Circumvent the Tariff challenges with an agile supply chain Consulting

Supply Chain Ecosystem Analysis now part of DBMR Reports

Global Atherectomy Systems Market

Market Size in USD Billion

CAGR :

%

USD

640.15 Million

USD

1,083.57 Million

2024

2032

Forecast Period

2025 –2032

Market Size(Base Year)

USD

640.15 Million

Market Size (Forecast Year)

USD

1,083.57 Million

CAGR

%

Major Markets Players

BD

Medtronic

Koninklijke Philips N.V.

Cardinal Health.

Cardiovascular SystemsInc.

Global Atherectomy Systems Market Segmentation, By Product (Directional Atherectomy, Orbital Atherectomy, Photo-Ablative (Laser) Atherectomy, Rotational Atherectomy and Support Devices), Application (Peripheral Vascular, Cardiovascular, Neurovascular and Others), End User (Hospitals and Surgical Centres, Ambulatory Care Centres, Research Laboratories and Academic Institutes and Others) - Industry Trends and Forecast to 2032

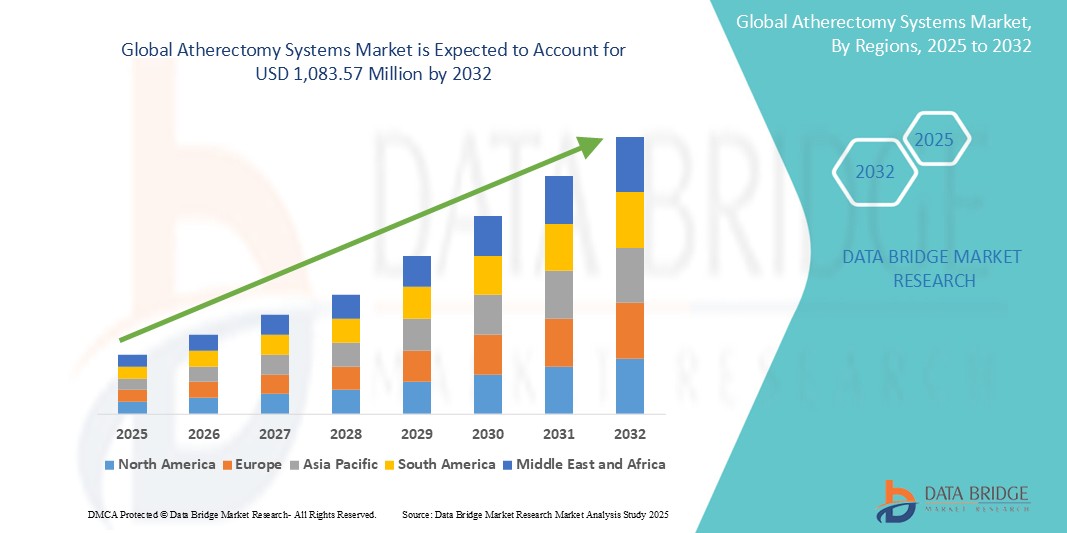

Atherectomy Systems Market Size

The global atherectomy systems market size was valued at USD 640.15 million in 2024 and is expected to reach USD 1,083.57 million by 2032,at a CAGR of 6.8% during the forecast period

The market growth is largely fueled by the increasing prevalence of peripheral artery disease (PAD) and coronary artery disease (CAD), the growing aging population susceptible to arterial blockages, and technological advancements in device design and functionality, leading to enhanced patient outcomes in cardiovascular interventions

Furthermore, rising demand for minimally invasive endovascular procedures, coupled with the need for effective and safe plaque removal during critical cardiac and peripheral interventions, is establishing atherectomy systems as essential tools for interventional cardiologists and radiologists. These converging factors are accelerating the uptake of atherectomy systems solutions, thereby significantly boosting the industry's growth

