Global Automotive Labels Market

Market Size in USD Billion

USD

9.17 Billion

USD

13.24 Billion

2025

2033

USD

9.17 Billion

USD

13.24 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.17 Billion | |

| USD 13.24 Billion | |

| % | |

|

Automotive Labels Market Size

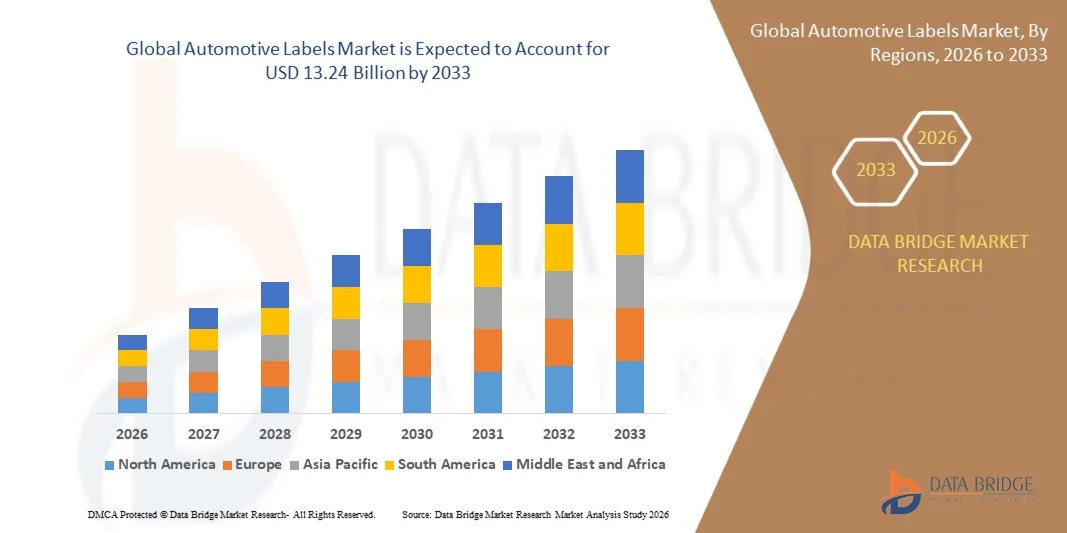

- The global automotive labels market size was valued at USD 9.17 billion in 2025and is expected to reach USD 13.24 billion by 2033, at a CAGR of 4.70% during the forecast period

- The market growth is largely fuelled by the increasing demand for vehicle identification, safety compliance, and regulatory labeling requirements across the automotive industry

- Rising production of passenger and commercial vehicles along with growing adoption of advanced labeling technologies such as RFID and barcode labels is further driving market expansion

Automotive Labels Market Analysis

- The market is witnessing steady growth due to the rising need for high-performance labels that can withstand extreme temperatures, chemicals, and environmental conditions in automotive applications

- Increasing integration of smart labeling technologies and emphasis on supply chain transparency are further supporting the adoption of advanced automotive labeling solutions

- North America dominated the automotive labels market with the largest revenue share in 2025, driven by the strong presence of leading automotive manufacturers and increasing demand for advanced labeling solutions for safety and compliance.

- Asia-Pacific region is expected to witness the highest growth rate in the global automotive labels market, driven by rapid industrialization, increasing disposable incomes, and expanding automotive production in countries such as China, India, and Japan. The region is also benefiting from growing investments in manufacturing infrastructure and rising demand for advanced automotive components

- The warning and safety labels segment held the largest market revenue share in 2025 driven by stringent government regulations and increasing emphasis on vehicle safety and compliance standards. These labels play a critical role in providing essential information related to hazards, operational guidelines, and regulatory requirements, thereby ensuring consumer safety and adherence to legal norms across global automotive markets. In addition, the rising complexity of modern vehicles, including electric and hybrid systems, has increased the need for clear and durable warning labels. Manufacturers are also focusing on high-performance materials that can withstand extreme temperatures and exposure to chemicals. The integration of multilingual labels for global vehicle distribution further strengthens the demand in this segment

