Global Display Material Market

Market Size in USD Billion

USD

36.23 Billion

USD

53.57 Billion

2025

2033

USD

36.23 Billion

USD

53.57 Billion

2025

2033

| 2026 - 2033 | |

| USD 36.23 Billion | |

| USD 53.57 Billion | |

| % | |

|

What is the Global Display Material Market Size and Growth Rate?

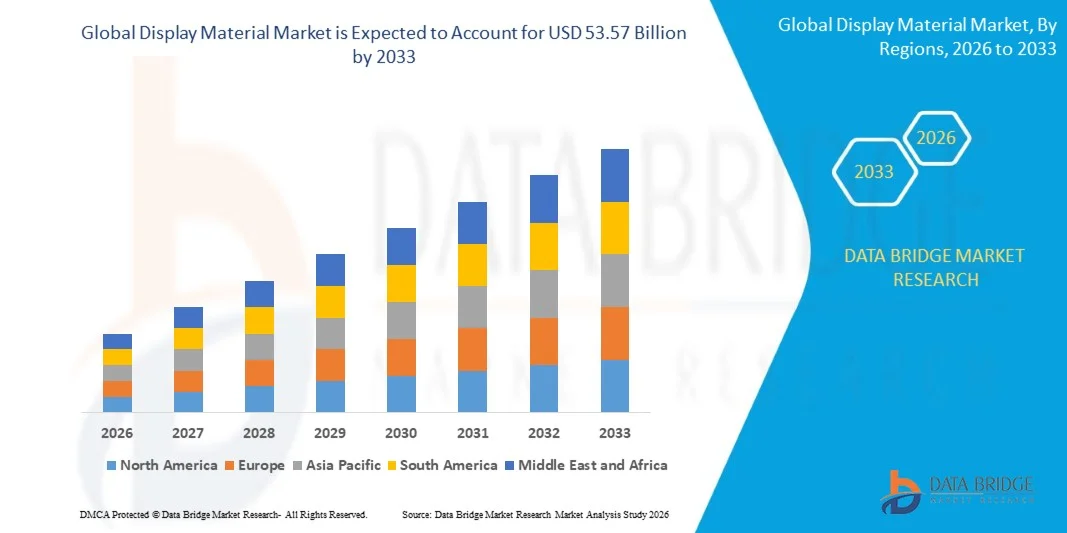

- The global display material market size was valued at USD 36.23 billion in 2025 and is expected to reach USD 53.57 billion by 2033, at a CAGR of 5.01% during the forecast period

- Rising globalization and growth in the focus towards development in manufacturing design and necessity to accomplish production efficacy will emerge as the major market growth driving factors

- Growing production and sale of television units, surging demand from various end user verticals, increasing penetration of smart consumer electronics such as smartphones and laptops especially in the developing economies, and widespread industrialization will further aggravate the market value

What are the Major Takeaways of Display Material Market?

- Growing expenditure to undertake research and development proficiencies, expanding application of organic light-emitting diode (OLED), display technologies and growing demand for optimum resource utilization in regards to the evolution of flexible displays will further carve the way for the growth of the market

- However, high costs associated with the latest display technologies such as transparent display and quantum dot displays and with the research and development proficiencies will act as a growth restraint for the market. Also, stagnant growth of desktop PCs, notebook, and tablets will further dampen the growth rate of the market. Large scale technological limitations in the underdeveloped economies will further challenge the market growth rate

- Asia-Pacific dominated the display material market with a 44.18% revenue share in 2025, driven by strong growth in consumer electronics manufacturing, semiconductor fabrication, display panel production, and smart device assembly activities across China, South Korea, Japan, India, and Southeast Asia

- North America is projected to register the fastest CAGR of 8.69% from 2026 to 2033, driven by rapid growth in premium consumer electronics, automotive digital cockpit systems, healthcare imaging displays, and smart retail signage solutions across the U.S. and Canada

- The Flat Panel segment dominated the market with a 43.7% share in 2025, as it remains the preferred format for televisions, desktops, laptops, commercial signage, and conventional smartphone displays

Report Scope and Display Material Market Segmentation

|

Attributes |

Display Material Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Display Material Market?

