Global Auto Injectors Market

Market Size in USD Billion

CAGR :

%

USD

101.13 Billion

USD

488.88 Billion

2024

2032

USD

101.13 Billion

USD

488.88 Billion

2024

2032

| 2025 –2032 | |

| USD 101.13 Billion | |

| USD 488.88 Billion | |

| % | |

|

Auto Injectors Market Size

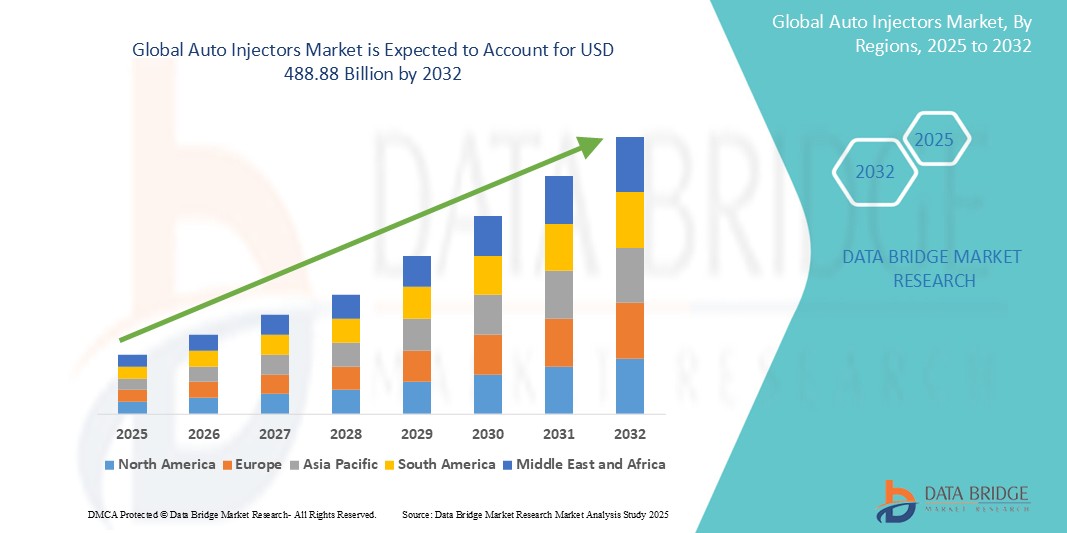

- The global auto injectors market size was valued at USD 101.13 billion in 2024 and is expected to reach USD 488.88 billion by 2032, at a CAGR of 21.77% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases requiring self-administration of medication, the growing aging population, and technological advancements in device design and functionality, leading to enhanced patient convenience and adherence in both hospital and home settings

- Furthermore, rising demand for user-friendly drug delivery systems, coupled with the need for effective and safe medication administration during critical care and emergencies, is establishing auto injectors as essential tools for both patients and healthcare professionals. These converging factors are accelerating the uptake of auto injectors solutions, thereby significantly boosting the industry's growth

Auto Injectors Market Analysis

- Auto injectors, providing essential tools for self-administering medication during medical conditions and emergencies, are increasingly critical components of modern healthcare settings, including hospitals, emergency medical services, and home healthcare, due to their vital role in ensuring patient safety and effective drug delivery

- The escalating demand for auto injectors is primarily fueled by the growing prevalence of chronic diseases requiring frequent injections, the increasing number of biologics and biosimilars available in pre-filled syringes, and the rising need for user-friendly drug delivery in emergency situations

- North America dominates the auto injectors market with the largest revenue share of 49.7% in 2024, characterized by advanced healthcare infrastructure, high adoption rates of sophisticated medical devices, and a strong presence of leading pharmaceutical and medical device manufacturers, with the U.S. experiencing substantial growth in the utilization of auto injectors across various healthcare settings

- Asia-Pacific is expected to be the fastest-growing region in the auto injectors market during the forecast period, with an anticipated CAGR of 8.9% due to increasing healthcare expenditure, a growing aging population susceptible to chronic diseases, and rising awareness of self-administration techniques in rapidly developing healthcare systems

- The disposable auto injectors segment dominates auto injectors market with the largest market revenue share of 35.6% in 2024, driven by continuous innovations that improve the safety and convenience of using these devices

Report Scope and Auto Injectors Market Segmentation

|

Attributes |

Auto Injectors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Auto Injectors Market Trends

“Enhanced Convenience Through AI and Voice Integration”

- A significant and accelerating trend in the global auto injectors market is the deepening integration with artificial intelligence (AI) and the incorporation of features that enhance user experience, such as audio-visual cues and potentially voice guidance. This fusion of technologies is significantly enhancing user convenience and control over their medication administration