Atherectomy Systems Market Analysis

Atherectomy systems, providing essential tools for removing plaque from arteries during minimally invasive cardiovascular procedures, are increasingly critical components of modern healthcare settings, including hospitals, specialty clinics, and ambulatory surgical centers, due to their vital role in ensuring patient safety and effective treatment of arterial diseases

The escalating demand for atherectomy systems is primarily fueled by the growing prevalence of peripheral artery disease (PAD) and coronary artery disease (CAD), the increasing number of interventional procedures, and the rising need for effective plaque removal in complex arterial lesions

North America dominates the atherectomy systems market with the largest revenue share of 42.7% in 2024, characterized by advanced healthcare infrastructure, high adoption rates of sophisticated medical devices, and a strong presence of leading medical device manufacturers

Asia-Pacific is expected to be the fastest-growing region in the atherectomy systems market during the forecast period, with an anticipated CAGR of 9.5%, due to increasing healthcare expenditure, a growing aging population susceptible to cardiovascular ailments, and rising awareness of advanced atherectomy techniques in rapidly developing healthcare systems

Orbital atherectomy devices segment dominates the largest market revenue share of 34.1% in 2024, driven by its effectiveness in treating calcified lesions and its ability to prepare vessels for optimal stent placement, making it a preferred choice among clinicians for a wide range of arterial interventions

Report Scope and Atherectomy Systems Market Segmentation

Attributes

Atherectomy Systems Key Market Insights

Segments Covered

By Product: Directional Atherectomy, Orbital Atherectomy, Photo-Ablative (Laser) Atherectomy, Rotational Atherectomy and Support Devices

By Application: Peripheral Vascular, Cardiovascular, Neurovascular and Others

By End User: Hospitals and Surgical Centres, Ambulatory Care Centres, Research Laboratories and Academic Institutes and Others

Technological Advancements and Integration with Advanced Imaging

Growing Adoption in Ambulatory Surgical Centers (ASCs) and Outpatient Settings

Value Added Data Infosets

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.

Atherectomy Systems Market Trends

“Enhanced Precision Through AI and Robotics Integration”

A significant and accelerating trend in the global atherectomy systems market is the deepening integration with artificial intelligence (AI) and robotic-assisted systems. This fusion of technologies is significantly enhancing procedural precision and control over arterial plaque removal

For instance, advanced atherectomy systems are increasingly incorporating AI-driven imaging technologies, allowing clinicians to visualize and target plaque with unprecedented accuracy. Robotic-assisted interventions are enabling more stable and controlled navigation of catheters, reducing human error and improving procedural efficiency

AI integration in atherectomy devices enables features such as automated lesion characterization, real-time feedback on plaque removal, and predictive analytics for potential complications. Some systems utilize AI to improve the accuracy of identifying critical anatomical features and optimizing device positioning during complex procedures. Furthermore, robotic control capabilities offer clinicians enhanced dexterity and remote operation, allowing for more precise and less invasive interventions

The seamless integration of atherectomy systems with digital imaging platforms and broader interventional suites facilitates centralized control over various aspects of the procedure. Through a unified interface, clinicians can manage device settings, view real-time data, and assess treatment progress, creating a more cohesive and optimized procedural experience

This trend towards more intelligent, intuitive, and interconnected interventional systems is fundamentally reshaping clinician expectations for cardiovascular treatments. Consequently, companies are developing AI-enabled atherectomy devices with features such as real-time plaque assessment, automated adjustments based on lesion characteristics, and integration with robotic platforms for enhanced control

The demand for atherectomy systems that offer seamless AI and robotic integration is growing rapidly across hospitals and specialized centers, as clinicians increasingly prioritize precision, improved outcomes, and reduced procedural risks

Atherectomy Systems Market Dynamics

Driver

“Growing Need Due to Rising Prevalence of Cardiovascular Diseases and Minimally Invasive Procedures”

The increasing prevalence of cardiovascular diseases (CVDs), particularly peripheral artery disease (PAD) and coronary artery disease (CAD), among a growing global population, coupled with the accelerating demand for minimally invasive interventions, is a significant driver for the heightened demand for atherectomy systems

