Global Bundling Films Market

Market Size in USD Billion

CAGR :

%

USD

2.49 Billion

USD

6.16 Billion

2025

2033

USD

2.49 Billion

USD

6.16 Billion

2025

2033

| 2026 –2033 | |

| USD 2.49 Billion | |

| USD 6.16 Billion | |

| % | |

|

Bundling Films Market Size

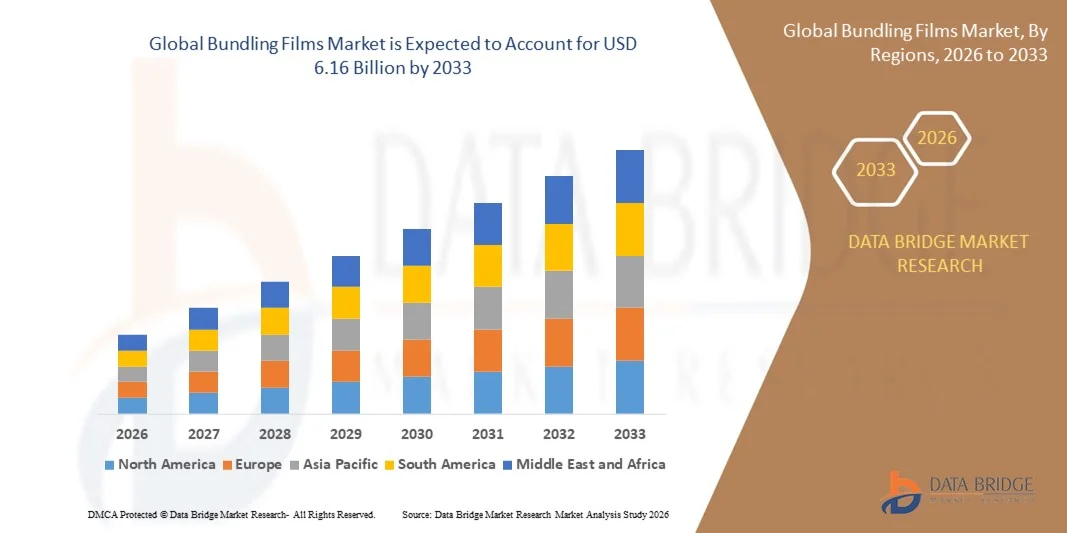

- The global bundling films market size was valued at USD 2.49 billion in 2025 and is expected to reach USD 6.16 billion by 2033, at a CAGR of 12.00% during the forecast period

- The market growth is largely fuelled by the rising demand for efficient and cost-effective packaging solutions in food, beverage, and consumer goods industries

- Increasing adoption of automated packaging systems and sustainable packaging materials is further driving market expansion

Bundling Films Market Analysis

- Rising preference for eco-friendly and recyclable packaging materials is shaping product innovation and consumer demand

- The market is witnessing increased application of bundling films in industrial, food and beverage, and retail sectors due to enhanced convenience and efficiency

- North America dominated the bundling films market with the largest revenue share of 38.7% in 2025, driven by high demand for industrial and retail packaging, along with increasing adoption of sustainable and recyclable films

- Asia-Pacific region is expected to witness the highest growth rate in the global bundling films market, driven by rising manufacturing activities, urbanization, increasing disposable incomes, and growing demand for sustainable and efficient packaging solutions

- The Polyethylene (PE) segment held the largest market revenue share in 2025, driven by its cost-effectiveness, ease of processing, and versatility across industrial and retail packaging applications. PE-based films are widely used due to their strong mechanical properties, high elongation, and ability to secure products efficiently

Report Scope and Bundling Films Market Segmentation

|

Attributes |

Bundling Films Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Bundling Films Market Trends

Shift Towards Eco-Friendly and Innovative Packaging

- The increasing focus on sustainability and environmental responsibility is reshaping the global bundling films market, as companies and consumers prioritize recyclable, biodegradable, or bio-based packaging solutions. Bundling films are gaining traction due to their ability to secure products, reduce packaging waste, and support regulatory compliance without compromising performance

- Growth in e-commerce, retail, and logistics sectors has accelerated demand for bundling films that improve product handling, reduce material usage, and enhance operational efficiency. Businesses are seeking packaging solutions that balance durability, cost-effectiveness, and environmental impact

- Consumer and corporate focus on green practices is influencing purchasing decisions, with companies highlighting eco-friendly certifications, reduced carbon footprint, and sustainable sourcing in marketing campaigns. These factors are helping brands differentiate products and build credibility with environmentally conscious clients

- For instance, in 2024, Amcor in Australia and Berry Global in the U.S. introduced biodegradable and high-strength bundling films for industrial and retail applications. The products were marketed across e-commerce, logistics, and retail channels as environmentally responsible options, strengthening brand loyalty and repeat business

