Global Contrast And Imaging Agents In Interventional X Ray Market

Market Size in USD Billion

USD

5.83 Billion

USD

9.37 Billion

2024

2032

USD

5.83 Billion

USD

9.37 Billion

2024

2032

| 2025 - 2032 | |

| USD 5.83 Billion | |

| USD 9.37 Billion | |

| % | |

|

Contrast and Imaging Agents in Interventional X-Ray Market Size

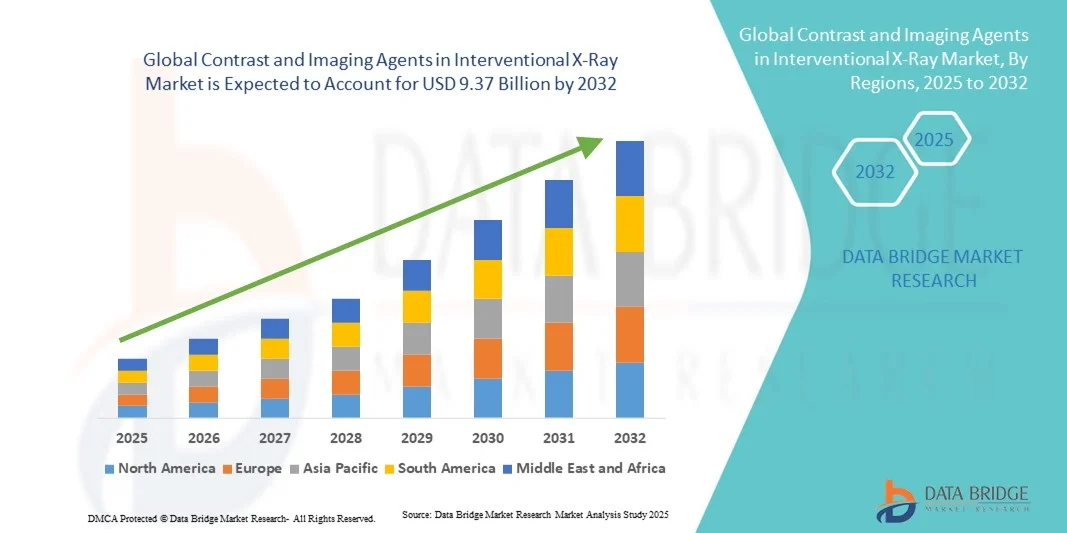

- The global contrast and imaging agents in interventional x-ray market size was valued at USD 5.83 billion in 2024 and is expected to reach USD 9.37 billion by 2032, at a CAGR of 6.1% during the forecast period

- The market growth is largely fueled by rising adoption of minimally invasive procedures and technological advancements in imaging agents, improving diagnostic accuracy and procedural safety

- Furthermore, increasing prevalence of cardiovascular diseases, cancer, and chronic conditions, coupled with growing demand for precise and efficient interventional procedures, is establishing contrast and imaging agents as essential tools in modern interventional radiology. These converging factors are accelerating market adoption, thereby significantly boosting the industry’s growth

Contrast and Imaging Agents in Interventional X-Ray Market Analysis

- Contrast and imaging agents, providing enhanced visualization during interventional X-ray procedures, are increasingly vital components of modern diagnostic and therapeutic practices in both hospitals and specialized clinics due to their ability to improve procedural accuracy, patient safety, and real-time imaging quality

- The escalating demand for these agents is primarily fueled by the growing adoption of minimally invasive procedures, increasing prevalence of cardiovascular diseases and cancers, and rising preference for precise, efficient imaging solutions in interventional radiology

- North America dominated the contrast and imaging agents market with the largest revenue share of 38.9% in 2024, characterized by advanced healthcare infrastructure, high adoption of interventional procedures, and a strong presence of key industry players, with the U.S. experiencing substantial growth in usage driven by technological innovations from both established pharmaceutical and medical imaging companies

- Asia-Pacific is expected to be the fastest-growing region in the contrast and imaging agents market during the forecast period due to expanding healthcare facilities, rising patient awareness, and increasing government investments in diagnostic and interventional imaging technologies