For instance, in February 2023, Abbott announced the acquisition of Cardiovascular Systems, Inc., a medical device company specializing in atherectomy systems. Such strategic initiatives by key companies are expected to drive the atherectomy systems industry growth in the forecast period

As healthcare providers become more aware of the critical need for effective plaque removal and seek enhanced patient outcomes, advanced atherectomy devices offer features such as sophisticated ablation modes, real-time imaging, and integrated safety mechanisms, providing a compelling upgrade over traditional surgical methods

Furthermore, the growing sophistication of endovascular procedures and cardiac catheterization laboratories, alongside the desire for interconnected patient monitoring systems, are making advanced atherectomy devices an integral component of these systems, offering seamless integration with other medical devices and platforms

The convenience of minimally invasive options, shorter recovery times for patients, and the ability to treat complex lesions through integrated hospital systems are key factors propelling the adoption of advanced atherectomy devices in both hospital and ambulatory surgical centers. The trend towards early intervention for arterial blockages and the increasing availability of user-friendly atherectomy systems options further contribute to market growth

Restraint/Challenge

“Concerns Regarding Device Complexity and High Implementation Costs”

Concerns surrounding the complexity of advanced atherectomy devices and the potential for user error or complications, pose a significant challenge to broader market penetration. As these devices rely on intricate settings and specialized techniques, they can be susceptible to incorrect usage and may require extensive training, raising anxieties among healthcare professionals about patient safety and procedural efficacy

For instance, high-profile reports of adverse events related to procedural complications, while rare, can make some clinicians hesitant to fully embrace the most advanced atherectomy solutions, especially for less experienced operators

Addressing these usability concerns through intuitive interfaces, comprehensive training programs, and standardized protocols is crucial for building clinician trust. Companies such as Boston Scientific Corporation and Medtronic emphasize user-friendly designs and extensive training resources in their marketing to reassure potential buyers

In addition, the relatively high initial cost of some advanced atherectomy systems compared to alternative therapies like balloon angioplasty or stenting can be a barrier to adoption for resource-constrained healthcare facilities, particularly in developing regions or for budget-conscious hospitals. While some devices have become more affordable, premium features such as advanced imaging integration or specialized cutting mechanisms often come with a higher price tag

While prices are gradually decreasing, the perceived premium for advanced atherectomy technology can still hinder widespread adoption, especially for those who do not see an immediate need for the most sophisticated features offered

Overcoming these challenges through enhanced device usability, comprehensive clinician education on best practices, and the development of more affordable atherectomy systems options will be vital for sustained market growth

Atherectomy Systems Market Scope

The market is segmented on the basis of product, application, and end user.

By Product

On the basis of product, the atherectomy systems market is segmented into directional atherectomy, orbital atherectomy, photo-ablative (laser) atherectomy, rotational atherectomy, and support devices. Orbital atherectomy devices segment dominates the largest market revenue share of 34.1% in 2024, driven by its effectiveness in treating calcified lesions and its ability to prepare vessels for optimal stent placement, making it a preferred choice among clinicians for a wide range of arterial interventions

The rotational atherectomy is expected to witness the fastest CAGR from 2025 to 2032, driven by technological advancements leading to improved device efficacy, safety, and broader applications in treating arterial blockages.

By Application

On the basis of application, the atherectomy systems market is segmented into peripheral vascular, cardiovascular, neurovascular, and others. The peripheral vascular segment held the largest market revenue share in 2024 of, driven by the high prevalence of peripheral artery disease (PAD) affecting over 200 million people globally, making it the largest application segment.

The cardiovascular applications is expected to witness the fastest CAGR from 2025 to 2032 atherectomy device market, primarily driven by increasing cases of coronary artery disease (CAD).

