Global Disposable Intravenous Products Market

Market Size in USD Billion

USD

3.16 Billion

USD

4.99 Billion

2025

2033

USD

3.16 Billion

USD

4.99 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.16 Billion | |

| USD 4.99 Billion | |

| % | |

|

Disposable Intravenous Products Market Size

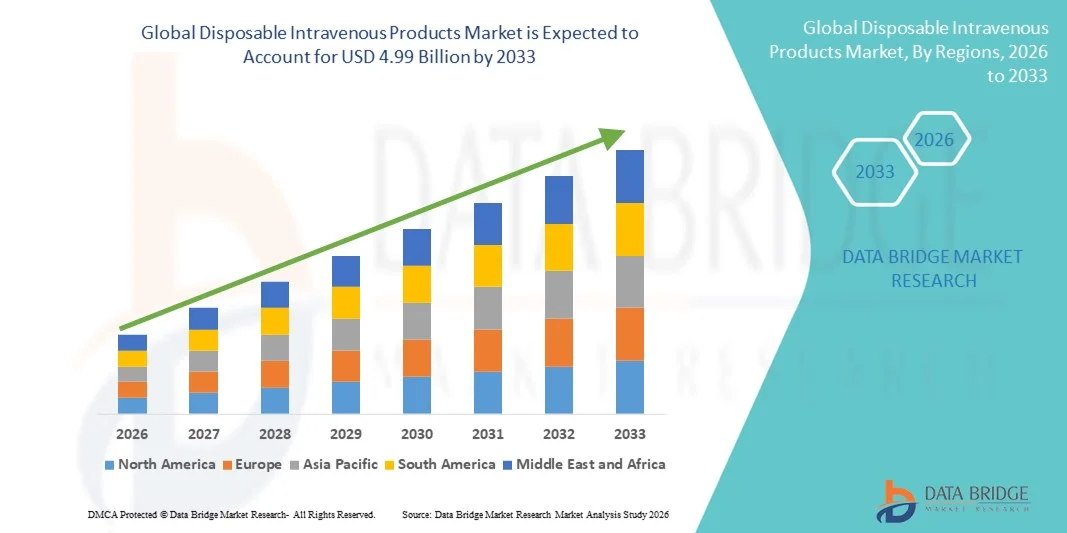

- The global disposable intravenous products market size was valued at USD 3.16 billion in 2025 and is expected to reach USD 4.99 billion by 2033, at a CAGR of 5.90% during the forecast period

- The market growth is largely fueled by the rising volume of hospital admissions, increasing prevalence of chronic diseases, and the growing need for intravenous drug delivery in acute and long-term care settings, leading to higher demand for disposable intravenous products across hospitals, clinics, and ambulatory care centers

- Furthermore, increasing focus on infection prevention, strict regulatory standards for patient safety, and the preference for single-use, sterile medical devices are establishing disposable intravenous products as essential components of modern healthcare delivery. These converging factors are accelerating the uptake of Disposable Intravenous Products solutions, thereby significantly boosting the industry’s growth

Disposable Intravenous Products Market Analysis

- Disposable intravenous products, including IV catheters, infusion sets, syringes, and IV tubing, are essential components of modern healthcare delivery, widely used across hospitals, clinics, and ambulatory care settings to ensure safe, efficient, and sterile administration of fluids, medications, blood products, and nutrients

- The escalating demand for disposable intravenous products is primarily driven by the increasing prevalence of chronic diseases, rising surgical and emergency procedures, and growing emphasis on infection prevention and patient safety, along with a strong preference for single-use medical devices to minimize cross-contamination risks

- North America dominated the disposable intravenous products market with the largest revenue share of approximately 38.5% in 2025, supported by advanced healthcare infrastructure, high hospitalization rates, strong adoption of safety-engineered IV devices, and stringent regulatory standards. The U.S. accounted for a major share due to high procedural volumes and continuous product innovation by leading manufacturers

- Asia-Pacific is expected to be the fastest-growing region in the disposable intravenous products market during the forecast period, driven by expanding healthcare infrastructure, rising healthcare expenditure, increasing patient population, and improving access to hospital and emergency care services across emerging economies

- The IV catheters segment dominated the largest market revenue share of 36.8% in 2025, driven by their extensive and routine use across hospitals, clinics, and emergency care settings

Report Scope and Disposable Intravenous Products Market Segmentation

|

Attributes |

Disposable Intravenous Products Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Baxter International Inc. (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Disposable Intravenous Products Market Trends

