Global Cardiac Rhythm Management Market

Market Size in USD Billion

CAGR :

%

USD

24.10 Billion

USD

44.60 Billion

2024

2032

USD

24.10 Billion

USD

44.60 Billion

2024

2032

| 2025 –2032 | |

| USD 24.10 Billion | |

| USD 44.60 Billion | |

| % | |

|

Cardiac Rhythm Management Market Size

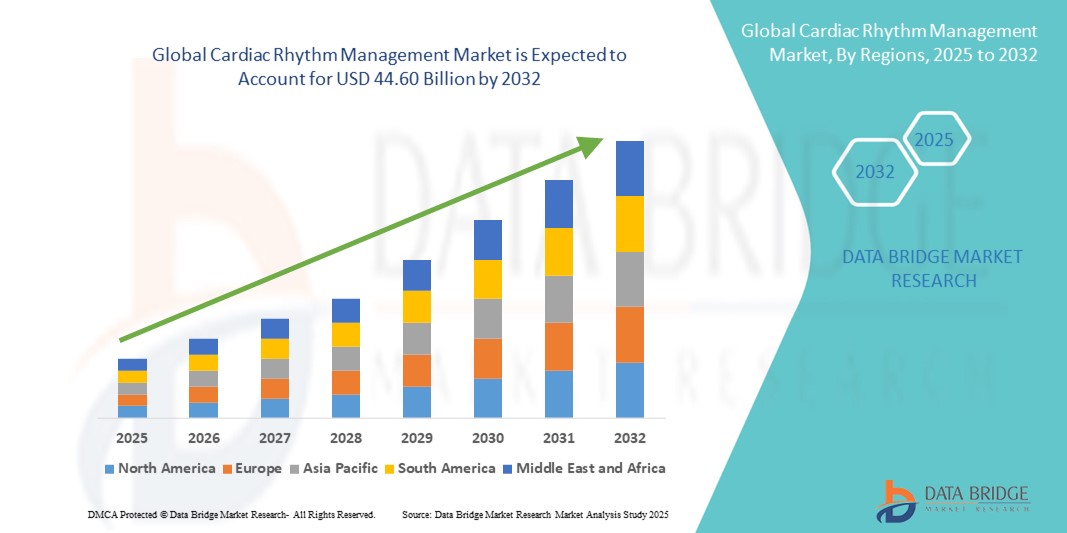

- The global cardiac rhythm management market size was valued at USD 24.10 billion in 2024 and is expected to reach USD 44.60 billion by 2032, at a CAGR of 8.00% during the forecast period

- The market growth is primarily driven by increasing prevalence of cardiac arrhythmias, advancements in implantable cardiac devices, and rising awareness about cardiovascular health across both developed and emerging economies

- In addition, ongoing innovations in device miniaturization, remote monitoring technologies, and integration with digital health platforms are enhancing patient outcomes and convenience, which is further boosting the adoption of cardiac rhythm management solutions globally. These combined factors are propelling steady market expansion in the foreseeable future

Cardiac Rhythm Management Market Analysis

- Cardiac rhythm management devices, including pacemakers, implantable cardioverter defibrillators (ICDs), and cardiac resynchronization therapy (CRT) devices, play a crucial role in diagnosing and treating arrhythmias, improving patient survival and quality of life in both acute and chronic cardiovascular conditions

- The rising prevalence of cardiovascular diseases, increasing geriatric population, and advancements in device technology such as leadless pacemakers and MRI-safe implants are key drivers accelerating the demand for cardiac rhythm management solutions worldwide

- North America dominated the cardiac rhythm management market with the largest revenue share of 39% in 2024, driven by high healthcare expenditure, strong presence of major device manufacturers, and widespread adoption of advanced cardiac monitoring and implantable devices, particularly in the U.S. healthcare system

- Asia-Pacific is anticipated to be the fastest-growing region in the cardiac rhythm management market during the forecast period, fueled by improving healthcare infrastructure, growing awareness about cardiac health, and expanding patient access to advanced therapies in countries such as China and India