- Iodinated contrast media dominated the market with a share of 55.6% in 2024, driven by their long-established efficacy, widespread clinical adoption, and compatibility with a broad range of interventional X-ray procedures

Report Scope and Contrast and Imaging Agents in Interventional X-Ray Market Segmentation

|

Attributes |

Contrast and Imaging Agents in Interventional X-Ray Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Contrast and Imaging Agents in Interventional X-Ray Market Trends

Advancements Through AI-Assisted Imaging and Real-Time Visualization

- A significant and accelerating trend in the global interventional X-ray contrast and imaging agents market is the integration of AI-assisted imaging and real-time visualization systems, significantly enhancing procedural accuracy and diagnostic confidence

- For instance, GE Healthcare’s AI-powered imaging platform enables real-time dose optimization and image reconstruction during complex cardiovascular interventions, improving both patient safety and clinician efficiency

- AI integration allows contrast agents to be more precisely targeted, reducing required volumes and potential adverse reactions. Some Siemens Healthineers systems analyze prior imaging data to optimize contrast injection protocols, enhancing procedural outcomes

- The seamless combination of AI analytics with imaging agents facilitates predictive insights during interventions, allowing clinicians to anticipate complications and adjust procedures in real time

- This trend towards more intelligent, data-driven imaging is fundamentally reshaping clinical expectations in interventional radiology. Consequently, companies such as Bracco are developing AI-enabled contrast agents with enhanced visualization capabilities and protocol optimization

- The demand for imaging agents compatible with AI-enhanced X-ray systems is growing rapidly across hospitals and specialty clinics, as healthcare providers increasingly prioritize efficiency, safety, and precision in interventional procedures

Contrast and Imaging Agents in Interventional X-Ray Market Dynamics

Driver

Rising Demand Due to Minimally Invasive Procedures and Chronic Disease Prevalence

- The increasing prevalence of cardiovascular diseases, cancers, and other chronic conditions, coupled with growing adoption of minimally invasive procedures, is a significant driver for the heightened demand for interventional imaging agents

- For instance, in 2023, Bracco introduced advanced low-osmolality contrast agents designed for safer cardiovascular interventions, aiming to improve patient outcomes and procedural efficiency

- As hospitals adopt more image-guided interventional procedures, contrast agents provide critical real-time visualization, allowing clinicians to navigate complex anatomy with greater precision

- Furthermore, the rising popularity of hybrid operating rooms and interventional suites is making imaging agents an essential component of these integrated clinical systems, enabling seamless procedural workflow

- The ability to reduce contrast volume, lower radiation exposure, and improve diagnostic clarity is propelling the adoption of advanced contrast agents in both diagnostic and therapeutic interventional procedures

- Expansion of outpatient interventional centers and ambulatory surgery facilities is increasing the overall demand for safe, efficient, and easy-to-administer contrast agents

- Continuous innovation in low-toxicity and targeted contrast agents is creating growth opportunities in high-risk patient populations, driving adoption in specialty hospitals and oncology centers

Restraint/Challenge

Safety Concerns and Regulatory Hurdles

- Potential adverse reactions, including nephrotoxicity and allergic responses, pose significant challenges to wider adoption of contrast agents in interventional X-ray procedures

- For instance, reports of contrast-induced nephropathy have made some clinicians cautious, particularly for high-risk patients with pre-existing kidney conditions

- Addressing these safety concerns through low-osmolality formulations, personalized dosing protocols, and improved patient screening is critical to maintaining clinical trust. In addition, stringent regulatory approval processes for new contrast agents can delay market entry and increase development costs, limiting rapid adoption

- While newer, safer agents are being developed, the high cost of advanced imaging solutions compared to conventional agents can hinder uptake, particularly in emerging markets

- Overcoming these challenges through rigorous safety protocols, clinical education, and cost-effective agent development will be vital for sustained growth of the global interventional imaging agents market

- Limited awareness and training among clinicians regarding new contrast protocols can slow adoption, necessitating focused educational initiatives by companies and healthcare institutions

- Supply chain constraints and reliance on a few key manufacturers for specialized contrast agents can create market vulnerability and impact timely availability, especially in high-demand regions

Contrast and Imaging Agents in Interventional X-Ray Market Scope

The market is segmented on the basis of agent type, application, and end user.

