Global Ascites Market

Market Size in USD Billion

CAGR :

%

USD

2.85 Billion

USD

4.05 Billion

2025

2033

USD

2.85 Billion

USD

4.05 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.85 Billion | |

| USD 4.05 Billion | |

| % | |

|

Ascites Market Overview

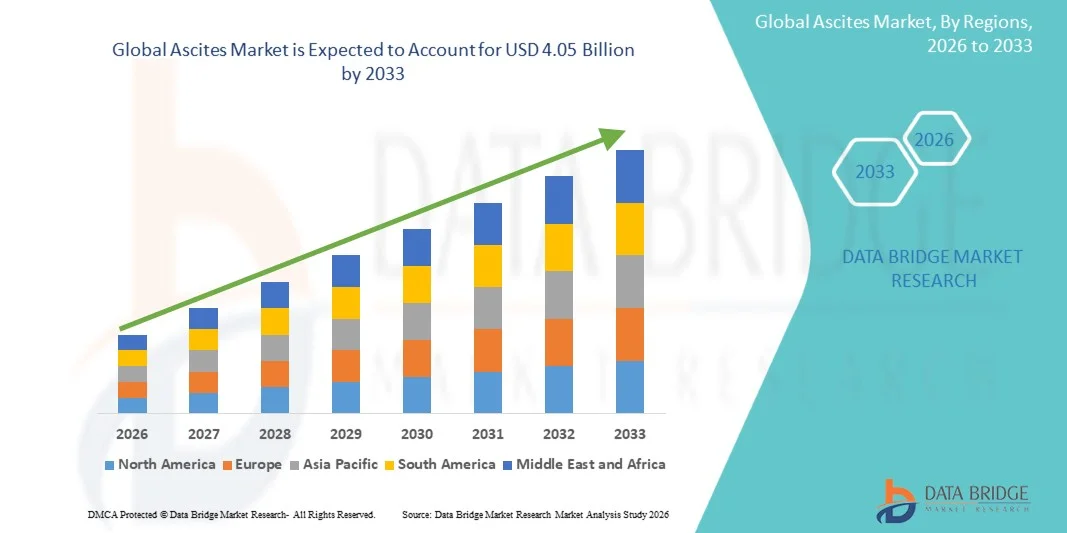

The Ascites Market was valued at USD 2.85 billion in 2025 and is projected to reach USD 4.05 billion by 2033, growing at a CAGR of 4.50% from 2026 to 2033. The market is witnessing steady growth driven by the increasing prevalence of chronic liver diseases, rising cases of cirrhosis and cancer-associated ascites, and growing demand for advanced diagnostic and therapeutic interventions.

The expanding burden of liver disorders, including alcoholic liver disease, hepatitis-related cirrhosis, and non-alcoholic steatohepatitis (NASH), is significantly contributing to the incidence of ascites worldwide. In addition, improvements in healthcare infrastructure, greater awareness of early disease management, and the adoption of minimally invasive treatment approaches such as paracentesis, indwelling peritoneal catheters, and targeted pharmacological therapies are supporting market expansion. Ongoing research focused on novel therapeutics and improved management strategies for refractory and recurrent ascites is further enhancing treatment outcomes and creating new growth opportunities across hospitals, specialty clinics, and ambulatory care settings.

Key Market Trends & Insights

- North America dominated the Ascites Market with the largest revenue share of 38.42% in 2025, supported by a high prevalence of liver diseases, advanced healthcare infrastructure, and strong adoption of specialized treatment procedures.

- The Transudative segment led the market with a 68.42% share in 2025, driven by the high prevalence of liver cirrhosis and portal hypertension, which remain the leading causes of ascites worldwide.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.4% from 2026 to 2033, fueled by rising incidences of chronic liver disorders, improving healthcare access, and expanding diagnostic capabilities across China, India, and Southeast Asia.

- Exudative are the fastest-growing type, projected to register a CAGR of 7.3%, reflecting the surge in incidence of malignancy-associated ascites, infections, and inflammatory disorders.

- The Ultrasound segment dominated the diagnosis category with a 36.85% revenue share in 2025, led by its widespread availability, cost-effectiveness, and ability to accurately detect even small volumes of ascitic fluid.

- Medication accounted for 47.63% of the market, preferred by the widespread use of diuretics as the standard first-line treatment for ascites management.

- The Parenteral segment is the fastest-growing route of administration category, with a CAGR of 7.0%, driven by the increasing use of injectable therapies in hospitalized and critically ill patients.

