Global Electrostatic Precipitator Market

Market Size in USD Billion

USD

7.65 Billion

USD

12.40 Billion

2024

2032

USD

7.65 Billion

USD

12.40 Billion

2024

2032

| 2025 - 2032 | |

| USD 7.65 Billion | |

| USD 12.40 Billion | |

| % | |

|

Electrostatic Precipitator Market Size

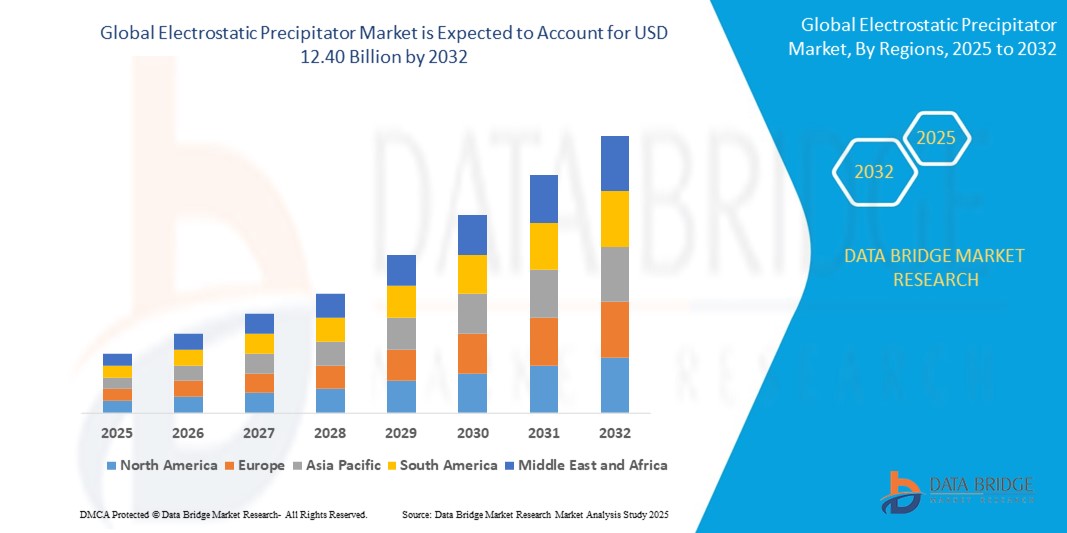

- The global electrostatic precipitator market size was valued at USD 7.65 billion in 2024 and is expected to reach USD 12.40 billion by 2032, at a CAGR of 6.22% during the forecast period

- The market growth is largely fueled by the increasing stringency of air pollution control regulations worldwide and the growing industrialization in emerging economies, leading to a higher demand for efficient particulate matter emission reduction solutions

- Furthermore, rising awareness about environmental protection and the need for sustainable industrial operations are establishing electrostatic precipitators as a preferred technology for air quality management

Electrostatic Precipitator Market Analysis

- Electrostatic precipitators (ESPs), offering highly efficient removal of particulate matter from industrial gas streams, are increasingly vital components of modern air pollution control systems across various industries due to their ability to handle large gas volumes, high temperatures, and diverse particulate characteristics

- The escalating demand for ESPs is primarily fueled by the global push for cleaner air, increasing industrial emissions, and a rising preference for cost-effective and reliable long-term particulate control technologies

- Asia-Pacific dominates the electrostatic precipitator market with the largest revenue share of 45.60% in 2025, driven by rapid industrialization, especially in emerging economies such as China and India, and a growing demand for energy coupled with increasing governmental focus on mitigating industrial air pollution

- Europe is expected to be the fastest-growing region in the electrostatic precipitator market during the forecast period, due to stringent emission standards and a strong emphasis on upgrading existing industrial facilities with advanced pollution control technologies

- The dry ESP segment is expected to dominate the electrostatic precipitator market with a market share of 61% in 2025, driven by its widespread application in power generation and cement industries, its effectiveness in capturing dry particulate matter, and lower operational complexities compared to wet ESPs

Report Scope and Electrostatic Precipitator Market Segmentation

|

Attributes |

Electrostatic Precipitator Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Electrostatic Precipitator Market Trends

“Advancements through IoT, AI, and Predictive Maintenance”

- A significant and accelerating trend in the global electrostatic precipitator (ESP) market is the deepening integration with Internet of Things (IoT) technologies, artificial intelligence (AI), and advanced analytics for predictive maintenance