- Sustained market expansion will depend on continuous R&D, innovative formulations, and production processes that maintain mechanical performance while meeting eco-friendly objectives. Manufacturers are focusing on improving scalability, supply chain efficiency, and cost competitiveness for broader adoption

Bundling Films Market Dynamics

Driver

Rising Demand for Efficient and Cost-Effective Packaging Solutions

- Increasing demand for packaging solutions that reduce material consumption, lower operational costs, and improve supply chain efficiency is driving the growth of the bundling films market. Manufacturers are seeking films that optimize product protection and handling while minimizing waste

- Expanding applications across food and beverage, pharmaceuticals, logistics, e-commerce, and industrial sectors are propelling market growth. Bundling films enhance stacking, transport safety, and product integrity, making them essential for operational efficiency in high-volume industries

- Companies are investing in advanced extrusion, coating, and lamination technologies to improve film strength, elasticity, and performance. These innovations are supporting adoption of sustainable films that meet environmental goals without compromising functionality

- For instance, in 2023, Sealed Air in the U.S. and Mondi in Germany reported increased use of high-performance bundling films in industrial and retail packaging. Improved operational efficiency, reduced material waste, and compliance with sustainability standards drove the adoption, supporting product differentiation and repeat orders

- Wider adoption still requires addressing raw material costs, scalability of production, and consistent supply. Investment in efficient manufacturing processes and supply chain optimization is crucial for sustaining growth and competitiveness

Restraint/Challenge

Higher Costs and Limited Awareness Compared to Conventional Films

- The relatively higher cost of sustainable bundling films compared to conventional plastic alternatives remains a key challenge, limiting adoption among price-sensitive manufacturers. Higher raw material costs, complex production processes, and certification requirements contribute to elevated pricing, while fluctuations in the supply of biodegradable or bio-based feedstocks can affect cost stability and market penetration

- Awareness among end-users and manufacturers remains uneven, particularly in emerging markets where sustainable packaging demand is still developing. Limited understanding of performance advantages and environmental benefits restricts adoption across certain product segments and slows innovation uptake in these regions

- Supply chain and logistical challenges also impact market growth, as sustainable bundling films require sourcing from certified suppliers and adherence to strict quality and storage standards. Cold storage, proper handling, and shorter shelf life of certain biodegradable films increase operational costs, affecting product availability and market visibility

- For instance, in 2024, distributors in India and Indonesia supplying retail and logistics companies reported slower uptake due to higher pricing and limited awareness of functional and environmental benefits compared to conventional films. Handling and storage requirements were additional barriers, prompting some retailers and logistics providers to limit shelf space or use conventional alternatives

- Overcoming these challenges will require cost-efficient production, expanded distribution networks, and focused educational initiatives for manufacturers and end-users. Collaboration with suppliers, retailers, and regulatory bodies can help unlock the long-term growth potential of the global bundling films market. Developing cost-competitive solutions and strengthening marketing around sustainability and performance will be essential for widespread adoption

Bundling Films Market Scope

The market is segmented on the basis of material, packaging type, product type, and application.

- By Material

On the basis of material, the bundling films market is segmented into Polyethylene (PE), Polyvinylidenchloride (PVDC), Polypropylene (PP), Polyvinylchloride (PVC), Polyester (PET), and Polyamide (PA). The Polyethylene (PE) segment held the largest market revenue share in 2025, driven by its cost-effectiveness, ease of processing, and versatility across industrial and retail packaging applications. PE-based films are widely used due to their strong mechanical properties, high elongation, and ability to secure products efficiently.

The Polyester (PET) segment is expected to witness the fastest growth rate from 2026 to 2033, attributed to its superior tensile strength, puncture resistance, and suitability for high-performance packaging. PET-based bundling films are increasingly preferred in logistics, food, and industrial sectors where durability and load stability are critical.

- By Packaging Type

On the basis of packaging type, the market is segmented into Flexible Packaging and Semi-Rigid Packaging. Flexible packaging held the largest market share in 2025 due to its adaptability, lightweight properties, and cost-efficient application in bundling and unitizing products for retail, logistics, and industrial use.

Semi-Rigid Packaging is anticipated to grow at the fastest rate from 2026 to 2033, driven by its enhanced load support, impact resistance, and suitability for heavy industrial and pharmaceutical applications where product protection is a priority.

- By Product Type

On the basis of product type, the market is segmented into Bundling Stretch Film, Hybrid Bundling Stretch Film, Extended Core Bundling Stretch Film, and Pre-Stretched Bundling Stretch Film. Bundling Stretch Film accounted for the largest share in 2025, supported by its versatility, high elasticity, and widespread use across food, beverage, and industrial logistics.

