Global Automotive Rain Sensor Market

Market Size in USD Billion

USD

7.14 Billion

USD

12.20 Billion

2024

2032

USD

7.14 Billion

USD

12.20 Billion

2024

2032

| 2025 - 2032 | |

| USD 7.14 Billion | |

| USD 12.20 Billion | |

| % | |

|

Automotive Rain Sensor Market Size

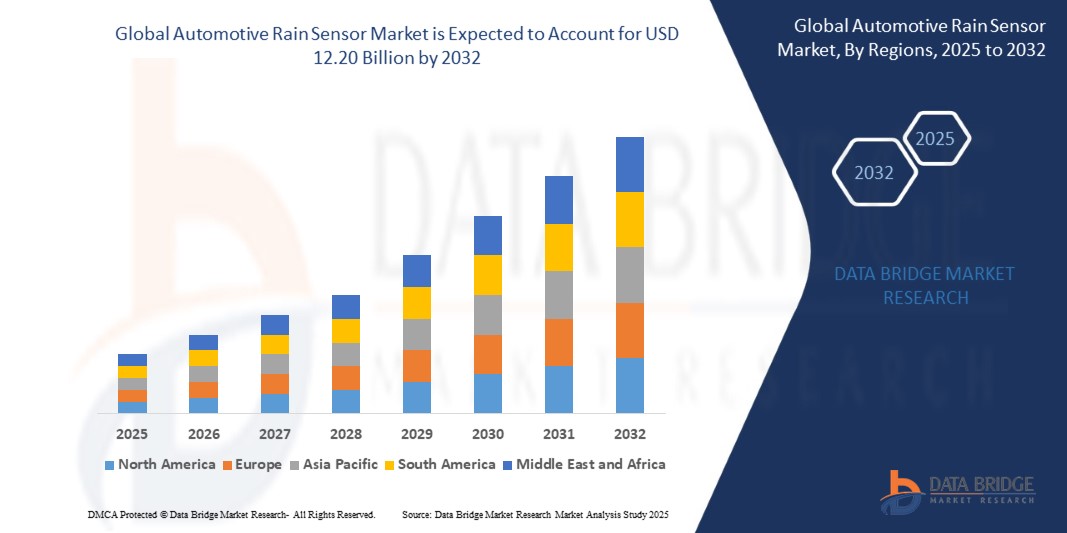

- The global Automotive Rain Sensor market size was valued at USD 7.14 billion in 2024 and is expected to reach USD 12.20 billion by 2032, at a CAGR of 6.93% during the forecast period

- The strong market growth is primarily driven by the increasing integration of advanced driver assistance systems (ADAS) and smart sensor technologies in modern vehicles. Automotive rain sensors, which automatically activate windshield wipers based on precipitation levels, are becoming a standard feature in mid- and high-end vehicle models due to enhanced driver safety and convenience.

- The market expansion is also supported by the global rise in vehicle production, especially in regions such as Asia-Pacific and North America, along with stringent automotive safety regulations pushing OEMs to incorporate automated functionalities.

Automotive Rain Sensor Market Analysis

- Automotive Rain Sensors, which detect precipitation on the windshield and automatically activate wiper systems, are increasingly integrated into modern vehicles to improve driver safety, comfort, and system automation. These sensors are vital components of Advanced Driver Assistance Systems (ADAS), contributing to safer and smarter driving experiences.

- The rising demand for vehicle automation and driver convenience technologies is a major driver of rain sensor adoption across both passenger and commercial vehicles. As automakers move toward semi-autonomous and fully autonomous driving, environmental sensing systems like rain sensors become critical.

- The global automotive industry's shift toward smart, connected vehicles is fueling adoption of sensors that support autonomous functions. Rain sensors, when integrated with windshield defogging systems, headlight automation, and ADAS modules, provide real-time response to changing environmental conditions.

- North America dominates the Automotive Rain Sensor market with the largest revenue share of 36.2% in 2024, driven by high vehicle production rates, advanced automotive R&D infrastructure, and strong consumer demand for premium vehicles with integrated safety and comfort features. U.S. automotive OEMs and Tier-1 suppliers are increasingly standardizing rain sensors in mid- to high-end vehicles.