Report Scope and Automotive Labels Market Segmentation

|

Attributes |

Automotive Labels Key Market Insights |

|

Segments Covered |

· By Type: Warning and Safety Labels, Asset Labels, Branding, Dome and Other Labels · By Raw Material: Polypropylene, Polyethylene, Terephthalate, Polyvinyl Chloride, Polycarbonate and Others · By Identification Technology (Barcode, RFID and Others · By Printing Technology: Flexography, Offset, Digital Printing, Screen Printing and Others · By Mechanism: Pressure Sensitive, Heat Transfer and Others · By Vehicle Type: Passenger Car and Commercial Vehicle |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• 3M Company (U.S.) |

|

Market Opportunities |

• Increasing Adoption Of Smart And RFID-Based Labeling Technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Automotive Labels Market Trends

“Rising Demand for Durable and Regulatory-Compliant Labeling Solutions”

- The increasing emphasis on vehicle safety, regulatory compliance, and traceability is significantly shaping the automotive labels market, as manufacturers require high-performance labeling solutions that can withstand extreme environmental conditions. Automotive labels are gaining traction due to their ability to provide critical information such as safety warnings, identification codes, and tracking details without compromising durability and readability. This trend is strengthening their adoption across passenger vehicles, commercial vehicles, and industrial automotive components, encouraging manufacturers to develop advanced labeling technologies

- Increasing awareness regarding vehicle safety standards and regulatory requirements has accelerated the demand for automotive labels across various applications such as engine components, interiors, and electrical systems. Automotive manufacturers are actively integrating high-quality labels that offer resistance to heat, chemicals, and abrasion, ensuring long-term performance and compliance. This has also led to collaborations between label manufacturers and automotive OEMs to enhance product functionality and reliability

- Compliance and traceability trends are influencing purchasing decisions, with manufacturers emphasizing high-durability materials, adhesive strength, and advanced printing technologies. These factors are helping companies differentiate their offerings in a competitive market and ensure product authenticity, while also driving the adoption of barcode, QR code, and RFID-enabled labels. Companies are increasingly focusing on innovation to meet evolving regulatory and operational requirements

- For instance, in 2024, companies such as 3M and Avery Dennison expanded their automotive label portfolios by introducing high-performance labels designed for extreme conditions and enhanced traceability. These products were developed in response to growing regulatory requirements and increasing demand for durable labeling solutions, with applications across vehicle manufacturing and aftermarket services. The labels were also marketed for their long lifespan and reliability, improving customer satisfaction and operational efficiency

- While demand for automotive labels is increasing, sustained market growth depends on continuous innovation, cost-effective production, and maintaining performance under harsh operating conditions. Manufacturers are also focusing on improving material efficiency, adhesive performance, and developing smart labeling solutions that balance durability, cost, and functionality for broader adoption

Automotive Labels Market Dynamics

Driver

“Increasing Regulatory Compliance and Vehicle Safety Requirements”

- Rising regulatory mandates for vehicle identification, safety warnings, and emissions labeling are a major driver for the automotive labels market. Manufacturers are increasingly adopting advanced labeling solutions to ensure compliance with global standards, improve product traceability, and enhance consumer safety. This trend is also encouraging the development of labels with improved resistance to environmental stress and longer service life

- Expanding automotive production and growing complexity of vehicle components are influencing market growth. Automotive labels play a critical role in providing essential information and ensuring proper functioning of various systems, enabling manufacturers to meet regulatory and operational requirements. The increasing adoption of electric and connected vehicles further reinforces the demand for advanced labeling solutions

- Automotive OEMs and label manufacturers are actively promoting innovative labeling technologies through product development, partnerships, and integration of smart features such as RFID and QR codes. These efforts are supported by the growing demand for efficient supply chain management and real-time tracking, encouraging collaboration across the value chain to improve performance and reduce operational risks

