Global Digital Diabetes Management Market

Market Size in USD Billion

USD

23.35 Billion

USD

48.62 Billion

2024

2032

USD

23.35 Billion

USD

48.62 Billion

2024

2032

| 2025 - 2032 | |

| USD 23.35 Billion | |

| USD 48.62 Billion | |

| % | |

|

Digital Diabetes Management Market Size

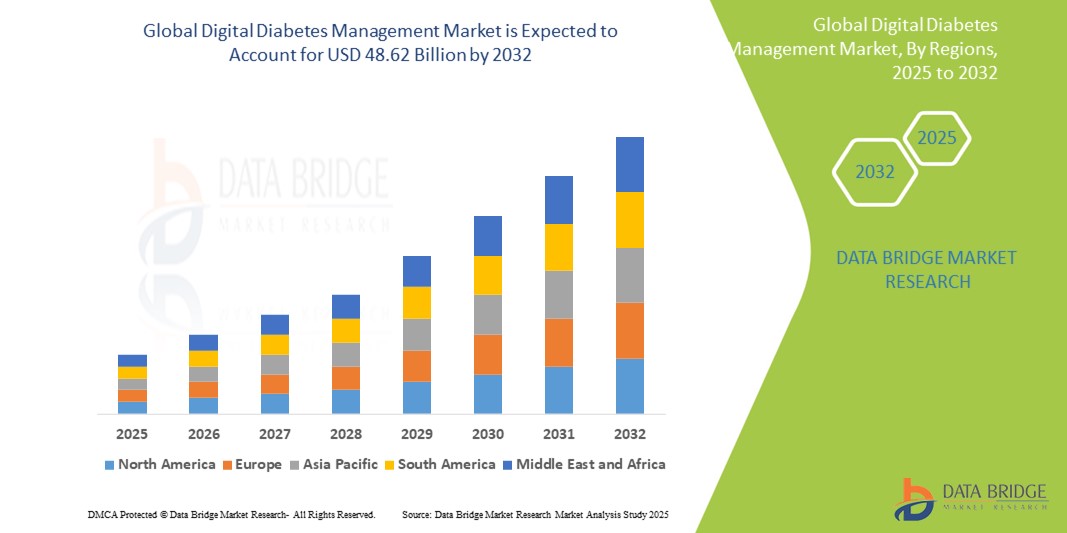

- The global digital diabetes management market size was valued at USD 23.35 billion in 2024 and is expected to reach USD 48.62 billion by 2032, at a CAGR of 9.60% during the forecast period

- Market growth is primarily driven by the increasing global prevalence of diabetes, rising adoption of digital health technologies, and growing awareness about real-time glucose monitoring and lifestyle management

- In addition, the market is benefiting from improved smartphone penetration, supportive reimbursement frameworks, and a growing preference for personalized, data-driven diabetes care solutions across major economies

Digital Diabetes Management Market Analysis

- The digital diabetes management industry is evolving toward more integrated ecosystems, combining continuous glucose monitoring (CGM), smart insulin delivery systems, and AI-based decision support to improve outcomes

- There is a rising demand for mobile health apps, cloud-based platforms, and wearable insulin pumps that offer convenience, real-time insights, and seamless doctor-patient data sharing

- Advancements in AI, increasing investments in digital therapeutics, and strategic collaborations between tech giants and healthcare providers are fostering innovation, expanding accessibility, and enhancing user engagement globally

- North America dominates the global digital diabetes management market with the largest revenue share of 39.62% as of 2024, driven by advanced healthcare infrastructure and widespread adoption of connected health solutions

- Asia-Pacific is expected to register the fastest growth in the digital diabetes management market through 2032 with the highest CAGR of 11.35%, fueled by rapid urbanization, increasing internet penetration, and a rising diabetic population

- The devices segment dominated the market with a revenue share of 38.7% in 2024, due to the widespread use of continuous glucose monitors (CGMs) and smart insulin pens

Report Scope and Digital Diabetes Management Market Segmentation

|

Attributes |

Digital Diabetes Management Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Digital Diabetes Management Market Trends

“Increasing Adoption of Connected Devices and AI-Driven Technologies”