- For instance, smart auto injectors are increasingly being developed with connectivity options such as Bluetooth, allowing patients to track their injections and dosage, and enabling healthcare professionals to monitor adherence remotely. Some auto injectors, such as AUVI-Q, already incorporate voice guidance to assist users during critical situations, enhancing user confidence

- AI integration in auto injectors enables features such as improving the accuracy of drug delivery, potentially personalizing treatments based on individual patient needs, and providing more intelligent alerts based on usage data. While full AI-powered auto injectors are still emerging, research is exploring their potential for real-time monitoring and timely interventions

- The seamless integration of auto injectors with digital health platforms and mobile applications facilitates centralized control over various aspects of medication management. Through a single interface, users can manage their injection schedules, receive reminders, and share data with healthcare providers, creating a unified and supportive treatment experience

- This trend towards more intelligent, intuitive, and interconnected drug delivery systems is fundamentally reshaping user expectations for home healthcare. Consequently, companies are developing AI-enabled auto injectors with features such as automatic adjustments for precise delivery, real-time data tracking, and user-friendly interfaces

- The demand for auto injectors that offer seamless AI and voice control integration (or similar smart features) is growing rapidly across both hospital and home healthcare sectors, as patients and clinicians increasingly prioritize convenience and comprehensive smart health functionality

Auto Injectors Market Dynamics

Driver

“Growing Need Due to Rising Chronic Diseases and Preference for Self-Administration”

- The increasing prevalence of chronic diseases among a growing global population, coupled with the accelerating demand for convenient and self-administered medical interventions, is a significant driver for the heightened demand for auto injectors

- For instance, in October 2023, Eli Lilly and Company announced the launch of a new auto injector for a specific diabetes medication, designed for improved patient ergonomics and ease of use. Such strategies by key companies are expected to drive the auto injectors industry growth in the forecast period

- As patients become more aware of the critical need for effective and timely medication delivery and seek enhanced treatment adherence, auto injectors offer features such as pre-filled doses, built-in safety mechanisms, and clear instructions, providing a compelling upgrade over traditional syringe-and-needle methods

- Furthermore, the growing sophistication of biologics and biosimilars requiring precise and patient-friendly administration, alongside the desire for interconnected patient adherence monitoring systems, are making auto injectors an integral component of these treatment regimens, offering seamless integration with digital health platforms

- The convenience of self-administration for chronically ill patients, remote monitoring capabilities, and the ability to manage complex drug regimens through integrated smart systems are key factors propelling the adoption of auto injectors in both hospital and home healthcare sectors. The trend towards improved patient experience and the increasing availability of user-friendly auto injectors options further contributes to market growth

Restraint/Challenge

“Concerns Regarding Device Complexity and High Implementation Costs”

- Concerns surrounding the complexity of some advanced auto injectors and the potential for user error, pose a significant challenge to broader market penetration. As these devices integrate more features and technologies, they can be susceptible to incorrect usage if not accompanied by clear instructions and proper training, raising anxieties among patients and caregivers about the safety of their medication administration

- For instance, anecdotal reports of patients struggling with multi-step injection processes or understanding indicator lights have made some hesitant to fully embrace the most advanced auto injector solutions

- Addressing these usability concerns through intuitive designs, comprehensive patient education programs, and standardized training protocols is crucial for building user confidence. Companies such as Ypsomed Holding and SHL Medical AG emphasize user-friendly designs and extensive training resources in their marketing to reassure potential users

- In addition, the relatively high initial cost of some advanced auto injectors systems compared to traditional manual syringes can be a barrier to adoption for resource-constrained healthcare systems or for patients without adequate insurance coverage. While more basic disposable auto injectors have become more affordable, premium features such as connectivity, dose tracking, or advanced safety mechanisms often come with a higher price tag

- While prices are gradually decreasing, the perceived premium for advanced auto injector technology can still hinder widespread adoption, especially for those who do not see an immediate need for the most sophisticated features offered

- Overcoming these challenges through enhanced device usability, comprehensive patient education on best practices, and the development of more affordable auto injectors options will be vital for sustained market growth

Auto Injectors Market Scope

The market is segmented on the basis of therapy, type, end-user, route of administration, type of molecule, design, and product.

By Therapy

On the basis of therapy, the auto injectors market is segmented into rheumatoid arthritis, multiple sclerosis, diabetes, anaphylaxis, and other therapies. The diabetes segment dominates the largest market revenue share, with 31.32%, driven by the increasing global incidence of diabetes and the high demand for self-administered insulin. Auto injectors provide convenience and enhance medication adherence for a large patient population managing this chronic condition.

The anaphylaxis segment is anticipated to witness the fastest growth rate, fueled by the rising awareness of life-threatening allergic reactions and the critical need for immediate epinephrine administration. Increased patient education and the widespread availability of epinephrine auto injectors contribute to this segment's rapid expansion.