“Increasing Shift Toward Flexible, High-Resolution, and Energy-Efficient Display Materials”

- The display material market is witnessing strong adoption of advanced OLED, quantum dot, micro-LED, and flexible display materials designed to support next-generation smartphones, televisions, automotive displays, wearables, and large-format signage

- Manufacturers are introducing high-brightness emissive materials, flexible substrates, advanced polarizers, and encapsulation layers that offer improved color accuracy, thinner form factors, and compatibility with modern display technologies

- Growing demand for cost-efficient, lightweight, and high-performance display solutions is driving usage across consumer electronics, automotive infotainment, retail signage, and healthcare imaging applications

- For instance, companies such as LG Display Co., Ltd., Samsung Electronics Co., Ltd., BOE Technology Group Co., Ltd., and Universal Display Corporation are expanding their display material portfolios with advanced OLED emitters, quantum dot films, and flexible panel materials

- Increasing need for higher refresh rates, ultra-HD resolution, foldable screens, and energy-efficient panels is accelerating the shift toward advanced display materials

- As consumer electronics become more compact and visually sophisticated, display materials will remain vital for next-generation visual performance, durability, and energy optimization

What are the Key Drivers of Display Material Market?

- Rising demand for high-resolution, durable, and energy-efficient display panels to support premium consumer electronics and smart devices is driving market growth

- For instance, in 2025, leading companies such as LG Display Co., Ltd., Samsung Electronics Co., Ltd., and BOE Technology Group Co., Ltd. upgraded their display portfolios with higher brightness OLED panels, flexible substrates, and advanced color enhancement materials

- Growing adoption of smartphones, tablets, televisions, EV displays, AR/VR devices, and digital signage is boosting demand across the U.S., Europe, and Asia-Pacific

- Advancements in organic emitter chemistry, quantum dot films, backlighting units, and encapsulation technologies have strengthened display performance, flexibility, and efficiency

- Rising use of AI-enabled consumer electronics, foldable devices, automotive cockpit displays, and wearable technologies is creating strong demand for advanced display materials

- Supported by steady investments in electronics R&D, semiconductor innovation, and display manufacturing infrastructure, the Display Material market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Display Material Market?

- High costs associated with premium OLED emitters, quantum dot materials, and flexible substrate technologies restrict adoption among cost-sensitive manufacturers

- For instance, during 2024–2025, fluctuations in raw material prices, semiconductor component shortages, and extended supply chain lead times increased production costs for several global vendors

- Complexity in manufacturing high-resolution, foldable, transparent, and ultra-thin display panels increases the need for advanced engineering capabilities and specialized production lines

- Limited awareness in emerging markets regarding premium display technologies and advanced material benefits slows adoption

- Competition from conventional LCD technologies and price-sensitive display alternatives creates pricing pressure and reduces product differentiation

- To address these issues, companies are focusing on cost-optimized materials, improved yield rates, scalable manufacturing, and stronger technology integration to increase global adoption of display materials

How is the Display Material Market Segmented?

The market is segmented on the basis of display type, technology, component and material, panel type, application, and end-use.

• By Display Type

On the basis of display type, the Display Material market is segmented into Flat Panel, Flexible Panel, and Transparent Panel. The Flat Panel segment dominated the market with a 43.7% share in 2025, as it remains the preferred format for televisions, desktops, laptops, commercial signage, and conventional smartphone displays. These panels offer high durability, cost efficiency, broad compatibility, and mature manufacturing processes, making them widely adopted across consumer and enterprise applications. Their strong deployment in household electronics, digital advertising, and professional display systems supports continued segment dominance.

The Flexible Panel segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand for foldable smartphones, wearable devices, automotive curved displays, and next-generation portable electronics. Increasing innovation in flexible substrates and OLED-based architectures is further accelerating growth.

