Global Cardiovascular Digital Solutions Market

Market Size in USD Billion

USD

113.89 Billion

USD

175.73 Billion

2024

2032

USD

113.89 Billion

USD

175.73 Billion

2024

2032

| 2025 - 2032 | |

| USD 113.89 Billion | |

| USD 175.73 Billion | |

| % | |

|

Cardiovascular Digital Solutions Market Size

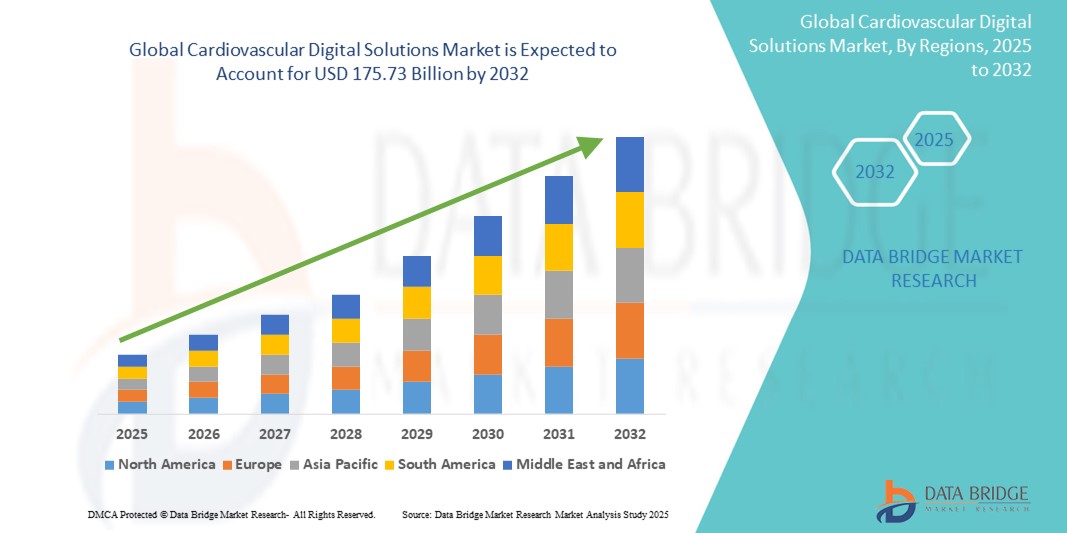

- The global cardiovascular digital solutions market size was valued at USD 113.89 billion in 2024 and is expected to reach USD 175.73 billion by 2032, at a CAGR of 5.57% during the forecast period

- The market growth for cardiovascular digital solutions is largely fueled by the growing adoption and technological progress within digital health platforms and remote patient monitoring technologies, leading to increased digitalization in cardiovascular care settings

- Furthermore, rising demand for proactive disease management, personalized treatment plans, and integrated solutions for cardiac patients is establishing cardiovascular digital solutions as the modern standard of care. These converging factors are accelerating the uptake of Cardiovascular Digital Solutions, thereby significantly boosting the industry's growth

Cardiovascular Digital Solutions Market Analysis

- Cardiovascular digital solutions, encompassing remote monitoring tools, AI-based diagnostics, and mobile health applications, are becoming increasingly essential in modern cardiovascular care due to their ability to improve patient outcomes, enable early detection, and streamline clinical workflows

- The growing adoption of these solutions is primarily driven by the rising prevalence of cardiovascular diseases, the global shift toward value-based care, and advancements in digital health technologies, including wearable devices and AI-powered decision support

- North America dominates the cardiovascular digital solutions market with the largest revenue share of 42.4% in 2024, supported by a robust healthcare infrastructure, early adoption of health tech innovations, and strong presence of leading digital health companies, particularly in the U.S., where remote cardiac monitoring and telehealth services have seen rapid uptake post-COVID

- Asia-Pacific is expected to be the fastest growing region in the cardiovascular digital solutions market during the forecast period, with a CAGR of 23.7%, driven by increasing investments in healthcare digitization, expanding insurance coverage, and a growing middle-class population demanding quality healthcare

- Devices segment dominates the cardiovascular digital solutions market with a market share of 41.7% in 2024, driven by the growing adoption of wearable and remote monitoring technologies such as ECG patches, smartwatches, and connected blood pressure monitors.