- A major trend shaping the digital diabetes management market is the rising adoption of connected glucose monitoring systems and smart insulin delivery devices. These technologies enable real-time glucose tracking, data sharing with healthcare providers, and proactive treatment adjustments

- For Instance, in early 2025, Medtronic unveiled an updated InPen app with a missed meal dose detection feature, enhancing dosing accuracy and integration with the Simplera CGM system

- The development of AI-powered diabetes management platforms is also transforming care by providing personalized insights, predictive alerts, and automated insulin recommendations, improving patient adherence and outcomes

- Another trend is the integration of wearable devices with digital diabetes apps, creating comprehensive ecosystems that track blood sugar, physical activity, diet, and medication adherence all in real time

- The market is further driven by the increasing availability of cloud-based platforms that enable remote patient monitoring, ensuring continuity of care and early intervention for at-risk patients

- As healthcare moves towards value-based care, digital diabetes solutions are being embraced for their potential to reduce complications, hospitalizations, and long-term healthcare costs

Digital Diabetes Management Market Dynamics

Driver

“Rising Diabetes Prevalence and Technological Advancements”

- The global rise in diabetes prevalence, especially type 2 diabetes, is a primary driver for the digital diabetes management market. With over 500 million people affected worldwide, there is a growing demand for accessible and efficient disease management tools

- For instance, Abbott’s collaboration with Tandem Diabetes Care to integrate the FreeStyle Libre 2 Plus sensor with the t:slim X2 pump underscores the push toward hybrid closed-loop systems that help maintain blood glucose within target ranges

- Advancements in CGM technology, smart pens, and mobile health apps are making it easier for patients to manage diabetes independently while enabling clinicians to make informed decisions

- The increasing acceptance of telemedicine and digital health platforms also supports broader adoption, particularly in remote and underserved regions

- Supportive government initiatives and reimbursement frameworks in major markets further bolster investment and adoption of digital diabetes solutions

Restraint/Challenge

“High Device Costs and Data Privacy Concerns”

- One of the key restraints in the market is the high cost of digital diabetes devices, particularly for continuous glucose monitors (CGMs) and automated insulin delivery systems, which can be prohibitive for patients without comprehensive insurance

- In some regions, limited reimbursement and high out-of-pocket expenses hinder widespread adoption, especially among lower-income populations

- In addition, the complexity of device integration with existing healthcare IT systems and electronic health records (EHRs) can be a challenge for providers

- Data privacy and cybersecurity concerns also act as a barrier, as patients may be hesitant to share sensitive health data over cloud platforms

- Moreover, lack of digital literacy, particularly among elderly or rural populations, can limit the effective use of these technologies, necessitating user education and support programs

Digital Diabetes Management Market Scope

The market is segmented on the basis of product and services, type, application, and end-user.

- By Product and Services

On the basis of product and services, the market is segmented into devices, digital diabetes management apps, data management software and platforms, and services. The devices segment dominated the market with a revenue share of 38.7% in 2024, owing to the widespread use of continuous glucose monitors (CGMs) and smart insulin pens. These devices enable real-time tracking and management of blood glucose levels, contributing significantly to patient adherence and glycemic control. Their integration with smartphones and wearable health technologies has expanded their adoption among both patients and healthcare providers.

The digital diabetes management apps segment is anticipated to grow at the fastest CAGR from 2025 to 2032, driven by increasing smartphone penetration, rising awareness about diabetes self-management, and enhanced features such as AI-driven analytics and personalized feedback.

- By Type

On the basis of type, the market is segmented into wearable devices and handheld devices. The wearable devices segment led the market with a market share of 56.2% in 2024, owing to their ability to provide continuous, non-invasive monitoring and improved patient convenience. Devices such as smartwatches, glucose monitoring patches, and fitness trackers are gaining traction as they integrate seamlessly into daily life, supporting proactive disease management.

The handheld devices segment is projected to grow steadily, particularly in low-resource settings where affordability and portability are key considerations.

- By Application

On the basis of application, the market is segmented into diabetes and blood glucose tracking apps and obesity and diet management apps. The diabetes and blood glucose tracking apps segment dominated the market with a revenue share of 63.5% in 2024, reflecting the growing global burden of diabetes and the need for effective glycemic control tools. These apps offer features such as real-time tracking, alerts for glucose fluctuations, and integration with medical records, making them indispensable in modern diabetes care.

