Global Capnography Device Market

Market Size in USD Million

USD

712.60 Million

USD

1,510.93 Million

2025

2033

USD

712.60 Million

USD

1,510.93 Million

2025

2033

| 2026 - 2033 | |

| USD 712.60 Million | |

| USD 1,510.93 Million | |

| % | |

|

Capnography Device Market Size

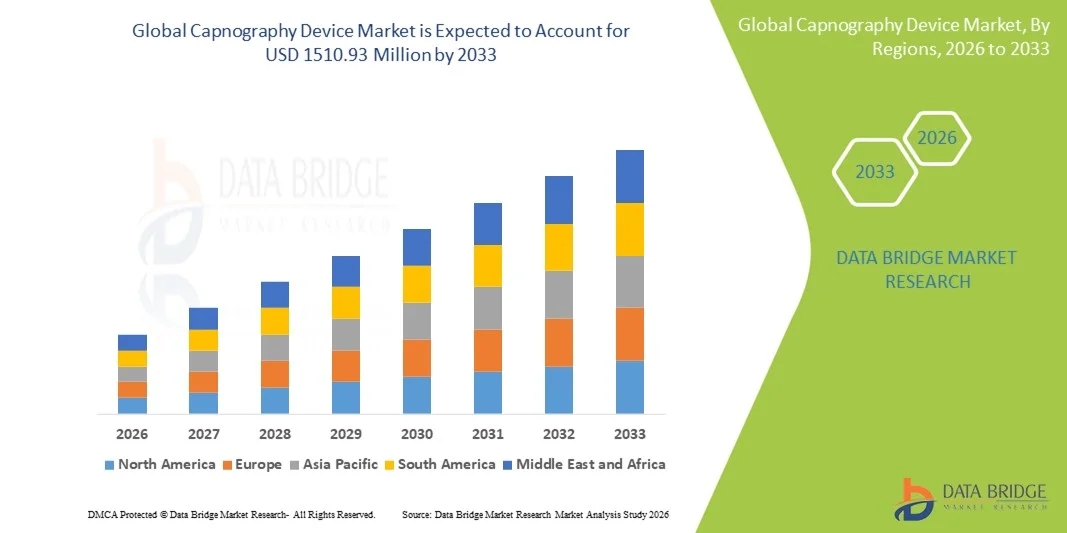

- The global capnography device market size was valued at USD 712.6 Million in 2025 and is expected to reach USD 1510.93 Million by 2033, at a CAGR of 9.85% during the forecast period

- The market growth is largely fueled by the increasing prevalence of respiratory and cardiac monitoring requirements, technological advancements in patient monitoring devices, and rising adoption of non-invasive diagnostic solutions across hospitals, surgical centers, and critical care units

- Furthermore, growing demand for real-time patient monitoring, enhanced procedural safety, and accurate anesthesia management is accelerating the uptake of Capnography Device solutions, thereby significantly boosting the industry's growth

Capnography Device Market Analysis

- Capnography devices, providing real-time monitoring of patients' respiratory status during surgery, anesthesia, and critical care, are increasingly vital components in modern healthcare settings due to their enhanced accuracy, non-invasive measurement, and integration with advanced patient monitoring systems

- The escalating demand for capnography devices is primarily fueled by rising surgical procedures, increasing prevalence of respiratory diseases, and the growing need for patient safety and early detection of respiratory complications

- North America dominated the capnography device market with the largest revenue share of 38.5% in 2025, characterized by advanced healthcare infrastructure, high adoption of patient monitoring technologies, and a strong presence of leading medical device manufacturers, with the U.S. experiencing substantial growth in Capnography Device installations across hospitals, surgical centers, and ICUs

- Asia-Pacific is expected to be the fastest growing region in the capnography device market during the forecast period, projected to record a CAGR from 2026 to 2033, driven by increasing healthcare investments, rising surgical procedures, and growing awareness of patient safety in countries such as China, India, and Japan

- The OEM Modules segment accounted for the largest market revenue share of 63.8% in 2025, driven by hospitals and manufacturers preferring original components for compatibility, accuracy, and regulatory compliance