- Asia-Pacific is projected to be the fastest-growing region during the forecast period, fueled by rapid vehicle manufacturing expansion in China, India, South Korea, and Japan, and the growing affordability of smart automotive components. Government policies supporting vehicle safety, along with rising consumer awareness of in-car tech, are accelerating regional market penetration.

- The Passenger Vehicle segment holds the dominant market share for Automotive Rain Sensors in 2024, as OEMs equip sedans, SUVs, and electric vehicles with rain-sensing wipers to enhance appeal and regulatory compliance. Meanwhile, commercial vehicles, particularly in fleet and logistics operations, are beginning to adopt such technologies for improved visibility and operational safety.

Report Scope and Automotive Rain Sensor Market Segmentation

|

Attributes |

Automotive Rain Sensor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Automotive Rain Sensor Market Trends

“Integration of Rain Sensors with ADAS and Autonomous Driving Technologies”

- A key trend in the global Automotive Rain Sensor market is the growing integration of rain-sensing technologies with ADAS (Advanced Driver Assistance Systems) to support semi-autonomous and autonomous vehicle functionalities. These systems help adjust vehicle responses in real-time based on weather conditions, enhancing driver safety and vehicle intelligence.

- For instance, in May 2023, Valeo launched an advanced rain and light sensor with enhanced sensitivity and integration capabilities tailored for electric vehicles and autonomous platforms. This innovation allows the system to respond to micro-climate variations, improving wiper accuracy and driver visibility.

- In March 2023, Denso Corporation announced that its next-generation ADAS sensor suite would include upgraded rain sensor modules optimized for integration with vehicle control units and optical lane-detection systems.

- Automakers such as BMW and Mercedes-Benz have increasingly standardized rain-sensing wipers in their latest models to comply with Euro NCAP safety standards and enhance consumer convenience.

- The growing demand for premium comfort features and intelligent environmental response systems is pushing OEMs to incorporate rain sensors not just in high-end models but also in mid-range and compact vehicles.

Automotive Rain Sensor Market Dynamics

Driver

“Rising Demand for Safety and Comfort Features in Passenger Vehicles”

- The demand for automated safety and comfort solutions in passenger vehicles is a major growth driver for the Automotive Rain Sensor market. Consumers increasingly expect advanced features such as automatic windshield wipers, headlamp activation, and climate-sensitive driving assistance.

- In February 2024, Continental AG announced mass production of a new generation of multifunctional sensors that combine rain detection with solar light monitoring and cabin climate control, aimed at reducing energy consumption in electric vehicles.

- The push toward vehicle electrification and automation is further boosting rain sensor adoption. For example, Tesla enhanced its camera-based "Deep Rain" algorithm in 2023, improving the accuracy of automatic wiper systems based on real-time weather detection and machine learning.

- Government regulations and safety standards in Europe, North America, and parts of Asia are also pushing automakers to integrate rain sensors as part of the standard feature set in new vehicles

Restraint/Challenge

“High Cost and Limited Adoption in Entry-Level Vehicles”

- A significant challenge for the Automotive Rain Sensor market is the relatively high cost of integration, which limits adoption in budget and entry-level vehicle segments, particularly in emerging economies.

- In October 2023, a study by IHS Markit noted that while over 75% of premium vehicles include rain sensors as standard, less than 30% of economy-class vehicles have them, due to pricing sensitivity and lower customer expectations in that segment.

- The high cost of optical sensing components, coupled with the need for integration with vehicle control modules, adds to manufacturing expenses, deterring widespread inclusion in lower-tier models.

- Additionally, aftermarket installations of rain sensors face challenges in compatibility, reliability, and serviceability, further restricting market expansion outside OEM-installed systems.

- To address this, companies like Hella and Mitsuba are working on cost-optimized rain sensor designs and multi-functional sensor units aimed at reducing per-unit costs and improving ease of integration for budget vehicles.

Automotive Rain Sensor Market Scope

The market is segmented on the basis of vehicle type, sales channel, sensitivity, and operation mode.