- The pacemaker segment dominated the cardiac rhythm management market with a share of 46.1% in 2024, supported by technological innovations improving battery life, device miniaturization, and enhanced functionalities such as remote monitoring capabilities

Report Scope and Cardiac Rhythm Management Market Segmentation

|

Attributes |

Cardiac Rhythm Management Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Cardiac Rhythm Management Market Trends

Advancements in Device Miniaturization and Remote Monitoring

- A prominent trend in the global cardiac rhythm management market is the ongoing innovation in device miniaturization, enabling smaller, less invasive implantable devices that improve patient comfort and reduce procedural risks

- For instance, leadless pacemakers such as Medtronic’s Micra offer minimally invasive implantation without the need for leads, significantly enhancing patient compliance and reducing complications. Similarly, advancements in battery technology extend device longevity, reducing replacement frequency

- Remote monitoring capabilities are becoming increasingly integrated into cardiac rhythm devices, allowing healthcare providers to track patient cardiac data in real time, detect arrhythmias early, and adjust therapies proactively. Abbott’s CardioMEMS system exemplifies such innovations by facilitating wireless hemodynamic monitoring to prevent heart failure hospitalizations

- The integration of AI and machine learning in rhythm management devices aids in improved diagnostics and personalized therapy adjustments by analyzing large volumes of patient data, leading to better clinical outcomes

- This shift toward more compact, connected, and intelligent cardiac rhythm devices is reshaping clinical practices and patient management, with companies such as Boston Scientific and Biotronik heavily investing in AI-enabled remote monitoring solutions

- Demand for smart, minimally invasive, and digitally connected cardiac rhythm management devices is accelerating globally, driven by patient preference for less intrusive treatments and healthcare systems’ focus on reducing hospitalization costs

Cardiac Rhythm Management Market Dynamics

Driver

Increasing Prevalence of Cardiovascular Diseases and Aging Population

- The growing burden of cardiovascular diseases worldwide, especially arrhythmias, coupled with the rapidly aging global population, is a primary driver boosting demand for cardiac rhythm management devices

- For instance, in March 2024, Boston Scientific announced FDA approval for its next-generation implantable defibrillator with enhanced battery life and remote monitoring capabilities, reflecting the ongoing innovation responding to rising clinical needs

- Increased awareness among patients and healthcare providers about the benefits of early diagnosis and treatment of cardiac rhythm disorders is also driving market expansion

- Moreover, improved healthcare infrastructure and reimbursement policies in developed and emerging markets facilitate greater access to advanced implantable cardiac devices

- The demand for solutions that improve quality of life, reduce hospital readmissions, and enable remote patient management is fueling rapid adoption of pacemakers, ICDs, and CRT devices across diverse geographies

Restraint/Challenge

High Device Costs and Regulatory Complexities

- The relatively high cost of implantable cardiac rhythm management devices and associated procedures remains a significant barrier to adoption, particularly in low- and middle-income countries

- For instance, the upfront cost and need for specialized implantation skills can limit patient access in regions with constrained healthcare budgets

- In addition, stringent regulatory requirements for device approvals and post-market surveillance add complexity and delay to product launches, impacting market growth

- Cybersecurity risks related to wireless connectivity of implantable devices raise concerns regarding patient safety and data privacy, necessitating robust security protocols from manufacturers

- Addressing these challenges through cost-reduction strategies, streamlined regulatory pathways, and enhanced cybersecurity measures will be crucial to sustaining market growth and broadening patient access to cardiac rhythm management therapies

Cardiac Rhythm Management Market Scope

The market is segmented on the basis of product type and end user.

- By Product Type

On the basis of product type, the cardiac rhythm management market is segmented into defibrillators, pacemakers, and cardiac resynchronization therapy (CRT) devices. The pacemaker segment dominated the market with the largest revenue share of 46.1% in 2024, driven by its widespread use in managing bradycardia and advancements such as leadless pacemakers that enhance patient comfort and reduce implantation risks. Pacemakers are favored due to their proven efficacy, expanding indications, and continuous technological improvements including extended battery life and remote monitoring capabilities.