The obesity and diet management apps segment is expected to witness rapid growth, supported by the rising prevalence of obesity, increasing health consciousness, and growing adoption of preventive healthcare practices.

- By End User

On the basis of end user, the market is segmented into home care settings, diabetes clinics, academic and research institutes, and others. The home care settings segment dominated the market with a share of 49.8% in 2024, due to the growing preference for remote monitoring and self-management of chronic diseases. The availability of user-friendly digital health tools empowers patients to track and manage their conditions from the comfort of their homes, reducing hospital visits and healthcare costs.

The diabetes clinics segment is expected to grow at the fastest rate, driven by the increasing number of specialized centers offering integrated diabetes care, advanced diagnostics, and patient education programs.

Digital Diabetes Management Market Regional Analysis

- North America dominates the global digital diabetes management market with the largest revenue share of 39.62% as of 2024, driven by advanced healthcare infrastructure and widespread adoption of connected health solutions

- The U.S. leads the region due to high diabetes prevalence, favorable reimbursement policies, and widespread integration of digital technologies such as mobile health apps and wearable glucose monitors

- Strong governmental support for telehealth and ongoing innovation by major market players enhance the market environment. The growing demand for remote monitoring tools and personalized diabetes management platforms continues to bolster regional growth

U.S. Digital Diabetes Management Market Insight

The U.S. digital diabetes management market dominates within North America, supported by a robust healthcare system, strong consumer awareness, and the rapid incorporation of digital tools into chronic disease management. High smartphone penetration and insurance coverage for digital health tools contribute to significant adoption. Leading players such as Dexcom, Medtronic, and Abbott are actively developing integrated platforms combining CGM (Continuous Glucose Monitoring) systems with AI-powered applications. Furthermore, collaborations between health-tech firms and insurance providers promote long-term patient engagement, accelerating market growth and positioning the U.S. as a global hub for digital diabetes innovation.

Canada Digital Diabetes Management Market Insight

The Canadian digital diabetes management market is showing consistent growth, supported by a well-developed healthcare infrastructure and rising awareness about the benefits of digital health solutions. Government initiatives focusing on chronic disease prevention and digital transformation in healthcare services are encouraging the adoption of smart insulin pens, health apps, and data analytics tools. The increasing prevalence of Type 2 diabetes and aging population demographics further elevate the demand for self-monitoring tools and digital care platforms. The market also benefits from public-private partnerships aimed at integrating technology into long-term diabetes care programs.

Asia-Pacific Digital Diabetes Management Market Insight

Asia-Pacific is expected to register the fastest growth in the digital diabetes management market through 2032 with the highest CAGR of 11.35%, fueled by rapid urbanization, increasing internet penetration, and a rising diabetic population. Countries such as China, India, and South Korea are witnessing significant investments in digital health infrastructure and mobile health technologies. The region’s growing middle-class population and government efforts to modernize healthcare delivery are accelerating the adoption of mobile apps and wearable glucose monitors. In addition, the surge in smartphone users and digital literacy among younger demographics makes Asia-Pacific a hotspot for innovation and market expansion.

China Digital Diabetes Management Market Insight

China is a key contributor to the Asia-Pacific digital diabetes management market, supported by a large diabetic population and expanding healthcare infrastructure. The government’s “Healthy China 2030” initiative promotes digital transformation in healthcare, including diabetes management tools. High mobile phone usage, a growing health-tech startup ecosystem, and increasing collaborations between hospitals and technology firms support widespread adoption of glucose monitoring apps, wearable CGM devices, and AI-powered diagnostics. The rising awareness about lifestyle-related diseases and increased availability of cost-effective digital solutions are expected to further drive market growth in the coming years.

Japan Digital Diabetes Management Market Insight

Japan’s digital diabetes management market is expanding steadily due to its aging population, high prevalence of chronic diseases, and strong emphasis on precision medicine. The country’s advanced technology infrastructure and government support for digital health innovation facilitate the adoption of remote monitoring systems and AI-integrated diabetes apps. In addition, collaborations between pharmaceutical companies and tech firms are fostering the development of sophisticated platforms that offer personalized care. Patients in Japan increasingly prefer digital solutions for self-management, and hospitals are incorporating telehealth services, contributing to sustained market momentum across urban and rural areas alike.

