Global Clinical Laboratory Tests Market

Market Size in USD Billion

USD

139.26 Billion

USD

269.44 Billion

2025

2033

USD

139.26 Billion

USD

269.44 Billion

2025

2033

| 2026 - 2033 | |

| USD 139.26 Billion | |

| USD 269.44 Billion | |

| % | |

|

Clinical Laboratory Tests Market Overview

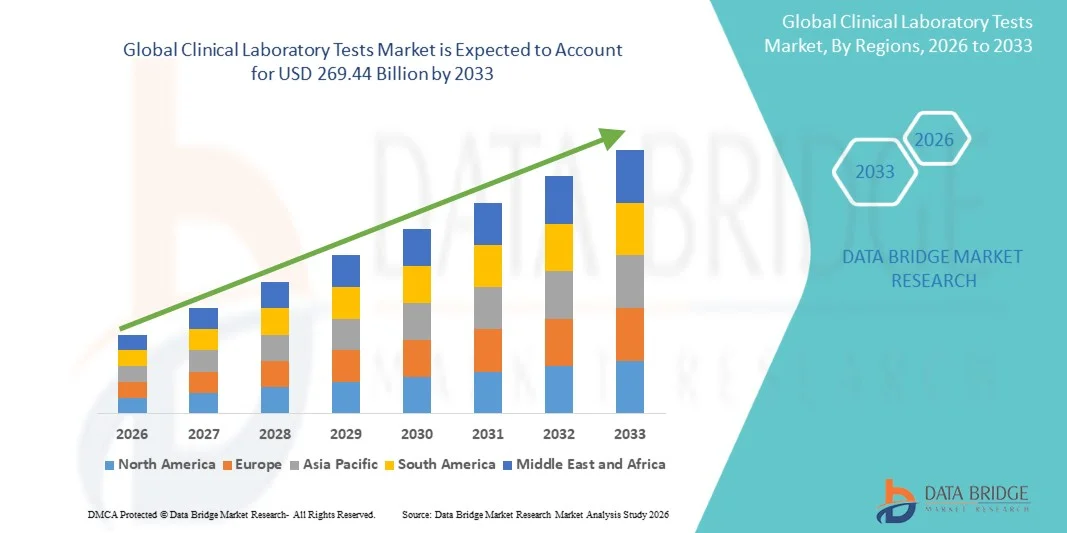

The Clinical Laboratory Tests Market was valued at USD 139.26 billion in 2025 and is projected to reach USD 269.44 billion by 2033, growing at a CAGR of 8.60% from 2026 to 2033. The market is witnessing steady expansion driven by the rising burden of chronic and infectious diseases, increasing demand for early and accurate disease diagnosis, and continuous advancements in diagnostic technologies including molecular testing and automated analyzers.

The growing global focus on preventive healthcare, routine health screening, and personalized medicine is significantly boosting the adoption of clinical laboratory testing services. In addition, the rising geriatric population, expansion of healthcare infrastructure in emerging economies, and increasing outsourcing of diagnostic services to independent laboratories are further accelerating market growth. Technological innovations such as high-throughput testing platforms, AI-enabled diagnostics, and integration of digital pathology are enhancing efficiency, accuracy, and turnaround time across clinical laboratories worldwide.

Key Market Trends & Insights

- North America dominated the Clinical Laboratory Tests Market with the largest revenue share of 38.62% in 2025, supported by strong healthcare infrastructure, high diagnostic testing volume, and widespread adoption of advanced molecular diagnostics.

- The Clinical Chemistry Tests segment led the market with a 29.47% share in 2025, driven by widespread use in routine diagnostics, chronic disease monitoring, and preventive health screening

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.6% from 2026 to 2033, fueled by expanding healthcare access, rising disease burden, increasing awareness of early diagnosis, and rapid laboratory infrastructure development in China and India.

- HbA1c Tests are the fastest-growing test type, projected to register a CAGR of 9.8%, reflecting the surge in the rising global prevalence of diabetes and increasing emphasis on long-term glucose monitoring.

- The Immunoassay-based Testing segment dominated the technology category with a 34.12% revenue share in 2025, led by its wide application in infectious disease detection, hormone analysis, and routine diagnostic screening.