Market Size & Forecast

- Global Market Value (2025): USD 2.85 Billion

- Expected Market Value (2033): USD 4.05 Billion

- Forecast CAGR (2026–2033): 4.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Ascites Market Segmentation

|

Attributes |

Ascites Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Baxter (U.S.) · B. Braun SE (Germany) · Fresenius Kabi AG (Germany) · Terumo Corporation (Japan) · Boston Scientific Corporation (U.S.) · BD (U.S.) · Cook (U.S.) · Teleflex Incorporated (U.S.) · Cardinal Health, Inc. (U.S.) · Merit Medical Systems, Inc. (U.S.) · ConvaTec Group PLC (U.K.) · AngioDynamics, Inc. (U.S.) · Sequana Medical NV (Belgium) · ewimed GmbH (Germany) · BioVie Inc. (U.S.) · Madrigal Pharmaceuticals, Inc. (U.S.) · AbbVie Inc. (U.S.) · F. Hoffmann-La Roche Ltd (Switzerland) · Pfizer Inc. (U.S.) · AstraZeneca (U.K.) |

|

Market Opportunities |

· Expansion of targeted therapies for refractory ascites · Growing adoption of long-term fluid management solutions · Increasing prevalence of NASH-related cirrhosis worldwide |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Ascites Market Trends

Trend: Rising Adoption of Minimally Invasive Ascites Management Procedures

Healthcare providers are increasingly adopting minimally invasive procedures for ascites management to reduce hospital stays, improve patient comfort, and lower complication risks associated with repeated interventions. The growing use of image-guided paracentesis, tunneled peritoneal drainage catheters, and outpatient fluid management approaches enables more efficient treatment of recurrent ascites. Hospitals and specialty clinics are similarly incorporating standardized care pathways to enhance treatment outcomes, while advances in diagnostic imaging and monitoring technologies support earlier intervention and more personalized disease management strategies.

For instance, in March 2024, researchers and healthcare providers reported increased adoption of ultrasound-guided paracentesis protocols across major liver disease treatment centers, supporting safer and more effective ascites management.

Ascites Market Dynamics

Key Market Driver: Increasing Prevalence of Chronic Liver Diseases and Cirrhosis

The rising prevalence of chronic liver diseases and cirrhosis has created substantial demand for ascites diagnosis, monitoring, and treatment services as fluid accumulation remains one of the most common complications of advanced liver dysfunction. Hospitals, hepatology centers, and specialty clinics are expanding treatment capabilities to manage growing patient volumes, improve clinical outcomes, and reduce disease-related complications. The increasing burden of alcohol-related liver disease, viral hepatitis, and metabolic dysfunction-associated steatotic liver disease is further supporting demand for comprehensive ascites care worldwide.

For instance, in April 2024, global liver health organizations highlighted the continued increase in cirrhosis-related hospitalizations, reinforcing the need for effective ascites management and monitoring solutions.

Key Restraint/Challenge: Limited Long-Term Treatment Options for Refractory Ascites

A significant restraint in the Ascites Market is the limited availability of effective long-term treatment options for patients with refractory or recurrent disease. Current management strategies often rely on repeated paracentesis procedures, diuretic therapy, and supportive care, which may not adequately address underlying disease progression. The overall treatment burden extends to frequent hospital visits, risk of complications, and substantial healthcare costs, creating challenges for patients, providers, and healthcare systems seeking sustainable disease management approaches.

For instance, in January 2024, clinical studies continued to emphasize the high recurrence rates associated with refractory ascites, highlighting ongoing challenges in achieving durable long-term treatment outcomes.

Key Market Opportunity: Development of Novel Therapies and Disease-Modifying Treatments

The development of novel therapies for ascites management presents a significant market opportunity. Emerging treatment approaches can improve fluid control, reduce recurrence rates, and address underlying mechanisms associated with portal hypertension and liver dysfunction. The advancement of targeted biologics, innovative medical devices, and regenerative medicine strategies is further expanding therapeutic possibilities, opening growth opportunities across specialized hepatology centers, hospitals, and advanced healthcare markets worldwide.

For instance, in February 2024, multiple clinical programs evaluating innovative therapies for complications of advanced liver disease continued to progress, supporting future opportunities for improved ascites treatment and patient care.

