Global Data Centre Liquid Cooling Market

Market Size in USD Billion

CAGR :

%

USD

3.52 Billion

USD

20.95 Billion

2025

2033

USD

3.52 Billion

USD

20.95 Billion

2025

2033

| 2026 –2033 | |

| USD 3.52 Billion | |

| USD 20.95 Billion | |

| % | |

|

Data Centre Liquid Cooling Market Size

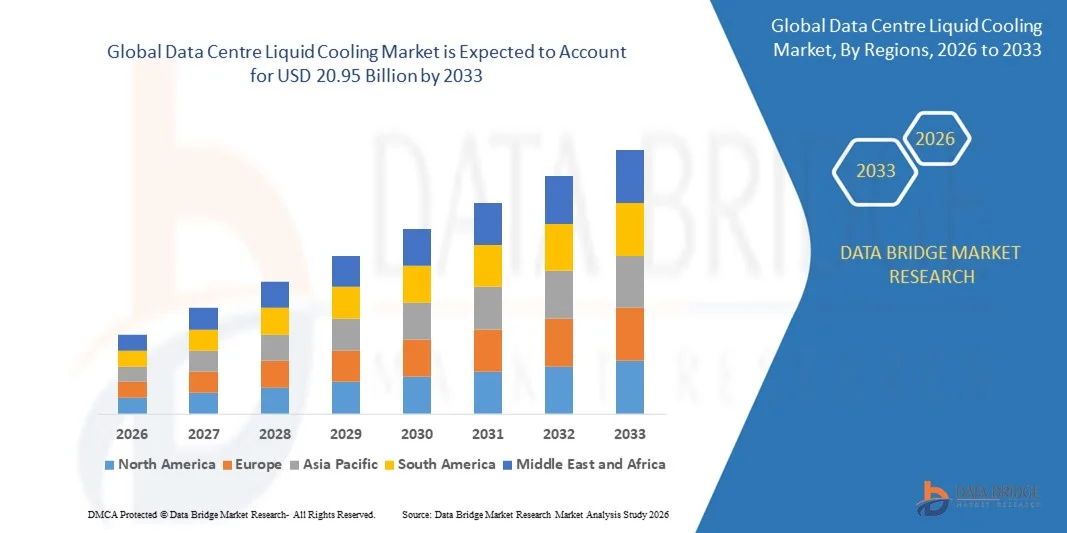

- The global data centre liquid cooling market size was valued at USD 3.52 billion in 2025 and is expected to reach USD 20.95 billion by 2033, at a CAGR of 24.96% during the forecast period

- The market growth is largely fuelled by the rapid increase in data centre density driven by AI workloads, high-performance computing, and cloud infrastructure expansion

- Rising limitations of traditional air cooling systems and the need for efficient heat dissipation in hyperscale and edge data centres are accelerating adoption

Data Centre Liquid Cooling Market Analysis

- The market is characterized by strong technological innovation, with increasing adoption of direct-to-chip and immersion cooling technologies across hyperscale and enterprise data centres

- Growing investments from cloud service providers and colocation operators, along with supportive regulations for energy-efficient data centres, are strengthening long-term market growth

- North America dominated the data centre liquid cooling market with the largest revenue share in 2025, driven by the rapid expansion of hyperscale data centres, rising adoption of high-performance computing, and increasing deployment of AI and cloud workloads

- Asia-Pacific region is expected to witness the highest growth rate in the global data centre liquid cooling market, driven by rising internet penetration, growing cloud adoption, expanding hyperscale and edge data centres, and increasing investments in high-performance and sustainable cooling technologies

- The solutions segment held the largest market revenue share in 2025, driven by the increasing deployment of liquid cooling systems such as cold plates and immersion solutions across high-density data centres. Liquid cooling solutions enable efficient heat dissipation, improved energy efficiency, and reliable performance for advanced workloads such as AI, HPC, and cloud computing, making them a preferred choice among data centre operators

Report Scope and Data Centre Liquid Cooling Market Segmentation

|

Attributes |

Data Centre Liquid Cooling Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Data Centre Liquid Cooling Market Trends

Rising Adoption Of High-Density Computing And AI Workloads

- The increasing deployment of high-density servers, AI workloads, and advanced computing applications is significantly shaping the data centre liquid cooling market, as traditional air-cooling systems struggle to manage rising heat loads efficiently. Liquid cooling solutions are gaining traction due to their superior heat dissipation, reduced energy consumption, and ability to support compact, high-performance data centre architectures. This trend is strengthening adoption across hyperscale, colocation, and enterprise data centres, encouraging operators to modernize cooling infrastructure