Europe Digital Diabetes Management Market Insight

Europe is experiencing steady growth in the digital diabetes management market, driven by increasing healthcare digitization and a strong focus on early intervention for chronic diseases. Countries such as Germany, France, and the U.K. are leading the way with their adoption of CGM devices, mobile health platforms, and cloud-based data management systems. EU-wide policies promoting digital innovation and patient empowerment have further fueled demand. In addition, high levels of health literacy and insurance coverage in most European countries make it easier for patients to access and engage with digital health technologies on a regular basis.

U.K. Digital Diabetes Management Market Insight

The U.K. market for digital diabetes management is expanding rapidly, supported by the National Health Service’s (NHS) initiatives to integrate digital health into chronic care pathways. The country has seen increasing adoption of diabetes-focused mobile apps, remote monitoring tools, and AI-based decision support systems. Startups and established firms are actively collaborating with healthcare providers to deliver personalized digital solutions. The NHS’s long-term plan includes improving digital access to care and enhancing self-management options for diabetic patients, which is anticipated to further elevate demand and improve clinical outcomes in the coming years.

Germany Digital Diabetes Management Market Insight

Germany is one of the fastest-growing markets in Europe for digital diabetes management, fueled by its well-established healthcare infrastructure and a proactive regulatory framework that supports digital therapeutics. The Digital Healthcare Act (DVG) allows for reimbursement of approved digital health applications (DiGA), encouraging both providers and patients to adopt digital solutions for chronic disease management. Leading healthcare institutions are leveraging data-driven platforms for real-time glucose monitoring and patient engagement. With the increasing prevalence of Type 1 and Type 2 diabetes, Germany is focusing on scaling digital diabetes tools to ensure long-term healthcare sustainability.

Digital Diabetes Management Market Share

The digital diabetes management industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- PHC Holdings Corporation (Japan)

- WellDoc, Inc (India)

- Sanofi (France)

- Dexcom, Inc (U.S.)

- DarioHealth Corp. (U.S.)

- Medtronic (Ireland)

- B. Braun AG (Germany)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Insulet Corporation (U.S.)

- Ascensia Diabetes Care Holdings AG (Switzerland)

- Tidepool (U.S.)

- Medtronic (Ireland)

- Tandem Diabetes Care (U.S.)

- LifeScan (U.S.)

- AgaMatrix (U.S.)

- Glooko Inc. (U.S.)

- DarioHealth (Israel)

Latest Developments in Global Anti-Counterfeit Packaging Market

- In November 2024, Medtronic plc received FDA clearance for its InPen app, which now features a missed meal dose detection function. This enhancement supports the company’s plan to introduce its Smart MDI system integrated with the Simplera continuous glucose monitor (CGM). This development marks a significant step toward more intelligent and responsive diabetes management

- In January 2024, Abbott and Tandem Diabetes Care, Inc. announced the integration of the t:slim X2 insulin pump with Control-IQ technology and Abbott's FreeStyle Libre 2 Plus sensor in the U.S. market. This hybrid closed-loop system helps users manage and prevent both hyperglycemia and hypoglycemia. This collaboration enhances automated insulin delivery, improving patient outcomes

- In April 2023, Insulet Corporation obtained FDA clearance for its Omnipod GO, a wearable insulin delivery device tailored for adults with type 2 diabetes who require long-acting insulin. The device offers a more user-friendly alternative to conventional daily injection methods. This innovation provides greater convenience and adherence for individuals managing type 2 diabetes

- In February 2023, Dexcom officially launched the Dexcom G7 continuous glucose monitoring (CGM) system in the U.S., with planned expansions into Europe and Asia-Pacific scheduled for the first quarter of 2024. This launch broadens access to advanced CGM technology across global markets

- In October 2022, Abbott Laboratories introduced the Freestyle Libre 3 CGM device globally, offering real-time glucose tracking in a compact and easy-to-use format. This global release demonstrates Abbott’s continued leadership in continuous glucose monitoring innovation

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.