Enhanced Efficiency Through Innovation and Safety Improvements

- A significant and accelerating trend in the global disposable intravenous products market is the continuous advancement in product design, material quality, and safety mechanisms to reduce infection risks and improve clinical efficiency. Manufacturers are increasingly focusing on needle-free systems, closed IV delivery systems, and improved flow control to enhance patient safety and healthcare worker protection

- For instance, the growing adoption of needle-free IV connectors and safety-engineered infusion sets has helped minimize the risk of needlestick injuries and catheter-related bloodstream infections (CRBSIs). These innovations are being widely implemented across hospitals, ambulatory surgical centers, and home healthcare settings

- Material innovations, including the use of medical-grade plastics and DEHP-free materials, are gaining traction as healthcare providers prioritize patient safety and regulatory compliance. Disposable IV products are also being designed for improved compatibility with automated infusion pumps and modern clinical workflows

- The increasing emphasis on single-use medical devices to prevent cross-contamination has further reinforced demand for disposable intravenous products, particularly in critical care units, oncology, and emergency medicine

- This trend toward safer, more reliable, and user-friendly disposable IV solutions is reshaping purchasing decisions among healthcare providers, encouraging manufacturers to invest in R&D and product differentiation

- Overall, continuous innovation aimed at infection control, ease of use, and regulatory adherence is driving the evolution of the disposable intravenous products market globally

Disposable Intravenous Products Market Dynamics

Driver

Rising Hospitalization Rates and Growing Demand for Infection Control

- The increasing number of hospital admissions, surgical procedures, and chronic disease cases worldwide is a major driver of demand for disposable intravenous products. IV therapy remains a critical component of fluid administration, medication delivery, blood transfusions, and nutritional support

- For instance, the rising prevalence of chronic conditions such as cancer, cardiovascular diseases, and diabetes has significantly increased the need for long-term and repeated IV treatments, thereby boosting the consumption of disposable IV catheters, infusion sets, and accessories

- Heightened awareness regarding hospital-acquired infections (HAIs) has led healthcare facilities to adopt disposable IV products as a standard infection-prevention measure, replacing reusable alternatives wherever possible

- In addition, the rapid growth of home healthcare and outpatient care services has expanded the use of disposable IV products outside traditional hospital settings, further supporting market growth

- Government initiatives, stricter infection-control guidelines, and investments in healthcare infrastructure—particularly in emerging economies—are also contributing to the sustained demand for disposable intravenous products across the globe

Restraint/Challenge

Environmental Concerns and Cost Pressures

- One of the key challenges facing the disposable intravenous products market is the environmental impact associated with the growing volume of medical waste generated by single-use IV catheters, infusion sets, and related accessories. The widespread reliance on disposable products contributes significantly to plastic waste in healthcare systems worldwide

- For instance, according to reports published by the World Health Organization (WHO), healthcare activities generate millions of tons of medical waste annually, with a substantial portion attributed to disposable medical devices such as intravenous products, prompting hospitals and regulators to reassess waste management practices and sustainability policies

- Disposal and waste management costs associated with disposable IV products can place a financial burden on healthcare facilities, particularly in regions with strict environmental regulations and limited waste-processing infrastructure

- In addition, pricing pressures and reimbursement constraints faced by hospitals and healthcare providers can limit the adoption of premium disposable IV products, especially in cost-sensitive markets

- In low- and middle-income countries, budget limitations often restrict access to advanced disposable IV technologies, leading some facilities to prioritize affordability over enhanced safety or sustainability features

- Addressing these challenges through the development of eco-friendly materials, recyclable components, and cost-efficient manufacturing processes will be critical for sustaining long-term growth in the disposable intravenous products market

Disposable Intravenous Products Market Scope

The market is segmented on the basis of product and end user.

- By Product

On the basis of product, the Disposable Intravenous Products market is segmented into IV catheters, administration sets, infusion sets, securement devices, stopcocks and check valves, drip chambers, needleless connectors, and others. The IV catheters segment dominated the largest market revenue share of 36.8% in 2025, driven by their extensive and routine use across hospitals, clinics, and emergency care settings. IV catheters are essential for fluid delivery, medication administration, blood transfusions, and nutritional support, making them indispensable in both acute and chronic care. Rising hospitalization rates, increasing surgical procedures, and growing prevalence of chronic diseases significantly support segment dominance. Technological advancements such as safety-engineered and antimicrobial-coated catheters further enhance adoption. High usage frequency per patient and recurring replacement needs strengthen revenue generation. Strong demand from emergency departments and intensive care units also fuels growth. Additionally, increasing emphasis on infection prevention supports the use of high-quality disposable IV catheters across healthcare facilities.