- Growing investments in AI, machine learning, cloud computing, and high-performance computing are accelerating the demand for liquid cooling technologies. Data centres supporting these workloads require consistent thermal management to ensure reliability, performance stability, and reduced downtime. Liquid cooling enables operators to maintain optimal operating temperatures while lowering power usage effectiveness, aligning with efficiency and performance goals

- Sustainability and energy efficiency objectives are influencing purchasing decisions, with data centre operators emphasizing reduced carbon footprint, lower water usage, and compliance with environmental regulations. Liquid cooling systems support these goals by minimizing energy-intensive cooling processes and enabling heat reuse strategies. As a result, operators are increasingly integrating liquid cooling into new builds and retrofitting existing facilities

- For instance, in 2024, Google in the U.S. and Microsoft in the U.S. expanded the deployment of liquid cooling technologies across selected hyperscale data centres to support AI-driven workloads. These implementations were aimed at improving energy efficiency, reducing cooling-related emissions, and supporting next-generation server architectures. The projects also reinforced long-term sustainability commitments and operational cost optimization

- While adoption is accelerating, sustained market growth depends on continued technological advancements, standardization, and integration compatibility with existing data centre infrastructure. Vendors and operators are focusing on improving system reliability, scalability, and total cost of ownership to support broader adoption across different data centre sizes

Data Centre Liquid Cooling Market Dynamics

Driver

Rising Demand For Energy Efficient And Sustainable Data Centre Operations

- Increasing pressure to reduce energy consumption and operational costs is a major driver for the data centre liquid cooling market. Data centre operators are adopting liquid cooling solutions to address escalating power densities while achieving better thermal efficiency compared to conventional air cooling. This shift supports compliance with energy efficiency targets and sustainability regulations

- Expanding use of hyperscale and colocation data centres is influencing market growth, as these facilities require advanced cooling systems to manage large-scale, high-density server deployments. Liquid cooling enables improved space utilization and consistent performance, supporting the rapid expansion of cloud services and digital infrastructure

- Technology providers and data centre operators are actively investing in liquid cooling through infrastructure upgrades, pilot projects, and strategic partnerships. These efforts are supported by the growing emphasis on environmental responsibility and long-term cost savings, encouraging collaboration between cooling solution providers, server manufacturers, and data centre operators

- For instance, in 2023, Amazon Web Services in the U.S. and Equinix in the U.S. reported increased adoption of liquid cooling technologies in new data centre developments. These initiatives were driven by the need to support high-performance workloads, improve energy efficiency, and align with corporate sustainability goals, enhancing operational resilience and scalability

- Despite strong demand drivers, continued growth will depend on reducing implementation complexity, improving interoperability, and optimizing costs. Ongoing innovation in cooling architectures and materials will be critical to maintaining performance advantages and supporting widespread adoption

Restraint/Challenge

High Initial Investment And Integration Complexity

- The high upfront cost associated with liquid cooling systems compared to traditional air-cooling solutions remains a key challenge, particularly for small and mid-sized data centre operators. Expenses related to system installation, specialized infrastructure, and skilled personnel contribute to higher capital investment requirements

- Integration complexity and concerns around compatibility with existing data centre layouts can slow adoption. Retrofitting older facilities with liquid cooling systems often requires significant design modifications and downtime planning, creating operational and financial barriers for operators

- Maintenance and reliability considerations also impact market growth, as liquid cooling systems involve fluid management, leak prevention, and monitoring requirements. Operators must invest in advanced control systems, staff training, and preventive maintenance to ensure long-term system performance

- For instance, in 2024, enterprise data centre operators in Germany and Singapore reported slower adoption of liquid cooling due to high retrofit costs and concerns over operational risk. Some operators delayed implementation in favor of incremental air-cooling upgrades, citing budget constraints and limited technical expertise

- Addressing these challenges will require cost-effective system designs, standardized solutions, and increased awareness of long-term efficiency benefits. Collaboration between equipment manufacturers, data centre operators, and technology providers will be essential to reduce complexity, improve confidence, and unlock the full growth potential of the global data centre liquid cooling market

Data Centre Liquid Cooling Market Scope

The market is segmented on the basis of component, type of cooling, data center types, enterprise, and end user.

- By Component

On the basis of component, the data centre liquid cooling market is segmented into solutions and services. The solutions segment held the largest market revenue share in 2025, driven by the increasing deployment of liquid cooling systems such as cold plates and immersion solutions across high-density data centres. Liquid cooling solutions enable efficient heat dissipation, improved energy efficiency, and reliable performance for advanced workloads such as AI, HPC, and cloud computing, making them a preferred choice among data centre operators.