Report Scope and Cardiovascular Digital Solutions Market Segmentation

|

Attributes |

Cardiovascular Digital Solutions Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Cardiovascular Digital Solutions Market Trends

“Enhanced Convenience in Cardiovascular Digital Solutions”

- A significant and accelerating trend in the global cardiovascular digital solutions market is the deepening integration with artificial intelligence (AI) and voice-interactive platforms, enabling real-time insights and personalized care management. This convergence of technologies is dramatically improving user engagement, patient monitoring, and physician workflow efficiency

- For instance, AI-enabled platforms such as Eko’s cardiac monitoring solutions are now integrating with digital voice assistants and EHR systems to allow hands-free operation and streamlined data sharing, empowering clinicians to conduct remote auscultation and receive diagnostic insights through voice-guided prompts

- AI integration in cardiovascular digital platforms allows for predictive analytics, automated arrhythmia detection, and intelligent alerts based on real-time biometrics. For instance, companies such as Biofourmis offer AI-powered platforms that learn from patient data trends and can flag early warning signs of cardiac deterioration, while voice-enabled tools guide patients through daily health checks

- The seamless integration of cardiovascular tools with smart health assistants and digital care ecosystems facilitates centralized and intuitive disease management. Patients can now interact with their care plans using simple voice commands, receive medication reminders, and even share health metrics with clinicians via connected health hubs

- The demand for cardiovascular digital tools with AI and voice-enabled capabilities is growing rapidly across both clinical and home care settings, as health systems increasingly prioritize remote patient management, convenience, and early intervention for better cardiac outcomes

Cardiovascular Digital Solutions Market Dynamics

Driver

“Growing Demand Due to Rising Cardiovascular Diseases and Advancements in Remote Monitoring”

- The global increase in cardiovascular diseases (CVDs), coupled with rising healthcare digitization, is a significant driver for the Cardiovascular Digital Solutions market. These solutions provide real-time monitoring, data-driven diagnostics, and personalized patient management, which are crucial in managing chronic cardiac conditions effectively

- For instance, in February 2024, Philips expanded its remote cardiac monitoring capabilities through the integration of AI-powered analytics into its wearable devices, enabling early detection of cardiac anomalies and proactive care management. Such advancements are fostering wider adoption of digital cardiovascular tools across healthcare systems

- Patients and providers are increasingly shifting toward remote monitoring technologies to reduce hospital readmissions, enhance patient engagement, and lower long-term healthcare costs

- The growth in wearable technology—such as ECG-enabled smartwatches, connected blood pressure monitors, and AI-powered cardiac patches—has made real-time cardiovascular data accessible to both patients and clinicians. This accessibility is enhancing decision-making, treatment personalization, and overall outcomes

- Furthermore, the integration of these tools into telehealth platforms and electronic health records (EHRs) ensures seamless communication and data flow, improving the quality of cardiovascular care delivery

Restraint/Challenge

“Data Privacy Concerns and High Implementation Costs”

- Despite its benefits, the cardiovascular digital solutions market faces significant challenges, particularly around patient data security and the high cost of advanced digital infrastructure

- As these systems generate and transmit sensitive health information over connected networks, they are vulnerable to data breaches, cyberattacks, and unauthorized access—raising compliance issues under regulations such as HIPAA and GDPR

High-profile incidents involving healthcare data breaches have eroded trust among patients and slowed adoption, especially in regions lacking stringent cybersecurity frameworks. Ensuring end-to-end encryption, secure data storage, and regular system updates is critical to mitigating these risks - In addition, the initial investment required to implement comprehensive cardiovascular digital platforms—including devices, software, training, and system integration—can be prohibitive, especially for smaller healthcare providers or facilities in developing regions

- While cloud-based and scalable solutions are emerging to reduce infrastructure burdens, financial constraints remain a key barrier. Bridging this gap through public-private partnerships, government incentives, and cost-effective technological innovations will be essential to expanding access to cardiovascular digital care globally

Cardiovascular Digital Solutions Market Scope

The market is segmented on the basis of service type, component, deployment type, and end-users.

• By Service Type

On the basis of service type, the cardiovascular digital solutions market is segmented into unobtrusive testing, CVD health informatics, and cardiac rehab programs. The unobtrusive testing segment held the largest market revenue share of 39.4% in 2024, driven by the increased adoption of wearable and remote monitoring technologies that allow continuous cardiovascular assessment without disrupting patients' daily routines. This segment is expected to further expand with advancements in sensor technology and growing preference for non-invasive monitoring solutions.