- For instance, in 2023, companies such as CCL Industries and UPM Raflatac reported increased deployment of high-performance automotive labels in vehicle manufacturing and supply chain operations. This expansion followed rising regulatory compliance requirements and demand for enhanced traceability, driving product differentiation and operational efficiency. Both companies also emphasized sustainability and recyclability in their labeling solutions to strengthen market positioning

- Although regulatory and safety requirements support growth, wider adoption depends on cost optimization, material innovation, and scalability of production processes. Investment in advanced printing technologies, durable materials, and efficient supply chain management will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

“High Cost of Advanced Label Materials and Performance Limitations”

- The relatively high cost of advanced automotive labels compared to conventional labeling solutions remains a key challenge, limiting adoption among cost-sensitive manufacturers. High-performance materials and specialized adhesives contribute to increased production costs. In addition, fluctuating raw material prices can further impact cost stability and market penetration

- Manufacturer awareness and adoption vary across regions, particularly in developing markets where regulatory enforcement may be less stringent. Limited understanding of the benefits of high-performance labels can restrict adoption in certain applications, leading to slower market growth in price-sensitive segments

- Supply chain and material challenges also impact market growth, as automotive labels require consistent quality, durability, and compliance with strict standards. Variability in material availability and performance under extreme conditions can increase operational complexities. Companies must invest in advanced materials, testing processes, and efficient distribution networks to ensure product reliability

- For instance, in 2024, suppliers working with automotive brands such as Bosch and Continental reported challenges related to rising material costs and maintaining label performance in high-temperature and chemical-exposed environments. These issues affected production efficiency and increased overall costs, prompting manufacturers to explore alternative materials and improved adhesive technologies

- Overcoming these challenges will require cost-efficient production, material innovation, and enhanced awareness among manufacturers. Collaboration with automotive OEMs, suppliers, and regulatory bodies can help unlock long-term growth potential in the automotive labels market. Furthermore, developing durable, cost-effective, and sustainable labeling solutions will be essential for widespread adoption

Automotive Labels Market Scope

The market is segmented on the basis of type, raw material, identification technology, printing technology, mechanism, and vehicle type.

- By Type

On the basis of type, the global automotive labels market is segmented into warning and safety labels, asset labels, branding, dome, and other labels. The warning and safety labels segment held the largest market revenue share in 2025 driven by stringent government regulations and increasing emphasis on vehicle safety and compliance standards. These labels play a critical role in providing essential information related to hazards, operational guidelines, and regulatory requirements, thereby ensuring consumer safety and adherence to legal norms across global automotive markets. In addition, the rising complexity of modern vehicles, including electric and hybrid systems, has increased the need for clear and durable warning labels. Manufacturers are also focusing on high-performance materials that can withstand extreme temperatures and exposure to chemicals. The integration of multilingual labels for global vehicle distribution further strengthens the demand in this segment.

The branding segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising focus of automotive manufacturers on brand differentiation and aesthetic appeal. Branding labels enhance vehicle identity and visual appeal through high-quality graphics and durable materials, making them an integral part of vehicle design and marketing strategies. In addition, increasing consumer preference for premium and customized vehicles is encouraging automakers to invest in visually appealing labels. Technological advancements in printing techniques are enabling intricate designs and long-lasting finishes. The use of eco-friendly inks and materials is also gaining traction in branding applications.

- By Raw Material

On the basis of raw material, the global automotive labels market is segmented into polypropylene, polyethylene, terephthalate, polyvinyl chloride, polycarbonate, and others. The polypropylene segment held the largest market revenue share in 2025 driven by its cost-effectiveness, flexibility, and excellent resistance to chemicals and moisture. It is widely used in automotive labeling applications due to its durability and ability to withstand harsh environmental conditions such as temperature fluctuations and exposure to automotive fluids. In addition, polypropylene offers excellent printability, making it suitable for high-quality labeling requirements. Its lightweight nature also supports overall vehicle weight reduction initiatives. The material’s recyclability aligns with the growing focus on sustainable automotive manufacturing.