The needleless connectors segment is expected to witness the fastest CAGR of 19.6% from 2026 to 2033, owing to rising awareness regarding needlestick injury prevention and hospital-acquired infection control. These devices reduce the risk of bloodborne pathogen transmission and enhance patient and healthcare worker safety. Growing regulatory emphasis on safety-engineered medical devices supports rapid adoption. Increasing use in long-term intravenous therapies and home care settings further accelerates growth. Technological improvements enhancing flow efficiency and compatibility with multiple IV systems also contribute. Expanding outpatient care and infusion therapy services globally reinforce strong CAGR momentum.

- By End User

On the basis of end user, the Disposable Intravenous Products market is segmented into hospitals and clinics, and home care. The hospitals and clinics segment accounted for the largest market revenue share of 72.4% in 2025, driven by high patient inflow, large surgical volumes, and extensive use of intravenous therapies. Hospitals rely heavily on disposable IV products to maintain strict infection control standards and comply with regulatory guidelines. The growing number of inpatient admissions, emergency cases, and intensive care treatments significantly supports segment dominance. Increasing adoption of advanced IV delivery systems in tertiary care hospitals also contributes to revenue share. Furthermore, the presence of skilled healthcare professionals and availability of advanced infrastructure sustain high product consumption. Rising investments in hospital expansion and modernization further reinforce this segment’s leadership.

The home care segment is projected to grow at the fastest CAGR of 21.2% from 2026 to 2033, driven by the rising preference for home-based treatment and long-term intravenous therapies. Increasing prevalence of chronic diseases such as cancer, diabetes, and renal disorders supports demand for home infusion services. Advancements in user-friendly and safe disposable IV products enable wider adoption in non-clinical settings. Cost savings associated with home care compared to hospital stays also accelerate growth. Expanding elderly population and growing focus on patient comfort further fuel demand. The rise of home healthcare providers and supportive reimbursement policies contribute to sustained high growth.

Disposable Intravenous Products Market Regional Analysis

- North America dominated the disposable intravenous products market with the largest revenue share of approximately 38.5% in 2025, supported by advanced healthcare infrastructure, high hospitalization rates, and strong adoption of safety-engineered IV devices across hospitals and ambulatory care settings

- The region benefits from stringent infection control regulations, widespread use of single-use medical products, and high healthcare expenditure, particularly in acute and critical care environments

- Continuous product innovation, strong presence of leading manufacturers, and high procedural volumes further reinforce North America’s leading position in both hospital and outpatient care settings

U.S. Disposable Intravenous Products Market Insight

The U.S. disposable intravenous products market accounted for the largest revenue share within North America in 2025, driven by a high volume of surgical procedures, emergency admissions, and chronic disease management requiring IV therapy. The country’s well-established hospital network and strong focus on patient safety accelerate the adoption of advanced disposable IV catheters, needleless connectors, and infusion accessories. Favorable reimbursement frameworks and strict FDA regulations promote the use of safety-engineered devices. Increasing use of IV therapies in home care and outpatient infusion centers further supports market growth. Ongoing investments in healthcare modernization and continuous innovation by domestic manufacturers continue to strengthen the U.S. market.

Europe Disposable Intravenous Products Market Insight

The Europe disposable intravenous products market is expected to expand at a steady CAGR during the forecast period, driven by rising healthcare demand and strict infection prevention policies across public and private healthcare systems. Increasing surgical volumes, aging population, and growing prevalence of chronic diseases support sustained demand for disposable IV products. European healthcare providers emphasize single-use devices to reduce cross-contamination risks and comply with regulatory standards. The expansion of ambulatory care and outpatient treatment centers also contributes to market growth. Strong government support for healthcare quality and patient safety further fuels adoption across the region.

U.K. Disposable Intravenous Products Market Insight

The U.K. disposable intravenous products market is anticipated to grow at a notable CAGR over the forecast period, supported by increasing NHS expenditure and rising demand for hospital and emergency care services. Growing adoption of disposable IV devices aligns with national infection control initiatives and patient safety guidelines. The increasing burden of chronic diseases and cancer treatments requiring infusion therapy supports product demand. Expansion of home-based care and outpatient infusion services also drives market growth. Continuous upgrades in hospital infrastructure and procurement of advanced IV consumables further strengthen the market outlook.

Germany Disposable Intravenous Products Market Insight

The Germany disposable intravenous products market is projected to grow at a considerable CAGR, driven by a robust healthcare system and high standards for medical safety and hygiene. The country’s strong emphasis on infection prevention and regulatory compliance accelerates adoption of disposable IV products across hospitals and specialty clinics. Rising surgical volumes and increasing use of infusion therapies support market expansion. Germany’s focus on technologically advanced medical consumables and sustainable healthcare practices also contributes to steady demand. Continuous investments in hospital modernization further reinforce market growth.

