Global Carbon Fiber Market

Market Size in USD Billion

USD

5.39 Billion

USD

11.06 Billion

2024

2032

USD

5.39 Billion

USD

11.06 Billion

2024

2032

| 2025 - 2032 | |

| USD 5.39 Billion | |

| USD 11.06 Billion | |

| % | |

|

Carbon Fiber Market Size

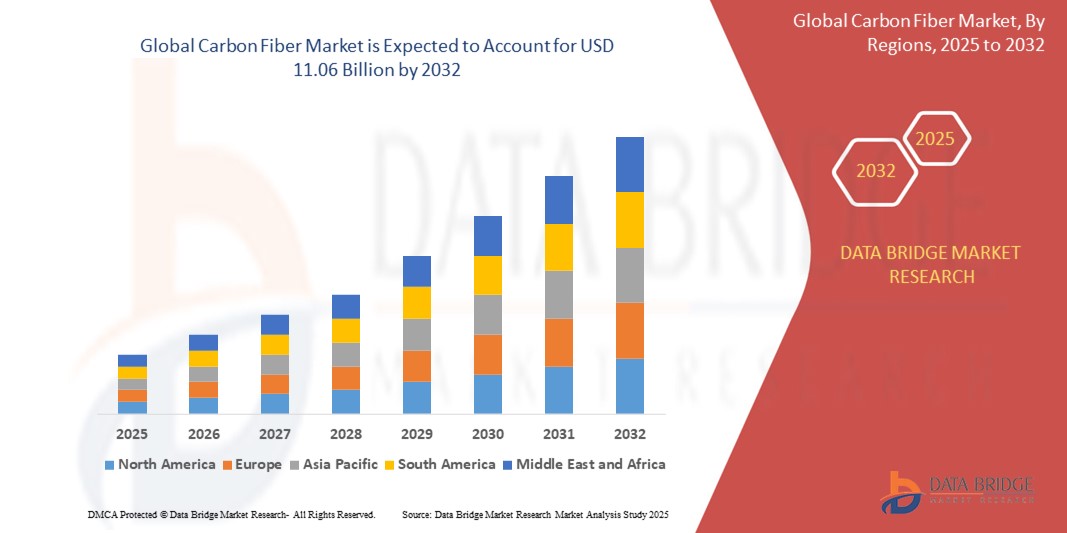

- The global carbon fiber market size was valued at USD 5.39 billion in 2024 and is expected to reach USD 11.06 billion by 2032, at a CAGR of 9.40% during the forecast period

- This growth is driven by factors such as rising demand from aerospace and automotive industries, increasing need for lightweight and high-strength materials, and ongoing advancements in carbon fiber manufacturing technologies

Carbon Fiber Market Analysis

- Carbon fiber is a high-strength, lightweight material widely used across industries such as aerospace, automotive, wind energy, and construction due to its excellent mechanical properties and corrosion resistance

- The demand for carbon fiber is significantly driven by the growing emphasis on fuel efficiency and emission reduction in the transportation sector, along with the increasing use of carbon composites in aircraft and high-performance vehicles

- Europe is expected to dominate the carbon fiber market with largest market share of 32.4%, due to significant revenue growth and market share. This dominance is attributed to the region's strong presence of major aircraft manufacturers and the increasing use of carbon fibers in electric vehicles

- North America is expected to be the fastest growing region in the carbon fiber market during the forecast period due to the expansion of various end-user industries in countries like China and India. As these nations continue to progress, North America stands to benefit significantly from increased demand for carbon fiber applications across multiple sectors

- Small tow segment is expected to dominate the market with a largest market share of 78.4% due to adoption in the automotive industry, particularly in luxury and high-performance vehicles where weight reduction and mechanical strength are paramount, is driving the market growth. Small tow carbon fiber is preferred in manufacturing body panels, roof structures, and other parts that benefit from its precise structural properties, ultimately enhancing vehicle speed, fuel economy, and stability

Report Scope and Carbon Fiber Market Segmentation

|

Attributes |

Carbon Fiber Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Carbon Fiber Market Trends

“Shift Toward Lightweight, High-Performance Materials Across Industries”

- One prominent trend in the global carbon fiber market is the growing shift toward lightweight and high-performance materials across key industries such as aerospace, automotive, and renewable energy

- Carbon fiber’s exceptional strength-to-weight ratio is becoming increasingly critical for improving fuel efficiency, reducing emissions, and enhancing structural performance in modern engineering applications