- Hematology accounted for 28.63% of the market, preferred by high utilization of complete blood count (CBC) and related tests for routine diagnostics and disease monitoring.

- The Immunology/Serology segment is the fastest-growing application category, with a CAGR of 10.6%, driven by rising incidence of autoimmune diseases and infectious conditions requiring antibody-based detection.

Market Size & Forecast

- Global Market Value (2025): USD 139.26 Billion

- Expected Market Value (2033): USD 269.44 Billion

- Forecast CAGR (2026–2033): 8.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Clinical Laboratory Tests Market Segmentation

|

Attributes |

Clinical Laboratory Tests Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Quest Diagnostics Inc. (U.S.) · Labcorp (U.S.) · Sonic Healthcare Limited (Australia) · Eurofins Scientific SE (Luxembourg) · Charles River Laboratories (U.S.) · Bio-Rad Laboratories, Inc. (U.S.) · Thermo Fisher Scientific Inc. (U.S.) · Abbott (U.S.) · SYNLAB International GmbH (Germany) · F. Hoffmann-La Roche Ltd (Switzerland) · Siemens Healthineers AG (Germany) · Danaher Corporation (U.S.) · PerkinElmer Inc. (U.S.) · Illumina, Inc. (U.S.) · QIAGEN (Netherlands) · BD (U.S.) · Agilent Technologies, Inc. (U.S.) · Beckman Coulter, Inc. (U.S.) · Randox Laboratories Ltd (U.K.) · ARUP Laboratories (U.S.) |

|

Market Opportunities |

· Expansion of AI-enabled clinical diagnostics and automated laboratory workflows · Rising demand for preventive health screening and at-home sample collection services · Rapid growth of precision medicine and biomarker-based testing |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Clinical Laboratory Tests Market Trends

Trend: Expansion of Automated and High-Throughput Diagnostic Testing

Clinical laboratories are increasingly adopting automated analyzers and high-throughput platforms to handle rising test volumes and reduce turnaround time across chemistry, hematology, and molecular diagnostics. Integration of digital laboratory information systems and AI-enabled interpretation tools is improving workflow efficiency, reducing human error, and supporting large-scale population screening programs. The shift toward fully automated lab ecosystems is also enabling standardized reporting and faster clinical decision-making, especially in hospital and reference laboratory settings. For instance, large diagnostic networks are deploying integrated automation lines for routine blood chemistry and immunoassay testing.

Clinical Laboratory Tests Market Dynamics

Key Market Driver: Rising Prevalence of Chronic and Infectious Diseases

The increasing global burden of chronic conditions such as diabetes, cardiovascular diseases, and cancer, along with recurring infectious disease outbreaks, is significantly driving demand for clinical laboratory testing services. Early diagnosis and continuous disease monitoring are becoming essential components of modern healthcare systems, leading to higher test volumes across routine and specialized diagnostics. Expanding healthcare access and growing preventive screening awareness are further accelerating laboratory utilization worldwide. For instance, national screening programs for diabetes and infectious diseases are expanding testing coverage in both developed and emerging economies.

Key Restraint/Challenge: High Cost of Advanced Diagnostic Infrastructure

A major restraint in the clinical laboratory tests market is the high cost associated with advanced diagnostic instruments, molecular testing platforms, and automated laboratory systems. Small and mid-sized laboratories often face financial constraints in adopting next-generation sequencing, PCR-based diagnostics, and fully automated analyzers due to high procurement, maintenance, and operational expenses. In addition, reimbursement limitations in several regions further restrict widespread adoption of advanced testing technologies. For instance, smaller diagnostic labs in developing regions continue to rely on semi-automated systems due to budget constraints and infrastructure limitations.

Key Market Opportunity: Expansion of Precision Medicine and Biomarker-Based Testing

The growing shift toward precision medicine is creating significant opportunities for biomarker-driven and genetic testing services across oncology, rare diseases, and personalized treatment pathways. Advances in molecular diagnostics, next-generation sequencing, and companion diagnostics are enabling more accurate disease classification and targeted therapy selection. Increasing collaboration between pharmaceutical companies and diagnostic laboratories is further expanding test development pipelines. For instance, oncology-focused biomarker panels are increasingly used to guide targeted cancer therapies in specialized diagnostic centers.

