flexible glass substrates involve complex and capital-intensive manufacturing processes including precision casting, multi-layer barrier coating deposition, and stringent quality control protocols that contribute to substantially higher per-unit costs compared to conventional FR4 rigid PCB substrates or standard soda-lime glass.

Reliability concerns related to substrate delamination, fatigue crack propagation in flexible metal foil interconnects, and permeation barrier degradation in moisture-sensitive OLED applications represent significant technical barriers that constrain adoption in reliability-critical applications including implantable medical devices, aerospace electronics, and long-lifetime industrial sensor systems. Industry qualification data indicates that flexible electronic assemblies on polymer substrates can experience a two to five times higher field failure rate compared to equivalent rigid electronics in harsh environment applications, reflecting the additional mechanical and environmental stress imposed by flexible form factors that accelerates material fatigue and degradation mechanisms.

Key Market Opportunity: Expansion of Thin-Film Photovoltaics and Building-Integrated Solar Applications

The accelerating global transition toward renewable energy generation is creating substantial growth opportunities for flexible substrate manufacturers serving the thin-film photovoltaic market, particularly as building-integrated photovoltaic (BIPV) applications, portable solar charging products, and flexible solar roofing solutions gain significant commercial momentum. Flexible photovoltaic modules based on CIGS, cadmium telluride, and organic photovoltaic technologies deposited on plastic film and metal foil substrates offer compelling advantages over conventional glass-based rigid solar panels including dramatically lower installation weight, improved aesthetic integration into building surfaces, and compatibility with curved and irregular mounting geometries.

Government renewable energy incentive programs across Europe, North America, and Asia-Pacific are significantly expanding the addressable market for flexible photovoltaic installations in commercial and residential building applications. Pilot installations of flexible BIPV systems in commercial office buildings and residential housing developments across Germany, Japan, and South Korea in 2024–2025 demonstrated energy generation performance within 15% of equivalent rigid crystalline silicon panel installations, while providing substantially improved architectural flexibility and installation cost savings. Market projections indicate that flexible thin-film photovoltaic substrate demand could represent a USD 900 million to 1.2 billion opportunity by 2033, driven by continued cost reduction in flexible PV manufacturing and expanding global net-zero building energy performance regulations.

Flexible Substrates Market Scope

The Flexible Substrates Market is segmented on the basis of substrate type, type, and application.

- By Substrate Type

On the basis of substrate type, the flexible substrates market is segmented into Plastic, Metal, and Glass. The Plastic segment held the largest market revenue share of approximately 63.2% in 2025, driven by the dominant adoption of polyimide (PI), polyethylene terephthalate (PET), and polyethylene naphthalate (PEN) films across flexible display, flexible PCB, and wearable sensor applications. Plastic substrates offer an unmatched combination of flexibility, lightweight performance, cost-effectiveness, and compatibility with high-throughput roll-to-roll manufacturing processes that make them the preferred substrate material across the majority of flexible electronics applications globally.

The Metal segment accounted for approximately 20.1% of market revenue in 2025, with stainless steel and aluminum foil substrates finding strong adoption in thin-film photovoltaic applications, high-temperature sensor systems, and ruggedized industrial flexible electronics requiring superior thermal conductivity and mechanical barrier performance. The Metal segment is expected to grow at the fastest CAGR of approximately 11.8% from 2026 to 2033, driven by expanding thin-film solar cell manufacturing and growing automotive flexible electronics demand.

- By Type

On the basis of type, the flexible substrates market is segmented into Flexible, Semi-Flexible, and Rigid. The Flexible segment held the largest market revenue share of approximately 58.4% in 2025, reflecting the core demand for fully bendable and rollable substrate solutions across flexible display, wearable electronics, and flexible sensor applications where unrestricted mechanical deformation is a fundamental product performance requirement.

The Semi-Flexible segment accounted for approximately 26.8% of market revenue in 2025, driven by applications in automotive electronics, industrial sensors, and medical monitoring devices where controlled partial flexibility and enhanced mechanical durability under repeated moderate bending cycles are required. The Semi-Flexible segment is projected to register a CAGR of approximately 12.3% from 2026 to 2033.

- By Application

On the basis of application, the market is segmented into Displays, Printed Circuit Boards (PCBs), Thin-film Photovoltaics (Solar Cells), Medical and Healthcare Devices, Sensors, and Others. The Displays segment held the largest market revenue share of approximately 46.2% in 2025, driven by the massive and growing demand for flexible OLED display substrates in foldable smartphones, flexible smartwatch displays, rollable television panels, and curved automotive infotainment systems. The continued expansion of flexible display production capacity by Samsung Display, LG Display, BOE Technology, and their peers is sustaining dominant demand from this application segment globally.

