Global Benign Prostatic Hyperplasia Devices Market

Market Size in USD Billion

USD

8.70 Billion

USD

24.99 Billion

2024

2032

USD

8.70 Billion

USD

24.99 Billion

2024

2032

| 2025 - 2032 | |

| USD 8.70 Billion | |

| USD 24.99 Billion | |

| % | |

|

Benign Prostatic Hyperplasia Devices Market Size

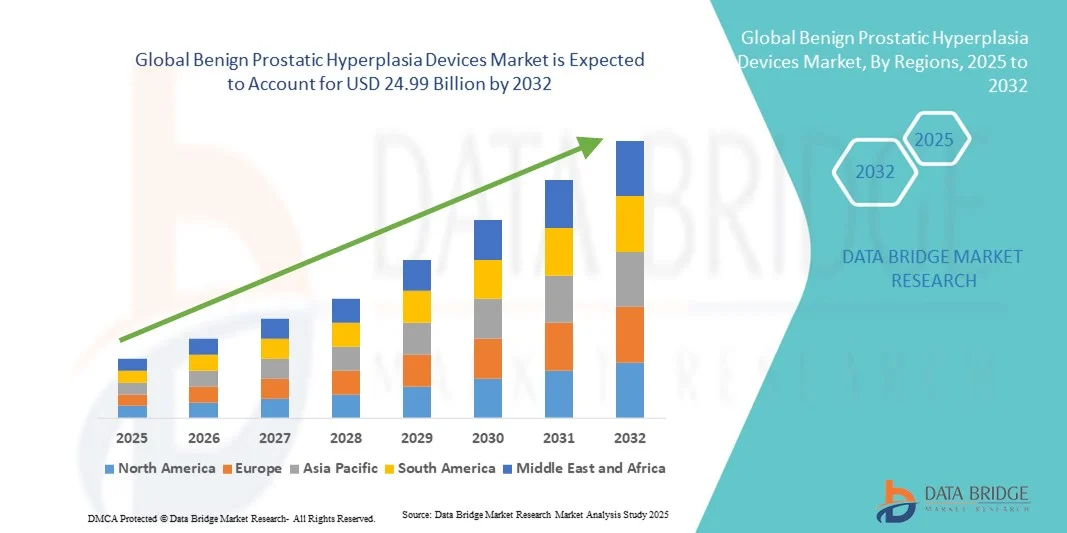

- The global benign prostatic hyperplasia devices market size was valued at USD 8.70 billion in 2024 and is expected to reach USD 24.99 billion by 2032, at a CAGR of 14.1% during the forecast period

- The market growth is largely driven by the increasing prevalence of BPH among the aging male population, coupled with the rising demand for minimally invasive and effective treatment options that offer faster recovery and fewer complications

- Furthermore, advancements in laser-based and prostatic urethral lift technologies, along with growing awareness about early diagnosis and outpatient procedures, are enhancing adoption rates across hospitals and specialty clinics. These factors are collectively propelling the expansion of the global BPH devices market

Benign Prostatic Hyperplasia Devices Market Analysis

- Benign prostatic hyperplasia (BPH) devices, encompassing minimally invasive and surgical tools designed to treat prostate enlargement, are becoming increasingly essential in urological care for managing lower urinary tract symptoms in aging men due to their improved safety, reduced hospital stays, and enhanced patient outcomes

- The rising demand for BPH treatment devices is primarily driven by the growing global geriatric male population, increasing awareness of advanced treatment options, and technological innovations in laser therapy and prostatic urethral lift systems offering effective alternatives to conventional surgery

- North America dominated the BPH devices market with the largest revenue share of 38.7% in 2024, supported by well-established healthcare infrastructure, higher diagnosis rates, and widespread adoption of minimally invasive techniques, particularly in the U.S., where strong manufacturer presence and supportive reimbursement policies further accelerate market growth

- Asia-Pacific is expected to be the fastest-growing region during the forecast period due to expanding healthcare access, increasing awareness about BPH treatments, and growing investments by medical device companies to penetrate emerging markets such as China, India, and South Korea

- The transurethral resection of the prostate (TURP) segment dominated the BPH devices market with a market share of 42.4% in 2024, attributed to its long-standing clinical efficacy, availability across hospitals, and continued preference among urologists as the standard surgical treatment for moderate to severe BPH cases

Report Scope and Benign Prostatic Hyperplasia Devices Market Segmentation

|

Attributes |

Benign Prostatic Hyperplasia Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Benign Prostatic Hyperplasia Devices Market Trends

Shift Toward Outpatient and Minimally Invasive BPH Treatments

- A significant and accelerating trend in the global benign prostatic hyperplasia (BPH) devices market is the growing shift toward minimally invasive and outpatient treatment approaches that reduce recovery time, hospital stays, and procedural risks while maintaining therapeutic efficacy