- By Vehicle Type

On the basis of vehicle type, the Automotive Rain Sensor market is segmented into Passenger Cars, Light Commercial Vehicles (LCVs), and Heavy Commercial Vehicles (HCVs).

The Passenger Cars segment accounted for the largest market share in 2024, driven by rising consumer demand for enhanced safety and comfort features such as automatic wipers and intelligent lighting. Major automakers like BMW, Hyundai, and Toyota continue to standardize rain sensors in premium and mid-range models, contributing to widespread adoption.

The Light Commercial Vehicles segment is expected to register the fastest growth during the forecast period, as fleet operators increasingly adopt rain-sensing technologies to improve driver visibility, reduce accident risk, and comply with evolving vehicle safety regulations. For instance, Ford Transit and Mercedes-Benz Sprinter models now offer rain-sensing wipers as standard or optional features in several markets.

- By Sales Channel

On the basis of sales channel, the market is segmented into Original Equipment Manufacturer (OEM) and Aftermarket.

The OEM segment dominated the market in 2024, accounting for the majority revenue share. Automakers are integrating rain sensors into new vehicle models as part of broader advanced driver assistance systems (ADAS) packages. For example, in late 2023, Volkswagen Group began integrating rain sensors into its next-generation MQB platform across multiple brands.

The Aftermarket segment is gaining traction, particularly in emerging economies where consumers retrofit rain sensors into older vehicles. Companies such as Valeo Service and Hella offer plug-and-play aftermarket rain sensor kits tailored for regional vehicle models, especially in Southeast Asia and Latin America.

- By Sensitivity

On the basis of sensitivity, the market is segmented into High, Medium, and Low.

The High Sensitivity segment held the largest share in 2024, as these sensors are preferred in luxury vehicles and EVs for their precision in detecting minute levels of moisture and rapidly adjusting wiper speed. In January 2024, Bosch introduced an advanced high-sensitivity sensor module aimed at next-generation EVs and autonomous vehicles.

The Medium Sensitivity segment is projected to experience steady growth, as it is widely used in mid-range vehicles, balancing performance and cost-efficiency.

The Low Sensitivity segment continues to serve entry-level vehicles where basic automatic functionality is prioritized over adaptive precision.

- By Operation Mode

On the basis of operation mode, the Automotive Rain Sensor market is segmented into Automatic and Manual.

The Automatic segment dominated the market in 2024 and is projected to witness the highest growth rate. This growth is driven by increasing consumer preference for convenience, along with safety regulations pushing OEMs to implement automated visibility systems. In October 2023, Hyundai launched a new SUV model equipped with a fully automatic rain sensor system that also integrates with adaptive lighting features.

The Manual segment is expected to grow at a slower pace, primarily catering to aftermarket users and low-cost vehicle categories where end-users prefer basic, user-controlled functionality.

Automotive Rain Sensor Market Regional Analysis

North America holds the largest revenue share of 34.7% in the global Automotive Rain Sensor market in 2024, owing to the high penetration of ADAS technologies, robust automotive manufacturing, and favorable government regulations promoting vehicle safety features. Automakers in the region are aggressively adopting rain sensor systems in both luxury and mass-market models as part of safety enhancements.

Ongoing R&D in sensor sensitivity and integrated electronics by regional players like Sensata Technologies, ZF Friedrichshafen, and TRW Automotive is contributing to market growth. Additionally, consumer preference for smart, connected vehicles is boosting demand for intelligent features such as automatic wipers enabled by rain sensors.

U.S. Automotive Rain Sensor Market Insight

The U.S. dominates the North American market, accounting for approximately 81% share in 2024, supported by the strong presence of Tier 1 suppliers and OEMs. Automakers such as Ford, GM, and Tesla have incorporated rain sensors as standard or optional features in multiple vehicle models. In March 2024, Ford announced the inclusion of a next-gen optical rain sensor module in its 2025 SUV lineup, reflecting rising OEM focus on smart safety systems.

The growing electric vehicle (EV) market and autonomous driving initiatives are further reinforcing demand for weather-adaptive technologies.