Hybrid Bundling Stretch Film is projected to register the highest growth during 2026–2033, as it combines the benefits of traditional stretch films with advanced properties such as improved load stability, puncture resistance, and reduced material usage, making it increasingly attractive for e-commerce and industrial applications.

- By Application

On the basis of application, the market is segmented into Food, Pharmaceuticals, Personal Care & Cosmetic Products, Industrial Goods, Commercial Goods, and Others. The Industrial Goods segment held the largest market share in 2025, driven by high demand for secure and efficient packaging solutions in logistics, manufacturing, and heavy machinery sectors.

The Food segment is expected to witness the fastest growth from 2026 to 2033, owing to increasing demand for hygienic, tamper-evident, and sustainable packaging in the food and beverage industry. Growth is supported by rising e-commerce food deliveries and the need for enhanced product protection during transportation.

Bundling Films Market Regional Analysis

- North America dominated the bundling films market with the largest revenue share of 38.7% in 2025, driven by high demand for industrial and retail packaging, along with increasing adoption of sustainable and recyclable films

- Manufacturers and distributors in the region are emphasizing packaging efficiency, waste reduction, and supply chain optimization, which has contributed to the widespread adoption of bundling films across logistics, food, and e-commerce sectors

- The region’s strong manufacturing base, high disposable incomes, and stringent environmental regulations are supporting the growth of advanced bundling films, positioning them as a preferred solution for secure and cost-effective packaging

U.S. Bundling Films Market Insight

The U.S. bundling films market captured the largest revenue share in 2025 within North America, fueled by the rapid growth of e-commerce, industrial manufacturing, and retail packaging. Companies are increasingly seeking films that offer high tensile strength, load stability, and environmentally friendly properties. Moreover, the adoption of pre-stretched and hybrid bundling films, alongside automation in packaging lines, is further driving market expansion.

Europe Bundling Films Market Insight

The Europe bundling films market is expected to witness the fastest growth rate from 2026 to 2033, driven by stringent sustainability regulations, increasing use of recyclable and biodegradable films, and rising industrial output. The region is seeing heightened demand in food, pharmaceuticals, and e-commerce sectors, with manufacturers prioritizing films that reduce packaging waste while ensuring product protection.

U.K. Bundling Films Market Insight

The U.K. bundling films market is projected to witness the fastest growth from 2026 to 2033, driven by increasing awareness of sustainable packaging solutions and rising e-commerce activities. Businesses are adopting high-performance films that provide durability and cost-efficiency, while complying with local environmental standards. Growth is supported by demand across logistics, retail, and industrial packaging segments.

Germany Bundling Films Market Insight

The Germany bundling films market is expected to grow significantly from 2026 to 2033, fueled by the country’s strong industrial base, focus on eco-friendly solutions, and advanced manufacturing infrastructure. Manufacturers are adopting high-strength and biodegradable films to improve operational efficiency and meet environmental regulations. Integration of sustainable packaging practices across industrial and food sectors is driving demand.

Asia-Pacific Bundling Films Market Insight

The Asia-Pacific bundling films market is projected to witness the fastest growth from 2026 to 2033, driven by rapid urbanization, industrialization, and the expansion of e-commerce in countries such as China, Japan, and India. Growing awareness of sustainable packaging, coupled with increasing logistics and manufacturing activities, is encouraging the adoption of high-performance bundling films.

Japan Bundling Films Market Insight

The Japan bundling films market is expected to grow rapidly from 2026 to 2033, owing to technological advancements, high demand for efficient packaging, and stringent waste reduction policies. Businesses are increasingly adopting pre-stretched and hybrid films for industrial and retail applications. The trend of smart logistics and automation in packaging lines is further supporting market growth.

China Bundling Films Market Insight

The China bundling films market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by a booming manufacturing sector, rising e-commerce penetration, and high demand for cost-effective and sustainable packaging solutions. The availability of locally manufactured high-performance films, along with the government’s push towards green packaging initiatives, is further propelling market growth.

Bundling Films Market Share

The Bundling Films industry is primarily led by well-established companies, including:

- Berry Global Inc. (U.S.)

- Amcor (Australia)

- Mondi (U.K.)

- Professional Packaging Systems, Inc. (U.S.)

- Plastipak Group (U.S.)

- Halsted Bag (U.S.)

- J&HM Dickson Ltd (U.K.)

- Intertape Polymer Group (Canada)

- Jumbo Bags (U.S.)

- LC Packaging (Netherlands)

- Langston University (U.S.)

- Shanghai Lucky Hi-Tech Material International Trade Co., Ltd. (China)

- Dongguan Yason Pack Co., Ltd. (China)

- Tongcheng Soma Package Co., Ltd. (China)

- Qingdao Bothwin International Trade Co., Ltd. (China)

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Bundling Films Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Bundling Films Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Bundling Films Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.