Global District Heating Market

Market Size in USD Billion

USD

209.34 Billion

USD

279.96 Billion

2024

2032

USD

209.34 Billion

USD

279.96 Billion

2024

2032

| 2025 - 2032 | |

| USD 209.34 Billion | |

| USD 279.96 Billion | |

| % | |

|

District Heating Market Size

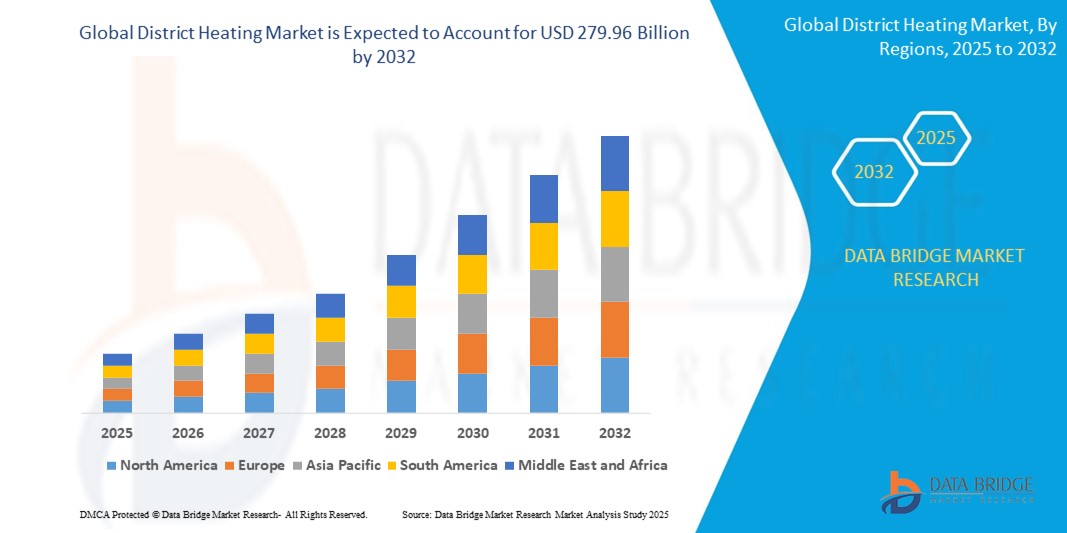

- The global district heating market size was valued at USD 209.35 billion in 2024 and is expected to reach USD 279.96 billion by 2032, at a CAGR of 3.70% during the forecast period

- The market growth is primarily driven by increasing urbanization and industrialization, leading to a higher demand for energy-efficient and cost-effective heating solutions

- Furthermore, rising global energy demand, stringent environmental regulations aimed at reducing carbon emissions, and growing government support for eco-friendly heating systems are significantly accelerating the adoption of district heating solutions

District Heating Market Analysis

- District heating, also known as heat networks or tele-heating, is a system that distributes heat generated from a centralized location to multiple buildings via a network of insulated pipes. It is a crucial component of modern urban heating systems, offering enhanced energy efficiency and environmental testing benefits compared to individual heating solutions

- The escalating demand for district heating is largely fueled by the global emphasis on energy efficiency and sustainability, the need for centralized and efficient heating in densely populated urban areas, and the increasing integration of renewable energy sources and waste heat recovery

- Europe dominates the district heating market with the largest revenue share of 70.5% in 2024, characterized by well-established district heating networks, strong government initiatives, and a high focus on sustainable energy solutions

- Asia-Pacific is expected to be the fastest-growing region in the district heating market during the forecast period. This growth is attributed to rapid urbanization, increasing industrialization, rising disposable incomes, and growing investments in energy-efficient and sustainable heating solutions in countries such as China and South Korea

- The combined heat and power segment holds the largest market share of 69.4% in 2024 by plant type, driven by its exceptional energy efficiency in simultaneously generating both heat and electricity from a single energy source. CHP systems maximize energy utilization and reduce greenhouse gas emissions

Report Scope and District Heating Market Segmentation

|

Attributes |

District Heating Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

District Heating Market Trends

“Digitalization and AI-Driven Optimization for Enhanced Efficiency”

- A significant and accelerating trend in the global district heating market is the increasing adoption of digitalization and artificial intelligence (AI) for optimizing network performance, enhancing energy efficiency, and reducing operational costs

