Global Blood Collection Market

Market Size in USD Billion

CAGR :

%

USD

9.63 Billion

USD

16.30 Billion

2025

2033

USD

9.63 Billion

USD

16.30 Billion

2025

2033

| 2026 –2033 | |

| USD 9.63 Billion | |

| USD 16.30 Billion | |

| % | |

|

Blood Collection Market Size

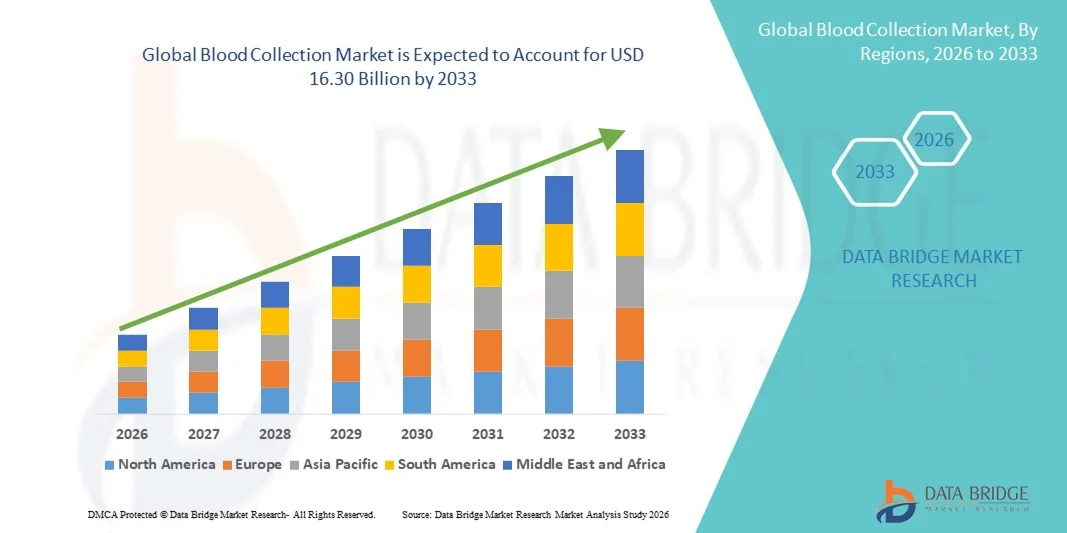

- The global blood collection market size was valued at USD 9.63 billion in 2025 and is expected to reach USD 16.30 billion by 2033, at a CAGR of 6.80% during the forecast period

- The market growth is largely fueled by the rising prevalence of chronic and infectious diseases, increasing number of diagnostic tests, and continuous advancements in blood sampling technologies, leading to greater demand across hospitals, diagnostic laboratories, and blood banks

- Furthermore, growing awareness regarding early disease detection, expanding healthcare infrastructure, and increasing adoption of minimally invasive and safety-engineered blood collection devices are establishing blood collection solutions as essential components of modern diagnostic and therapeutic procedures. These converging factors are accelerating the uptake of Blood Collection solutions, thereby significantly boosting the industry's growth

Blood Collection Market Analysis

- Blood collection devices, including needles, syringes, vacuum blood collection tubes, lancets, and blood bags, are increasingly vital components of modern diagnostic and transfusion services due to their role in accurate disease detection, therapeutic monitoring, and safe blood storage. Growing emphasis on early diagnosis and preventive healthcare continues to drive demand across healthcare facilities

- The escalating demand for blood collection products is primarily fueled by the rising prevalence of chronic diseases, increasing number of surgical procedures, expanding blood donation programs, and growing need for routine diagnostic testing across hospitals and laboratories

- North America dominated the blood collection market with the largest revenue share of 38.9% in 2025, characterized by advanced healthcare infrastructure, high diagnostic testing rates, strong presence of leading medical device manufacturers, and widespread adoption of safety-engineered blood collection systems. The U.S. accounts for a significant portion of regional demand due to increasing screening programs and high healthcare expenditure

- Asia-Pacific is expected to be the fastest-growing region in the blood collection market during the forecast period, expanding at a CAGR of 9.1% from 2026 to 2033, driven by increasing healthcare investments, growing awareness regarding early disease diagnosis, expanding hospital networks, and rising blood donation initiatives across emerging economies

- The diagnostics segment accounted for the largest market revenue share of 71.3% in 2025, driven by the increasing prevalence of chronic, infectious, and lifestyle-related diseases globally