By End User

On the basis of end user, the atherectomy systems market is segmented into hospitals and surgical centers, ambulatory care centers, research laboratories and academic institutes, and others. The hospitals and surgical centers segment accounted for the largest market revenue share in 2024 and is anticipated to hold a prominent market share in 2024, driven by the high volume of procedures performed, the availability of advanced medical infrastructure, and the concentration of critical care units and operating rooms.

The ambulatory care centers segment is expected to witness the fastest growth, fueled by the increasing shift towards outpatient procedures and the advantages of reduced trauma, faster recovery, and lower complication rates in these settings.

Atherectomy Systems Market Regional Analysis

North America dominates the atherectomy systems market with the largest revenue share of 42.7% in 2024, driven by a growing demand for advanced medical care, a high adoption rate of sophisticated medical devices, and a significant prevalence of peripheral artery disease (PAD) and coronary artery disease (CAD)

Consumers and healthcare providers in the region highly value the effectiveness, advanced features for patient safety, and seamless integration offered by advanced atherectomy devices within comprehensive healthcare systems, particularly for minimally invasive interventions

This widespread adoption is further supported by high healthcare expenditure, a technologically advanced medical community, favorable reimbursement policies for atherectomy procedures, and the increasing preference for precise plaque removal and improved patient outcomes, establishing atherectomy systems as a favored solution in hospital and ambulatory surgical settings

U.S. Atherectomy Systems Market Insight

The U.S. atherectomy systems market captured the largest revenue share within North America, of 42.5% in 2024, fueled by the swift uptake of advanced medical technologies and the expanding trend of patient care. Healthcare providers are increasingly prioritizing the enhancement of patient safety and treatment efficacy through intelligent, integrated atherectomy solutions. The growing preference for minimally invasive procedures for treating cardiovascular and peripheral artery diseases, combined with robust demand for advanced imaging and precise plaque removal devices, further propels the Atherectomy Systems industry. Moreover, the increasing integration of sophisticated software and connectivity features is significantly contributing to the market's expansion.

Europe Atherectomy Systems Market Insight

The European atherectomy systems market is projected to expand at a substantial CAGR of approximately 6.7% from 2025 to 2032, primarily driven by stringent healthcare regulations and the escalating need for effective treatment of cardiovascular and peripheral artery diseases in hospitals and specialized care settings. The increase in the aging population, coupled with the demand for advanced medical devices, is fostering the adoption of atherectomy technologies. European healthcare providers are also drawn to the enhanced patient outcomes and safety features these devices offer. The region is experiencing significant growth across hospital interventional cardiology units, vascular surgery centers, and cardiology clinics, with advanced atherectomy devices being incorporated into both new healthcare facilities and upgrades of existing ones.

U.K. Atherectomy Systems Market Insight

The U.K. atherectomy systems market is anticipated to grow at a noteworthy CAGR of approximately 7.5% from 2020 to 2026, driven by the escalating trend of minimally invasive healthcare practices and a desire for heightened patient safety and treatment effectiveness. In addition, concerns regarding arterial blockages and the need for effective plaque removal solutions are encouraging both hospitals and specialized care providers to choose advanced atherectomy technologies. The UK’s embrace of technological advancements in healthcare, alongside its robust healthcare infrastructure, is expected to continue to stimulate market growth.

Germany Atherectomy Systems Market Insight

The German atherectomy systems market is expected to expand at a considerable CAGR of 8.1%, fueled by increasing awareness of advanced cardiovascular care and the demand for technologically advanced, patient-centric solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation and patient safety, promotes the adoption of advanced atherectomy devices, particularly in hospital and specialized care settings. The integration of atherectomy devices with patient monitoring systems is also becoming increasingly prevalent, with a strong preference for secure, reliable solutions aligning with local healthcare standards.