- For instance, companies are increasingly offering ESPs with integrated sensors and data analytics platforms, allowing operators to monitor key parameters in real-time, such as particulate concentration, temperature, and electrical performance. This enables proactive adjustments and optimization of the ESP's collection efficiency

- AI integration in ESPs enables features such as learning flue gas characteristics to potentially suggest operational optimizations and providing more intelligent alerts based on performance deviations

- The seamless integration of ESPs with broader industrial automation systems and digital twins facilitates centralized control over various aspects of plant operations

- This trend towards more intelligent, intuitive, and interconnected air pollution control systems is fundamentally reshaping industry expectations for environmental compliance and operational efficiency

- The demand for ESPs that offer seamless IoT, AI, and predictive maintenance integration is growing rapidly across various industrial sectors, as companies increasingly prioritize operational efficiency, reduced downtime, and robust compliance with ever-stricter environmental regulations

Electrostatic Precipitator Market Dynamics

Driver

“Growing Need Due to Increasing Stringency of Air Pollution Control Regulations”

- The increasing stringency of air pollution control regulations globally, coupled with the accelerating pace of industrialization, particularly in emerging economies, is a significant driver for the heightened demand for electrostatic precipitators

- As governments worldwide impose stricter limits on particulate matter emissions from industrial sources, companies are compelled to invest in highly efficient pollution control technologies such as ESPs to ensure compliance

- For instance, regulatory bodies in various regions, such as the EPA in the U.S., the European Union and national environmental agencies in China and India, are enforcing stricter emission standards for industries such as power generation, cement, and metal processing. This pushes industries to adopt or upgrade ESP systems to achieve required emission levels

- Furthermore, the continuous growth in industrial output across sectors such as chemicals, manufacturing, and waste incineration leads to higher volumes of exhaust gases requiring effective particulate removal

- The need for long-term, reliable, and high-capacity solutions to manage these emissions makes ESPs an indispensable choice. The increasing focus on sustainable industrial practices and corporate social responsibility also encourages companies to adopt advanced pollution control systems

Restraint/Challenge

“High Initial Capital Investment and Operational Complexity”

- Concerns surrounding the high initial capital investment required for the installation of electrostatic precipitators, along with their inherent operational complexity and specific maintenance requirements, pose significant challenges to broader market penetration

- For instance, installing an ESP often involves significant engineering, specialized equipment, and integration into existing plant infrastructure, leading to a considerable capital expenditure. This can be a barrier for small and medium-sized enterprises (SMEs) or industries with limited capital budgets

- Addressing these cost concerns through modular designs, financing options, and demonstrating long-term ROI is crucial for wider adoption. In addition, ESP systems require specialized skills and knowledge for optimal operation and maintenance

- Factors such as dust resistivity fluctuations, temperature variations, and the presence of sticky or corrosive particulate matter can impact ESP performance and necessitate careful monitoring and adjustment

- Overcoming these challenges through technological advancements that reduce installation complexity, enhance automation, offer predictive maintenance solutions, and provide comprehensive training programs will be vital for sustained market growth

Electrostatic Precipitator Market Scope

The market is segmented on the basis of design, type, offering, and end user.

- By Design

On the basis of design, the electrostatic precipitator market is segmented into plate and tubular. The plate segment dominates the largest market revenue share in 2025, driven by its widespread use in large-scale industrial applications, superior collection efficiency for a broad range of particulate sizes, and adaptability to various industrial processes. Plate designs are favored for their robustness and ability to handle high gas volumes.

The tubular segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by increasing adoption in specialized applications involving wet collection, fine particulate removal, and hazardous waste incineration. Tubular ESPs offer advantages in specific gas conditions and often provide more compact designs for certain industrial setups.

- By Type

On the basis of type, the electrostatic precipitator market is segmented into dry ESP, wet ESP, plate wire, flat plate, tubular, and two-stage. The dry ESP segment held the largest market revenue share in 2025, driven by its extensive application in key industries such as power generation and cement manufacturing, its effectiveness in capturing dry particulate matter, and relatively lower operational complexities in dry dust handling.

The wet ESP segment is expected to witness the fastest CAGR from 2025 to 2032, driven by its superior ability to handle sticky, corrosive, or sub-micron particulate matter, and its effectiveness in simultaneously removing acid gases and heavy metals, making it ideal for industries with complex emission challenges.