Asia-Pacific Disposable Intravenous Products Market Insight

The Asia- disposable intravenous products market is expected to register the fastest CAGR during the forecast period, driven by expanding healthcare infrastructure and rapidly growing patient populations. Increasing healthcare expenditure, rising hospitalization rates, and improved access to emergency and critical care services fuel market growth. Governments across the region are investing heavily in hospital expansion and infection control initiatives. Growing medical tourism and rising awareness of hygiene standards further boost demand for disposable IV products. The shift toward single-use medical devices to prevent hospital-acquired infections strongly supports regional growth.

Japan Disposable Intravenous Products Market Insight

The Japan disposable intravenous products market is witnessing steady growth, supported by an aging population and increasing demand for long-term and acute care services. High healthcare quality standards and strict infection control practices drive the use of disposable IV consumables. Rising prevalence of chronic conditions requiring continuous infusion therapy supports sustained demand. Japan’s technologically advanced healthcare system enables rapid adoption of safety-engineered IV devices. Expansion of home healthcare services also contributes to market growth.

China Disposable Intravenous Products Market Insight

The China disposable intravenous products market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid expansion of healthcare infrastructure and increasing patient volumes. Rising government investments in hospital development and public health programs support strong demand for disposable IV products. Growing awareness of infection prevention and adoption of single-use medical devices accelerate market penetration. Increasing surgical procedures and emergency care utilization further strengthen demand. The presence of domestic manufacturers offering cost-effective IV consumables also supports widespread adoption across healthcare facilities.

Disposable Intravenous Products Market Share

The Disposable Intravenous Products industry is primarily led by well-established companies, including:

• Baxter International Inc. (U.S.)

• Terumo Corporation (Japan)

• Fresenius Kabi (Germany)

• ICU Medical, Inc. (U.S.)

• Smiths Medical (U.K.)

• Nipro Corporation (Japan)

• Cardinal Health (U.S.)

• Vygon SA (France)

• Teleflex Incorporated (U.S.)

• Merit Medical Systems (U.S.)

• Zhejiang Weigao Group (China)

• Polymedicure Ltd. (India)

• Hindustan Syringes & Medical Devices (India)

• Medtronic plc (Ireland)

• AngioDynamics (U.S.)

• CODAN Medizinische Geräte GmbH (Germany)

• Renax Biomedical (India)

• Sarstedt AG & Co. (Germany)

Latest Developments in Global Disposable Intravenous Products Market

- In July 2021, Becton Dickinson & Company (BD) announced the acquisition of Tepha, Inc., strengthening BD’s capabilities in advanced biomaterials and supporting the development of next-generation resorbable medical devices relevant to disposable IV components

- In May 2022, Fresenius Kabi completed the acquisition of Ivenix, Inc., expanding its portfolio of infusion therapy solutions and enhancing its ability to deliver disposable IV administration sets and infusion system components across global healthcare settings

- In November 2023, Smiths Medical partnered with major U.S. hospital institutions to adopt needle-free connectors for IV tubing, aiming to reduce needlestick injuries and improve safety for disposable IV products used in clinical workflows

- In December 2023, B. Braun Melsungen AG introduced a series of AI-integrated smart infusion pumps, designed to improve medication delivery accuracy and integrate with electronic health record systems—advancements that drive higher utilization of compatible disposable IV sets and accessories

- In January 2024, BD (Becton Dickinson & Company) expanded its IV solutions portfolio with the launch of a next-generation closed IV catheter system engineered to minimize bloodstream infections and enhance patient safety during intravenous therapy

- In May 2024, Vygon launched a novel closed IV infusion set incorporating antimicrobial connectors designed to reduce infection risk in hospitals and acute care centers, reflecting the industry emphasis on infection control in disposable products

- In July 2024, Becton Dickinson & Company (BD) completed the acquisition of Tepha, Inc. (repeat noted in some industry sources as strategic expansion of advanced intravenous coping materials supporting disposable products)

- In April 2025, BD introduced the HemoSphere Alta platform featuring advanced clinical decision support for hemodynamic monitoring; its adoption drives greater use of disposable pressure transducers, sensor sets, and fluid management accessories associated with IV therapy

- In May 2025, Fresenius Kabi finalized its acquisition of Ivenix, enhancing its infusion therapy portfolio and globally expanding compatible disposable IV tubing sets and connector products integral to modern IV administration

- In March 2025, ICU Medical expanded its portfolio with premixed IV solutions, including new ready-to-administer electrolyte and balanced crystalloid bags designed for ambulatory infusion centers, supporting broader adoption of disposable IV bags and accessory products

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.