The defibrillators segment is expected to witness robust growth over the forecast period, propelled by rising incidences of sudden cardiac arrest and technological innovations such as subcutaneous implantable cardioverter defibrillators (S-ICDs) that offer less invasive options with fewer complications. Increasing awareness and screening programs also contribute to growing demand for defibrillators in both hospital and ambulatory settings.

- By End User

On the basis of end user, the cardiac rhythm management market is segmented into hospitals, ambulatory care centers, home care, and others. Hospitals dominated the market in 2024, accounting for the largest revenue share due to the requirement for complex implantation procedures, device programming, and post-operative monitoring performed by specialized cardiology units. The availability of advanced facilities and expert healthcare professionals in hospitals supports the preference for device implantation and follow-up care within these settings.

The home care segment is projected to witness the fastest growth rate during the forecast period, driven by increasing adoption of remote patient monitoring technologies that enable continuous cardiac device surveillance outside clinical settings. Growing patient preference for home-based management, supported by advances in telehealth and mobile health applications, is making home care an increasingly viable and cost-effective option for long-term rhythm management.

Cardiac Rhythm Management Market Regional Analysis

- North America dominated the cardiac rhythm management market with the largest revenue share of 39% in 2024, driven by high healthcare expenditure, strong presence of major device manufacturers, and widespread adoption of advanced cardiac monitoring and implantable devices, particularly in the U.S. healthcare system

- Patients and healthcare providers in the region benefit from early access to innovative implantable devices and remote monitoring technologies, supported by robust reimbursement frameworks and significant healthcare expenditure.

- The U.S., as the largest market within North America, experiences strong demand due to an aging population and widespread awareness of arrhythmia management, positioning cardiac rhythm devices as essential components of cardiovascular care in hospitals and outpatient settings

U.S. Cardiac Rhythm Management Market Insight

The U.S. cardiac rhythm management market captured the largest revenue share of 42% in 2024 within North America, driven by a high prevalence of cardiac arrhythmias and robust healthcare infrastructure. The widespread availability of advanced implantable devices, such as leadless pacemakers and subcutaneous defibrillators, supports strong market demand. In addition, increasing patient awareness, favorable reimbursement policies, and technological innovations in remote monitoring and AI-enabled diagnostics further fuel growth. The U.S. remains a key hub for research and development, accelerating adoption of next-generation cardiac rhythm solutions.

Europe Cardiac Rhythm Management Market Insight

The Europe cardiac rhythm management market is projected to grow steadily at a notable CAGR during the forecast period, supported by an aging population and rising incidence of cardiovascular diseases. Stringent regulatory standards and well-established healthcare systems facilitate adoption of advanced implantable devices. Countries such as Germany, France, and the U.K. are witnessing increased demand across hospitals and ambulatory care settings, driven by advancements in device miniaturization and remote patient monitoring. Enhanced awareness programs and government initiatives aimed at cardiovascular health are also contributing to market expansion.

U.K. Cardiac Rhythm Management Market Insight

The U.K. cardiac rhythm management market is expected to experience steady growth, fueled by increasing investments in healthcare infrastructure and a growing elderly population prone to arrhythmias. The NHS’s focus on improving cardiac care pathways and integrating remote monitoring technologies supports rising device utilization. Furthermore, the country’s strong presence of medical device manufacturers and collaborative clinical research enhance accessibility to innovative rhythm management therapies. Growing patient preference for minimally invasive and home-based cardiac care solutions also drives market growth.

Germany Cardiac Rhythm Management Market Insight

The Germany cardiac rhythm management market is anticipated to expand significantly, supported by a high incidence of heart failure and arrhythmias. Germany’s advanced healthcare infrastructure, coupled with strong government support for digital health integration, promotes adoption of sophisticated cardiac rhythm devices, including CRT and ICDs. The country’s emphasis on innovation and clinical trials accelerates availability of next-gen implantable devices. In addition, increasing demand for personalized cardiac therapies and home monitoring solutions aligns with local healthcare strategies, fostering market growth.