- By Agent Type

On the basis of agent type, the market is segmented into iodinated contrast media, barium-based contrast media, microbubble contrast media, gold nanoparticle contrast agents, and others. The iodinated contrast media segment dominated the market with the largest revenue share of 55.6% in 2024, driven by its well-established clinical use in cardiovascular, neurological, and general interventional procedures. Iodinated agents are highly compatible with a broad range of imaging equipment and provide high-quality visualization, making them the preferred choice in hospitals and specialized interventional centers. Their long-standing safety profile, reliability, and effectiveness in both routine and complex procedures further contribute to their dominance. In addition, ongoing improvements in low-osmolality formulations enhance patient safety, expanding their adoption across high-risk populations. Clinicians often rely on iodinated media for precise anatomical delineation, which is critical in minimally invasive interventions. The segment benefits from widespread availability and cost-effectiveness compared to newer, niche contrast agents.

The microbubble contrast media segment is anticipated to witness the fastest growth rate of 12.5% CAGR from 2024 to 2032, fueled by its increasing use in echocardiography, oncology, and liver imaging applications. Microbubble agents enhance ultrasound-based imaging, providing real-time perfusion and tissue characterization, which is particularly valuable in early disease detection and targeted therapy monitoring. The growing preference for non-invasive and radiation-free imaging in pediatrics and cardiology further accelerates adoption. Technological innovations improving bubble stability and imaging clarity are expanding their clinical utility. Their ability to work synergistically with AI-assisted imaging systems enhances procedural precision. Hospitals and diagnostic centers are rapidly incorporating microbubble agents to improve patient outcomes and procedural efficiency.

- By Application

On the basis of application, the market is segmented into cardiology, gastroenterology, neurology, oncology, urology, and general surgery. The cardiology segment dominated the market with the largest revenue share of 35% in 2024, driven by the high prevalence of cardiovascular diseases and growing adoption of minimally invasive cardiac interventions such as angiography and percutaneous coronary interventions. Cardiologists rely heavily on contrast agents for real-time imaging to navigate complex vascular anatomy safely. The demand is further fueled by the integration of hybrid operating rooms and advanced interventional suites that require high-quality imaging agents. Technological advancements improving image clarity and reducing contrast volumes increase procedural safety and patient comfort. The established clinical protocols and extensive use of iodinated agents in cardiology procedures reinforce market dominance. In addition, government initiatives and awareness programs targeting cardiovascular disease detection support steady growth.

The oncology segment is expected to witness the fastest growth rate of 11.8% CAGR from 2024 to 2032, driven by the rising global cancer incidence and increasing adoption of image-guided interventions such as tumor ablation, biopsy, and targeted therapy monitoring. Contrast agents enable accurate tumor visualization, early detection, and procedural precision, which are critical in improving patient outcomes. Advanced imaging modalities and hybrid systems that combine X-ray, CT, and ultrasound further expand the use of contrast agents in oncology. Rising investment in oncology-focused diagnostic infrastructure across hospitals and specialty centers is accelerating adoption. The growing emphasis on personalized medicine and precision oncology also fuels demand for innovative, targeted contrast solutions. In addition, ongoing research into nanoparticle-based agents for enhanced tumor imaging supports long-term growth.

- By End User

On the basis of end user, the market is segmented into imaging centers, hospitals, clinics, diagnostic centers, ambulatory surgical centers, and private practices. The hospital segment dominated the market with the largest revenue share of 50% in 2024, due to hospitals offering the widest range of interventional procedures, advanced imaging infrastructure, and high patient volumes. Hospitals conduct complex cardiac, neurological, and oncological interventions that require high-quality contrast agents and real-time imaging support. The availability of hybrid ORs, full-time radiology staff, and integration of AI-assisted imaging platforms enhances procedural efficiency and safety. Hospitals often prefer established contrast media with proven clinical efficacy and low adverse reaction rates. Large-scale procurement and long-term supply agreements further reinforce the segment’s market dominance. The hospital segment also benefits from increasing healthcare expenditures and governmental support for advanced medical imaging adoption.