Europe Automotive Rain Sensor Market Insight

Europe is the second-largest market and is projected to expand at a healthy CAGR, driven by stringent EU safety regulations (e.g., GSR2 – General Safety Regulation), which mandate several ADAS components in vehicles including rain sensors.

Leading automotive hubs such as Germany, France, and the U.K. are actively deploying smart sensor technologies to comply with these norms. Companies like Bosch, Valeo, and HELLA are at the forefront of innovation in integrated sensor modules.

Germany Automotive Rain Sensor Market Insight

Germany’s dominance in automotive R&D and manufacturing makes it a key contributor to the European market. The country's premium carmakers—BMW, Audi, and Mercedes-Benz—are equipping most new vehicles with high-sensitivity rain sensors. Moreover, government emphasis on road safety and automation is accelerating integration of such features across model ranges. In February 2024, Bosch launched its new all-weather optical sensor system tailored for EVs in the German market.

U.K. Automotive Rain Sensor Market Insight

The U.K. market is witnessing steady growth as ADAS adoption becomes more common even in compact vehicle segments. Domestic demand is supported by road safety campaigns and regulatory push for autonomous readiness. In 2023, Jaguar Land Rover partnered with Valeo to introduce adaptive rain sensors with glare detection technology in its Range Rover lineup.

Asia-Pacific Automotive Rain Sensor Market Insight

The Asia-Pacific Automotive Rain Sensor market is anticipated to register the fastest CAGR of 9.6% from 2025 to 2032, fueled by rapid vehicle production, increasing demand for passenger vehicles, and growing focus on smart driving features. Major automotive economies like China, Japan, India, and South Korea are witnessing a surge in adoption of rain sensors due to rising consumer safety awareness and expanding middle-class demographics.

Local OEMs are partnering with global suppliers to integrate advanced sensor technologies at scale and affordable cost.

China Automotive Rain Sensor Market Insight

China captured the largest market share in Asia-Pacific in 2024, driven by its massive auto production base and government push for intelligent and connected vehicles. Local manufacturers like BYD and Geely are incorporating rain sensors in electric vehicles to meet consumer expectations. In January 2024, DJI Automotive launched its optical sensor suite, including rain detection, for integration into domestic EVs, enhancing the country’s sensor tech ecosystem.

Japan Automotive Rain Sensor Market Insight

Japan's market is mature and innovation-driven, with a focus on enhancing driving comfort and automation. Key automakers such as Toyota and Honda have been early adopters of rain-sensing technology. The country's aging population is also encouraging the deployment of advanced driver assistance features that rely on sensors for weather adaptability. In April 2024, Denso Corporation unveiled a high-resolution rain sensor designed for hybrid and plug-in hybrid models.

Automotive Rain Sensor Market Share

The Automotive Rain Sensor industry is primarily led by well-established companies, including:

- HELLA GmbH & Co. KGaA (Germany)

- Valeo SA (France)

- Denso Corporation (Japan)

- Robert Bosch GmbH (Germany)

- ZF Friedrichshafen AG (Germany)

- Vishay Intertechnology, Inc. (U.S.)

- Hamamatsu Photonics K.K. (Japan)

- Melexis Microelectronic Systems (Belgium)

- Mitsubishi Motors Corporation (Japan)

- ams-OSRAM International GmbH (Austria)

Latest Developments in Global Automotive Rain Sensor Market

- In February 2024, Nearmap, a leading provider of aerial imagery and location intelligence, announced the expansion of its AI-powered aerial imagery services to additional metropolitan areas across the United States and Australia. This expansion aims to support sectors like insurance, urban planning, and construction by offering more granular, high-resolution visual data—thereby reinforcing Nearmap’s leadership in integrated Automotive Rain Sensor solutions.

- In January 2024, EagleView Technologies launched its next-generation EagleView Cloud platform, combining ultra-high-resolution aerial imagery with real-time geospatial analytics. This development marks a significant leap in rain sensor-enabled data platforms, offering improved decision-making for verticals such as public safety, disaster response, and asset management.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.