Asia-Pacific Cardiac Rhythm Management Market Insight

The Asia-Pacific cardiac rhythm management market is poised for the fastest growth at a CAGR of 22% during 2025–2032, driven by rising cardiovascular disease burden, improving healthcare access, and increasing awareness. Rapid urbanization, expanding healthcare infrastructure, and growing geriatric populations in China, India, Japan, and Southeast Asia are major growth factors. Government initiatives focused on chronic disease management and increasing adoption of telehealth and remote monitoring technologies accelerate market penetration. Furthermore, the region benefits from cost-effective manufacturing and expanding distribution networks.

Japan Cardiac Rhythm Management Market Insight

The Japan cardiac rhythm management market is growing steadily due to the country’s aging population and advanced medical technology adoption. Japan places strong emphasis on preventive cardiac care and innovation, supporting widespread use of implantable devices equipped with remote monitoring capabilities. Integration of AI and machine learning in cardiac diagnostics and therapy optimization is gaining traction. In addition, the government’s healthcare policies promoting digital health and home care solutions are expected to enhance market growth across residential and clinical settings.

India Cardiac Rhythm Management Market Insight

The India cardiac rhythm management market accounted for the largest revenue share in South Asia in 2024, propelled by increasing prevalence of cardiovascular diseases and expanding healthcare infrastructure. Rising awareness about arrhythmia management, improving affordability of devices, and growing patient access to advanced therapies contribute to market growth. Government initiatives such as Ayushman Bharat to improve healthcare coverage and increasing private sector participation are key drivers. The expanding middle class and rising demand for minimally invasive cardiac interventions are further accelerating adoption in both urban and semi-urban regions.

Cardiac Rhythm Management Market Share

The Cardiac Rhythm Management industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- BIOTRONIK SE & Co. KG (Germany)

- Johnson & Johnson and its affiliates (U.S.)

- MicroPort Scientific Corporation (China)

- LivaNova PLC (U.K.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthineers AG (Germany)

- Lepu Medical Technology Co., Ltd. (China)

- Shanghai MicroPort Medical (China)

- Zoll Medical Corporation (U.S.)

- CathRx Limited (U.K.)

- Oscor, Inc. (U.S.)

- Cardiac Science Corporation (U.S.)

- EBR Systems, Inc. (U.S.)

- Nevro Corp. (U.S.)

- Proteus Digital Health, Inc. (U.S.)

- Medicover Cardiac Rhythm Management (India)

- Synapse Biomedical, Inc. (U.S.)

What are the Recent Developments in Global Cardiac Rhythm Management Market?

- In February 2025, the FDA approved an adaptive brain pacemaker developed by Medtronic for treating Parkinson's disease symptoms. This device represents the largest commercial deployment of brain-computer interface technology, adjusting treatment based on the patient's immediate needs

- In May 2024, Royal Philips, a global leader in health technology, is presenting new retrospective study results demonstrating the clinical and economic benefits of Philips’ AI-powered cardiac care solutions at the Heart Rhythm Annual Meeting in Boston

- In April 2024, BIOTRONIK introduced the BIOMONITOR IV insertable cardiac monitor featuring an AI-powered SmartECG algorithm. This advancement aims to reduce false positive atrial fibrillation detections, improving diagnostic accuracy and patient care

- In January 2024, Medtronic received the CE Mark for its next-generation Micra AV2 and Micra VR2 leadless pacemakers. These devices offer 40% more battery life compared to previous models, enhancing the longevity and reliability of pacemaker therapy

- In September 2023, Abbott announced the FDA approval of the world's first dual-chamber leadless pacemaker system. This innovative device enables wireless communication between two leadless pacemakers, offering a minimally invasive solution for patients requiring dual-chamber pacing

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.