- For instance, Boston Scientific’s Rezūm Water Vapor Therapy and Teleflex’s UroLift System have gained notable traction as effective office-based alternatives to traditional surgical methods, enabling faster patient recovery and minimal anesthesia use

- The adoption of advanced laser therapies such as holmium laser enucleation of the prostate (HoLEP) is also increasing due to precision tissue removal and reduced postoperative complications, enhancing clinical outcomes and patient satisfaction

- Furthermore, the demand for ambulatory and same-day procedures is growing as healthcare systems globally focus on cost-efficiency and patient comfort, fueling demand for compact and easy-to-use treatment systems

- This trend toward minimally invasive and outpatient BPH management is driving device manufacturers to innovate in compact, energy-efficient platforms with improved ergonomics and real-time imaging guidance, transforming the standard of BPH care worldwide

- The demand for efficient, safe, and clinic-based BPH treatment devices continues to rise across developed and emerging markets, as patients and healthcare providers increasingly prioritize convenience, safety, and reduced procedural burden

Benign Prostatic Hyperplasia Devices Market Dynamics

Driver

Rising Prevalence of BPH and Demand for Minimally Invasive Therapies

- The increasing prevalence of benign prostatic hyperplasia among aging male populations, coupled with growing patient preference for minimally invasive solutions, is a significant driver for the rising demand for advanced BPH treatment devices

- For instance, in March 2024, Teleflex Incorporated expanded the availability of its UroLift 2 System across major urology centers in Europe, addressing the rising need for effective, non-surgical treatment alternatives

- As healthcare systems emphasize improved patient outcomes and cost reduction, BPH devices offering shorter recovery times, reduced bleeding, and outpatient compatibility are being rapidly adopted

- Furthermore, advancements in laser and prostatic urethral lift technologies are enabling physicians to deliver precision therapy with fewer complications, thereby increasing procedural safety and patient satisfaction

- The rising awareness of early intervention and the growing presence of trained urologists in both developed and developing regions are further strengthening the market’s growth trajectory. The parallel expansion of hospital infrastructure and adoption of digital urology platforms are also contributing to market momentum

Restraint/Challenge

High Device Cost and Reimbursement Limitation

- The high cost associated with advanced BPH treatment devices and limited reimbursement coverage in several regions pose significant challenges to widespread adoption, particularly in low- and middle-income countries

- For instance, despite proven clinical efficacy, the out-of-pocket costs for procedures involving laser systems such as HoLEP or GreenLight PVP remain high in regions with underdeveloped insurance frameworks

- Addressing these affordability barriers through value-based pricing, government health initiatives, and reimbursement expansion is crucial for improving patient access to modern BPH treatments

- Moreover, the need for specialized training and infrastructure for device operation further increases overall treatment costs and limits accessibility in rural or resource-constrained settings

- In addition, the absence of standardized clinical guidelines across some healthcare systems affects the adoption of newer technologies, while economic disparities and uneven reimbursement policies continue to hinder consistent market penetration

- Although manufacturers are working toward cost-effective solutions and greater reimbursement inclusion, achieving broad accessibility remains a key challenge for sustained BPH device market expansion

Benign Prostatic Hyperplasia Devices Market Scope

The market is segmented on the basis of procedure type and end user.

- By Procedure Type

On the basis of procedure type, the benign prostatic hyperplasia devices market is segmented into Transurethral Resection of the Prostate (TURP), Prostatic Urethral Lift (PUL), Prostatectomy, Laser Surgery, Transurethral Microwave Therapy (TUMT), Transurethral Needle Ablation of the Prostate (TUNA), Prostatic Stenting/Implants, and Others. Transurethral Resection of the Prostate (TURP) segment dominated the market with the largest market revenue share of 42.4% in 2024. TURP remains the gold-standard surgical procedure for the treatment of moderate to severe BPH symptoms due to its proven long-term efficacy and widespread clinical acceptance. The technique allows for effective removal of excess prostatic tissue, providing immediate symptom relief and improved urinary flow. The dominance of TURP is supported by its availability across both public and private healthcare facilities and the high level of physician familiarity with the procedure. In addition, continuous improvements in resectoscope design and electrosurgical technology have enhanced procedural safety and outcomes, maintaining TURP’s leadership position in the market. Hospitals continue to favor TURP for its well-documented success rates, reliability, and cost-effectiveness compared to other interventions.