Ascites Market Scope

The ascites market is segmented on the basis of type, diagnosis, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the Ascites Market is segmented into transudative, exudative, and others. The Transudative segment dominated the market with an estimated 68.42% share in 2025, owing to the high prevalence of liver cirrhosis and portal hypertension, which remain the leading causes of ascites worldwide. Transudative ascites is frequently diagnosed in patients with chronic liver disease, creating a substantial patient pool requiring ongoing monitoring and treatment. The segment benefits from increasing rates of alcohol-related liver disease and metabolic dysfunction-associated steatotic liver disease globally. Healthcare providers routinely manage transudative ascites through diuretics, paracentesis, and supportive care, supporting consistent demand for therapeutic interventions. Improved diagnostic capabilities are enabling earlier detection and disease management. The widespread burden of chronic liver disorders continues to reinforce the segment’s dominant position.

The Exudative segment is projected to register the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by increasing incidence of malignancy-associated ascites, infections, and inflammatory disorders. Rising global cancer prevalence is contributing significantly to the number of patients developing exudative ascites. Advanced diagnostic techniques are improving differentiation between exudative and transudative fluid accumulation, supporting targeted treatment approaches. Growing awareness among healthcare professionals regarding cancer-related complications is accelerating diagnosis rates. The segment is also benefiting from increasing oncology treatment volumes and improved survival rates among cancer patients. Expanding research into novel therapies for malignant ascites management is expected to further support market growth.

- By Diagnosis

On the basis of diagnosis, the Ascites Market is segmented into ultrasound, CT scan, MRI, blood test, laparoscopy, angiography, and others. The Ultrasound segment dominated the market with an estimated 36.85% share in 2025 due to its widespread availability, cost-effectiveness, and ability to accurately detect even small volumes of ascitic fluid. Ultrasound is commonly used as the first-line imaging modality for diagnosing and monitoring ascites in clinical practice. The technology offers real-time visualization without exposing patients to ionizing radiation. Its portability makes it highly suitable for use in hospitals, emergency departments, and outpatient settings. Continuous advancements in imaging quality are further improving diagnostic accuracy. The combination of accessibility, affordability, and clinical effectiveness supports its market leadership.

The MRI segment is anticipated to witness the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by increasing demand for advanced imaging techniques capable of providing detailed soft tissue characterization. MRI plays an important role in evaluating underlying liver diseases, malignancies, and complex abdominal conditions associated with ascites. Technological advancements are improving scan quality and reducing imaging times. Growing adoption of precision diagnostics and personalized treatment planning is supporting utilization. Increased healthcare investments in advanced imaging infrastructure are also contributing to growth. The modality’s superior diagnostic capabilities are expected to expand its use in specialized healthcare settings.

- By Treatment

On the basis of treatment, the Ascites Market is segmented into medication, paracentesis, surgery, and others. The Medication segment dominated the market with an estimated 47.63% share in 2025, driven by the widespread use of diuretics as the standard first-line treatment for ascites management. Medications help control fluid accumulation and reduce symptoms in a large proportion of patients with liver-related ascites. The segment benefits from established treatment guidelines and broad physician familiarity. Oral pharmacological therapies are generally more accessible and cost-effective than invasive procedures. Ongoing monitoring and long-term disease management further contribute to recurring medication demand. The extensive patient population requiring chronic treatment continues to sustain segment dominance.

The Paracentesis segment is expected to register the fastest growth at a CAGR of 7.5% from 2026 to 2033 due to increasing prevalence of refractory and recurrent ascites cases. Paracentesis provides rapid symptom relief through direct removal of excess fluid from the abdominal cavity. Growing preference for minimally invasive treatment options is accelerating adoption across healthcare facilities. Improvements in ultrasound-guided procedures are enhancing safety and clinical outcomes. The procedure is increasingly utilized in both inpatient and outpatient settings. Rising hospitalization rates for advanced liver disease are further supporting segment expansion.

- By Route of Administration

On the basis of route of administration, the Ascites Market is segmented into oral, parenteral, and others. The Oral segment held the largest market share of 61.27% in 2025 owing to the extensive use of oral diuretics and supportive medications for long-term ascites management. Oral therapies offer convenience, ease of administration, and improved patient compliance. Most patients diagnosed with ascites receive oral treatment as part of standard disease management protocols. The availability of established medications across healthcare systems supports widespread utilization. Lower treatment costs compared to injectable alternatives further contribute to segment leadership. Continuous demand for chronic therapy reinforces its dominant market position.

The Parenteral segment is projected to experience the fastest growth at a CAGR of 7.0% from 2026 to 2033, driven by increasing use of injectable therapies in hospitalized and critically ill patients. Parenteral administration enables rapid therapeutic effects and precise dosing control. Growing utilization of albumin infusions following large-volume paracentesis is significantly supporting demand. The segment is benefiting from increasing admissions for advanced liver disease and complications. Improved hospital treatment protocols are expanding the use of injectable supportive therapies. Rising focus on optimizing clinical outcomes in severe ascites cases is expected to sustain growth.