Clinical Laboratory Tests Market Scope

The clinical laboratory tests market is segmented on the basis of test type, technology, application, and end users.

- By Test Type

On the basis of test type, the Clinical Laboratory Tests Market is segmented into clinical chemistry tests, complete comprehensive tests, complete blood count (CBC), basic metabolic panel (BMP), HGB/HCT tests, HbA1c tests, BUN creatinine tests, electrolyte tests, renal panel tests, lipid panel tests, routine tests, specialty tests, and others. The Clinical Chemistry Tests segment dominated the market with a 29.47% share in 2025, driven by widespread use in routine diagnostics, chronic disease monitoring, and preventive health screening. These tests are fundamental in assessing organ function, metabolic conditions, and overall patient health status. High test volumes across hospitals and diagnostic laboratories further strengthen its dominance. Increasing prevalence of diabetes, cardiovascular diseases, and kidney disorders is significantly supporting demand. Automation in chemistry analyzers and integration with digital laboratory systems is improving efficiency and accuracy. The segment remains the backbone of clinical laboratory workflows globally.

The HbA1c Tests segment is projected to register the fastest growth during the forecast period at a CAGR of 9.8%, driven by the rising global prevalence of diabetes and increasing emphasis on long-term glucose monitoring. HbA1c testing provides critical insights into average blood sugar levels over time, making it essential for diabetes diagnosis and management. Growing awareness of early diabetes detection is boosting test adoption across healthcare systems. Expanding screening programs in both developed and emerging economies are further accelerating demand. Technological improvements in point-of-care HbA1c testing devices are enhancing accessibility and turnaround time. Rising healthcare expenditure on chronic disease management is also supporting rapid segment expansion.

- By Technology

On the basis of technology, the Clinical Laboratory Tests Market is segmented into immunoassay-based testing, PCR & molecular diagnostics, next-generation sequencing, automated chemistry analyzers, mass spectrometry, and manual methods. The Immunoassay-based Testing segment dominated the market with a 34.12% share in 2025, driven by its wide application in infectious disease detection, hormone analysis, and routine diagnostic screening. These systems are highly reliable, cost-effective, and widely deployed across hospital and independent laboratories. High throughput capability and standardized workflows make them suitable for large-scale testing environments. Continuous improvements in reagent sensitivity and automation are enhancing diagnostic accuracy. Strong adoption in clinical chemistry and infectious disease panels further supports its dominance. The segment remains a core pillar of modern diagnostic laboratories globally.

The Next-Generation Sequencing (NGS) segment is expected to witness the fastest growth during the forecast period at a CAGR of 12.4%, driven by increasing demand for precision medicine and advanced genetic testing. NGS enables comprehensive genomic analysis, supporting cancer diagnostics, rare disease identification, and personalized treatment planning. Declining sequencing costs and improved bioinformatics capabilities are accelerating adoption across research and clinical settings. Expanding use in oncology companion diagnostics is further boosting growth. Rising investments in genomic medicine infrastructure are strengthening market penetration. Integration of AI-based sequencing analysis is also enhancing scalability and clinical utility.

- By Application

On the basis of application, the Clinical Laboratory Tests Market is segmented into parasitology, hematology, virology, toxicology, immunology/serology, histopathology, and urinalysis. The Hematology segment dominated the market with a 28.63% revenue share in 2025, driven by high utilization of complete blood count (CBC) and related tests for routine diagnostics and disease monitoring. Hematology testing is essential in diagnosing infections, anemia, blood cancers, and chronic disorders. High patient inflow in hospitals and diagnostic labs significantly supports test volumes. Automation in hematology analyzers has improved efficiency and reduced turnaround time. Growing prevalence of blood-related disorders further strengthens demand. The segment remains a core component of routine clinical laboratory workflows worldwide.

The Immunology/Serology segment is projected to grow at the fastest rate during the forecast period at a CAGR of 10.6%, driven by rising incidence of autoimmune diseases and infectious conditions requiring antibody-based detection. Increasing demand for early disease identification and immune profiling is accelerating adoption. Expanding vaccine monitoring and infectious disease surveillance programs are further boosting growth. Advances in high-sensitivity immunoassay platforms are improving diagnostic accuracy. Growing use in allergy and chronic inflammation testing is also supporting expansion. Rising awareness of immune-related disorders is further strengthening market demand.