The Printed Circuit Boards (PCBs) segment accounted for approximately 22.6% of application revenue in 2025, driven by widespread adoption of flexible PCBs in consumer electronics miniaturization, wearable devices, medical instruments, and aerospace electronics where flexible circuit routing provides critical space-saving and weight reduction advantages versus rigid PCB alternatives. The PCBs segment is projected to grow at a CAGR of approximately 12.6% from 2026 to 2033.

Flexible Substrates Market Regional Analysis

North America Flexible Substrates Market Insight

North America dominated the Flexible Substrates Market with the largest revenue share of 42.7% in 2025, supported by the presence of major technology companies, world-class flexible electronics research institutions, and a strong ecosystem of flexible substrate material manufacturers and flexible electronics solution providers. The region benefits from high consumer adoption rates of premium flexible OLED smartphones and wearables, significant government investment in advanced electronics manufacturing including flexible electronics programs under the U.S. CHIPS and Science Act, and robust demand from the medical device and aerospace industries for high-reliability flexible substrate solutions. Continued strength in the North American renewable energy market is further supporting flexible photovoltaic substrate demand across the region.

U.S. Flexible Substrates Market Insight

The U.S. flexible substrates market captured the largest revenue share in North America in 2025, driven by the country’s leading position in flexible electronics innovation, strong consumer electronics demand including high adoption of foldable smartphones and smartwatches, and significant procurement of flexible substrate solutions across defense, aerospace, and medical device applications. The presence of key flexible substrate manufacturers including Corning, Rogers Corporation, DuPont, and 3M, combined with strong university-industry collaboration programs in flexible electronics materials research, maintains the U.S. as the global center of flexible substrate technology development. Federal investment in domestic semiconductor and advanced packaging manufacturing is also expanding U.S. glass substrate production capacity for next-generation AI chip packaging applications.

Europe Flexible Substrates Market Insight

The Europe flexible substrates market is expected to witness steady growth from 2026 to 2033, driven by strong demand from the region’s automotive electronics industry, expanding adoption of flexible solar modules in BIPV applications supported by the European Green Deal, and increasing investment in flexible medical device manufacturing across Germany, the U.K., and the Netherlands. European automotive manufacturers are increasingly integrating flexible display panels and curved sensor systems into premium vehicle interiors, creating sustained demand for automotive-grade flexible substrate materials meeting stringent AEC-Q200 qualification standards. The presence of Heraeus Materials Technology and SCHOTT AG further strengthens the European flexible substrates supply chain.

U.K. Flexible Substrates Market Insight

The U.K. flexible substrates market is expected to witness steady growth from 2026 to 2033, driven by strong investment in flexible electronics research through the Henry Royce Institute and the National Physical Laboratory, growing adoption of flexible medical devices in NHS digital health transformation programs, and increasing deployment of flexible photovoltaic solutions in commercial building renewable energy systems. The U.K.’s strengths in printed electronics and organic photovoltaics research are creating technology commercialization opportunities in flexible substrate applications aligned with the country’s net-zero energy transition objectives.

Germany Flexible Substrates Market Insight

The Germany flexible substrates market is expected to witness strong growth from 2026 to 2033, primarily driven by the country’s world-leading automotive electronics industry adopting flexible displays and advanced flexible sensor systems at scale, combined with Germany’s strong industrial electronics manufacturing base creating demand for high-reliability flexible PCB substrates. Germany’s aggressive solar energy expansion program under the Erneuerbare-Energien-Gesetz (EEG) renewable energy law is supporting growing flexible thin-film photovoltaic installation volumes, creating incremental flexible substrate demand. SCHOTT AG’s continued expansion of ultra-thin glass production for flexible display and semiconductor packaging applications further reinforces Germany’s position in the European flexible substrates market.

Asia-Pacific Flexible Substrates Market Insight

The Asia-Pacific flexible substrates market is expected to witness the fastest growth rate from 2026 to 2033, recording a CAGR of approximately 14.5%, supported by the region’s dominant position in global consumer electronics manufacturing, particularly flexible OLED smartphone and wearable device production in South Korea, China, Japan, and Taiwan. South Korea’s Samsung Display and LG Display collectively account for a dominant share of global flexible OLED panel production capacity, generating massive substrate demand. China’s rapidly expanding BOE Technology Group and its growing ecosystem of domestic flexible electronics manufacturers represent a significant and fast-growing demand center. Strong government support for domestic flexible electronics production capability across China, South Korea, and Japan is driving substantial new capacity investment and substrate demand growth across the region.