The cardiac rehab programs segment is expected to witness the fastest CAGR of 21.2% from 2025 to 2032, owing to the rising need for post-treatment care and remote rehabilitation support. Increased awareness about secondary prevention and the integration of digital platforms for guided exercise and recovery plans are contributing to the strong growth of this segment.

• By Component

On the basis of component, the cardiovascular digital solutions market is segmented into devices and software. The devices segment held the largest market share of 41.7% in 2024, propelled by the widespread use of ECG monitors, smartwatches, and portable diagnostic tools. These devices provide real-time data collection and analysis, essential for early detection and ongoing disease management.

The software segment is projected to grow at the fastest CAGR of 20.5% from 2025 to 2032, driven by increasing deployment of AI-powered analytics and predictive modeling tools. The demand for interoperable platforms that integrate patient records and deliver actionable insights is accelerating growth in this segment.

• By Deployment Type

On the basis of deployment type, the cardiovascular digital solutions market is segmented into cloud-based/web-based and on-premise solutions. The cloud-based/web-based segment held the largest revenue share of 56.3% in 2024, owing to its scalability, ease of remote access, and integration with mobile health applications. Healthcare providers are increasingly favoring cloud platforms for their lower upfront costs and enhanced data sharing capabilities.

The on-premise segment, while currently smaller, is expected to see steady growth with a CAGR of 16.7%, driven by institutions requiring high security, regulatory compliance, and control over patient data.

• By End-Users

On the basis of end-users, the cardiovascular digital solutions market is segmented into homecare settings, ambulatory care centers, hospitals, and clinics. The hospitals segment held the highest revenue share of 38.9% in 2024, supported by the comprehensive adoption of advanced cardiovascular diagnostics and monitoring systems for inpatient care. The presence of structured care pathways and high patient throughput makes hospitals a major user base.

The homecare settings segment is projected to witness the fastest growth at a CAGR of 23.1% from 2025 to 2032, driven by the increasing trend toward remote patient monitoring, aging populations, and the convenience of managing chronic conditions from home. Consumer demand for personalized, tech-enabled care is a major catalyst in this segment.

Cardiovascular Digital Solutions Market Regional Analysis

- North America dominates the cardiovascular digital solutions market with the largest revenue share of 42.4% in 2024, driven by early adoption of digital health technologies, strong healthcare infrastructure, and the growing prevalence of cardiovascular diseases

- Consumers and healthcare providers in the region prioritize real-time monitoring, AI-powered diagnostics, and seamless data integration, making digital cardiovascular solutions essential for preventive care and chronic disease management

- This leadership is further supported by favorable reimbursement policies, high digital literacy, and robust investments from public and private stakeholders, solidifying North America’s position as a key driver in the global adoption of cardiovascular digital health solutions

U.S. Cardiovascular Digital Solutions Market Insight

In 2024, the U.S. cardiovascular digital solutions market dominated the market from 2025 to 2032. This growth is driven by the increasing prevalence of cardiovascular diseases and the adoption of advanced digital health technologies. The integration of wearable devices, remote patient monitoring systems, and AI-driven diagnostics is enhancing patient care and enabling proactive health management

Europe Cardiovascular Digital Solutions Market Insight

The Europe cardiovascular digital solutions market is experiencing steady growth, with a focus on enhancing patient outcomes and optimizing healthcare delivery. The market is supported by stringent healthcare regulations and the increasing adoption of digital health solutions across the region. Countries such as Germany and the U.K. are investing in telemedicine platforms, electronic health records, and AI-based diagnostic tools to improve cardiovascular care.

U.K. Cardiovascular Digital Solutions Market Insight

The U.K. cardiovascular digital solutions market is expanding due to the National Health Service's (NHS) initiatives to digitize healthcare services. The adoption of remote monitoring devices and telehealth platforms is facilitating better management of cardiovascular conditions, especially in remote and underserved areas. The emphasis on preventive care and patient engagement is further propelling market growth.