- For instance, companies are implementing smart meters, sensors, and real-time monitoring systems that collect vast amounts of data on heat consumption, weather conditions, and system performance. AI algorithms then analyze this data to predict heating demand, optimize the dispatch of heat sources, and adjust distribution parameters in real-time

- AI plays a crucial role in load forecasting, enabling operators to anticipate demand fluctuations and optimize the operation of heating plants. It also assists in optimizing the use of diverse energy sources, including fossil fuels, renewables and waste heat

- Furthermore, AI-driven control systems can dynamically adjust pumps, valves, and heat exchangers to maintain desired temperatures and flow rates, leading to significant energy savings and reduced wear and tear on equipment

- The seamless integration of these digital technologies not only improves the operational efficiency and resilience of district heating systems but also facilitates better customer engagement

- This trend towards more intelligent, intuitive, and interconnected district heating systems is fundamentally reshaping the industry. Companies are actively developing AI-enabled solutions to meet the growing demand for optimized and sustainable heating, driving innovation

District Heating Market Dynamics

Driver

“Growing Focus on Decarbonization and Energy Efficiency”

- The increasing global imperative to reduce carbon emissions and enhance energy efficiency is a primary driver for the heightened demand for district heating systems. As countries and urban areas strive to achieve net-zero emission targets

- For instance, many European nations have implemented stringent environmental regulations and support policies, such as the EU Green Deal and national clean heating programs, which actively promote the development and expansion of district heating networks

- The ability of district heating to recover waste heat from industrial processes, power generation, and even data centers, which would otherwise be lost, further boosts its appeal as an energy-efficient solution

- Furthermore, the growing awareness among consumers and industries regarding the environmental impact of traditional heating methods is driving the adoption of cleaner alternatives

- District heating, by leveraging a diverse mix of heat sources including biomass, geothermal, solar thermal, and large-scale heat pumps, contributes to a more sustainable and environmentally friendly heating infrastructure. This collective push towards a greener energy landscape is accelerating the growth of the district heating market

Restraint/Challenge

“High Initial Capital Investment and Complex Infrastructure Requirements”

- The substantial upfront capital expenditure required for the development of district heating infrastructure poses a significant challenge to broader market penetration and expansion

- For instance, installing insulated pipes underground, especially in densely built urban areas with existing complex underground infrastructure, is technically challenging, time-consuming, and costly. This can lead to higher construction expenses, extended project timelines, and potential disruptions, which may be met with resistance from local communities

- While district heating offers long-term operational cost savings and environmental benefits, the high initial investment can be a barrier for potential investors and limit the expansion of these systems, particularly in smaller communities or regions with limited public funding

- In addition, retrofitting older buildings and heating systems to connect them to district heating networks presents technical and financial hurdles. It often requires extensive renovations and disruptions, making it less appealing to property owners and developers

- Overcoming these challenges will require innovative financing models, strong government support through grants and subsidies, and strategic urban planning to integrate district heating infrastructure during new developments or major urban renewal projects

District Heating Market Scope

The market is segmented on the basis of heat source, plant type, and application.

- By Heat Source

On the basis of heat source, the district heating market is segmented into Coal, Natural Gas, Renewable, Oil and Petroleum Products, and Others. The oil and petroleum products held the largest market revenue share of 41.6% in 2024, driven by their high energy content per unit volume or weight, making them ideal for applications with space and logistical constraints. Their energy density enables compact storage and efficient transportation, allowing widespread use in urban areas where space for fuel storage is limited, ensuring reliable and accessible heat sources.

The renewable segment (including biomass, geothermal, solar thermal, and heat pumps utilizing environmental heat) is anticipated to witness the fastest growth rate of 5.7% from 2025 to 2032, fueled by increasing global focus on decarbonization, stringent environmental policies, and supportive government incentives for clean energy. The imperative to reduce carbon footprints and achieve energy independence is driving substantial investments in integrating diverse renewable sources into district heating systems.

- By Plant Type

On the basis of plant type, the district heating market is segmented into Boiler, combined heat and power, and others. The combined heat and power segment is expected to hold the largest market revenue share of 69.4% in 2024. This dominance is driven by the high energy efficiency of combined heat and power plants, which simultaneously produce electricity and usable heat, significantly reducing overall energy consumption and greenhouse gas emissions. Governments and utilities increasingly favor combined heat and power for its economic benefits and contribution to energy security.