Report Scope and Blood Collection Market Segmentation

|

Attributes |

Blood Collection Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Blood Collection Market Trends

Technological Advancements in Automated and Safety-Engineered Blood Collection Devices

- A significant and accelerating trend in the global Blood Collection market is the growing adoption of automated, safety-engineered, and patient-centric blood collection systems designed to enhance accuracy, reduce contamination risks, and improve overall workflow efficiency in healthcare settings

- Modern blood collection devices, including vacuum-based blood collection tubes, advanced lancets, and needle safety systems, are increasingly being developed with improved ergonomics and integrated safety mechanisms to minimize needlestick injuries among healthcare professionals

- For instance, manufacturers are introducing pre-assembled blood collection kits and closed-system transfer devices that reduce handling errors and lower the risk of sample contamination

- The incorporation of barcoding and digital labeling technologies is also streamlining sample identification, tracking, and data management within hospitals and diagnostic laboratories

- In addition, the demand for minimally invasive capillary blood collection methods is increasing, particularly in home healthcare and point-of-care testing environments

- This shift toward safer, more efficient, and technologically advanced blood collection solutions is transforming clinical diagnostics and strengthening product adoption across hospitals, blood banks, diagnostic centers, and ambulatory care facilities

Blood Collection Market Dynamics

Driver

Rising Prevalence of Chronic Diseases and Growing Diagnostic Testing Volumes

- The increasing global burden of chronic diseases such as diabetes, cardiovascular disorders, cancer, and infectious diseases is a major driver propelling demand for blood collection product

- Routine blood testing plays a critical role in early disease detection, treatment monitoring, and preventive healthcare, thereby significantly increasing the volume of blood samples collected worldwide

- The expansion of diagnostic laboratories, blood banks, and pathology services—particularly in emerging economies—is accelerating the procurement of advanced blood collection tubes, needles, syringes, and lancets

- Government initiatives promoting preventive healthcare screening programs and regular health check-ups are further contributing to sustained market growth

- Moreover, the growth of home healthcare services and decentralized diagnostic testing is increasing demand for user-friendly and safe blood collection devices

- The rising number of surgical procedures, trauma cases, and blood donation campaigns globally also supports consistent demand across healthcare systems

Restraint/Challenge

Risk of Needlestick Injuries and Regulatory Compliance Requirements

- One of the primary challenges in the Blood Collection market is the risk of needlestick injuries and associated transmission of blood-borne infections among healthcare workers

- Despite advancements in safety-engineered devices, improper handling or inadequate training can still result in occupational hazards

- Stringent regulatory requirements governing the manufacturing, sterilization, labeling, and disposal of blood collection products can increase compliance costs for manufacturers

- For instance, In addition, fluctuations in raw material prices and supply chain disruptions may affect product availability and pricing stability

- In low-resource settings, limited access to high-quality blood collection devices and insufficient training infrastructure can further restrict market penetration

- Addressing these challenges through enhanced safety designs, comprehensive training programs, cost-effective manufacturing strategies, and adherence to global quality standards will be essential to ensure sustainable growth in the Blood Collection market

Blood Collection Market Scope

The market is segmented on the basis of product, method, application, and end-user.

- By Product

On the basis of product, the Blood Collection market is segmented into Serum Tube, Plasma Tube, EDTA, Heparin, Coagulation, Glucose, Needle, Lancet, ESR, Syringe, and Blood Bag. The serum tube segment dominated the largest market revenue share of 28.4% in 2025, driven by its extensive utilization in routine biochemical, immunological, and serological testing procedures worldwide. Serum tubes are widely preferred in diagnostic laboratories due to their ability to deliver high-quality, interference-free samples for accurate analysis. The growing burden of chronic diseases such as diabetes, cardiovascular disorders, and kidney diseases has significantly increased routine blood testing volumes. Rising awareness regarding preventive healthcare and annual health check-ups further supports segment dominance. The increasing expansion of diagnostic laboratory chains across emerging economies also contributes to strong demand. Technological advancements such as gel-based separation systems and clot activators enhance efficiency and reliability. Hospitals prefer serum tubes due to their compatibility with automated analyzers and standardized testing protocols. In addition, strong procurement by government hospitals and private healthcare providers sustains revenue growth. Increasing insurance coverage for diagnostic procedures also promotes higher testing frequency. Rising geriatric population requiring continuous monitoring further strengthens the segment.