• By Technology

On the basis of technology, the market is segmented into Organic Light-Emitting Diode (OLED), Quantum Dot, Light-Emitting Diode (LED), Liquid Crystal Display (LCD), and Others. The LCD segment dominated the market with a 38.9% share in 2025, supported by its extensive use in televisions, laptops, desktops, industrial monitors, and signage systems. LCD materials continue to maintain strong market presence due to their cost-effectiveness, wide production scale, and stable performance.

The OLED segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing adoption in premium smartphones, smart wearables, automotive displays, and foldable devices. Superior color contrast, thinner form factor, and energy efficiency are accelerating material demand.

• By Component and Material

On the basis of component and material, the market is segmented into Emitter and Organic Layer Materials, Substrate, Encapsulation, Polarizer, Electrodes, Color Filters Layer, Liquid Crystals, Backlighting Unit, and Other LCD Materials. The Emitter and Organic Layer Materials segment dominated the market with a 35.8% share in 2025, driven by increasing use in OLED panels, flexible displays, and high-performance visual systems. These materials are essential for brightness, color rendering, and energy efficiency.

The Encapsulation segment is expected to grow at the fastest CAGR from 2026 to 2033, propelled by rising need for moisture protection, longer panel lifespan, and durability in foldable and transparent displays.

• By Panel Type

On the basis of panel type, the market is segmented into Rigid and Flexible. The Rigid segment dominated the market with a 62.4% share in 2025, supported by widespread use in televisions, desktops, industrial displays, and standard consumer electronics. Established manufacturing ecosystems and lower production costs drive strong adoption.

The Flexible segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising investments in foldable phones, wearable displays, and automotive curved panels.

• By Application

On the basis of application, the market is segmented into Television, Smartphones and Tablets, Laptop, Desktop, Signage/Large Format Display, Automotive, Wearable, and Others. The Smartphones and Tablets segment dominated the market with a 31.6% share in 2025, driven by high-volume production and frequent display upgrades.

The Automotive segment is expected to grow at the fastest CAGR from 2026 to 2033, propelled by increasing deployment in digital cockpit displays, infotainment systems, and ADAS interfaces.

• By End-Use

On the basis of end-use, the market is segmented into Healthcare, Consumer Electronics, Retail, BFSI, Military and Defense, Transportation, and Others. The Consumer Electronics segment dominated the market with a 40.2% share in 2025, driven by extensive use in smartphones, televisions, laptops, tablets, and wearables.

The Healthcare segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by rising demand for medical imaging displays, diagnostic monitors, and portable healthcare devices.

Which Region Holds the Largest Share of the Display Material Market?

- Asia-Pacific dominated the display material market with a 44.18% revenue share in 2025, driven by strong growth in consumer electronics manufacturing, semiconductor fabrication, display panel production, and smart device assembly activities across China, South Korea, Japan, India, and Southeast Asia. High adoption of OLED, LCD, LED, and quantum dot display materials continues to fuel demand across smartphones, televisions, automotive displays, wearables, and large-format signage applications

- Leading companies in Asia-Pacific are introducing advanced OLED emitters, flexible substrates, encapsulation layers, and quantum dot films, strengthening the region’s technological and manufacturing advantage. Continuous investment in foldable displays, high-resolution panels, EV cockpit systems, and next-generation consumer electronics drives long-term market expansion

- Strong electronics manufacturing capacity, integrated supply chains, and sustained investment in advanced display technologies further reinforce regional market leadership

China Display Material Market Insight

China is the largest contributor in Asia-Pacific, supported by strong display panel manufacturing capacity, smartphone production, and large-scale consumer electronics ecosystems. Increasing development of OLED fabrication lines, smart televisions, tablets, and signage solutions intensifies demand for advanced display materials. Presence of large domestic manufacturers and cost-efficient production capabilities further drives market growth.

South Korea Display Material Market Insight

South Korea contributes significantly to regional growth, driven by advanced OLED panel innovation, foldable smartphone development, and premium television manufacturing. Major electronics players increasingly utilize advanced display materials for high-resolution screens, automotive infotainment systems, and wearable devices, strengthening market adoption.

Japan Display Material Market Insight

Japan supports steady market expansion through precision display component manufacturing, advanced material innovation, and automotive display integration. Strong focus on display quality, durability, and high-performance visual systems continues to support long-term growth.