By Type

On the basis of type, the auto injectors market is segmented into disposable auto injectors and reusable auto injectors. The disposable auto injectors segment dominates the largest market revenue share with 35.6% share, driven by their convenience, ease of use, and minimized risk of cross-contamination, making them a preferred choice for single-dose injections.

The reusable auto injectors segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing patient preference for cost-effectiveness, sustainability, and advancements in reusable device designs that offer multiple doses and better control.

By End-User

On the basis of end-user, the auto injectors market is segmented into home care settings, hospitals and clinics, and ambulatory surgical centers. The home care settings segment held the largest market revenue share, driven by the growing trend of self-administration for chronic disease management and the convenience auto injectors offer in a home environment, reducing the need for frequent clinic visits.

The ambulatory surgical centers segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the increasing number of outpatient procedures and minor surgeries where auto injectors can be effectively utilized for pre-operative and post-operative medication administration, enhancing efficiency and patient comfort.

By Route of Administration

On the basis of route of administration, the auto injectors market is segmented into subcutaneous and intramuscular. The subcutaneous segment dominates the largest market revenue share, primarily due to the ease of self-administration for subcutaneous injections, which are less painful and can be given in various body parts, making them ideal for patient convenience.

The intramuscular segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the increasing development of drugs that require intramuscular delivery for optimal absorption and efficacy, particularly in emergency situations or for certain therapeutic applications.

By Type of Molecule

On the basis of type of molecule, the auto injectors market is segmented into monoclonal antibody, peptide, protein, and small molecule. The protein segment accounted for the largest market revenue share. This is largely due to the increasing development and approval of protein-based biologics for a wide range of chronic diseases.

The peptide segment is anticipated to witness the fastest CAGR from 2025 to 2032, fueled by the growing research and development in peptide therapeutics, which often require precise and convenient self-injection.

By Design

On the basis of design, the auto injectors market is segmented into standardized and customized. The standardized segment held the largest market revenue share in 2024, driven by the economies of scale in manufacturing, broader applicability across various drug types, and established regulatory pathways for standard designs.

The customized segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the increasing demand for patient-centric solutions, personalized medicine, and specific drug formulations that require tailored auto injector designs for optimal delivery and patient adherence.

By Product

On the basis of product, the auto injectors market is segmented into prefilled and fillable. The prefilled segment held the largest market revenue share. This is driven by their user-friendly design, convenience, and reduced risk of dosing errors, directly enhancing patient adherence and safety.

The fillable segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the flexibility it offers to healthcare professionals for customizing dosing regimens and the potential for cost-effectiveness for patients requiring multiple medication types or varying doses.

Auto Injectors Market Regional Analysis

- North America dominates the auto injectors market with the largest revenue share of 49.7% in 2024, driven by a growing demand for advanced medical care, a high adoption rate of sophisticated medical devices, and a high prevalence of chronic diseases such as diabetes, anaphylaxis, and rheumatoid arthritis

- Consumers and healthcare providers in the region highly value the effectiveness, advanced features for patient safety, and seamless integration offered by auto injectors within comprehensive healthcare systems, particularly for self-administration of biologics and biosimilars

- This widespread adoption is further supported by high healthcare expenditure, a technologically advanced medical community, favorable reimbursement policies, and the increasing preference for self-management of chronic conditions, establishing auto injectors as a favored solution for both hospital and home healthcare settings

Auto Injectors Market Regional Analysis

U.S. Auto Injectors Market Insight

The U.S. auto injectors market captured the largest revenue share of 30.03% or a significant portion of North America's auto-injector industry in 2024, fueled by the swift uptake of advanced medical technologies and the expanding trend of patient care. Healthcare and emergency medical services are increasingly prioritizing the enhancement of patient safety and treatment efficacy through intelligent, integrated auto injection solutions. The growing preference for convenient self-administration techniques, combined with robust demand for advanced monitoring and portable devices, further propels the auto injectors industry. Moreover, the increasing integration of sophisticated software and connectivity features is significantly contributing to the market's expansion.

Europe Auto Injectors Market Insight

The European auto injectors market is projected to expand at a substantial CAGR of around 17.4% from 2025 to 2032, primarily driven by stringent healthcare regulations and the escalating need for self-administered medication in hospitals and homecare settings. The increase in the aging population, coupled with the demand for user-friendly medical devices for chronic conditions, is fostering the adoption of advanced auto injection technologies. European healthcare providers are also drawn to the enhanced patient outcomes and safety features these devices offer. The region is experiencing significant growth across hospital intensive care units, emergency rooms, and home healthcare applications, with auto injectors being incorporated into both new healthcare facilities and upgrades of existing ones.