Asia-Pacific Atherectomy Systems Market Insight

The Asia-Pacific atherectomy systems market is poised to grow at the fastest CAGR of 9.5%, driven by increasing healthcare investments, rising disposable incomes, and technological advancements in countries such as China, Japan, and India. The region's growing inclination towards advanced cardiovascular interventions, supported by government initiatives promoting healthcare modernization, is driving the adoption of advanced atherectomy devices. Furthermore, as APAC emerges as a manufacturing hub for medical device components and systems, the affordability and accessibility of certain atherectomy technologies are expanding to a wider healthcare base.

Japan Atherectomy Systems Market Insight

The Japan atherectomy systems market is gaining momentum due to the country’s high-tech culture, rapid aging population, and demand for advanced healthcare solutions. The Japanese market places a significant emphasis on patient safety and comfort, and the adoption of advanced atherectomy devices is driven by the increasing number of elderly patients and complex medical cases requiring precise plaque removal. The integration of atherectomy devices with other medical IoT devices and monitoring systems is fueling growth. Moreover, Japan's aging population is likely to spur demand for highly precise, reliable interventional solutions in hospitals and specialized centers.

China Atherectomy Systems Market Insight

The China atherectomy systems market expected to witness the highest compound annual growth rate in Asia Pacific in 2024 with 12.3%, due to increasing healthcare investments, a rising prevalence of cardiovascular diseases, a growing aging population, and increasing access to advanced medical technologies. The expanding healthcare sector and rising awareness of minimally invasive cardiovascular procedures are key factors driving this growth.

Atherectomy Systems Market Share

The atherectomy systems industry is primarily led by well-established companies, including:

Latest Developments in Global Atherectomy Systems Market

In April 2024, Otsuka Medical Devices Co., Ltd. announced a definitive agreement to transfer the distribution of the Diamondback 360 Coronary Orbital Atherectomy System (OAS) in Japan to Abbott Medical Japan LLC. This strategic move aims to expand the market reach of the Diamondback 360 system by leveraging Abbott's established distribution network

In November 2024, Philips announced the enrollment of the first patient in the U.S. THOR IDE clinical trial, evaluating a combined laser atherectomy and intravascular lithotripsy catheter. This innovative device aims to simplify peripheral artery disease (PAD) treatment by integrating two therapies into a single procedure, potentially reducing procedural complexity and improving patient outcomes

In November 2024, Medtronic announced results from two studies evaluating the utility of atherectomy for peripheral endovascular interventions, presented as late-breaking data presentations at VIVA 2024. These studies added to the body of research demonstrating the safety and effectiveness of atherectomy as a treatment for peripheral arterial disease

In October 2023, Cardio Flow announced it received US Food and Drug Administration (FDA) 510(k) clearance for the company's FreedomFlow orbital atherectomy peripheral platform, expanding the available treatment options for peripheral arterial disease.

In February 2023, the FDA issued an early alert about potential risks associated with the Rotarex Atherectomy Systems (Bard Peripheral Vascular), specifically concerning helix fracture or breakage. This highlights the ongoing need for device vigilance and adherence to updated instructions for safe use.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

Interactive Data Analysis Dashboard

Company Analysis Dashboard for high growth potential opportunities

Research Analyst Access for customization & queries

Competitor Analysis with Interactive dashboard

Latest News, Updates & Trend analysis

Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.

Frequently Asked Questions

Who are major players in atherectomy systems market?

Companies such as BD (U.S.), Medtronic (Ireland), Koninklijke Philips N.V. (Netherlands), Cardinal Health (U.S.) and Boston Scientific Corporation (U.S.) are major players in atherectomy systems market.

What are the recent product launches by major companies in the atherectomy systems market?

In April 2024, Otsuka Medical Devices Co., Ltd. announced a definitive agreement to transfer the distribution of the Diamondback 360 Coronary Orbital Atherectomy System (OAS) in Japan to Abbott Medical Japan LLC. This strategic move aims to expand the market reach of the Diamondback 360 system by leveraging Abbott's established distribution network

Which countries data is covered in the atherectomy systems market?