The polycarbonate segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its superior strength, heat resistance, and long-term durability. Polycarbonate-based labels are increasingly preferred in high-performance applications where labels must endure extreme conditions without degradation. In addition, these labels provide excellent resistance to UV radiation and mechanical wear, ensuring long-term readability. The increasing adoption of electric vehicles is further boosting demand for high-performance materials such as polycarbonate. Manufacturers are also focusing on developing advanced coatings to enhance the lifespan of these labels.

- By Identification Technology

On the basis of identification technology, the global automotive labels market is segmented into barcode, RFID, and others. The barcode segment held the largest market revenue share in 2025 driven by its widespread adoption, low implementation cost, and ease of integration across automotive manufacturing and supply chain operations. Barcode labels enable efficient tracking, inventory management, and product identification, making them a standard solution in the industry. In addition, their compatibility with existing infrastructure ensures seamless deployment across facilities. The simplicity and reliability of barcode systems continue to support their dominance in the market. They are also widely used in aftermarket services and spare parts management.

The RFID segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for advanced tracking and real-time data monitoring capabilities. RFID technology enhances supply chain visibility, improves operational efficiency, and supports automation in automotive manufacturing processes. In addition, RFID labels enable contactless data transfer and can store larger amounts of information compared to barcodes. The growing trend toward Industry 4.0 and smart manufacturing is accelerating RFID adoption. These labels are also beneficial for theft prevention and asset tracking in high-value automotive components.

- By Printing Technology

On the basis of printing technology, the global automotive labels market is segmented into flexography, offset, digital printing, screen printing, and others. The flexography segment held the largest market revenue share in 2025 driven by its high-speed production capabilities and cost efficiency for large-scale label manufacturing. It is widely used for producing durable labels with consistent quality across high-volume automotive applications. In addition, flexographic printing supports a wide range of substrates and inks, enhancing its versatility. The technology is well-suited for long production runs with minimal variation. Continuous advancements in flexographic equipment are further improving print quality and efficiency.

The digital printing segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the growing need for customization, shorter production runs, and quick turnaround times. Digital printing enables high-resolution graphics and variable data printing, making it ideal for modern automotive labeling requirements. In addition, it reduces material waste and setup time compared to conventional printing methods. The technology allows manufacturers to respond quickly to design changes and regulatory updates. Increasing adoption of smart labels is also supporting the growth of digital printing solutions.

- By Mechanism

On the basis of mechanism, the global automotive labels market is segmented into pressure sensitive, heat transfer, and others. The pressure sensitive segment held the largest market revenue share in 2025 driven by its ease of application and strong adhesive properties that ensure durability under varying environmental conditions. These labels are widely used across automotive components due to their versatility and reliability. In addition, they do not require heat, water, or solvents for application, simplifying the labeling process. Their compatibility with different surfaces makes them suitable for a wide range of automotive parts. Ongoing innovations in adhesive technologies are enhancing their performance.

The heat transfer segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its ability to produce highly durable and long-lasting labels that can withstand extreme temperatures and abrasion. Heat transfer labels are increasingly used in applications requiring permanent marking and resistance to harsh conditions. In addition, these labels offer excellent print clarity and resistance to fading over time. They are particularly suitable for engine components and under-the-hood applications. Growing demand for high-durability labeling solutions is driving adoption in this segment.

- By Vehicle Type

On the basis of vehicle type, the global automotive labels market is segmented into passenger car and commercial vehicle. The passenger car segment held the largest market revenue share in 2025 driven by the high production volume of passenger vehicles and increasing consumer demand for advanced labeling solutions for safety, branding, and regulatory compliance. The growing adoption of electric and connected vehicles further supports the demand for automotive labels in this segment. In addition, rising disposable incomes and urbanization are contributing to increased passenger vehicle sales globally. Automakers are also incorporating advanced labeling solutions for enhanced user experience.

The commercial vehicle segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the expansion of logistics, transportation, and e-commerce industries. The need for durable and high-performance labeling solutions in heavy-duty vehicles is increasing, supporting the growth of this segment. In addition, fleet operators are focusing on efficient asset tracking and maintenance, boosting demand for advanced labels. The growth of cross-border trade and infrastructure development is further driving commercial vehicle production. Increasing regulatory requirements for safety and tracking also contribute to segment growth.