The boiler plant segment is expected to witness the fastest growth rate of 29.3% from 2025 to 2032, fueled by its flexibility and cost-effectiveness in addressing diverse heat demand profiles. Boiler plants support natural gas, biomass, coal, and oil, ensuring operational adaptability amid fluctuating fuel prices and regulatory shifts. Their versatility enables district heating operators to optimize efficiency, integrate sustainable energy sources, and align with local fuel availability requirements.

- By Application

On the basis of application, the district heating market is segmented into residential, commercial, and industrial. The residential segment accounted for the largest market revenue share of 65.6% in 2024, driven by the widespread demand for space heating and hot water in urban residential areas. The convenience, reliability, and cost-effectiveness of centralized heating for large housing complexes, apartments, and urban communities make district heating a favored solution for modern residential developments.

The Commercial segment is expected to witness the fastest growth rate of 4.6% from 2025 to 2032, fueled by the growing need for efficient and sustainable heating solutions in office buildings, retail centers, educational institutions, and healthcare facilities. Businesses increasingly recognize the benefits of district heating, including lower operational costs, reduced on-site emissions, and compliance with green building standards, offering a flexible and controlled heating solution for diverse commercial spaces.

District Heating Market Regional Analysis

- Europe dominates the district heating market with the largest revenue share of 70.5% in 2024, characterized by well-established district heating networks, strong government initiatives, and a high focus on sustainable energy solutions

- Consumers and municipalities in the region highly value the environmental benefits, energy security, and cost-effectiveness offered by district heating systems, which often integrate renewable energy sources and waste heat

- This widespread adoption is further supported by favorable regulatory frameworks, significant investments in network expansion and modernization, and a high awareness of the environmental and economic benefits of centralized heating systems

Europe District Heating Market Insight

The Europe district heating market with the largest revenue share of 70.5% in 2024, projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent energy efficiency regulations, escalating climate change mitigation goals, and the widespread implementation of sustainable urban development plans. The increase in urbanization, coupled with the demand for reliable and clean heating, is fostering the continuous expansion and modernization of district heating networks. European consumers and businesses are also drawn to the environmental benefits and stable heat supply these systems offer. The region is experiencing significant growth across residential, commercial, and multi-family housing applications, with district heating systems being incorporated into both new constructions and renovation projects.

U.K. District Heating Market Insight

The U.K. district heating market is anticipated to grow at a noteworthy CAGR of 6.6% during the forecast period, driven by the escalating trend of decarbonization in the heating sector and a desire for heightened energy efficiency and reliability. In addition, concerns regarding energy security and reducing carbon emissions are encouraging both public and private sectors to choose centralized heating solutions. The UK’s commitment to achieving net-zero emissions, alongside its robust investment in new urban developments and energy infrastructure, is expected to continue to stimulate market growth.

Germany District Heating Market Insight

The Germany district heating market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of climate protection and the demand for technologically advanced, eco-conscious heating solutions. Germany’s well-developed infrastructure, combined with its strong emphasis on energy transition and sustainability, promotes the adoption of district heating, particularly in residential and commercial buildings. The integration of renewable heat sources and waste heat recovery into district heating systems is also becoming increasingly prevalent, with a strong preference for secure, efficient, and environmentally friendly solutions aligning with national energy goals.

Asia-Pacific District Heating Market Insight

The Asia-Pacific district heating market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing urbanization, rapid industrialization, and significant government investments in infrastructure development across countries such as China, Japan, and South Korea. The region's growing energy demand, coupled with rising concerns over air pollution and energy security, is driving the adoption of centralized heating systems. Furthermore, as APAC becomes a key area for new urban developments and smart city initiatives, the affordability and accessibility of district heating solutions are expanding to a wider consumer base.

Japan District Heating Market Insight

The Japan district heating market is gaining momentum due to the country’s high-tech culture, rapid urbanization, and strong demand for energy efficiency and resilience. The Japanese market places a significant emphasis on sustainability and disaster preparedness, and the adoption of district heating is driven by the increasing number of smart cities and eco-friendly building initiatives. The integration of district heating with other urban infrastructure, such as waste heat recovery from industrial facilities and power plants, is fueling growth. Moreover, Japan's focus on innovative energy management solutions is to spur demand for highly efficient, secure heating solutions in both residential and commercial sectors.