- For instance, in the aerospace industry, manufacturers are replacing traditional metals with carbon fiber composites in aircraft fuselages and interiors to achieve significant weight reductions and operational cost savings

- This trend is accelerating innovation in carbon fiber production processes and composite technologies, driving broader adoption and expanding its use in both existing and emerging applications

Carbon Fiber Market Dynamics

Driver

“Increasing Adoption in Renewable Energy Applications”

- The growing global focus on renewable energy sources, particularly wind power, is significantly driving the demand for carbon fiber

- Carbon fiber is widely used in manufacturing wind turbine blades due to its high strength, lightweight nature, and fatigue resistance, which are essential for improving turbine efficiency and lifespan

- As countries invest heavily in clean energy to meet sustainability goals and reduce dependence on fossil fuels, the deployment of larger and more efficient wind turbines is accelerating the use of advanced composite materials like carbon fiber

For instance,

- The shift toward offshore wind farms, which require longer and stronger blades, is pushing manufacturers to adopt carbon fiber for optimal performance under extreme conditions

- This rising demand in the renewable energy sector is a key growth driver for the carbon fiber market, aligning with global environmental and energy transition targets

Opportunity

“Innovation in Carbon Fiber Recycling and Sustainable Manufacturing”

- As environmental sustainability becomes a top priority across industries, there is a growing opportunity in the development of cost-effective carbon fiber recycling and eco-friendly manufacturing processes

- Traditional carbon fiber production is energy-intensive and costly; thus, innovations in recycling technologies can help lower production costs and reduce environmental impact, making carbon fiber more accessible for wider applications

- Recycled carbon fiber retains many of the material’s desirable properties and can be used in sectors such as automotive, construction, and consumer goods, where ultra-high performance is not always required

For instance,

- Companies are investing in closed-loop recycling systems and pyrolysis methods to recover carbon fibers from composite waste, reducing landfill use and supporting circular economy initiatives

- This shift toward sustainable carbon fiber solutions opens new market segments and aligns with global regulatory trends, creating long-term growth potential for manufacturers and suppliers

Restraint/Challenge

“High Production Costs and Limited Scalability”

- The high cost of carbon fiber production remains a significant challenge, restricting its widespread adoption across cost-sensitive industries such as automotive and construction

- Producing carbon fiber involves complex and energy-intensive processes, including the stabilization, carbonization, and surface treatment of precursor materials like polyacrylonitrile (PAN), contributing to high material and operational expenses

- These high costs can deter manufacturers from incorporating carbon fiber into mainstream products, especially in regions or sectors with tighter budget constraints

For instance,

- According to industry reports, the cost of carbon fiber can be more than 10 times that of traditional materials like steel or aluminum, which makes mass-market applications economically unviable for many companies

- As a result, this pricing barrier limits carbon fiber’s scalability, especially in emerging markets, and poses a challenge to achieving cost competitiveness in high-volume manufacturing sectors

Carbon Fiber Market Scope

The market is segmented on the basis of type, fiber type, application, raw material, modulus, end user, and tow size

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Fiber Type |

|

|

By Application |

|

|

By Raw Material |

|

|

By Modulus |

|

|

By End User |

|

|

By Tow Size |

|

In 2025, the small tow is projected to dominate the market with a largest share in tow size segment

The small tow segment is expected to dominate the carbon fiber market with the largest share of 78.4% due to adoption in the automotive industry, particularly in luxury and high-performance vehicles where weight reduction and mechanical strength are paramount, is driving the market growth. Small tow carbon fiber is preferred in manufacturing body panels, roof structures, and other parts that benefit from its precise structural properties, ultimately enhancing vehicle speed, fuel economy, and stability

The aerospace & defense is expected to account for the largest share during the forecast period in end user segment

In 2025, the aerospace & defense segment is expected to dominate the market with the largest market share of 32.7% due to the increased investment in next-generation aircraft and space exploration is driving the demand for carbon fiber in aerospace. As the industry develops advanced aircraft, satellites, and spacecraft, carbon fiber’s properties become essential for achieving the structural integrity and lightness required for long-term missions and extreme environmental conditions. The rise of commercial space ventures, as well as government-led space missions, further strengthens the demand for carbon fiber.