The services segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising need for installation, maintenance, monitoring, and optimization services associated with liquid cooling infrastructure. As data centre operators increasingly adopt complex cooling architectures, demand for specialized support services is growing to ensure system reliability, reduce downtime, and optimize operational efficiency, particularly in large-scale and hyperscale facilities.

- By Type Of Cooling

On the basis of type of cooling, the data centre liquid cooling market is segmented into cold plate liquid cooling, immersion liquid cooling, and spray liquid cooling. The cold plate liquid cooling segment accounted for the largest market revenue share in 2025, supported by its widespread adoption in existing data centre infrastructure due to easier integration and compatibility with standard server designs. Cold plate systems offer targeted cooling for high-heat components such as CPUs and GPUs, improving thermal efficiency while minimizing changes to overall facility layout.

The immersion liquid cooling segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rapid increase in power-dense computing applications and the need for superior cooling efficiency. Immersion cooling provides uniform heat removal, reduced energy consumption, and lower operational costs, making it increasingly attractive for hyperscale data centres and next-generation computing environments.

- By Data Center Types

On the basis of data center types, the market is segmented into small and mid-sized data centers and large data centers. Large data centers held the largest market revenue share in 2025, driven by high server density, extensive cloud infrastructure, and increasing deployment of AI and big data workloads. These facilities require advanced cooling solutions to manage high thermal loads and maintain energy efficiency, supporting the adoption of liquid cooling technologies.

Small and mid-sized data centers are expected to witness steady growth from 2026 to 2033, supported by the rising adoption of edge computing and regional data facilities. As these data centers seek efficient cooling solutions to manage growing workloads within limited space, liquid cooling is gaining traction due to its ability to deliver higher performance with reduced energy consumption.

- By Enterprise

On the basis of enterprise, the data centre liquid cooling market is segmented into BFSI, IT and telecom, media and entertainment, healthcare, government and defence, retail, research and academic, and others. The IT and telecom segment dominated the market in 2025, driven by the rapid expansion of cloud services, 5G infrastructure, and data-intensive applications. High-performance computing requirements and continuous network operations are accelerating the adoption of liquid cooling solutions in this segment.

The research and academic segment is expected to witness the fastest growth rate from 2026 to 2033, supported by increasing investments in supercomputing, AI research, and data-driven scientific studies. Liquid cooling is increasingly preferred in research facilities due to its ability to support high-density computing environments while maintaining thermal stability and energy efficiency.

- By End User

On the basis of end user, the data centre liquid cooling market is segmented into cloud providers, colocation providers, enterprises, and hyperscale data centres. Hyperscale data centres accounted for the largest market revenue share in 2025, driven by massive data processing requirements, large-scale cloud deployments, and the growing adoption of AI and machine learning workloads. These facilities increasingly rely on liquid cooling to manage extreme power densities and reduce operational costs.

Cloud providers are expected to witness the fastest growth rate from 2026 to 2033, driven by the continued expansion of cloud computing services and the need to improve energy efficiency across large server farms. Liquid cooling enables cloud providers to optimize cooling performance, reduce carbon footprint, and support scalable infrastructure to meet rising global data demand.

Data Centre Liquid Cooling Market Regional Analysis

- North America dominated the data centre liquid cooling market with the largest revenue share in 2025, driven by the rapid expansion of hyperscale data centres, rising adoption of high-performance computing, and increasing deployment of AI and cloud workloads

- Data centre operators in the region prioritize energy efficiency, thermal performance, and sustainability, accelerating the shift from traditional air cooling to advanced liquid cooling technologies

- This strong adoption is further supported by high capital investments, advanced digital infrastructure, and stringent energy efficiency regulations, positioning liquid cooling as a preferred solution across enterprise and hyperscale data centres

U.S. Data Centre Liquid Cooling Market Insight

The U.S. data centre liquid cooling market captured the largest revenue share in 2025 within North America, fueled by the growing density of servers, increasing AI workloads, and rapid expansion of cloud service providers. Data centre operators are increasingly adopting liquid cooling solutions to manage heat dissipation and reduce energy consumption. The strong presence of hyperscale cloud providers and continuous investments in next-generation data centres are significantly supporting market growth.

Europe Data Centre Liquid Cooling Market Insight

The Europe data centre liquid cooling market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent energy efficiency regulations and strong sustainability mandates. Rising data traffic, digital transformation initiatives, and increasing adoption of green data centres are encouraging the deployment of liquid cooling technologies. Growth is observed across colocation, enterprise, and hyperscale facilities, particularly in urban and high-density locations.