The diagnostic centers segment is anticipated to witness the fastest growth rate of 13% CAGR from 2024 to 2032, fueled by rising outpatient imaging procedures, cost-effectiveness, and increasing demand for non-invasive diagnostics. Diagnostic centers are rapidly adopting advanced X-ray and CT imaging suites requiring contrast agents for specialized interventions. The growth is further driven by urbanization, increasing patient awareness, and preference for early disease detection. Integration with AI-based imaging software improves diagnostic precision and procedural efficiency. Collaboration with hospitals for pre- and post-operative imaging is expanding their utilization of contrast agents. In addition, the proliferation of standalone imaging centers in emerging markets is accelerating segment growth.

Contrast and Imaging Agents in Interventional X-Ray Market Regional Analysis

- North America dominated the contrast and imaging agents market with the largest revenue share of 38.9% in 2023, characterized by advanced healthcare infrastructure, high adoption of interventional procedures, and a strong presence of key industry players, with the U.S. experiencing substantial growth in usage driven by technological innovations from both established pharmaceutical and medical imaging companies

- Healthcare providers in the region highly value the precision, real-time imaging capabilities, and improved patient safety offered by modern contrast agents during cardiovascular, neurological, and oncological interventions

- This widespread adoption is further supported by high healthcare spending, well-established interventional radiology programs, and a technologically advanced clinician base, establishing contrast and imaging agents as essential tools for hospitals, diagnostic centers, and specialized interventional suites

U.S. Contrast and Imaging Agents in Interventional X-Ray Market Insight

The U.S. contrast and imaging agents market captured the largest revenue share of 40% in 2024 within North America, fueled by the rapid adoption of advanced interventional procedures and hybrid imaging suites. Hospitals and specialty centers are increasingly prioritizing patient safety, precision, and real-time visualization through high-quality contrast agents. The growing use of minimally invasive cardiology, neurology, and oncology procedures, combined with AI-assisted imaging systems, further propels the market. Moreover, the availability of low-osmolality and targeted contrast agents is significantly contributing to the market’s expansion, supported by a technologically advanced clinician base and well-established healthcare infrastructure.

Europe Contrast and Imaging Agents in Interventional X-Ray Market Insight

The Europe market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising prevalence of chronic diseases and government initiatives promoting minimally invasive procedures. Increasing adoption of hybrid operating rooms and image-guided interventions is fostering the use of advanced contrast agents. European healthcare providers are also attracted to contrast agents offering enhanced diagnostic accuracy and reduced adverse effects. The region is experiencing significant growth across cardiology, oncology, and neurology applications, with agents being incorporated into both new interventional suites and upgrades of existing facilities.

U.K. Contrast and Imaging Agents in Interventional X-Ray Market Insight

The U.K. market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing interventional radiology procedures and a focus on patient safety. In addition, concerns regarding procedure-related complications are encouraging hospitals and clinics to adopt high-quality contrast agents. The U.K.’s robust healthcare infrastructure, coupled with early adoption of AI-enhanced imaging systems, is expected to continue to stimulate market growth, particularly in cardiovascular and oncological interventions.

Germany Contrast and Imaging Agents in Interventional X-Ray Market Insight

The Germany market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of advanced imaging techniques and demand for patient-centric care. Germany’s well-developed hospital infrastructure, combined with emphasis on clinical innovation and safety, promotes adoption of both traditional and next-generation contrast agents. Integration of contrast agents with hybrid interventional suites and AI-assisted imaging platforms is increasingly prevalent, with hospitals seeking precise, low-risk solutions for complex procedures.