Automotive Labels Market Regional Analysis

- North America dominated the automotive labels market with the largest revenue share in 2025, driven by the strong presence of leading automotive manufacturers and increasing demand for advanced labeling solutions for safety and compliance.

- Consumers and manufacturers in the region place high importance on regulatory compliance, durability, and performance of labels, particularly for applications exposed to harsh environmental conditions such as heat, chemicals, and abrasion.

- This widespread adoption is further supported by technological advancements in printing and material science, along with high vehicle production and growing demand for electric vehicles, establishing automotive labels as a critical component across vehicle manufacturing and aftermarket applications.

U.S. Automotive Labels Market Insight

The U.S. automotive labels market captured the largest revenue share in 2025 within North America, fueled by strong automotive production and the increasing adoption of advanced labeling technologies. Manufacturers are focusing on high-performance labels that ensure durability, traceability, and compliance with stringent safety regulations. The growing demand for electric and connected vehicles is further driving the need for specialized labels. In addition, the presence of major automotive OEMs and technological innovation in printing solutions is significantly contributing to market growth.

Europe Automotive Labels Market Insight

The Europe automotive labels market is expected to witness steady growth from 2026 to 2033, primarily driven by stringent regulatory standards related to vehicle safety, emissions, and product traceability. The increasing focus on sustainability and the use of eco-friendly materials in labeling solutions are fostering market expansion. In addition, the rise in electric vehicle adoption and advanced manufacturing practices is supporting demand. The region continues to experience consistent growth across passenger and commercial vehicle segments.

U.K. Automotive Labels Market Insight

The U.K. automotive labels market is expected to witness notable growth from 2026 to 2033, driven by the increasing demand for high-quality and durable labeling solutions in both domestic manufacturing and imports. In addition, the rising focus on compliance with safety standards and product identification is boosting the adoption of automotive labels. The growth of electric vehicles and aftermarket services is further contributing to market expansion. The presence of advanced printing technologies and strong distribution networks also supports industry growth.

Germany Automotive Labels Market Insight

The Germany automotive labels market is expected to witness strong growth from 2026 to 2033, fueled by the country’s well-established automotive industry and focus on engineering excellence. The demand for durable, high-performance labels that can withstand extreme conditions is significantly increasing. In addition, Germany’s emphasis on sustainability and innovation is encouraging the use of advanced materials and eco-friendly labeling solutions. The integration of smart manufacturing and Industry 4.0 practices is also contributing to market expansion.

Asia-Pacific Automotive Labels Market Insight

The Asia-Pacific automotive labels market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, increasing vehicle production, and rising disposable incomes in countries such as China, India, and Japan. The growing adoption of electric vehicles and expansion of automotive manufacturing facilities are further supporting market growth. In addition, favorable government policies and increasing investments in infrastructure are boosting demand for automotive components, including labels. The region is also emerging as a key manufacturing hub, improving accessibility and affordability of labeling solutions.

Japan Automotive Labels Market Insight

The Japan automotive labels market is expected to witness significant growth from 2026 to 2033 due to the country’s advanced automotive technologies and strong focus on quality and precision. The demand for high-performance labels that meet strict safety and durability standards is increasing. In addition, the integration of smart technologies and automation in vehicle manufacturing is driving the adoption of advanced labeling solutions. The growing focus on electric and hybrid vehicles is further contributing to market development.

China Automotive Labels Market Insight

The China automotive labels market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s massive automotive production capacity and rapid technological advancements. The increasing demand for cost-effective and durable labeling solutions is driving market growth. In addition, the expansion of electric vehicle production and strong presence of domestic manufacturers are key factors supporting the market. Government initiatives promoting smart manufacturing and industrial growth are further accelerating the adoption of automotive labels across various applications.

Automotive Labels Market Share

The Automotive Labels industry is primarily led by well-established companies, including:

- 3M Company (U.S.)

- Avery Dennison Corporation (U.S.)