The Prostatic Urethral Lift (PUL) segment is anticipated to witness the fastest growth rate from 2025 to 2032, driven by the rising preference for minimally invasive, office-based procedures. PUL, exemplified by devices such as the Teleflex UroLift System, offers an effective alternative to traditional surgery without the need for cutting or removal of tissue, significantly reducing the risk of complications such as sexual dysfunction. Its suitability for outpatient settings aligns with the global shift toward day-care urology and cost-efficient healthcare delivery. Increasing clinical validation and favorable reimbursement policies in developed markets are further accelerating its adoption. Moreover, growing awareness among urologists and patients regarding its short recovery time and durable outcomes is expected to boost PUL’s market share substantially in the coming years.

- By End User

On the basis of end user, the benign prostatic hyperplasia devices market is segmented into hospitals and clinics, ambulatory surgical centres (ASCs), and others. The Hospitals and Clinics segment dominated the market with the largest revenue share in 2024, driven by the high volume of surgical and minimally invasive BPH procedures performed in hospital settings. Hospitals benefit from advanced surgical infrastructure, skilled urologists, and access to comprehensive post-operative care facilities, making them the preferred choice for TURP and laser-based procedures. In addition, favorable reimbursement coverage and the availability of advanced imaging and diagnostic systems contribute to their dominance. The concentration of major medical device suppliers and training programs in hospital networks further strengthens this segment’s leadership. The strong patient trust in hospital-based interventions also plays a critical role in sustaining demand for BPH treatment devices across global healthcare systems.

The Ambulatory Surgical Centres (ASCs) segment is expected to record the fastest growth from 2025 to 2032, supported by the expanding adoption of minimally invasive and outpatient-based procedures such as PUL, TUMT, and laser ablation therapies. ASCs offer significant cost advantages, reduced hospital stays, and faster recovery, which are increasingly appealing to both patients and healthcare providers. For instance, the growing preference for same-day discharge and lower procedural expenses is driving the shift of BPH treatments to ASCs, particularly in North America and Europe. Technological advances enabling compact and user-friendly BPH devices suitable for ambulatory use are further fueling this trend. The rise of value-based care models and insurance support for outpatient procedures will continue to accelerate the growth of ASCs as key end users in the global BPH devices market.

Benign Prostatic Hyperplasia Devices Market Regional Analysis

- North America dominated the BPH devices market with the largest revenue share of 38.7% in 2024, supported by well-established healthcare infrastructure, higher diagnosis rates, and widespread adoption of minimally invasive techniques, particularly in the U.S., where strong manufacturer presence and supportive reimbursement policies further accelerate market growth

- The region’s healthcare infrastructure supports early diagnosis, precision treatment, and wide availability of innovative solutions such as laser therapy and prostatic urethral lift systems, enhancing overall procedural outcomes

- This dominance is further reinforced by favorable reimbursement frameworks, significant R&D investments by leading manufacturers, and the presence of skilled urologists, making North America a key hub for technological innovation and adoption in the global BPH devices market

U.S. Benign Prostatic Hyperplasia Devices Market Insight

The U.S. benign prostatic hyperplasia devices market captured the largest revenue share of over 78% in 2024 within North America, driven by the high prevalence of BPH among the aging male population and strong clinical adoption of minimally invasive treatments such as Rezūm Water Vapor Therapy and UroLift. The nation’s advanced healthcare infrastructure, presence of leading medical device companies, and supportive reimbursement policies significantly promote market growth. Growing awareness of early intervention, coupled with patient preference for outpatient and same-day procedures, is accelerating the use of innovative BPH treatment devices. Moreover, continuous technological advancements and clinical research initiatives further strengthen the U.S. position as the leading market for BPH treatment devices.

Europe Benign Prostatic Hyperplasia (BPH) Devices Market Insight

The Europe benign prostatic hyperplasia devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of men’s health and the growing adoption of minimally invasive procedures. Rising healthcare spending, coupled with the region’s aging population, is fostering the demand for advanced BPH treatment options. European healthcare systems are emphasizing improved quality of life and outpatient care, promoting the use of laser and PUL technologies. In addition, regulatory support for innovative medical devices and continuous product introductions are enhancing treatment accessibility across the region. Hospitals and specialized urology clinics across Western Europe remain key contributors to this growth trend.

U.K. Benign Prostatic Hyperplasia (BPH) Devices Market Insight

The U.K. benign prostatic hyperplasia devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of urological health and increased access to advanced treatment technologies. A growing elderly male population and the National Health Service’s (NHS) focus on minimally invasive therapies are boosting demand for laser-based and PUL systems. For instance, healthcare providers are increasingly adopting UroLift and Rezūm procedures due to shorter recovery times and fewer postoperative complications. Furthermore, investments in hospital infrastructure and ongoing clinical training programs are expected to enhance the U.K.’s adoption of modern BPH treatment solutions.