Report Scope and Capnography Device Market Segmentation

|

Attributes |

Capnography Device Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Medtronic (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Capnography Device Market Trends

Rising Adoption of Portable and Wearable Capnography Devices

- The demand for portable, compact, and user-friendly capnography devices is accelerating across the home healthcare and ambulatory care sectors. These devices allow continuous respiratory monitoring in non-traditional care settings, including outpatient clinics and home care facilities

- For instance, in March 2023, Masimo launched the Rad-97 pulse CO-oximeter with integrated capnography capabilities, designed for portability and real-time patient monitoring in critical care and emergency situations

- The trend is also influenced by the growing integration of capnography with multi-parameter monitors and telehealth platforms, enabling clinicians to remotely assess patient respiratory status, improve early intervention, and enhance clinical outcomes

- In addition, the miniaturization of sensors and the development of lightweight, wearable devices are encouraging adoption among healthcare professionals, especially in surgical, emergency, and intensive care units

- Continuous innovation in sensor technology, battery life, and wireless data transmission is expected to further accelerate the adoption of portable capnography devices globally

Capnography Device Market Dynamics

Driver

Growing Need for Continuous Patient Monitoring and Early Detection

- A significant and accelerating trend in the global capnography device market is the increasing adoption of advanced patient monitoring systems across hospitals, ambulatory surgical centers, and critical care units. Clinicians are increasingly relying on capnography for real-time respiratory monitoring, early detection of adverse events, and enhanced patient safety

- For instance, in April 2025, Medtronic announced the launch of its latest Capnostream™ 35 portable capnography system, designed to offer continuous, non-invasive monitoring for both adult and pediatric patients. This device integrates advanced sensors for high-accuracy readings, helping hospitals reduce clinical complications during anesthesia and sedation

- The growing prevalence of chronic respiratory diseases, such as COPD, asthma, and sleep apnea, is driving the demand for capnography devices in both inpatient and outpatient settings, enabling healthcare providers to monitor ventilation parameters and optimize treatment

- Furthermore, the increasing number of surgical procedures worldwide, coupled with a rising focus on patient safety and anesthesia monitoring standards, is making capnography devices an essential component of modern operating rooms

Restraint/Challenge

High Device Cost and Regulatory Compliance Challenges

- The relatively high initial cost of advanced capnography devices can be a barrier to adoption, particularly in small hospitals, outpatient clinics, and in developing regions. Devices with multi-parameter integration, wireless connectivity, and high-accuracy sensors often come at premium prices, limiting their accessibility for budget-constrained healthcare facilities

- For instance, in 2022, reports indicated that smaller community hospitals in Southeast Asia were hesitant to adopt high-end capnography systems due to financial constraints and limited reimbursement policies

- Compliance with stringent regulatory standards, such as FDA approval, CE marking, and ISO certifications, also poses challenges for new entrants in the market. Manufacturers must invest significantly in testing, documentation, and clinical validation to meet global regulatory requirements

- Concerns regarding proper device usage, maintenance, and clinician training further impact market penetration, as inaccurate readings can compromise patient safety and clinical decisions

- Overcoming these challenges through cost-effective device solutions, local manufacturing, enhanced clinician training programs, and simplified regulatory approval processes will be essential for sustained growth in the capnography device market

Capnography Device Market Scope

The market is segmented on the basis of product, technology, component, application, and end user.

- By Product

On the basis of product, the Global Capnography Device market is segmented into Capnometers, Parameters, and Accessories. The Capnometers segment dominated the largest market revenue share of 58.4% in 2025, driven by the increasing adoption of capnometry for continuous respiratory monitoring in critical care and surgical procedures. Hospitals and emergency care units across North America, Europe, and Asia-Pacific prefer capnometers for their high accuracy, reliability, and real-time monitoring capabilities. Growing awareness about patient safety and early detection of respiratory complications contributes to the segment’s dominance. Integration with modern patient monitoring systems and electronic health records enhances clinical efficiency. Technological improvements in sensor accuracy and display interfaces further reinforce adoption. The increasing prevalence of surgical procedures requiring anesthesia also supports consistent demand. OEM partnerships and hospital procurement programs contribute to higher market penetration. Regulatory approvals and standardized guidelines for respiratory monitoring encourage institutional adoption. Rising focus on reducing ICU morbidity and improving patient outcomes strengthens segment leadership. The availability of both portable and fixed capnometers facilitates diverse clinical use, increasing overall market share.