The blood bag segment is anticipated to witness the fastest CAGR of 11.9% from 2026 to 2033, driven by rising demand for blood transfusions, trauma management, and complex surgical procedures. Increasing road accidents and emergency admissions globally are significantly boosting transfusion requirements. Growing prevalence of hematological disorders such as anemia, hemophilia, and thalassemia is further contributing to demand. Governments are actively promoting voluntary blood donation drives, strengthening blood bank infrastructure worldwide. Technological innovations including multi-compartment blood bags for component separation improve operational efficiency. Stringent regulations regarding safe blood storage and transportation are encouraging adoption of advanced blood bags. Expanding healthcare infrastructure in developing countries is accelerating penetration. Rising organ transplant procedures and oncology treatments also increase blood usage. Increasing awareness about safe transfusion practices further fuels growth. Investments in modernization of blood banks and cold chain logistics significantly support rapid expansion of this segment.

- By Method

On the basis of method, the Blood Collection market is segmented into Manual and Automated. The manual segment dominated the largest market revenue share of 62.7% in 2025, primarily due to its widespread use in hospitals, clinics, diagnostic centers, and rural healthcare settings. Manual blood collection methods are cost-effective and require minimal technological infrastructure, making them highly accessible in low-resource regions. Skilled phlebotomists continue to rely on traditional needles and syringes for precise and controlled sample extraction. The affordability of manual devices supports high-volume procurement across public healthcare systems. Increasing outpatient visits and routine diagnostic testing further sustain strong demand. Manual methods offer flexibility in emergency and bedside sample collection situations. Developing countries with limited automation infrastructure continue to rely heavily on conventional systems. Training programs for healthcare professionals predominantly emphasize manual collection techniques. The simplicity and reliability of manual devices further reinforce their dominance.

The automated segment is projected to register the fastest CAGR of 13.6% from 2026 to 2033, driven by rising demand for precision, efficiency, and reduced human error in blood collection procedures. Automated systems minimize needlestick injuries and improve patient safety standards. Growing emphasis on infection control protocols and occupational safety regulations accelerates adoption. Advanced diagnostic laboratories increasingly prefer automation to reduce turnaround time and enhance workflow efficiency. Integration with digital health records and laboratory information systems further strengthens market growth. Increasing healthcare expenditure globally supports investment in automated technologies. Technological advancements enabling vacuum-assisted and closed-system blood collection enhance reliability. Rising focus on quality assurance and standardized sample handling also fuels growth. Expansion of corporate hospitals and specialty diagnostic chains significantly contributes to rapid adoption.

- By Application

On the basis of application, the Blood Collection market is segmented into Diagnostics and Treatment. The diagnostics segment accounted for the largest market revenue share of 71.3% in 2025, driven by the increasing prevalence of chronic, infectious, and lifestyle-related diseases globally. Rising adoption of preventive healthcare and routine screening programs significantly increases blood testing volumes. Government initiatives supporting early disease detection programs further enhance demand. The expanding geriatric population requiring regular health monitoring strengthens dominance. Technological advancements in molecular diagnostics and biomarker testing further boost sample requirements. Increasing cases of diabetes, cardiovascular diseases, and thyroid disorders drive routine testing frequency. Growth in personalized medicine and precision diagnostics also supports expansion. Expanding laboratory networks and diagnostic chains across emerging economies further contribute to segment strength. Insurance coverage for laboratory tests promotes higher testing rates.

The treatment segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, fueled by rising blood transfusion procedures, chemotherapy treatments, and surgical interventions worldwide. Increasing trauma and accident cases significantly raise emergency transfusion needs. Growing cancer prevalence requiring supportive blood therapy further accelerates demand. Expansion of intensive care units and trauma centers enhances blood utilization. Rising organ transplant surgeries also contribute to growth. Technological advancements in transfusion medicine improve safety and compatibility testing. Government investments in emergency healthcare infrastructure further support expansion. Increasing awareness regarding advanced therapeutic procedures strengthens demand. The growing burden of hematological disorders globally also accelerates the segment’s rapid growth.

- By End-User

On the basis of end-user, the Blood Collection market is segmented into Hospital, Blood Bank Center, Academics, and Home Care. The hospital segment dominated the largest market revenue share of 48.9% in 2025, driven by high patient admissions, advanced diagnostic infrastructure, and comprehensive treatment capabilities. Hospitals conduct a substantial number of daily blood tests for inpatient and outpatient services. Increasing surgical procedures and emergency admissions significantly contribute to blood collection demand. Integration of automated laboratory systems enhances operational efficiency within hospitals. Rising chronic disease burden requires continuous monitoring, supporting higher testing volumes. Expansion of multi-specialty hospitals in developing economies further strengthens segment dominance. Availability of skilled healthcare professionals ensures efficient sample handling and processing. Government funding for hospital infrastructure also contributes to growth.