Asia-Pacific Contrast and Imaging Agents in Interventional X-Ray Market Insight

The Asia-Pacific market is poised to grow at the fastest CAGR of 12% during the forecast period of 2024 to 2032, driven by expanding healthcare infrastructure, rising prevalence of cardiovascular and oncological diseases, and increasing government support for minimally invasive procedures. Countries such as China, Japan, and India are rapidly upgrading interventional radiology capabilities, which fuels demand for contrast agents. Furthermore, as APAC emerges as a manufacturing and distribution hub for medical imaging products, affordability and accessibility of contrast agents are improving, allowing broader adoption across hospitals, diagnostic centers, and outpatient clinics.

Japan Contrast and Imaging Agents in Interventional X-Ray Market Insight

The Japan market is gaining momentum due to the country’s high-tech medical culture, rapid urbanization, and focus on precision medicine. The Japanese market emphasizes patient safety and diagnostic accuracy, and the adoption of advanced contrast agents is driven by the increasing number of minimally invasive procedures. Integration of contrast media with AI-assisted imaging systems and hybrid operating rooms is fueling growth. Moreover, Japan’s aging population is such asly to spur demand for safer, easier-to-administer imaging solutions in both residential healthcare facilities and specialized interventional centers.

India Contrast and Imaging Agents in Interventional X-Ray Market Insight

The India market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to expanding healthcare infrastructure, rapid urbanization, and growing prevalence of chronic diseases. India stands as one of the largest emerging markets for interventional procedures, and contrast agents are becoming increasingly important in hospitals, diagnostic centers, and outpatient facilities. Government initiatives promoting minimally invasive procedures, along with the availability of cost-effective imaging solutions and strong domestic manufacturers, are key factors propelling the market in India.

Contrast and Imaging Agents in Interventional X-Ray Market Share

The Contrast and Imaging Agents in Interventional X-Ray industry is primarily led by well-established companies, including:

- Bracco. (Italy)

- GE HealthCare (U.S.)

- Guerbet (U.S.)

- Bayer AG (Germany)

- Lantheus (U.S.)

- Beilu Pharmaceutical Co., Ltd. (China)

- Iso-Tex Diagnostics, Inc. (U.S.)

- Novartis AG (Switzerland)

- FUJIFILM Corporation (Japan)

- DAIICHI SANKYO COMPANY, LIMITED (Japan)

- JB Chemicals and Pharmaceuticals Ltd. (India)

- Unijules Life Sciences Ltd. (India)

- Mallinckrodt (U.S.)

- Hikma Pharmaceuticals PLC (U.K.)

- Amgen Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Samsung (South Korea)

What are the Recent Developments in Global Contrast and Imaging Agents in Interventional X-Ray Market?

- In June 2025, Bayer submitted gadoquatrane, a new low-dose macrocyclic gadolinium-based contrast agent, to the U.S. Food and Drug Administration (FDA) for approval. If approved, gadoquatrane would become the lowest-dose macrocyclic gadolinium-based contrast agent available in the U.S. market. This submission follows promising results from Bayer’s Phase III QUANTI clinical program, which assessed the efficacy and safety of gadoquatrane across a broad patient population

- In March 2025, advancements in the development of new contrast agents were reported, focusing on improving diagnostic accuracy, enhancing patient safety, and enabling more personalized approaches to therapy. These developments aim to push the envelope in terms of image quality and diagnostic detail, addressing the evolving needs of the medical imaging field

- In January 2025, GE Healthcare announced a €132 million investment to expand its media fill and finish manufacturing site in Cork, Ireland. This expansion includes a new state-of-the-art facility expected to produce 25 million more yearly patient doses of contrast media by 2027, addressing the growing global demand for contrast agents used in X-ray, CT, and interventional procedures

- In October 2023, the global shortage of iodinated contrast media led to discussions about the necessity of contrast usage, overuse in current protocols, and alternative imaging techniques. Strategies such as reducing contrast-enhanced CT performance and deferring diagnostic imaging were considered to combat the shortage

- In February 2023, the U.S. FDA approved a new gadolinium-based contrast agent for use in adults and children aged 2 and older. This agent uses half the dose of gadolinium contained in most GBCAs and boasts the highest relaxivity of all approved GBCAs, maintaining image quality at a lower dose. This approval marks a significant advancement in reducing gadolinium exposure while enhancing imaging quality

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.