- CCL Industries (Canada)

- UPM (Finland)

- Sika AG (Switzerland)

- Dunmore (U.S.)

- ImageTek Labels (U.S.)

- Lintec Corporation (Japan)

- tesa Tapes (India) Private Limited (India)

- Labels & Labeling (U.K.)

- Seiko Holdings Corporation (Japan)

- Honeywell International Inc. (U.S.)

- Polylabel (U.S.)

- Intertronics (U.K.)

- OpSec Security (U.K.)

- H.B. Fuller Company (U.S.)

- FLEXcon Company Inc. (U.S.)

- Bemis Manufacturing Company (U.S.)

- Adhesive Research (U.S.)

- Brady Worldwide Inc. (U.S.)

- Resource Label Group (U.S.)

Latest Developments in Global Automotive Labels Market

- In July 2024, AWT Labels & Packaging Inc., acquisition, announced the acquisition of American Label Technologies to expand its capabilities in RFID and NFC printing technologies across healthcare, retail, warehousing, and automotive sectors, enhancing its product portfolio and strengthening its presence in North America. This development enables AWT to integrate advanced smart labeling solutions into its offerings, improving traceability and real-time tracking capabilities. In addition, the acquisition supports the company’s strategy to cater to high-growth sectors requiring intelligent labeling systems. The continued operation of ALT under AWT ensures business continuity and customer retention. This move is expected to accelerate innovation and increase competitiveness in the automotive labels market

- In April 2023, Cognosos, product launch, unveiled the RT-270 FVL tags equipped with 900MHz wireless networking, Bluetooth (BLE) connectivity, and LED features to enhance usability, aimed at improving efficiency, productivity, and safety in automotive logistics operations. These advanced tags enable better visibility of finished vehicle movement across supply chains. In addition, the integration of multiple connectivity technologies enhances flexibility in deployment across different environments. The LED feature improves operational efficiency by simplifying tag identification in large facilities. This innovation is expected to streamline automotive logistics and reduce operational bottlenecks

- In January 2023, Avery Dennison Corporation, expansion, announced an investment of over USD 100 million to build a new manufacturing facility in Queretaro, Mexico, to expand RFID production capacity and strengthen its position as a leading provider of digital identification solutions. This expansion aligns with the company’s vision of assigning a unique digital ID to every product. In addition, the new facility enhances regional supply capabilities and reduces dependency on imports. The investment also supports advancements in connected packaging and smart labeling technologies. This initiative is expected to drive efficiency, transparency, and scalability across automotive and broader industrial supply chains

- In March 2022, Brady Corporation, partnership, entered into a collaboration with HSI to deliver integrated safety management solutions and labeling systems, enabling companies to enhance compliance and workplace safety. This partnership allows Brady to leverage advanced EHS and training technologies to strengthen its service offerings. In addition, the integration of labeling systems with safety management platforms improves operational efficiency and risk mitigation. The collaboration also supports customization of safety solutions for different industrial requirements. This is expected to boost adoption of advanced labeling solutions in automotive and manufacturing sectors

- In January 2022, Resource Label Group, LLC, acquisition, acquired QSX Labels to strengthen its regional presence in New England and expand its labeling solutions portfolio. This acquisition enhances the company’s ability to deliver customized labeling solutions across various industries, including automotive. In addition, it supports increased production capacity and faster turnaround times for customers. The move also strengthens Resource Label Group’s competitive positioning in the U.S. labeling market. This strategic expansion is expected to contribute to market consolidation and improved service capabilities

- In October 2021, Armor Group, acquisition, acquired International Imaging Materials (IIMAK) to reinforce its global leadership in thermal transfer ribbon production. This acquisition enhances Armor’s technological expertise and broadens its product offerings in high-performance labeling solutions. In addition, it strengthens the company’s global distribution network and customer base. The combined capabilities enable the development of more durable and efficient labeling products. This move is expected to support innovation and improve supply chain efficiency within the automotive labels market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Automotive Labels Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Automotive Labels Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Automotive Labels Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.