- By End Users

On the basis of end users, the Clinical Laboratory Tests Market is segmented into hospital-based laboratories, clinic-based laboratories, central/independent laboratories, physician office-based laboratories, and others. The Hospital-Based Laboratories segment dominated the market with a 39.85% share in 2025, driven by high patient volume, emergency care testing, and integrated diagnostic infrastructure. Hospitals perform a wide range of routine and specialized tests, supporting continuous demand. Availability of advanced diagnostic equipment and skilled personnel strengthens their dominance. Increasing hospitalization rates due to chronic diseases further boost testing volumes. Strong integration with electronic health record systems improves workflow efficiency. The segment remains a primary hub for clinical diagnostics globally.

The Central/Independent Laboratories segment is expected to grow at the fastest pace during the forecast period at a CAGR of 8.9%, driven by rising outsourcing of diagnostic services and cost efficiency advantages. These laboratories offer high-throughput testing, faster turnaround times, and specialized diagnostic services. Increasing demand for standardized and scalable testing solutions is supporting adoption. Expansion of large diagnostic chains in emerging markets is further accelerating growth. Technological investments in automation and digital lab platforms are enhancing operational efficiency. Growing preference for consolidated testing services among healthcare providers is also fueling expansion.

Clinical Laboratory Tests Market Regional Analysis

North America dominated the Clinical Laboratory Tests Market with the largest revenue share of 38.62% in 2025, supported by strong healthcare infrastructure, high diagnostic testing volume, and widespread adoption of advanced molecular diagnostics. The region also benefits from widespread insurance coverage, high awareness of preventive healthcare, and the presence of leading diagnostic laboratory networks and hospital systems. Increasing prevalence of chronic diseases such as diabetes, cardiovascular disorders, and cancer continues to drive sustained demand for clinical testing services. Growing integration of AI-enabled diagnostics and expanding use of precision medicine further strengthen North America’s leadership position in the global market.

U.S. Clinical Laboratory Tests Market Insight

The U.S. clinical laboratory tests market is witnessing strong growth due to rising prevalence of chronic diseases, high diagnostic testing volumes, and advanced adoption of automated and molecular diagnostic technologies. The country’s well-established healthcare infrastructure, strong insurance penetration, and presence of major diagnostic laboratory networks are driving demand across hospitals and independent laboratories. In addition, increasing focus on preventive healthcare, precision medicine, and early disease detection is accelerating test utilization. Growing integration of AI-based diagnostics and expanding use of high-throughput testing platforms continue to strengthen the U.S. market leadership in the global clinical laboratory testing industry.

Europe Clinical Laboratory Tests Market Insight

The Europe clinical laboratory tests market remains a major contributor to global revenue, driven by strong public healthcare systems, rising geriatric population, and high demand for routine and specialized diagnostic testing. The widespread use of standardized laboratory protocols and strong regulatory frameworks are supporting consistent service quality across the region. Increasing investments in molecular diagnostics, digital pathology, and automated laboratory systems are further enhancing market growth. Expanding focus on early disease screening and chronic disease management continues to strengthen adoption of advanced clinical testing solutions across Europe.

U.K. Clinical Laboratory Tests Market Insight

The U.K. clinical laboratory tests market is experiencing steady growth, supported by the National Health Service (NHS), rising demand for diagnostic services, and increasing adoption of centralized laboratory testing models. Growing investments in digital health infrastructure and laboratory automation are improving testing efficiency and turnaround times. In addition, rising prevalence of lifestyle-related diseases and strong focus on preventive screening programs are contributing to market expansion. Integration of AI-driven diagnostics and expansion of large-scale laboratory networks are further positioning the U.K. as a key hub for clinical laboratory innovation.

Germany Clinical Laboratory Tests Market Insight

The Germany clinical laboratory tests market is expanding steadily due to a strong healthcare system, advanced diagnostic infrastructure, and increasing focus on precision medicine and laboratory automation. Hospitals and independent laboratories are widely adopting molecular diagnostics and high-throughput testing systems for improved accuracy and efficiency. Rising incidence of chronic diseases and strong emphasis on early disease detection are further driving demand. Continuous advancements in biotechnology and strong government support for healthcare innovation are strengthening Germany’s position in the European clinical diagnostics market.