The Parameters segment is expected to witness the fastest CAGR of 14.2% from 2026 to 2033, fueled by the rising demand for multi-parameter monitoring devices that measure CO₂, tidal volume, and respiratory rate simultaneously. Advances in real-time data analytics and alarm systems drive adoption across operating rooms and critical care units. The increasing trend toward personalized patient monitoring, including neonatal and pediatric care, supports rapid growth. Hospitals and homecare settings are increasingly procuring modular parameter systems compatible with existing monitors. Integration with telehealth platforms enhances remote monitoring capabilities. Continuous monitoring in trauma and emergency care units drives high utilization. Emerging markets in Asia-Pacific and the Middle East are witnessing growing adoption due to improving healthcare infrastructure. Rising awareness among clinicians about early warning scores and patient safety initiatives accelerates expansion. Collaborations between device manufacturers and healthcare providers further facilitate widespread adoption. Portable and wearable parameter devices are gaining traction, adding to market momentum.

- By Technology

On the basis of technology, the market is segmented into Mainstream Capnography, Sidestream Capnography, and Microstream Capnography. The Mainstream Capnography segment held the largest market revenue share of 49.6% in 2025, owing to its direct measurement at the airway, providing fast and accurate readings during surgeries and mechanical ventilation. Hospitals and ambulatory care centers favor mainstream systems for their reliability in high-acuity environments. Reduced sensor lag, fewer calibration requirements, and enhanced integration with ventilators support segment dominance. Increased surgical volumes, critical care expansions, and heightened focus on anesthesia safety drive consistent adoption. OEM enhancements, including smaller form factors and improved ergonomic designs, promote usage. Regulatory guidelines advocating continuous respiratory monitoring reinforce demand. Widespread adoption in developed countries, particularly in cardiac and trauma care, maintains market leadership. Integration with advanced monitoring platforms facilitates improved workflow efficiency. Cost-effectiveness relative to repeated disposable components also supports growth. Continuous training programs for clinicians on capnography usage boost penetration.

The Sidestream Capnography segment is expected to witness the fastest CAGR of 15.1% from 2026 to 2033, driven by its non-invasive design, suitability for spontaneously breathing patients, and versatility across emergency, homecare, and transport applications. Portable sidestream devices are increasingly deployed in ambulances, ICU, and homecare settings. Continuous innovation in sampling lines and filter technology improves reliability. The growing elderly population and rise in chronic respiratory conditions increase demand. Hospitals and clinics favor sidestream systems for flexible patient management. Integration with telemonitoring platforms supports remote patient observation. Training programs for emergency care providers enhance adoption rates. Emerging markets in Latin America and Asia-Pacific offer significant growth opportunities. Improved battery life and miniaturized designs make sidestream capnography suitable for mobile applications. Rising awareness about patient safety and early detection of hypoventilation accelerates market expansion.

- By Component

On the basis of component, the market is segmented into OEM Modules and Others. The OEM Modules segment accounted for the largest market revenue share of 63.8% in 2025, driven by hospitals and manufacturers preferring original components for compatibility, accuracy, and regulatory compliance. OEM modules ensure device reliability, reduce maintenance costs, and enhance integration with existing monitoring infrastructure. Large hospitals and critical care centers prioritize certified modules for continuous monitoring. Technological improvements, including miniaturized sensors and high-precision components, further reinforce dominance. OEM partnerships with healthcare providers streamline supply chains and reduce downtime. Regulatory approvals and safety certifications contribute to segment adoption. Hospitals in developed countries prefer OEM modules for risk mitigation and device longevity. Integration with electronic medical record systems supports efficient patient monitoring. Increased awareness about patient safety and device reliability drives consistent demand. The segment benefits from recurring purchases of consumable OEM components, increasing market share.