The home care segment is anticipated to witness the fastest CAGR of 12.4% from 2026 to 2033, driven by increasing demand for remote patient monitoring and convenient diagnostic services. Rising geriatric population preferring home-based healthcare solutions significantly supports growth. Technological advancements enabling safe at-home blood sample collection kits enhance accessibility. Expansion of telehealth platforms and doorstep diagnostic sample collection services accelerates adoption. Growing awareness about preventive healthcare and regular health monitoring further boosts demand. Increasing prevalence of chronic diseases requiring frequent testing supports home-based services. Cost-effectiveness and reduced hospital visits also encourage patients to opt for home care solutions. Investments in digital health infrastructure further strengthen this rapidly growing segment.

Blood Collection Market Regional Analysis

- North America dominated the blood collection market with the largest revenue share of 38.9% in 2025, characterized by advanced healthcare infrastructure, high diagnostic testing volumes, strong presence of leading medical device manufacturers, and widespread adoption of safety-engineered blood collection systems

- The region benefits from well-established hospital networks, organized blood banks, and a high frequency of routine health screenings and preventive diagnostic programs

- The market accounts for a significant portion of regional demand due to increasing nationwide screening initiatives, rising chronic disease prevalence, and consistently high healthcare expenditure supporting the procurement of advanced blood collection devices

U.S. Blood Collection Market Insight

The U.S. blood collection market captured the largest revenue share within North America in 2025, supported by a robust diagnostic testing ecosystem and strong clinical laboratory infrastructure. The growing burden of diabetes, cardiovascular diseases, cancer, and infectious diseases is significantly increasing the demand for routine blood testing. Government-supported screening programs and preventive healthcare initiatives are further boosting testing volumes across hospitals and diagnostic laboratories. In addition, the presence of major global manufacturers and continuous innovation in safety-engineered devices, vacuum blood collection tubes, and minimally invasive lancets are strengthening market growth. Expansion of home healthcare services and point-of-care diagnostics is also contributing to sustained demand across the country.

Europe Blood Collection Market Insight

The Europe blood collection market is projected to expand at a steady CAGR throughout the forecast period, driven by strong public healthcare systems and increasing emphasis on early disease detection. Rising geriatric populations and the growing prevalence of chronic illnesses are increasing the need for regular blood-based diagnostic testing. Regulatory mandates promoting the use of safety-engineered devices to prevent needlestick injuries are accelerating the replacement of conventional blood collection products. Furthermore, expanding blood donation programs and well-established transfusion services across major European countries are supporting consistent product demand. Investments in laboratory automation and digital sample tracking systems are also contributing to regional growth.

U.K. Blood Collection Market Insight

The U.K. blood collection market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by structured national screening programs and a strong diagnostic laboratory network. Increasing awareness regarding preventive healthcare and early disease diagnosis is encouraging routine blood testing across various age groups. Government-backed blood donation campaigns and modernization of pathology services are further driving demand for advanced blood collection systems. In addition, the adoption of safety-compliant devices to reduce occupational hazards among healthcare workers is strengthening market penetration. The expansion of community healthcare services is also contributing to broader product utilization.

Germany Blood Collection Market Insight

The Germany blood collection market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s advanced healthcare infrastructure and high diagnostic standards. Germany’s strong emphasis on precision medicine and laboratory accuracy supports the adoption of high-quality blood collection tubes, needles, and safety devices. Rising incidence of chronic conditions and increasing laboratory testing volumes are creating sustained demand. Moreover, regulatory compliance requirements encouraging safer medical device usage are accelerating the shift toward advanced blood collection systems. The presence of established medical device manufacturers and research institutions further enhances market growth prospects.

Asia-Pacific Blood Collection Market Insight

The Asia-Pacific blood collection market is expected to be the fastest-growing region, expanding at a CAGR of 9.1% from 2026 to 2033, driven by increasing healthcare investments, expanding hospital infrastructure, and growing awareness regarding early disease diagnosis. Rapid urbanization and improving access to healthcare services in countries such as China, India, Japan, and South Korea are significantly increasing diagnostic testing volumes. Government initiatives promoting routine health check-ups and strengthening blood donation programs are further stimulating demand. In addition, the expansion of private diagnostic chains and rising medical tourism are contributing to increased procurement of blood collection products across the region.