U.K. Data Centre Liquid Cooling Market Insight

The U.K. data centre liquid cooling market is expected to witness the fastest growth rate from 2026 to 2033, supported by increasing cloud adoption, expansion of colocation facilities, and rising focus on carbon reduction. The demand for efficient cooling solutions is growing as data centres handle higher power densities. Government initiatives promoting sustainable infrastructure and energy-efficient technologies are further supporting market expansion.

Germany Data Centre Liquid Cooling Market Insight

The Germany data centre liquid cooling market is expected to witness the fastest growth rate from 2026 to 2033, driven by strong industrial digitization, emphasis on energy efficiency, and growing investments in high-performance computing. Germany’s advanced infrastructure and focus on sustainability are accelerating the adoption of liquid cooling solutions. Data centre operators are increasingly integrating liquid cooling to meet regulatory requirements and optimize operational efficiency.

Asia-Pacific Data Centre Liquid Cooling Market Insight

The Asia-Pacific data centre liquid cooling market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid digitalization, increasing internet penetration, and expanding cloud and AI deployments in countries such as China, Japan, and India. Rising data centre construction and growing demand for efficient cooling solutions are boosting adoption. The region’s role as a global data centre expansion hub further strengthens market growth.

Japan Data Centre Liquid Cooling Market Insight

The Japan data centre liquid cooling market is expected to witness the fastest growth rate from 2026 to 2033 due to increasing demand for high-performance computing, limited space for data centre expansion, and strong focus on energy efficiency. Japanese operators are adopting liquid cooling to manage high server densities and reduce operational costs. Integration with advanced IT infrastructure and smart energy management systems is further supporting growth.

China Data Centre Liquid Cooling Market Insight

The China data centre liquid cooling market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to massive investments in cloud computing, AI, and digital infrastructure. Rapid expansion of hyperscale data centres, government support for data centre modernization, and the need to manage high power densities are driving adoption. The availability of cost-effective liquid cooling solutions and strong domestic manufacturers further propel market growth.

Data Centre Liquid Cooling Market Share

The Data Centre Liquid Cooling industry is primarily led by well-established companies, including:

- Asetek (Denmark)

- Schneider Electric (France)

- Vertiv (U.S.)

- Rittal (Germany)

- CoolIT Systems (Canada)

- Stulz (Germany)

- Green Revolution Cooling (U.S.)

- Midas Green Technologies (U.S.)

- Evapco (U.S.)

- Wikstrøm Cooling Solutions (Finland)

Latest Developments in Global Data Centre Liquid Cooling Market

- In June 2024, Perstorp, a specialty chemicals company under PETRONAS Chemicals Group Berhad (PCG), entered into a strategic partnership with Intel’s Open IP Advanced Liquid Cooling team to develop a synthetic thermal management fluid for immersion cooling in data centers. The solution, leveraging Intel’s SuperFluid technology, enhances cooling efficiency and boosts thermal management capacity from 500 W to 800 W per chip, supporting high-density data center operations and promoting advanced liquid cooling adoption

- In May 2024, STULZ Modular, a modular data center solutions provider and subsidiary of STULZ GmbH, collaborated with Asperitas to explore advanced immersion cooling technologies. The partnership focuses on integrating immersion cooling into modular data center designs for both indoor and outdoor deployments, improving thermal performance, energy efficiency, and scalability in high-density environments, thereby driving liquid cooling innovation in the market

- In April 2024, Schneider Electric announced a USD 438.4 million investment in India to establish a strategic manufacturing hub for data center cooling solutions. The opening of a facility in Bengaluru with an initial USD 130 million investment aims to support India’s rapidly expanding data center ecosystem, enhance local production capabilities, and ensure timely deployment of advanced cooling technologies, strengthening Schneider Electric’s market presence in Asia-Pacific

- In March 2024, Daikin Applied launched the Navigator WW water-cooled screw chiller using the low-GWP R-513A refrigerant, offering an energy-efficient and environmentally sustainable cooling solution. Paired with the optional Templifier TW water heater for heat recovery, the system improves cost-effectiveness, reduces carbon footprint, and provides reliable cooling for data centers and industrial facilities, promoting sustainable thermal management

- In February 2024, SK Enmove signed a Memorandum of Understanding (MOU) with SK Telecom and Precision Liquid Cooling Iceotope Technologies to advance next-generation liquid cooling solutions. The collaboration focuses on developing efficient and sustainable thermal management technologies, addressing the rising demand for advanced cooling in data centers, and supporting the adoption of innovative, high-performance liquid cooling systems globally

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.