- By Offering

On the basis of offering, the electrostatic precipitator market is segmented into hardware and software, and services. The hardware and software segment held the largest market revenue share in 2025, driven by the high capital expenditure associated with purchasing and installing ESP units, which include the precipitator structure, power supply, control systems, and associated software for monitoring and operation.

The services segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the increasing need for maintenance, retrofitting, upgrades, and operational support to ensure optimal performance, extend the lifespan, and meet evolving emission standards for existing ESP installations.

- By End User

On the basis of end user, the electrostatic precipitator market is segmented into power generation, chemicals and petrochemicals, cement, metal processing and mining, manufacturing, marine, and others. The power generation segment accounted for the largest market revenue share in 2024, driven by stringent emission regulations on thermal power plants (coal and biomass) globally, and the large volume of flue gases requiring particulate control in this industry.

The marine segment is expected to witness the fastest CAGR from 2025 to 2032, driven by new regulations on exhaust gas cleaning systems from the International Maritime Organization (IMO) and increasing demand for cleaner emissions from ships to comply with sulfur and particulate matter limits in emission control areas.

Electrostatic Precipitator Market Regional Analysis

- Asia-Pacific dominates the electrostatic precipitator market with the largest revenue share of 45.60% in 2025, driven by rapid industrialization, especially in emerging economies such as China and India, and a growing demand for energy coupled with increasing governmental focus on mitigating industrial air pollution

- The region's substantial industrial base, combined with the implementation of stricter environmental policies and investment in new power plants and manufacturing facilities, significantly contributes to the high adoption of electrostatic precipitators

- This widespread use is further supported by local manufacturing capabilities and the drive for sustainable development

U.S. Electrostatic Precipitator Market Insight

The U.S. electrostatic precipitator market is projected to expand at a significant CAGR, driven by stringent environmental regulations, particularly the Clean Air Act, and the ongoing modernization of industrial infrastructure. Industries are increasingly investing in advanced emission control technologies to comply with federal and state mandates for particulate matter reduction. The focus on upgrading aging power plants and the expansion of manufacturing sectors are fueling the demand for highly efficient and reliable ESP systems. Furthermore, technological advancements in ESP designs that offer improved performance and energy efficiency are contributing to market growth in the U.S.

Europe Electrostatic Precipitator Market Insight

The European electrostatic precipitator market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the European Union's stringent Industrial Emissions Directive (IED) and the escalating need for enhanced air quality in industrial and urban areas. The increasing focus on decarbonization and circular economy principles is fostering the adoption of advanced ESPs in sectors such as power generation, waste-to-energy, and metallurgy. European industries are also drawn to the long-term operational efficiency and low maintenance of these devices. The region is experiencing significant growth across various industrial applications, with ESPs being incorporated into both new constructions and retrofitting projects to meet ambitious emission reduction targets.

U.K. Electrostatic Precipitator Market Insight

The U.K. electrostatic precipitator market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating trend of industrial modernization and a desire for heightened environmental compliance. In addition, concerns regarding air quality and public health are encouraging both industries and power generators to choose advanced particulate control solutions. The UK’s embrace of sustainable industrial practices, alongside its robust manufacturing and energy infrastructure, is expected to continue to stimulate market growth, with a particular focus on upgrading existing facilities to meet post-Brexit environmental standards.

Germany Electrostatic Precipitator Market Insight

The German electrostatic precipitator market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of industrial air quality and the demand for technologically advanced, energy-efficient, and sustainable solutions. Germany’s well-developed industrial infrastructure, combined with its emphasis on innovation and green technologies, promotes the adoption of ESPs, particularly in power generation, chemical, and cement sectors. The integration of ESPs with smart monitoring and control systems is also becoming increasingly prevalent, with a strong preference for high-performance, long-lasting solutions aligning with local industry expectations and stringent environmental regulations.

Asia-Pacific Electrostatic Precipitator Market Insight

The Asia-Pacific electrostatic precipitator market is poised to grow at the fastest CAGR, driven by increasing industrialization, rising energy demand, and rapid urbanization in countries such as China, Japan, and India. The region's growing inclination towards stricter environmental regulations, supported by government initiatives promoting cleaner production, is driving the adoption of ESPs across diverse industries. Furthermore, as APAC emerges as a manufacturing hub for industrial equipment and environmental technologies, the affordability and accessibility of ESP solutions are expanding to a wider industrial base, leading to significant market expansion.