Japan Blood Collection Market Insight

The Japan blood collection market is gaining steady momentum due to the country’s aging population and strong focus on preventive healthcare. High diagnostic accuracy standards and advanced laboratory systems are encouraging the use of technologically advanced blood collection devices. Increasing incidence of age-related chronic diseases is leading to frequent blood-based monitoring and testing. Furthermore, Japan’s well-organized blood transfusion services and strict regulatory compliance requirements are supporting steady product adoption. Continuous innovation in minimally invasive and patient-friendly collection methods is also enhancing market growth.

China Blood Collection Market Insight

China blood collection market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid healthcare infrastructure development and expanding diagnostic laboratory networks. Rising healthcare awareness, increasing government healthcare expenditure, and large-scale population screening programs are driving blood testing volumes. The country’s expanding hospital network and growing private healthcare sector are significantly boosting demand for blood collection tubes, syringes, and safety devices. In addition, national blood donation initiatives and improvements in transfusion medicine infrastructure are supporting sustained market expansion. The presence of domestic manufacturers is also improving affordability and accessibility of blood collection products across urban and rural regions.

Blood Collection Market Share

The Blood Collection industry is primarily led by well-established companies, including:

- BD (U.S.)

- Terumo Corporation (Japan)

- Sarstedt AG & Co. (Germany)

- Greiner Bio-One (Austria)

- Hamilton Company (U.S.)

- S-Monovette (Germany)

- Vacuette (Austria)

- BD Vacutainer (U.S.)

- Micropoint Diagnostics (U.S.)

- Haemonetics Corporation (U.S.)

- Cardinal Health (U.S.)

- Sigma-Aldrich (U.S.)

- Lonza Group (Switzerland)

- Novacyt (U.K.)

- ooperSurgical (U.S.)

- Ortho Clinical Diagnostics (U.S.)

- Ceveron AB (Sweden)

- ITEA Medical AB (Sweden)

- Tecan Group (Switzerland)

- Bio-Rad Laboratories (U.S.)

Latest Developments in Global Blood Collection Market

- In December 2023, Becton, Dickinson and Company (BD) received U.S. FDA 510(k) clearance for a novel fingerstick blood collection device that enables laboratory-quality results from fingerstick samples, helping expand point-of-care testing and reduce reliance on traditional venipuncture. This device supports easier, less invasive blood sampling for routine diagnostics

- In December 2024, BD, together with Babson Diagnostics, launched the BD MiniDraw Capillary Blood Collection System, incorporating BetterWay technologies to collect small volumes of capillary blood for diagnostic testing — broadening blood draw options in pharmacies and outpatient setting

- In March 2024, BD launched the BD Vacutainer UltraTouch Push Button Blood Collection Set in India, featuring BD RightGauge and PentaPoint technologies that reduce patient discomfort with a thinner needle and smoother insertion, enhancing patient experience during blood collection

- In June 2024, Tasso Inc. partnered with Lindus Health to introduce a remote blood collection system for clinical trials, enabling patients to collect their own blood samples with minimal discomfort, which increases accessibility for decentralized research and large-scale studies

- In April 2024, Streck launched the Protein Plus BCT whole blood collection tube* designed to stabilize plasma proteins across a wide concentration range at room temperature for research applications, supporting biomarker and proteomic studies

- In January 2025, Terumo BCT signed a strategic partnership Memorandum of Understanding (MoU) with the Shandong Institute of Medical Devices and Pharmaceutical Packaging Inspection to bolster technical research and innovation in blood component collection technologies, strengthening long-term product development strategies

- In January 2025, Fresenius Kabi received FDA clearance for the Adaptive Nomogram feature for its Aurora Xi Plasmapheresis System, enabling an ~11.5 % increase in plasma collection per donation while ensuring safe operation — a key improvement for plasma collection efficiency in blood banks

- In March 2025, BD and Babson Diagnostics reported that fingertip capillary blood tests can match the accuracy of traditional venous draws for wellness and chronic disease monitoring, highlighting a shift in clinical practice toward alternative blood collection methods that maintain diagnostic reliability

- In March 2025, Shin Nippon Biomedical Laboratories and Tasso Inc. formed a joint venture to distribute on-demand blood collection devices in Japan, expanding access to minimally invasive and decentralized blood sampling solutions in telehealth and self-care markets

- In April 2025, research reported the development of a microneedle-based patch blood collection method by a University of Wisconsin-Madison team, offering a nearly painless alternative to traditional needles and pointing toward future advancements in non-invasive blood sampling

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.