Asia-Pacific Clinical Laboratory Tests Market Insight

The Asia-Pacific clinical laboratory tests market is expected to witness rapid growth, driven by expanding healthcare access, rising disease burden, and increasing investments in diagnostic infrastructure across countries such as China, India, and Japan. Growing awareness of preventive healthcare and early diagnosis is significantly boosting test adoption across urban and rural populations. In addition, rapid expansion of private diagnostic chains and increasing use of automated laboratory systems are supporting regional growth. Strong government initiatives to improve healthcare accessibility and affordability are further accelerating market expansion in the region.

Japan Clinical Laboratory Tests Market Insight

The Japan clinical laboratory tests market is witnessing consistent growth due to an aging population, high demand for advanced diagnostic services, and strong adoption of automated laboratory technologies. Healthcare providers are increasingly utilizing molecular diagnostics, immunoassays, and genetic testing for early disease detection and chronic disease management. Integration of digital laboratory systems and robotics is improving testing efficiency and accuracy. In addition, Japan’s strong focus on preventive healthcare and precision medicine is further supporting sustained growth in the clinical laboratory testing market.

China Clinical Laboratory Tests Market Insight

The China clinical laboratory tests market is growing rapidly, driven by rising urbanization, expanding healthcare infrastructure, and increasing demand for high-quality diagnostic services. Government initiatives to improve healthcare accessibility and strengthen disease screening programs are significantly boosting test volumes. Growing adoption of automated analyzers, molecular diagnostics, and AI-enabled laboratory systems is further accelerating market development. In addition, rising prevalence of chronic diseases and expanding private diagnostic laboratory networks are positioning China as one of the fastest-growing markets for clinical laboratory tests globally.

Clinical Laboratory Tests Market Share

The clinical laboratory tests industry is primarily led by well-established companies, including:

- Quest Diagnostics Inc. (U.S.)

- Labcorp (U.S.)

- Sonic Healthcare Limited (Australia)

- Eurofins Scientific SE (Luxembourg)

- Charles River Laboratories (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Abbott (U.S.)

- SYNLAB International GmbH (Germany)

- Hoffmann-La Roche Ltd (Switzerland)

- Siemens Healthineers AG (Germany)

- Danaher Corporation (U.S.)

- PerkinElmer Inc. (U.S.)

- Illumina, Inc. (U.S.)

- QIAGEN (Netherlands)

- BD (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Beckman Coulter, Inc. (U.S.)

- Randox Laboratories Ltd (U.K.)

- ARUP Laboratories (U.S.)

Latest Developments in Clinical Laboratory Tests Market

- In October 2023, Cepheid received FDA 510(k) clearance for its Xpert Xpress CoV-2 Plus test, enabling continued high-throughput respiratory disease testing beyond emergency authorization frameworks. This strengthened long-term molecular diagnostic infrastructure in clinical laboratories

- In February 2023, Cepheid received FDA Emergency Use Authorization for its Xpert Mpox test, expanding point-of-care molecular testing for infectious diseases using its GeneXpert platform. The approval improved rapid diagnostic access in decentralized clinical laboratory settings

- In October 2022, Roche announced FDA clearance for its cobas SARS-CoV-2 PCR test on high-throughput systems, improving automated molecular diagnostic capacity for COVID-19 testing in hospital and reference laboratories. The clearance strengthened standardized large-scale infectious disease testing infrastructure globally

- In September 2022, Quest Diagnostics received FDA Emergency Use Authorization (EUA) for its first Monkeypox molecular diagnostic test, enabling rapid PCR-based detection of the Mpox virus in clinical laboratories across the U.S. The test strengthened outbreak response capabilities and expanded high-complexity molecular testing in large reference labs

- In June 2022, Labcorp received FDA Emergency Use Authorization for its VirSeq SARS-CoV-2 Next-Generation Sequencing (NGS) test, enabling identification of COVID-19 variants using advanced genomic sequencing. The development enhanced molecular surveillance capabilities and supported strain-level infectious disease monitoring

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.