- By End-Users

On the basis of end-users, the Ascites Market is segmented into hospitals, homecare, specialty clinics, and others. The Hospitals segment dominated the market with a 52.36% share in 2025 due to the availability of comprehensive diagnostic, therapeutic, and emergency care services. Most patients with moderate to severe ascites receive treatment in hospital settings, particularly during episodes of disease progression or complications. Hospitals provide access to imaging technologies, paracentesis procedures, and multidisciplinary specialist care. The segment benefits from increasing hospitalization rates associated with chronic liver diseases and cancer-related ascites. Availability of skilled healthcare professionals further strengthens utilization. Hospitals remain the primary centers for advanced ascites management worldwide.

The Homecare segment is expected to witness the fastest growth at a CAGR of 7.4% from 2026 to 2033, supported by growing demand for patient-centered and cost-effective care models. Increasing use of long-term drainage systems and remote patient monitoring technologies is enabling treatment outside traditional healthcare facilities. Homecare services improve patient convenience and reduce hospital readmissions. Aging populations and rising chronic disease burdens are accelerating adoption. Healthcare systems are increasingly promoting home-based management to optimize resource utilization. Technological advancements in remote healthcare delivery continue to support segment growth.

- By Distribution Channel

On the basis of distribution channel, the Ascites Market is segmented into hospital pharmacy, retail pharmacy, online pharmacies, and others. The Hospital Pharmacy segment dominated the market with an estimated 49.18% share in 2025 owing to the high volume of ascites-related treatments administered within hospital settings. Hospital pharmacies ensure immediate access to essential medications, albumin products, and supportive therapies required for patient care. The segment benefits from strong integration with inpatient treatment pathways and specialist care programs. Healthcare professionals closely monitor medication use through hospital pharmacy networks. Increasing hospitalization rates for liver disease complications continue to support demand. Their critical role in managing acute and advanced cases reinforces market leadership.

The Online Pharmacies segment is projected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by increasing digitalization of healthcare services and growing consumer preference for convenient medication access. Online platforms offer home delivery services, competitive pricing, and improved accessibility for chronic disease patients. Expanding internet penetration and smartphone adoption are accelerating utilization globally. Regulatory improvements in digital healthcare ecosystems are supporting market development. The segment is also benefiting from increased use of telemedicine and remote prescription services. Growing patient preference for contactless healthcare solutions is expected to drive future growth.

Ascites Market Regional Analysis

North America dominated the Ascites Market with the largest revenue share of 38.42% in 2025, supported by a high prevalence of liver diseases, advanced healthcare infrastructure, and strong adoption of specialized treatment procedures. The region also benefits from strong healthcare expenditure, favorable reimbursement frameworks, and the presence of leading pharmaceutical and medical technology companies. Increasing adoption of minimally invasive procedures, growing awareness of liver disease complications, and rising utilization of advanced imaging technologies are supporting market growth. Ongoing clinical research activities and expanding access to innovative therapies for refractory ascites continue to strengthen North America’s leadership position in the global market.

U.S. Ascites Market Insight

The U.S. ascites market is witnessing strong growth due to rising prevalence of chronic liver diseases, increasing incidence of cirrhosis, and growing demand for advanced diagnostic and therapeutic solutions. The country’s well-established healthcare infrastructure, along with increasing adoption of minimally invasive procedures and specialized hepatology care, is driving demand across hospitals and specialty clinics. In addition, growing focus on early disease detection and effective management of liver-related complications is accelerating the adoption of advanced ascites treatment and monitoring approaches throughout the United States.

Europe Ascites Market Insight

The Europe ascites market remains a major contributor to global revenue, driven by strong healthcare systems, increasing awareness of liver disease management, and high demand for advanced treatment solutions. The widespread availability of specialized hepatology services, diagnostic imaging technologies, and evidence-based treatment protocols is supporting market expansion across the region. Increasing investments in healthcare modernization, coupled with growing prevalence of liver cirrhosis and cancer-related ascites, continue to enhance the adoption of ascites diagnosis and treatment solutions throughout Europe.

U.K. Ascites Market Insight

The U.K. ascites market is experiencing steady growth, supported by increasing incidence of chronic liver diseases, rising healthcare expenditure, and growing adoption of advanced disease management practices. Increasing investments in diagnostic infrastructure and growing demand for effective, patient-centered treatment solutions are contributing to market growth. Furthermore, integration of advanced imaging technologies and improved clinical care pathways is enhancing treatment outcomes and healthcare efficiency, positioning the U.K. as an important market within the ascites treatment industry.