India Display Material Market Insight

India is emerging as a major growth hub, driven by expanding smartphone manufacturing, government-backed electronics production initiatives, and rising domestic demand for consumer electronics. Increasing investments in display assembly and component sourcing further accelerate market penetration.

North America Display Material Market

North America is projected to register the fastest CAGR of 8.69% from 2026 to 2033, driven by rapid growth in premium consumer electronics, automotive digital cockpit systems, healthcare imaging displays, and smart retail signage solutions across the U.S. and Canada. High adoption of OLED panels, flexible displays, transparent screens, and advanced visual technologies increases demand across enterprise and consumer applications. Growth in AR/VR devices, AI-powered consumer electronics, autonomous vehicles, and healthcare monitoring infrastructure continues to accelerate the need for high-performance display materials.

U.S. Display Material Market Insight

The U.S. is the largest contributor in North America, supported by strong consumer electronics demand, advanced automotive display integration, healthcare imaging systems, and technology R&D infrastructure. Increasing deployment of smart displays, premium laptops, wearables, and digital signage solutions further drives market growth.

Canada Display Material Market Insight

Canada contributes significantly to regional growth, driven by rising investment in retail technology, healthcare imaging, transportation systems, and enterprise display infrastructure. Growing demand for advanced display solutions continues to strengthen market adoption across the country.

Which are the Top Companies in Display Material Market?

The display material industry is primarily led by well-established companies, including:

- LG Display Co., Ltd. (South Korea)

- BOE Technology Group Co., Ltd. (China)

- Japan Display Inc. (Japan)

- Koninklijke Philips N.V. (Netherlands)

- Samsung Electronics Co., Ltd. (South Korea)

- Apple Inc. (U.S.)

- Corning Incorporated (U.S.)

- DuPont de Nemours, Inc. (U.S.)

- ASUSTeK Computer Inc. (Taiwan)

- BenQ Materials Corporation (Taiwan)

- AU Optronics Corp. (Taiwan)

- Bolymin Inc. (Taiwan)

- CASIO COMPUTER CO., LTD. (Japan)

- Chunghwa Picture Tubes, Ltd. (Taiwan)

- Planar Systems, Inc. (U.S.)

- Toshiba Corporation (Japan)

- Sony Corporation (Japan)

- Atmel Corporation (U.S.)

- Universal Display Corporation (U.S.)

- Novaled AG (Germany)

What are the Recent Developments in Global Display Material Market?

- In January 2026, Titan Intech introduced its new premium LED display brand, UltraLED Displays, aimed at strengthening India’s domestic display technology ecosystem. The initiative reflects the company’s strategic shift from assembly-led operations toward the development and ownership of core LED display technologies, reinforcing its long-term position in the display materials industry. This development is expected to accelerate innovation, local manufacturing capabilities, and future market growth in advanced display materials

- In November 2025, TSK Corporation entered into a strategic collaboration with Samsung Display Co., Ltd., to jointly advance the large-scale development of next-generation blue OLED display materials. The partnership focuses on improving material efficiency, durability, and performance to support advanced OLED panel applications worldwide. This collaboration is expected to strengthen technological advancements and enhance competitive intensity in the global display materials market

- In September 2024, researchers at KAIST, in collaboration with the Korea Institute of Machinery and Materials, developed South Korea’s first stretchable display material capable of maintaining image clarity under physical stretching. The breakthrough utilizes an innovative auxetic structure with a negative Poisson’s ratio, enabling the material to expand uniformly and minimize image distortion. This innovation is expected to significantly drive growth in flexible electronics and next-generation display material applications

- In February 2024, Helio Display Materials formed a strategic partnership with Haylo Ventures to accelerate the commercialization of its perovskite-based color conversion materials for displays. The alliance specifically targets micro-display applications for AR/VR headsets, marking an important strategic shift in the company’s product development direction. This partnership is expected to support the rapid expansion of immersive display technologies and strengthen future market opportunities

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Display Material Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Display Material Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Display Material Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.