Japan Flexible Substrates Market Insight

The Japan flexible substrates market is expected to witness steady growth from 2026 to 2033, driven by the country’s strong position in advanced substrate material innovation, including Toray Industries’ polyimide film leadership, AGC Inc.’s ultra-thin glass development, and Taiyo Holdings’ photosensitive flexible material solutions. Japan’s advanced consumer electronics industry, innovative automotive electronics ecosystem, and significant investment in flexible medical device development collectively sustain strong domestic flexible substrate demand. The Japan Ministry of Economy, Trade and Industry’s investment in next-generation flexible electronics manufacturing process innovation is further supporting technology leadership and export competitiveness across Japanese substrate material suppliers.

China Flexible Substrates Market Insight

The China flexible substrates market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s position as the world’s largest consumer electronics manufacturing hub, massive and rapidly growing flexible OLED panel production capacity at BOE Technology Group, Tianma Microelectronics, and EverDisplay Optronics, and significant government investment in domestic flexible substrate material supply chain development. China’s 14th Five-Year Plan includes targeted support for flexible electronics manufacturing infrastructure and domestic substrate material capability development, reducing reliance on imported polyimide films and ultra-thin glass from Japanese and Korean suppliers. Growing deployment of flexible solar panels in China’s expanding renewable energy installations is creating additional incremental demand for flexible photovoltaic substrate materials through the forecast period.

Flexible Substrates Market Share

The Flexible Substrates industry is primarily led by well-established companies, including:

- Corning Incorporated (U.S.)

- DuPont de Nemours, Inc. (U.S.)

- 3M Company (U.S.)

- Samsung Display Co., Ltd. (South Korea)

- LG Display Co., Ltd. (South Korea)

- BOE Technology Group Co., Ltd. (China)

- Heraeus Materials Technology GmbH & Co. KG (Germany)

- Rogers Corporation (U.S.)

- Polyonics, Inc. (U.S.)

- BenQ Materials Corporation (Taiwan)

- American Semiconductor, Inc. (U.S.)

- SCHOTT AG (Germany)

- AGC Inc. (Japan)

- Toray Industries, Inc. (Japan)

- Taiyo Holdings Co., Ltd. (Japan)

Latest Developments in Flexible Substrates Market

- In May 2025, Samsung Display (South Korea) commenced production at a new USD 3.1 billion flexible OLED manufacturing line dedicated to ultra-thin panel production for next-generation foldable smartphones and tablet devices, significantly expanding global flexible display substrate consumption. The new production line utilizes advanced polyimide substrate films with enhanced thermal resistance and improved optical clarity specifications that set new performance benchmarks for the flexible display substrate supply chain globally.

- In March 2025, Merck Group (Germany) announced the acquisition of Nissan Chemical Corporation’s electronics materials division, significantly expanding its portfolio of advanced semiconductor and display substrate materials including polyimide precursor resins, photosensitive coatings, and functional interlayer materials for flexible display and flexible electronics manufacturing applications. The acquisition strengthens Merck’s position as an integrated materials supplier across the global flexible substrate value chain.

- In January 2025, TE Connectivity (Switzerland) announced a major contract to supply flexible interconnect solutions for Samsung Electronics’ foldable device lineup, encompassing advanced flexible PCB substrates and flexible flat cable assemblies engineered to survive 200,000-fold cycles without electrical performance degradation, demonstrating the advancing reliability and commercial maturity of flexible substrate technology in premium consumer electronics applications.

- In April 2025, LG Innotek (South Korea) disclosed plans to begin sampling glass substrates for semiconductor packaging applications by the end of 2025, marking a strategic diversification of the company’s substrate portfolio beyond camera module components into the rapidly growing advanced packaging market. Glass substrate technology offers up to 40% speed improvement and 50% power consumption reduction compared to conventional organic substrates for AI accelerator chip applications.

- In June 2024, LG Display (South Korea) announced a strategic partnership with Dow (U.S.) to jointly develop next-generation high-performance polymer substrates for flexible OLED display panels, targeting improved encapsulation performance, enhanced mechanical fatigue resistance, and reduced substrate-related display defect rates to support the demanding quality requirements of premium foldable smartphone display production.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Flexible Substrates Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Flexible Substrates Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Flexible Substrates Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.