Japan Electrostatic Precipitator Market Insight

The Japan electrostatic precipitator market is gaining momentum due to the country’s high-tech manufacturing sector, strong environmental consciousness, and demand for highly efficient and compact air pollution control solutions. The Japanese market places a significant emphasis on technological precision and reliability, and the adoption of ESPs is driven by the increasing need for advanced emission control in power plants, steel mills, and various industrial facilities. The integration of ESPs with smart monitoring, predictive maintenance, and energy-efficient designs is fueling growth. Moreover, Japan's focus on sustainable development and circular economy models is likely to spur demand for cutting-edge ESP technologies in both new projects and existing infrastructure upgrades.

China Electrostatic Precipitator Market Insight

The China electrostatic precipitator market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country's rapid industrial growth, massive energy consumption, and the government's aggressive push for environmental protection. China stands as one of the largest industrial nations, and ESPs are becoming increasingly vital in sectors such as coal-fired power generation, cement, and metallurgy to combat severe air pollution. The "Blue Sky" initiatives and ultra-low emission policies, coupled with the availability of robust domestic manufacturers and continuous technological upgrades, are key factors propelling the market in Chin.

Electrostatic Precipitator Market Share

The electrostatic precipitators industry is primarily led by well-established companies, including:

- FLSmidth Cement A/S (U.S.)

- Siemens (U.S.)

- Babcock & Wilcox Enterprises, Inc. (U.S.)

- John Wood Group PLC (U.K.)

- SEI (U.S.)

- KC Cottrell (India)

- Balcke-Dürr GmbH (Germany)

- ELEX AG (Switzerland)

- Beltran Technologies, Inc. (U.S.)

- Mitsubishi Hitachi Power, Ltd. (Japan)

- Fujian Longking Co., Ltd. (China)

- GEA Group Aktiengesellschaft (Germany)

- Thermax Limited (India)

- Sumitomo Heavy Industries, Ltd. (Japan)

- Bharat Heavy Electricals Limited (India)

Latest Developments in Global Electrostatic Precipitator Market

-

In May 2024, Ardagh Glass Packaging-Africa installed an electrostatic precipitator (ESP) at its Wadeville facility to minimize dust and smoke emissions, ensuring compliance with strict environmental regulations. This investment underscores the company’s commitment to industrial sustainability and air quality improvement. The ESP technology enhances filtration efficiency, supporting cleaner production processes while aligning with global emission standards. Ardagh continues to integrate advanced environmental solutions across its operations

- In January 2024, Babcock & Wilcox (B&W) acquired Hamon Research-Cottrell’s emissions control technologies, enhancing its portfolio of advanced air quality control systems. This strategic acquisition expands B&W’s capabilities in emissions reduction, offering customers improved solutions for cleaner energy production. By integrating Hamon Research-Cottrell’s expertise, B&W strengthens its commitment to environmental sustainability and regulatory compliance. The move reinforces B&W’s leadership in air quality control innovations

- In March 2023, GEA Group AG formed a strategic partnership with environmental engineering firms in India and Southeast Asia to expand its regional presence and deliver next-generation electrostatic precipitator (ESP) solutions. This collaboration addresses the increasing demand for air pollution control in rapidly industrializing regions, reinforcing GEA’s commitment to sustainability and advanced emissions reduction technologies. By leveraging innovative ESP systems, the partnership aims to enhance air quality and regulatory compliance across diverse industries

- In December 2022, General Electric Company introduced a technical solution aimed at reducing carbon emissions through engineering studies integrating Selective Catalytic Reduction (SCR) technology. This innovation effectively curbs nitrogen oxide (NOx) and carbon monoxide (CO) emissions by over 90%, surpassing World Bank Emissions Standards. By leveraging advanced emission control systems, GE reinforces its commitment to sustainability and cleaner energy solutions. The initiative aligns with global efforts to mitigate environmental impact and enhance air quality.

- In December 2022, ProcessBarron, a U.S.-based manufacturer specializing in air and gas handling products, established a wholly-owned subsidiary in Toronto, Canada. This expansion strengthens its presence in North America, enabling the company to provide electrostatic precipitator and air pollution control services through its Southern Field-Environmental Elements division. The subsidiary aims to enhance service offerings and operational reach, supporting industries with advanced air quality solutions. By investing in regional growth, ProcessBarron reinforces its commitment to environmental sustainability and industrial efficiency

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Electrostatic Precipitator Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Electrostatic Precipitator Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Electrostatic Precipitator Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.