Carbon Fiber Market Regional Analysis

“Europe Holds the Largest Share in the Carbon Fiber Market”

- Europe dominates the global carbon fiber market with largest market share of 32.4%, driven by the strong presence of aerospace and automotive manufacturing hubs, coupled with stringent environmental regulations promoting the use of lightweight materials

- Germany holds a largest market share of 35.4%, due to country's robust automotive and aerospace industries, with companies like BMW and Airbus driving demand for lightweight materials. Carbon fiber's role in reducing vehicle weight by up to 30% aligns with EU emission reduction targets, further boosting adoption in electric vehicles (EVs)

- The region also benefits from collaborations between governments, research institutions, and key market players to develop sustainable and cost-effective carbon fiber solutions for diverse industrial applications

- In addition, Europe's aggressive climate goals and support for electric vehicle (EV) production and renewable energy projects, particularly wind power, are further fueling the demand for carbon fiber composites

“North America is Projected to Register the Highest CAGR in the Carbon Fiber Market”

- North America is expected to experience the highest growth rate during the forecast period, driven by increasing demand from the aerospace, defense, and automotive sectors

- The U.S. remains a major contributor to market growth due to its leadership in aerospace innovation, defense spending, and rising adoption of carbon fiber in electric vehicles and infrastructure projects

- Robust R&D activities, government initiatives supporting lightweight and sustainable materials, and the presence of leading carbon fiber manufacturers contribute to the region’s rapid market expansion

- Moreover, increasing investments in wind energy and next-generation transportation technologies continue to strengthen the carbon fiber market outlook in North America

Carbon Fiber Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Evonik Industries (Germany)

- TEIJIN LIMITED (Japan)

- SGL Carbon (Germany)

- dsm-firmenich (Netherlands)

- SABIC (Saudi Arabia)

- Hexcel Corporation (U.S.)

- TORAY INDUSTRIES, INC. (Japan)

- 3M (U.S.)

- BASF (Germany)

- Covestro AG (Germany)

- Dow (U.S.)

- Zoltek Corporation / Toray Group (U.S.)

- Celanese Corporation (U.S.)

- Formosa Plastics Corporation, U.S.A. (Taiwan)

- Nippon Graphite Fiber Co., Ltd. (Japan)

- HS HYOSUNG ADVANCED MATERIALS (South Korea)

Latest Developments in Global Carbon Fiber Market

- In December 2022, Solvay entered into a strategic partnership with Trillium to develop bio-based acrylonitrile for the production of carbon fiber. This collaboration focuses on creating sustainable materials for use in key industries such as automotive, aerospace, consumer goods, and energy. This initiative aligns with the global carbon fiber market's growing emphasis on reducing the environmental footprint of composite materials, responding to increasing demand for sustainable and high-performance materials across various sectors

- In September 2022, Solvay launched LTM 350, an advanced epoxy prepreg carbon fiber tooling material designed to deliver significant cost and time efficiencies across industries such as aerospace, automotive, industrial applications, and motorsports. LTM 350’s introduction reflects the global carbon fiber market’s ongoing trend towards more efficient, cost-effective solutions, aligning with the growing need for high-performance materials that meet the demands of a variety of industries while maintaining competitive pricing and sustainability

- In 2022, Hexcel signed a contract with Dassault Aviation to supply carbon fiber prepreg for the Falcon 10X program, marking Dassault's inaugural use of advanced carbon fiber composites in the production of business jet wings. The partnership underscores the growing trend within the global carbon fiber market, where the aerospace industry is increasingly adopting lightweight, high-strength composites to meet the demand for more fuel-efficient and high-performance aircraft

- In July 2021, Toray Industries Inc. completed the acquisition of TenCate Advanced Composites Holding BV, a leading Dutch manufacturer and distributor of carbon fiber composite materials, in a deal valued at €930 million (approximately USD 1 billion), inclusive of net debt. The acquisition, finalized with TenCate's parent company, Koninklijke Ten Cate BV, significantly strengthens Toray's product portfolio This strategic move enhances Toray's position in the global carbon fiber market, enabling the company to meet the increasing demand for advanced, lightweight composite materials across industries such as aerospace, automotive, and industrial applications

- In February 2021, Teijin Limited launched its Tenax BM (Beam Series) and Tenax PW (Power Series) brands of carbon fiber intermediate materials, specifically engineered for sports applications. These innovative materials are designed to optimize performance by maximizing power and speed, owing to their exceptional durability and toughness. This product launch aligns with the broader trends in the global carbon fiber market, where the demand for lightweight, high-strength materials continues to grow across diverse sectors, including sports, automotive, and aerospace, driven by the need for enhanced performance and efficiency

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Carbon Fiber Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Carbon Fiber Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Carbon Fiber Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.