U.K. Auto Injectors Market Insight

The U.K. auto injectors market is anticipated to grow at a noteworthy CAGR during 2025-2032, driven by the escalating trend of home healthcare practices and a desire for heightened patient safety and treatment effectiveness. In addition, concerns regarding chronic disease management and the need for convenient drug delivery solutions are encouraging both hospitals and homecare providers to choose advanced auto injection technologies. The UK’s embrace of technological advancements in healthcare, alongside its robust healthcare infrastructure, is expected to continue to stimulate market growth.

Germany Auto Injectors Market Insight

The German auto injectors market is expected to expand at a considerable CAGR from 2025 to 2032, fueled by increasing awareness of self-care and the demand for technologically advanced, patient-centric solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation and patient safety, promotes the adoption of advanced auto injector devices, particularly in hospital and specialized care settings. The integration of auto injectors with patient monitoring systems is also becoming increasingly prevalent, with a strong preference for secure, reliable solutions aligning with local healthcare standards.

Asia-Pacific Auto Injectors Market Insight

The Asia-Pacific auto injectors market is poised to grow at the fastest CAGR of 8.9% from 2025 to 2032, driven by increasing healthcare investments, rising disposable incomes, and technological advancements in countries such as China, Japan, and India. The region's growing inclination towards self-care and advanced drug delivery, supported by government initiatives promoting healthcare modernization, is driving the adoption of advanced auto injector devices. Furthermore, as APAC emerges as a manufacturing hub for medical device components and systems, the affordability and accessibility of certain auto injector technologies are expanding to a wider healthcare base.

Japan Auto Injectors Market Insight

The Japan auto injectors market is gaining momentum due to the country’s high-tech culture, rapid aging population, and demand for convenient healthcare solutions. The Japanese market places a significant emphasis on patient safety and comfort, and the adoption of advanced auto injector devices is driven by the increasing number of elderly patients and complex medical cases requiring self-administration. The integration of auto injectors with other medical IoT devices and monitoring systems is fueling growth. Moreover, Japan's aging population is likely to spur demand for easier-to-use, reliable drug delivery solutions in both hospital and homecare sectors.

India Auto Injectors Market Insight

The India auto injectors market accounted for a significant market revenue share in Asia Pacific in 2024, attributed to the country's expanding middle class, rapid urbanization, and increasing healthcare awareness and access. The growing demand for medical care, coupled with increasing investments in healthcare infrastructure and the rising prevalence of chronic diseases such as diabetes and anaphylaxis, is driving the adoption of advanced auto injector devices in hospitals and home care settings across India. The push towards self-management of health and the increasing availability of medical device options are key factors propelling the market in India, with a CAGR of 15.92% from 2025 to 2032.

Auto Injectors Market Share

The auto injectors industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Viatris Inc. (U.S.)

- Lilly (U.S.)

- Amgen Inc. (U.S.)

- YPSOMED (Switzerland)

- BD (U.S.)

- Owen Mumford Limited (U.K.)

- SHL Medical (Switzerland)

- Johnson Medtech (U.S.)

- Teva Pharmaceuticals Industries Ltd. (U.S.)

- AstraZeneca (U.K.)

- Union Medico Inc. (Denmark)

- Gerresheimer AG (Germany)

- West Pharmaceutical Services, Inc. (U.S.)

- EMERGENT (U.S.)

- Halozyme, Inc. (U.S.)

- Stevanato Group S.p.a. (Italy)

- SMC Ltd (U.S.)

- Nemera (France)

Latest Developments in Global Auto Injectors Market

- In November 2023, Teva Pharmaceuticals USA, Inc., a U.S. affiliate of Teva Pharmaceutical Industries Ltd., announced the approval of a generic version of Forteo (teriparatide) in the United States, expanding accessible options for osteoporosis treatment via auto injector

- In May 2023, Coherus BioSciences, a leading global biosimilar company, announced the commercial launch of UDENYCA (pegfilgrastim-cbqv) in a single-dose prefilled auto-injector package in the U.S. market. This biosimilar is administered the day following chemotherapy to reduce the risk of infection. Similarly, Boehringer Ingelheim also commercially launched a new autoinjector option for its interchangeable biosimilar to Humira, Cyltezo Pen, in the U.S. marketplace

- In April 2023, Ypsomed Holding AG (Switzerland) opened a production facility in the Changzhou National Hi-tech District in China to cater to the rapidly growing Chinese market for injection systems, demonstrating strategic expansion to meet global demand for auto injectors

- In January 2023, Novo Nordisk signed a long-term supply agreement with Ypsomed for the delivery of auto injectors for its GLP-1 drugs, highlighting the increasing demand for auto injectors for chronic conditions such as diabetes and obesity

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.