China District Heating Market Insight

The China district heating market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to the country's expanding middle class, rapid urbanization, and substantial government investments in large-scale infrastructure projects. China stands as one of the largest consumers of heating energy, and district heating is becoming increasingly popular in northern residential and commercial areas to manage energy consumption, improve air quality, and enhance energy efficiency. The push towards smart cities and the availability of affordable, large-scale district heating solutions, alongside strong domestic manufacturing capabilities, are key factors propelling the market in China.

U.S. District Heating Market Insight

The U.S. district heating market captured a significant revenue share within North America in 2024, fueled by the swift uptake of energy-efficient solutions and the expanding trend of modernizing urban infrastructure. Consumers and building operators are increasingly prioritizing the enhancement of heating efficiency through intelligent, centralized systems. The growing emphasis on reducing environmental impact, combined with robust demand for reliable and cost-effective heating solutions in large commercial and institutional complexes, further propels the U.S. district heating market.

District Heating Market Share

The district heating industry is primarily led by well-established companies, including:

- ALFA LAVAL (Sweden)

- Danfoss (Denmark)

- ENGIE (France)

- Fortum (Finland)

- FVB Energy Inc. (U.S.)

- Keppel Corporation Ltd. (Singapore)

- LOGSTOR A/S (Denmark)

- NRG Energy (U.S.)

- Ramboll Group A/S (Denmark)

- Shinryo Corporation (Japan)

- Statkraft (Norway)

- Vattenfall (Sweden)

- Veolia (France)

- Siemens (Germany)

- General Electric Company (U.S.)

Latest Developments in Global District Heating Market

- In February 2024, Evonik and Uniper formally launched the technical options for thermal energy recovery project in Gelsenkirchen, Germany. This initiative focuses on repurposing industrial waste heat from isophorone production to supply over 1,000 homes in the Ruhr region by the end of 2024. By integrating waste heat into the district heating network, the project enhances energy efficiency and supports sustainable urban heating. The TORTE project is part of broader efforts to reduce carbon emissions and optimize renewable energy use

- In October 2023, South Korea's Naepo district heating Plant officially began commercial operations, utilizing GE Vernova's H-Class combined cycle equipment. This advanced gas turbine-based facility replaces a previously planned solid refuse fuel boiler plant, marking a significant transition towards more efficient and flexible heat generation. The plant supplies approximately 500 megawatts of electricity meter to the national grid while providing district heating for over 100,000 residents in Naepo City. This shift aligns with South Korea’s broader efforts to enhance energy efficiency and reduce carbon emissions

- In October 2023, Gradska toplana, the district heating operator in Niš, Serbia, announced plans to construct a high-capacity heat pump utilizing water from the Nišava River for heating. This initiative is part of a broader effort to replace fossil fuel-fired boilers with cleaner energy solutions, supporting the transition to sustainable district heating. The project aims to reduce carbon emissions and enhance energy efficiency, aligning with Serbia’s commitment to environmentally friendly urban heating. The heat pump will serve as a base heating source, supplemented by other energy inputs as needed

- In April 2023, the European Union approved USD 456.77 million to support the Czech green district heating scheme, reinforcing its commitment to modernizing and decarbonizing heating networks across member states. This initiative aims to transition district heating systems toward sustainable energy sources, reducing carbon emissions and enhancing energy efficiency. The funding will facilitate the installation of renewable heat generation units, including biomass and waste-based systems, ensuring a cleaner and more resilient heating infrastructure. This effort aligns with the European Green Deal objectives

- In March 2023, the United Kingdom's Energy Security Bill introduced new regulations to support heat network zoning, aiming to expand and optimize district heating systems. This initiative recognizes the critical role of heat networks in achieving the UK’s decarbonization goals while reducing reliance on individual fossil fuel heating systems. The regulation enhances consumer protections, ensures cost-effective heat distribution, and promotes low-carbon energy solutions. By enabling efficient heat zoning, the bill supports sustainable urban heating and aligns with the UK’s net-zero strategy

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global District Heating Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global District Heating Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global District Heating Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.