Germany Cardiovascular Digital Solutions Market Insight

The Germany cardiovascular digital solutions market is characterized by a strong emphasis on technological innovation and data security. The integration of digital health applications, such as mobile health apps and connected medical devices, is improving the diagnosis and treatment of cardiovascular diseases. Government support for digital health initiatives and a robust healthcare infrastructure are key factors contributing to market expansion

Asia-Pacific Cardiovascular Digital Solutions Market Insight

The Asia-Pacific cardiovascular digital solutions market is expected to grow with the highest CAGR of 23.7% during the forecast period. This rapid growth is attributed to increasing urbanization, rising disposable incomes, and technological advancements in countries like China, Japan, and India. Government initiatives promoting digitalization and smart healthcare solutions are also driving market development

Japan Cardiovascular Digital Solutions Market Insight

The Japan's cardiovascular digital solutions market is advancing due to its high-tech infrastructure and aging population. The adoption of wearable health devices, telemedicine services, and AI-powered diagnostic tools is enhancing cardiovascular care. The focus on personalized medicine and preventive healthcare is encouraging the integration of digital solutions in both clinical and home settings

China Cardiovascular Digital Solutions Market Insight

The China’s cardiovascular digital solutions market accounted for the largest market revenue share in Asia Pacific in 2024, driven by a growing middle class, rapid urbanization, and high technological adoption rates. The government's push towards smart healthcare and the availability of affordable digital health solutions from domestic manufacturers are propelling market growth. The integration of AI and big data analytics is further enhancing the efficiency of cardiovascular care

India Cardiovascular Digital Solutions Market Insight

The India’s cardiovascular digital solutions market is rapidly expanding with a projected CAGR exceeding 22% from 2025 to 2032. The growth is fueled by increasing urbanization, rising disposable incomes, and a growing awareness of digital health technologies. Government initiatives promoting digital infrastructure and smart healthcare, along with a burgeoning e-commerce ecosystem, are enhancing access to advanced cardiovascular digital solutions across the country

Cardiovascular Digital Solutions Market Share

The cardiovascular digital solutions industry is primarily led by well-established companies, including:

- iRhythm Inc. (U.S.)

- Apple Inc. (U.S.)

- GE HealthCare (U.S.)

- Baxter (U.S.)

- Cardiotrack (India)

- AliveCor, Inc. (U.S.)

- Verily (U.S.)

- HeartFlow, Inc. (U.S.)

- Bardy Diagnostics, Inc. (U.S.)

- Nanowear Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Cardiac Insight, Inc. (U.S.)

- EviCore healthcare (U.S.)

- Wainscot Media (U.S.)

- Optum Inc. (U.S.)

- Medtronic (Ireland)

Latest Developments in Global Cardiovascular Digital Solutions Market

- In April 2024, Medtronic plc, a global leader in medical technology, announced the launch of its next-generation cardiovascular digital monitoring system designed to enhance remote patient care. This advanced system integrates AI-powered analytics with wearable devices to provide continuous, real-time cardiac health monitoring, aiming to improve early detection and personalized treatment of cardiovascular diseases. This launch reflects Medtronic’s commitment to innovation and expanding its footprint in the growing cardiovascular digital solutions market

- In March 2024, Philips Healthcare unveiled its new cloud-based cardiovascular data management platform, enabling seamless integration of patient data from multiple sources for improved clinical decision-making. The platform supports telehealth services and remote monitoring, addressing the increasing demand for digital healthcare solutions driven by the rise in cardiovascular disease prevalence globally. Philips’ initiative highlights the strategic focus on digital transformation in cardiovascular care.

- In February 2024, Abbott Laboratories introduced its updated wearable cardiac monitor with enhanced battery life and AI-driven diagnostic capabilities. The device is designed to support both in-clinic and at-home patient monitoring, facilitating early intervention and reducing hospital readmissions. Abbott’s innovation underscores the growing importance of patient-centric digital solutions in cardiovascular health management

- In January 2024, GE Healthcare partnered with a leading cloud service provider to develop scalable, secure cloud infrastructure for cardiovascular digital data storage and analytics. This collaboration aims to accelerate data-driven research and improve clinical workflows in cardiology departments worldwide. GE Healthcare’s move signals increasing investments in cloud computing to support the expanding digital health ecosystem

- In January 2024, Boston Scientific launched its integrated cardiovascular remote monitoring service, combining implantable devices with digital health platforms to enhance post-procedure patient care. This development highlights the company’s dedication to advancing connected care solutions and improving patient outcomes through innovative cardiovascular digital technologies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.