The Others segment is expected to witness the fastest CAGR of 12.9% from 2026 to 2033, fueled by growing demand for aftermarket components, third-party accessories, and cost-effective replacements. Emerging hospitals and homecare centers increasingly adopt non-OEM parts to reduce capital expenditure. Customizable and modular designs enhance the flexibility of devices. Suppliers focusing on compatibility and cost-effectiveness expand adoption in price-sensitive markets. The rise of small clinics and remote patient monitoring applications supports demand. Third-party components facilitate rapid deployment in regions with limited access to OEM products. Innovations in disposable sensors and tubing further drive growth. Expansion in developing countries accelerates aftermarket component utilization. Clinician familiarity with compatible alternatives supports adoption. Growth is supported by rising device maintenance and replacement cycles.

- By Application

On the basis of application, the market is segmented into Cardiac Care, Trauma & Emergency Care, Respiratory Monitoring, and Other Applications. The Cardiac Care segment dominated the largest market revenue share of 52.3% in 2025, driven by the widespread adoption of capnography for intraoperative and perioperative monitoring during cardiac surgeries. Hospitals and specialized cardiac centers prefer capnography devices to track ventilation efficacy and patient safety. Integration with anesthesia workstations and ICU monitoring systems enhances workflow efficiency. Rising incidence of cardiovascular diseases globally supports segment dominance. Technological improvements in real-time monitoring, alarms, and data analytics further reinforce adoption. Regulatory guidelines mandating continuous monitoring in cardiac units encourage usage. Training programs for clinicians and anesthesiologists strengthen adoption. Hospitals investing in advanced surgical infrastructure prioritize capnography. OEM collaborations and maintenance contracts support high penetration.

The Respiratory Monitoring segment is expected to witness the fastest CAGR of 14.8% from 2026 to 2033, driven by increasing prevalence of respiratory disorders, chronic obstructive pulmonary disease (COPD), and COVID-19-related monitoring requirements. Homecare settings, ICUs, and emergency departments increasingly deploy capnography for early detection of hypoventilation. Continuous monitoring improves patient outcomes and reduces hospital readmissions. Portable devices and wearable systems enhance adoption. Training programs for respiratory therapists facilitate usage. Rising government healthcare initiatives in emerging markets support growth. Integration with telemedicine and remote monitoring platforms accelerates adoption. Technological advancements, including wireless data transmission and battery optimization, further boost segment expansion.

- By End User

On the basis of end user, the market is segmented into Hospitals, Ambulatory Care Centers, Homecare, and Others. The Hospitals segment accounted for the largest market revenue share of 56.7% in 2025, owing to the presence of critical care units, ORs, and high patient volumes requiring continuous monitoring. Hospitals prefer capnography devices for their accuracy, reliability, and integration with existing monitoring systems. Increasing surgical procedures, ICU expansions, and regulatory guidelines promote device adoption. OEM support, service agreements, and recurring module purchases reinforce market dominance. Training and awareness programs for clinicians support effective utilization. Large hospitals in North America and Europe continue to lead in adoption rates.

The Homecare segment is expected to witness the fastest CAGR of 15.3% from 2026 to 2033, driven by rising demand for remote patient monitoring, chronic respiratory care, and portable capnography systems. Elderly patients, post-operative care, and chronic disease management in home settings contribute to rapid growth. Integration with telemedicine platforms allows continuous monitoring by healthcare providers. Emerging markets are witnessing increasing adoption due to improving healthcare infrastructure. Portable, cost-effective devices make homecare monitoring feasible. Rising awareness among caregivers and healthcare professionals supports adoption. Government initiatives for remote care monitoring further accelerate growth.

Capnography Device Market Regional Analysis

- North America dominated the capnography device market with the largest revenue share of 38.5% in 2025

- Characterized by advanced healthcare infrastructure, high adoption of patient monitoring technologies, and a strong presence of leading medical device manufacturers

- The U.S. is experiencing substantial growth in Capnography Device installations across hospitals, surgical centers, and ICUs, driven by innovations in mainstream, sidestream, and microstream capnography systems

U.S. Capnography Device Market Insight

The U.S. capnography device market captured the largest revenue share in 2025 within North America, fueled by advanced healthcare infrastructure, increasing surgical and ICU procedures, and high adoption of automated patient monitoring systems. The presence of key medical device manufacturers and ongoing innovations further support market expansion.