Germany Ascites Market Insight

The Germany ascites market is expanding steadily due to the country’s advanced healthcare infrastructure, strong clinical research capabilities, and increasing focus on liver disease management. Hospitals, specialty clinics, and academic medical centers are increasingly utilizing advanced diagnostic and therapeutic approaches for ascites care. Continuous advancements in imaging technologies, minimally invasive procedures, and supportive care strategies, along with strong government focus on healthcare quality and innovation, are further driving market growth in Germany.

Asia-Pacific Ascites Market Insight

The Asia-Pacific ascites market is expected to witness rapid growth, driven by increasing prevalence of liver disorders, expanding healthcare infrastructure, and rising investments in disease diagnosis and treatment across countries such as China, India, and Japan. Growing awareness regarding liver health, rising adoption of advanced medical technologies, and increasing demand for accessible and cost-effective treatment solutions are supporting regional market expansion. In addition, improving healthcare access and growing patient populations are accelerating adoption of ascites management solutions across hospitals and specialty care centers.

Japan Ascites Market Insight

The Japan ascites market is witnessing consistent growth due to rising incidence of chronic liver diseases, increasing healthcare investments, and growing focus on advanced patient care. Healthcare providers, research institutions, and specialty treatment centers are increasingly adopting innovative diagnostic and therapeutic approaches for effective ascites management. Moreover, increasing utilization of minimally invasive procedures and the country’s emphasis on high-quality healthcare delivery are further contributing to market growth.

China Ascites Market Insight

The China ascites market is growing rapidly, driven by increasing prevalence of liver diseases, expanding healthcare infrastructure, and rising government focus on improving disease diagnosis and treatment accessibility. Growing adoption of advanced imaging technologies and minimally invasive treatment procedures across hospitals and specialty care facilities is significantly boosting market demand. In addition, rising healthcare investments, increasing awareness regarding liver disease complications, and rapid improvements in medical services are positioning China as one of the fastest-growing markets for ascites management globally.

Ascites Market Share

The ascites industry is primarily led by well-established companies, including:

- Baxter (U.S.)

- Braun SE (Germany)

- Fresenius Kabi AG (Germany)

- Terumo Corporation (Japan)

- Boston Scientific Corporation (U.S.)

- BD (U.S.)

- Cook (U.S.)

- Teleflex Incorporated (U.S.)

- Cardinal Health, Inc. (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- ConvaTec Group PLC (U.K.)

- AngioDynamics, Inc. (U.S.)

- Sequana Medical NV (Belgium)

- ewimed GmbH (Germany)

- BioVie Inc. (U.S.)

- Madrigal Pharmaceuticals, Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- Pfizer Inc. (U.S.)

- AstraZeneca (U.K.)

Latest Developments in Ascites Market

- In December 2024, Sequana Medical announced that the U.S. FDA approved the alfapump® System for the treatment of recurrent or refractory ascites due to liver cirrhosis. The alfapump became the first FDA-approved active implantable medical device designed to automatically transfer excess ascitic fluid from the abdominal cavity to the bladder, significantly reducing the need for repeated paracentesis procedures and offering a new long-term treatment option for patients with advanced liver disease

- In January 2024, Sequana Medical announced that the U.S. FDA accepted its Premarket Approval (PMA) application for substantive review of the alfapump® System for recurrent or refractory ascites caused by liver cirrhosis. The acceptance marked a significant regulatory milestone and initiated the formal review process for a novel implantable solution aimed at reducing the burden of repeated fluid drainage procedures in patients suffering from severe ascites

- In December 2023, Sequana Medical submitted a Premarket Approval application to the U.S. FDA for its alfapump® System intended to treat recurrent or refractory ascites due to liver cirrhosis. The submission was supported by data from the North American POSEIDON study and represented an important step toward introducing the first active implantable device in the United States specifically developed for continuous ascites management

- In June 2023, Sequana Medical presented additional findings from its North American pivotal POSEIDON study at the European Association for the Study of the Liver (EASL) Congress 2023. The results demonstrated that the alfapump system substantially reduced the need for therapeutic paracentesis, improved patient quality of life, and showed encouraging long-term safety and survival outcomes, highlighting its potential to transform the treatment landscape for refractory ascites

- In September 2021, Sequana Medical reported continued progress in the North American POSEIDON pivotal study, which evaluated the safety and effectiveness of the alfapump system in patients with recurrent or refractory ascites resulting from liver cirrhosis. The ongoing clinical development generated critical evidence supporting future regulatory submissions and reinforced growing interest in innovative device-based approaches for long-term ascites management

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.