Germany Benign Prostatic Hyperplasia (BPH) Devices Market Insight

The Germany benign prostatic hyperplasia devices market is expected to expand at a considerable CAGR during the forecast period, supported by the country’s strong focus on technological innovation and advanced urological care. High healthcare standards and early adoption of next-generation laser and minimally invasive devices are key growth drivers. German hospitals are actively integrating HoLEP and photoselective vaporization systems to improve patient outcomes and reduce hospital stays. The nation’s emphasis on precision medicine and digital integration in healthcare is also fostering faster acceptance of newer BPH therapies. Moreover, a well-structured reimbursement environment continues to promote procedural adoption across both public and private healthcare facilities.

Asia-Pacific Benign Prostatic Hyperplasia (BPH) Devices Market Insight

The Asia-Pacific benign prostatic hyperplasia devices market is poised to grow at the fastest CAGR of over 20% during 2025–2032, fueled by rapid urbanization, growing healthcare awareness, and expanding access to urological services. Countries such as China, Japan, and India are witnessing increased adoption of minimally invasive and outpatient-based BPH treatments. Government-led healthcare reforms and private sector investment are strengthening regional infrastructure for advanced urology procedures. Furthermore, the rise of medical tourism and growing local manufacturing of cost-effective BPH devices are enhancing affordability and access. The increasing burden of BPH-related symptoms among aging males further accelerates the regional market’s growth trajectory.

Japan Benign Prostatic Hyperplasia (BPH) Devices Market Insight

The Japan benign prostatic hyperplasia devices market is gaining momentum due to the nation’s aging population, advanced healthcare infrastructure, and strong preference for minimally invasive therapies. Japanese healthcare providers are increasingly adopting laser-based and vapor therapy systems for their precision, safety, and faster recovery benefits. For instance, hospitals are utilizing advanced holmium laser systems for tissue resection with minimal blood loss. The country’s emphasis on technological innovation and early disease management supports the integration of next-generation BPH devices. In addition, favorable government initiatives and an emphasis on outpatient treatment settings are expanding the reach of these therapies nationwide.

India Benign Prostatic Hyperplasia (BPH) Devices Market Insight

The India benign prostatic hyperplasia devices market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding healthcare infrastructure, rising awareness about men’s health, and improving access to specialized urology services. The growing elderly male population and the emergence of affordable, locally produced medical devices are driving the demand for effective BPH treatments. Increasing adoption of laser therapies and minimally invasive systems in private hospitals and specialty clinics is supporting market expansion. In addition, government initiatives aimed at modernizing hospital facilities and promoting medical device innovation are enhancing India’s position as a fast-developing market for BPH treatment devices.

Benign Prostatic Hyperplasia Devices Market Share

The Benign Prostatic Hyperplasia Devices industry is primarily led by well-established companies, including:

- Boston Scientific Corporation (U.S.)

- Teleflex Incorporated (U.S.)

- PROCEPT BioRobotics Corporation (U.S.)

- Olympus Corporation (Japan)

- KARL STORZ SE & Co. KG (Germany)

- Richard Wolf GmbH (Germany)

- Dornier MedTech GmbH (Germany)

- Cook Medical LLC (U.S.)

- Quanta System S.p.A. (Italy)

- biolitec AG (Germany)

- Lumenis Ltd. (Israel)

- Coloplast A/S (Denmark)

- Medtronic (Ireland)

- CONMED Corporation (U.S.)

- Urotronic, Inc. (U.S.)

- Laborie (Canada)

- OmniGuide, Inc. (U.S.)

- ForTec Medical (Italy)

- SonaCare Medical, LLC (U.S.)

- PNN Medical A/S (Denmark)

What are the Recent Developments in Global Benign Prostatic Hyperplasia Devices Market?

- In June 2025, the FDA cleared a 510(k) label expansion for the Rezūm System (water-vapor thermal therapy for BPH), increasing the maximum prostate volume treatable from 80 g to 150 g, thereby broadening the eligible patient population for this outpatient therapy

- In September 2023, the U.S. Food and Drug Administration (FDA) approved the Optilume BPH Catheter System, a drug-coated balloon device for treatment of lower urinary tract symptoms due to BPH, representing a novel non-ablative, minimally invasive treatment option

- In April 2023, Olympus highlighted its minimally invasive BPH portfolio—including the iTind procedure and SOLTIVE SuperPulsed Thulium Fiber Laser—at the American Urological Association (AUA) meeting, emphasizing the shift toward outpatient and non-tissue-removal treatments

- In March 2024, Olympus announced a treatment milestone: its iTind device became available through major group-purchasing organization (GPO) contracts in the U.S., expanding hospital and outpatient access nationwide

- In May 2021, Olympus Corporation completed the acquisition of Israeli medical-device company Medi-Tate, maker of the iTind device for BPH, strengthening its minimally invasive urology portfolio and global market reach

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.