Europe Capnography Device Market Insight

The Europe capnography device market is projected to expand at a substantial CAGR throughout the forecast period, supported by increasing awareness of patient safety, rising prevalence of respiratory and cardiac disorders, and growing adoption of advanced monitoring systems in hospitals and surgical centers.

U.K. Capnography Device Market Insight

The U.K. capnography device market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by government initiatives for healthcare modernization, expanding hospital networks, and increasing adoption of automated patient monitoring devices across ICUs and surgical centers.

Germany Capnography Device Market Insight

The Germany capnography device market is expected to expand at a considerable CAGR during the forecast period, fueled by rising investments in healthcare infrastructure, increasing number of surgical procedures, and growing awareness of patient safety protocols.

Asia-Pacific Capnography Device Market Insight

The Asia-Pacific capnography device market is poised to grow at the fastest CAGR of 12.5% during the forecast period of 2026 to 2033, driven by rising healthcare expenditures, increasing surgical and critical care procedures, and growing awareness of patient monitoring and safety in countries such as China, India, and Japan.

Japan Capnography Device Market Insight

The Japan capnography device market is gaining momentum due to the country’s advanced healthcare system, rising number of surgical procedures, and increasing focus on patient safety. The market growth is further supported by technological advancements in mainstream, sidestream, and microstream capnography devices. Increasing government initiatives to improve perioperative care and patient monitoring standards are also driving adoption across hospitals and surgical centers. Additionally, the aging population in Japan is contributing to higher demand for continuous monitoring solutions in critical care and home healthcare settings.

China Capnography Device Market Insight

The China capnography device market accounted for the largest market revenue share of 39.2% in Asia-Pacific in 2025, driven by the rapid expansion of healthcare infrastructure, high prevalence of respiratory and cardiac disorders, increasing surgical procedures, and the adoption of advanced monitoring devices across hospitals and specialty clinics.

Capnography Device Market Share

The Capnography Device industry is primarily led by well-established companies, including:

• Medtronic (U.S.)

• Philips Healthcare (Netherlands)

• GE Healthcare (U.S.)

• Drägerwerk (Germany)

• Masimo Corporation (U.S.)

• Smiths Medical (U.K.)

• Nihon Kohden (Japan)

• Spacelabs Healthcare (U.S.)

• Cardinal Health (U.S.)

• Flaem Nuova (Italy)

• Covidien (U.S.)

• Vyaire Medical (U.S.)

• Edan Instruments (China)

• Respironics (U.S.)

• CareFusion (U.S.)

• ConvaTec (U.K.)

• Rheon Medical (South Korea)

Latest Developments in Global Capnography Device Market

- In April 2021, Masimo announced that its new portable real‑time capnograph, Radius PCG, received U.S. FDA 510(k) clearance — offering a tetherless mainstream capnography option with Bluetooth connectivity, usable for patients of all ages

- In July 2021, Spacelabs Healthcare partnered with Masimo to incorporate Masimo’s NomoLine capnography and other advanced monitoring parameters into selected Spacelabs multi‑parameter patient monitors, indicating early steps toward broader integration and improved monitoring workflow

- In April 2024, a report by a major market research firm forecasted notable market expansion for capnography equipment, driven by increasing demand for non‑invasive respiratory monitoring — especially in intensive care units, emergency, anesthesia and ambulatory surgical settings

- In June 2024, the push for increased access and safety in low-resource settings gained attention: health‑care organizations and NGOs began promoting capnography more broadly during surgical and sedation procedures — underscoring growing global awareness of its importance for patient safety

- In August 2025, a market‑forecast update reported that the global capnography devices market continues expanding strongly, supported by rising prevalence of respiratory diseases, increased surgical volumes worldwide, and growing adoption of capnography across critical care and perioperative applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.