The countries covered in the atherectomy systems market are U.S., Canada, Mexico, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, rest of Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, rest of Asia-Pacific, Brazil, Argentina, rest of South America, Saudi Arabia, U.A.E., South Africa, Egypt, Israel, and rest of Middle East and Africa.

Claudio Rondena

Group Business Development & Strategic Marketing Director, C.O.C Farmaceutici SRL

"This morning we were involved in the first part, the data presentation of MKT analysis, selected abstract from your work. The board team was really impressed and very appreciated, as well."

David Manning - Thermo Fisher Scientific

Director, Global Strategic Accounts,

Dear Ricky, I want to thank you for the excellent market analysis (LIMS INSTALLED BASE DATA) that you and your team delivered, especially end of year on short notice.

Sachin and Shraddha captured the requirements, determined their path forward and executed quickly.

You, Sachin and Shraddha have been a pleasure to work with – very responsive, professional and thorough.

Your work is much appreciated.

Manager - Market Analytics,

Uriah D. Avila - Zeus Polymer Solutions

Thank you for all the assistance and the level of detail in the market report. We are very pleased with the results and the customization. We would like to continue to do business.

Business Development Manager,

(Pharmaceuticals Partner for Nasal Sprays) | Renaissance Lakewood LLC

DBMR was attentive and engaged while discussing the Global Nasal Spray Market. They understood what we were looking for and was able to provide some examples from the report as requested. DBMR Service team has been responsive as needed. Depending on what my colleagues were looking for, I will recommend your services and would be happy to stay connected in case we can utilize your research in the future.

Business Intelligence and Analytics,

Ipsen Biopharm Limited

We are impressed by the CENTRAL PRECOCIOUS PUBERTY (CPP) TREATMENT report - so a BIG thanks to you colleagues.

Competition Analyst,

Basler Web

I just wanted to share a quick note and let you know that you guys did a really good job. I’m glad I decided to work with you. I shall continue being associated with your company as long as we have market intelligence needs.

Marketing Director,

Buhler Group

It was indeed a good experience, would definitely recommend and come back for future prospects.

COO,

A global leader providing Drug Delivery Services

DBMR did an outstanding job on the Global Drug Delivery project, We were extremely impressed by the simple but comprehensive presentation of the study and the quality of work done. This report really helped us to access untapped opportunities across the globe.

Marketing Director,

Philips Healthcare

The study was customized to our targets and needs with well-defined milestones. We were impressed by the in-depth customization and inclusion of not only major but also minor players across the globe. The DBMR Market position grid helped us to analyze the market in different dimension which was very helpful for the team to get into the minute details.

Product manager,

Fujifilms

Thankful to the team for the amazing coordination, and helping me at the last moment with my presentation. It was indeed a comprehensive report that gave us revenue impacting solution enabling us to plan the right move.

Investor relations,

GE Healthcare

Thank you for the report, and addressing our needs in such short time. DBMR has outdone themselves in this project with such short timeframe.

Market Analyst,

Medincell

We found the results of this study compelling and will help our organization validate a market we are considering to enter. Thank you for a job well done.

Andrew - Senior Global Marketing Manager,

Medtronic (US)

I want to thank you for your help with this report – It’s been very helpful in our business planning and it well organized.

Amarildo - Manager, Global Strategic Alignment

MasterCard

We believe the work done by Data Bridge Team for our requirements in the North America Loyalty Management Market was fantastic and would love to continue working with your team moving forward.

Tor Hammer

Green Nexus LLc

Thank you for your quick response to this unfortunate circumstance. Please extend my thanks to your reach team. I will be contacting you in the future with further projects

I acknowledge the difficulty given by the very short warning for this report, and I think that its quality and your delivering time have been very satisfying.

Obviously, as a provider Data Bridge Market Research will be considered as a plus for future needs of Nippon Gases.

Yuki Kopyl (Asian Business Development Department)

UENO FOOD TECHNO INDUSTRY, LTD. (JAPAN)

Xylose report was very useful for our team. Thank you very much & hope to work with you again in the future